Japan's Economic Depression Deepens, Protectionism Could Trigger Global Depression

Economics / Economic Depression Mar 15, 2009 - 01:28 AM GMTBy: John_Mauldin

Where Have My Earnings Gone?

Where Have My Earnings Gone?- The Land of the Setting Sun

- The Swiss Start Their Engines

- My One True Nightmare

This week we look at the Land of the Rising Sun. Japan is going through major upheavals, and they will have consequences all over the world. And what are those wild and crazy Swiss central bankers up to? It's time for another round of competitive devaluation. And of course I have to look at the recent Barron's cover story, about how stocks are cheap. There's a lot to cover.

But first, and quickly, I just wanted to take a moment and remind you to sign up for the Richard Russell Tribute Dinner, all set for Saturday, April 4 at the Manchester Grand Hyatt in San Diego - if you haven't already. This is sure to be an extraordinary evening honoring a great friend and associate of mine, and yours as well. I do hope that you can join us for a night of memories, laughs, and good fun with fellow admirers and long-time readers of Richard's Dow Theory Letter. The room is filling up and there will be a very large crowd.

A significant number of my fellow writers and publishers have committed to attend. It is going to be an investment-writer, Richard-reader, star-studded event. You are going to be able to rub shoulders with some very famous analysts and writers. If you are a fellow writer, you should make plans to attend or send me a note that I can put in a tribute book we are preparing for Richard. And feel free to mention this event in your letter as well. We want to make this night a special event for Richard and his family of readers and friends. So, if you haven't, go ahead and log on to https://www.johnmauldin.com/russell-tribute.html and sign up today. The room will be full, so don't procrastinate. I wouldn't want any of you to miss out on this tribute. I look forward to sharing the evening with all of you.

Where Have My Earnings Gone?

Barron's probably jinxed the stock market by stating why they think the Dow won't fall to 5000, although we do have what I hope is the start of a nice bear market rally. Part of their reasoning is that stocks are cheap. They assign a price to earnings (P/E) ratio of a lowly 13, based upon 2009 estimated earnings of $51 in operating profits, which they suggest is historically low. And I agree that 13 is toward the low end and would represent a good long-term buying opportunity - if indeed it was 13.

Actually, if you want to get really bullish, go to S&P's web site and look at their estimated earnings for 2009. They calculate a P/E of 10.89 on 2009 estimated operating earnings.

As I have written over the years, the long-term P/E studies all use "as-reported" earnings, or earnings that are reported on tax returns. Operating earnings are of the EBBS variety, or Earnings Before Bad Stuff (or whatever you want to designate as the BS component). Companies like to tell us to ignore all those "one-time" writedowns, which seem to happen a lot more than once these days.

Going back a few decades, operating and as-reported earnings were very closely aligned. That relationship began to change in the mid-'90s, as management wanted to make a more bullish case, which certainly helped with their stock options. And the difference between operating and as-reported earnings is now wider than ever.

The difference between estimates for 2009 operating and as-reported earnings is almost exactly 100%. Which means that analysts are projecting there is going to be a lot of Bad Stuff in 2009 to be written down. The table below is a cut and paste from the S&P web site, where they calculate the earnings for the S&P 500. Notice the difference between the P/E ratios for operating and as-reported earnings. The latter P/E is based on the previous 12 months and used Thursday's price, so if you calculate it today it would be slightly higher.

Did you notice the as-reported estimated earnings P/E for the quarter ending September 30, 2009? In the 20 years of data on the web site, the highest it ever got to was 46, in the last recession. That P/E of 181 is because of the negative earnings for the 4th quarter of 2008. Of course, this assumes that earnings estimates don't keep being revised downward, which is not a safe assumption. They have been revised downward every quarter for almost two years. Seemingly, past projections are not indicative of future results.

Now, to be fair, using the extremely bad earnings of the recent past as a one-time metric is not altogether indicative either. Robert Shiller of Yale uses ten-year average earnings to smooth out the business cycle, and this would give you a P/E of about 13.

My good friend Ed Easterling uses a different methodology to project earnings, involving the historical relationship between GDP and P/E ratios. This is based upon the historical fact that earnings more or less rise at the level of GDP plus inflation. This is a mean-reverting chart, as earnings cannot grow faster than GDP for too long, and also acknowledges that rough patches like the one we are in now will not last, and earnings will rebound. Using his methodology we end up with a P/E just south of 13.

So, I know a lot of you have stayed in the market the whole time it has been falling and are now wondering what to do. If you have a ten-year time horizon you probably can buy here and do OK. But I wouldn't. I think this market is going to have more problems as we confront the real possibility that we will get some really poor earnings for the first and second quarters. The economy is simply weak, and that weakness is hitting more and more companies. From exporting companies to the big international firms, a global slowdown is hitting almost everyone. Even hospitals are being challenged. We could see a real bear market rally lure investors back in, just to crush their hopes this summer.

Markets go from high valuations to low valuations and back again over long periods of time. I believe that we have a long time to go in the current secular bear cycle. As I have written for years, this one began in 2000 and could last until the middle of the next decade. While we will see a "bottom" in stock prices at some point, maybe even this year, we have a long way to go to get to a really low P/E ratio.

Big secular bull markets happen when P/E ratios drop below 10 (and even lower). That acts just like winding a spring. When it is let loose, it explodes for a very long time. There is another bull market in front of us. I would rather be patient and rely on an absolute-return style of investing for now. If I miss the first part of this run, so be it. I see more risk than reward in this latest run-up.

The Land of the Setting Sun

Japan has been in a malaise for 20 years. And just when it looked like the country might turn around, the bottom has seemingly fallen out. Japan's economy shrank a slightly revised 3.2% in the last quarter of last year, confirming the sharpest contraction since the oil crisis in 1974, and economists warn of further contraction in the next two quarters.

The Japanese economy, mired in its worst recession since World War II, is forecast to shrink a further 2.5% in the first quarter of this year and another 0.4% in the second quarter, a Reuters poll shows.

But if you look at the underlying data, it's even worse. Let's turn to a recent letter from my good friend and favorite data maven, Greg Weldon. ( www.weldononline.com )

Japanese exports have fallen 54% in the last 6 months, an average of $40 billion a month, or down over a quarter of a trillion dollars. Greg notes that past 6-month changes in exports in Japan were hardly ever up or down more than a trillion yen. This is four times that level, about 4 trillion yen. To get a visual view, look at the graph below. That is called falling off a cliff.

The decline in exports is about 45% year over year. Japan is one of the countries that has run a very large trade surplus, allowing them to buy lots of dollars and lend a great deal of money. Their banks have been an engine for growth worldwide, but especially in Asia. And the graph below shows that trade surplus turning into a large trade deficit of 952 billion yen, or somewhere over 9 billion dollars.

To give that some perspective, the US trade deficit came in today and was "only" $36 billion, the lowest level in six years, mainly due to lower oil prices, as our exports have been shrinking as well (more on that below). The US economy is roughly three times the size of Japan's (and Japan is the world's second largest economy); so $9 billion is no small sum of money, relatively speaking.

(Quick note - while looking for that number on the web, I came across this tidbit in the China Daily. They project that the GDP of China will surpass Japan's next year.)

Inventory-to-shipping ratios in Japan are rising by over 50%, as industrial production is down more than 10% and likely to fall much further. Japanese auto exports are down 63% in just four months. Auto exports have literally fallen off a cliff, as inventories have doubled.

No surprise, Japan is promising even more government support programs, and aid to industries of all sorts. This from a government that has over 140% of debt to GDP, about twice that of the US. And their rapidly rising credit default swap rate is not helping. Who would have thought of Japan as a credit risk? Three years ago, almost no one. Now, rates are 30 times higher.

Japan's economy is driven by exports. And those exports were crushed as the yen rose in buying power and Japan's exports became less competitive in the last quarter, with calls for intervention to bring the yen back to a level where their industries can be more competitive. Look at the chart below of the Japanese yen versus the US dollar. (The moving average is 90 days.)

Note that less than two years ago the yen was over 124 to the dollar, and fell last quarter to below 87, and has risen back to 98 today. Think about the Japanese auto manufacturer. Two years ago he could sell his car in the US (or wherever) for $30,000 and get 3,750,000 yen. Today, that $30k only gets him a little under 3,000,000 yen. Think his costs dropped 20%? Think he can raise prices 25%?

If you sell machinery, you are competing with companies, countries, and currencies all over the world. If your currency rises, you are less competitive, or your profits have to fall.

Japan has problems, and not just in manufacturing. The population of the country is now literally shrinking, as they have the highest proportion of elderly people and the lowest proportion of children. By 2050, 70% of the labor force will have disappeared. While Toyota is the world's largest car company, auto sales in Japan peaked 18 years ago. Supermarket sales have fallen every year for the last 11 years. This is a country in a long-term decline, with massive debt. While there is still a lot of economic power there, it is not the country of the future. Unless they figure out how to grow their population, it will be a long slow slide.

The Swiss Start Their Engines

About five years ago Greg Weldon (mentioned above), a big NASCAR fan, introduced the idea of a competitive devaluation raceway among Asian countries trying to make sure they could compete against each other to produce "stuff" for the US consumer, with each "car" drafting the other as they went around the turns, trying to get a competitive advantage by manipulating their currencies.

Today, I heard a new engine roar, one that I have never heard before. It is a deep-throated and powerful new entry into the devaluation race, and one that will have large ramifications for world trade. Gentle reader, this is huge, and we visited Japan first to give you some idea of the problems all over the world, for indeed we could have picked any number of countries and told as sad a tale.

But who would have picked Switzerland? Yet we read this morning, "The Swiss franc posted its biggest weekly decline against the euro since 1999 after the country's central bank sold the currency to halt a 7.6 percent appreciation in the past six months.

"The franc was also near the lowest level versus the dollar in three months after the Swiss National Bank's (SNB) first solo intervention in foreign-exchange markets since 1992. The SNB also said yesterday it will buy corporate bonds as it cut the benchmark three-month Libor target rate to 0.25% from 0.5% to revive the economy."

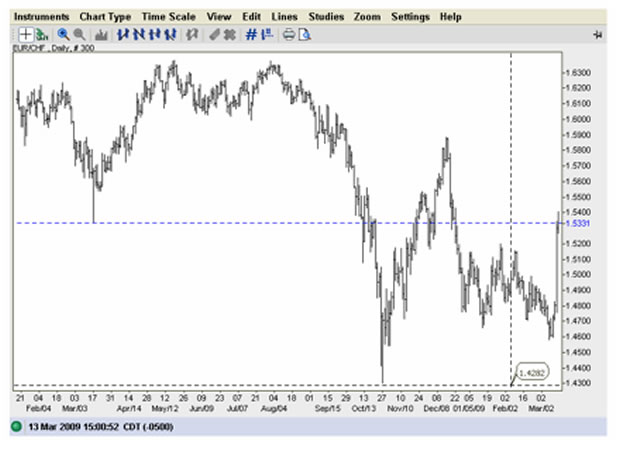

This is tectonic. It is a game changer. First, they did it before the upcoming G-20 meeting. They clearly felt they could not wait. And they moved the currency big-time. Look at the chart below of the Swiss franc against the euro. The far right bar jumped 7 big "handles" in a few hours. (A handle is trader talk for a unit of movement.) Currency markets have been violent of late, but this is huge. Currencies are supposed to move at a glacial pace, not by 4-5% in a day!

The Swiss economy will slump by as much as 3% this year, the most since at least 1975, the central bank said yesterday. Price pressures evaporated in recent months as oil prices sank, the franc strengthened, and domestic demand dropped. Prices will probably decline this year and inflation will be "very close to zero" in 2010 and 2011, the SNB said. The franc's appreciation made Swiss products less competitive in Europe and the US, where deepening recessions were already curbing demand. (Bloomberg)

The story goes on to talk about numerous Swiss businesses that simply were not competitive with the rise in the value of the franc against the euro. With their economy slumping, with deflation knocking at their door, they clearly felt the need to act. Note they plan to buy corporate bonds to inject money into their economy. The Swiss, being frugal, don't have that many bonds, so the central bank may have some trouble finding enough to stimulate their economy - thus they are clearly prepared to use the currency tool in the cabinet to help stimulate their economy.

The last time a G-10 nation intervened in its currency was in 2003 when Japan tried, and oddly failed, as their currency had risen about 6% a year later. That caused me to write back then that their central bank established a new level of central bank ineffectiveness, because they could not figure out how to destroy their own currency, even when they wanted to.

The point is that such interventions by major developed countries are rare. Whatever their reasons, the Swiss have opened Pandora's box. Do Senators Schumer and Graham now start talking about that major currency manipulator, Switzerland, and start to introduce bills to punish them? Will Secretary Geithner come before a Congressional committee and call the Swiss currency manipulators? If not, then how do we deal with China?

Because China can now say, with some justification, that if the Swiss can manipulate their currency to make themselves more competitive, then why is it wrong for us? And how long do you think it will be until Japan tries once again to push the yen lower, with its export industries in tatters? And Korea? Taiwan?

You can almost hear the announcement over the loudspeakers: "Gentlemen, start your engines!"

My One True Nightmare

Let's be clear. As bad as things are, and they will probably get worse, I am a believer in free markets and the ability of people to figure out their own paths. And it is 300,000,000 people in the US and billions worldwide, each acting in their own interest, that will bring us back to a growing global economy.

But there is one thing that worries me above all else. For over six years I have been writing that the one thing that could truly derail the world economy is protectionism. Nothing would be more deleterious in today's global economy.

And that brings us to this stark note I read today on Bloomberg. It sent chills down my spine: "American exports have slumped at a 44% annual pace in the most recent six months of data, with imports shrinking 51%, probably the most since the Great Depression, according to Morgan Stanley analysts. The figures may add to pressure on the Obama administration to rework international agreements and include protections for US workers and the environment."

The US steel industry is planning to bring anti-dumping charges against foreign steel. India just raised steel tariffs. It seems like every day I read that someone somewhere is calling for their particular industry to be protected, bailed out, or subsidized. And it is not just the US. It is happening all over the world.

Right now, it is just small amounts and nothing that will rock the system. But these things can get a life of their own. If the Swiss can move to take their currency lower, then there will be a score of countries that will ask why they shouldn't be allowed to do the same. And the one currency they all want to be lower against? The dollar. Even though our economy is in shambles and consumer spending is falling, it is still a huge spending machine. And every export-growth-led country wants a piece of it.

We are getting ready to run a huge, $3-trillion deficit, and the Fed is going to print a lot of money and inject it into the economy. There is real reason to worry about the strength of the dollar. And yet, the dollar is the weakest currency except for all the others. As much as we in the US worry about the fall of the dollar, it could rise over the coming year.

That is going to put a lot of pressure from a lot of sources on President Obama, who ran as a populist. Here is hoping that his advisors steer him away from starting a round of trade protectionism that could beggar the world, just as Smoot-Hawley did 75 years ago. This bears watching closely.

New York, Vegas, and Happy Birthday, Tiffani

I will be in New York next week for a few days, and hope to have dinner with Art Cashin. I have a lot of meetings scheduled. Details are firming up. Then it's Doug Casey's "Crisis & Opportunity Summit," March 20-22 in Las Vegas, where I get to be the resident bull! Click to learn more about the Summit .

I will then go to La Jolla for my own Strategic Investment Conference, April 2-4. It is sold out; but as I mentioned at the top of the letter, you can still get tickets to the Richard Russell Tribute Dinner.

And today, Tiffani, my oldest daughter and business partner, is 32. She is holed up in the wilds of Kentucky working on our book. It is hard for me to express how great it is to be working with her. As all my partners know, she really does run the business, letting me do what I do and giving me the time to research and write to you.

And just to brag a little, here is a picture of my four girls. Dad is very lucky. And maybe this is just a little reason I remain so optimistic in spite of everything.

Time to hit the send button. Have a great week, and remember that we will all get through this together. That is what friends are for.

Your ready for some down time analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2009 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.