Economic Depression 2009?

Economics / Economic Depression Feb 08, 2009 - 02:59 PM GMTBy: Mick_Phoenix

Whilst the great inflation/deflation debate continues (its deflation that wins, the inflationistas are being misled by the Fed's actions with its bail out facilities) we need to look at some startling new facts and projections that have appeared in the public arena. My worry, as you can gather from the title of this article, is that we face a global depression that cannot be avoided even if the events discussed below favour the results that the Central Banks et al seek.

Whilst the great inflation/deflation debate continues (its deflation that wins, the inflationistas are being misled by the Fed's actions with its bail out facilities) we need to look at some startling new facts and projections that have appeared in the public arena. My worry, as you can gather from the title of this article, is that we face a global depression that cannot be avoided even if the events discussed below favour the results that the Central Banks et al seek.

Events are moving to a point were attempts to disguise the effects of certain outcomes can no longer be hidden.

The Federal Reserve.

"The Federal Reserve on Tuesday announced the extension through October 30, 2009, of its existing liquidity programs that were scheduled to expire on April 30, 2009. The Board of Governors and the Federal Open Market Committee (FOMC) took these actions in light of continuing substantial strains in many financial markets.

- The Board of Governors approved the extension through October 30 of the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF), the Commercial Paper Funding Facility (CPFF), the Money Market Investor Funding Facility (MMIFF), the Primary Dealer Credit Facility (PDCF), and the Term Securities Lending Facility (TSLF). The FOMC also took action to extend the TSLF, which is established under the joint authority of the Board and the FOMC.

In addition, to address continued pressures in global U.S. dollar funding markets, the temporary reciprocal currency arrangements (swap lines) between the Federal Reserve and other central banks have been extended to October 30. This extension currently applies to the swap lines between the Federal Reserve and each of the following central banks: the Reserve Bank of Australia, the Banco Central do Brasil, the Bank of Canada, Danmarks Nationalbank, the Bank of England, the European Central Bank, the Bank of Korea, the Banco de Mexico, the Reserve Bank of New Zealand, the Norges Bank, the Monetary Authority of Singapore, the Sveriges Riksbank, and the Swiss National Bank. The Bank of Japan will consider the extension at its next Monetary Policy Meeting. The Federal Reserve action to extend the swap lines was taken by the Federal Open Market Committee.

The current expiration date for the Term Asset-Backed Securities Loan Facility (TALF) remains December 31, 2009. Other Federal Reserve liquidity facilities, such as the Term Auction Facility (TAF), do not have a fixed expiration date.

The AMLF provides loans to depository institutions to purchase asset-backed commercial paper from money market mutual funds. The CPFF provides a liquidity backstop to U.S. issuers of commercial paper. The MMIFF supports a private-sector initiative to provide liquidity to U.S. money market investors. The PDCF provides discount window loans to primary dealers. Under the TSLF, the Federal Reserve Bank of New York auctions term loans of Treasury securities to primary dealers. The TALF will support the issuance of asset-backed securities collateralized by student loans, auto loans, credit card loans, and loans guaranteed by the Small Business Administration. Under the TAF, Reserve Banks auction term discount window loans to depository institutions."

Regular readers will know that the extension comes as no surprise to me and I expect further extensions to happen for sometime to come. Clearly the supposed purpose of all these schemes, to recapitalise Banks (and just about anything else) and allow the credit markets functionality to return to a state of "normality" has failed. The extension reflects the Fed's position as lender/borrower of last resort, rather than any ongoing success in achieving the aims they were designed for.

Fear not readers for the Fed is readying itself for the next stage of the battle to defeat deflation, as the Chairman so presciently foresaw:

- "However, a principal message of my talk today is that a central bank whose accustomed policy rate has been forced down to zero has most definitely not run out of ammunition. As I will discuss, a central bank, either alone or in cooperation with other parts of the government, retains considerable power to expand aggregate demand and economic activity even when its accustomed policy rate is at zero.

U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation.

Of course, the U.S. government is not going to print money and distribute it willy-nilly (although as we will see later, there are practical policies that approximate this behavior). Normally, money is injected into the economy through asset purchases by the Federal Reserve. To stimulate aggregate spending when short-term interest rates have reached zero, the Fed must expand the scale of its asset purchases or, possibly, expand the menu of assets that it buys. Alternatively, the Fed could find other ways of injecting money into the system--for example, by making low-interest-rate loans to banks or cooperating with the fiscal authorities.

So what then might the Fed do if its target interest rate, the overnight federal funds rate, fell to zero? One relatively straightforward extension of current procedures would be to try to stimulate spending by lowering rates further out along the Treasury term structure --that is, rates on government bonds of longer maturities. There are at least two ways of bringing down longer-term rates, which are complementary and could be employed separately or in combination. One approach, similar to an action taken in the past couple of years by the Bank of Japan, would be for the Fed to commit to holding the overnight rate at zero for some specified period. Because long-term interest rates represent averages of current and expected future short-term rates, plus a term premium, a commitment to keep short-term rates at zero for some time--if it were credible--would induce a decline in longer-term rates. A more direct method, which I personally prefer, would be for the Fed to begin announcing explicit ceilings for yields on longer-maturity Treasury debt (say, bonds maturing within the next two years). The Fed could enforce these interest-rate ceilings by committing to make unlimited purchases of securities up to two years from maturity at prices consistent with the targeted yields . If this program were successful, not only would yields on medium-term Treasury securities fall, but (because of links operating through expectations of future interest rates) yields on longer-term public and private debt (such as mortgages) would likely fall as well.

Lower rates over the maturity spectrum of public and private securities should strengthen aggregate demand in the usual ways and thus help to end deflation. Of course, if operating in relatively short-dated Treasury debt proved insufficient, the Fed could also attempt to cap yields of Treasury securities at still longer maturities, say three to six years . Yet another option would be for the Fed to use its existing authority to operate in the markets for agency debt (for example, mortgage-backed securities issued by Ginnie Mae, the Government National Mortgage Association)."

Quotes from " Deflation: Making Sure "It" Doesn't Happen Here " Ben Bernanke November 2002. (Red highlights mine)

Within the next few days we will see the ideas in this speech, now set up as a theory, tried in actual market conditions. Its success or failure will set the future direction of the global economy. The enabling agent to allow this test to go ahead is:

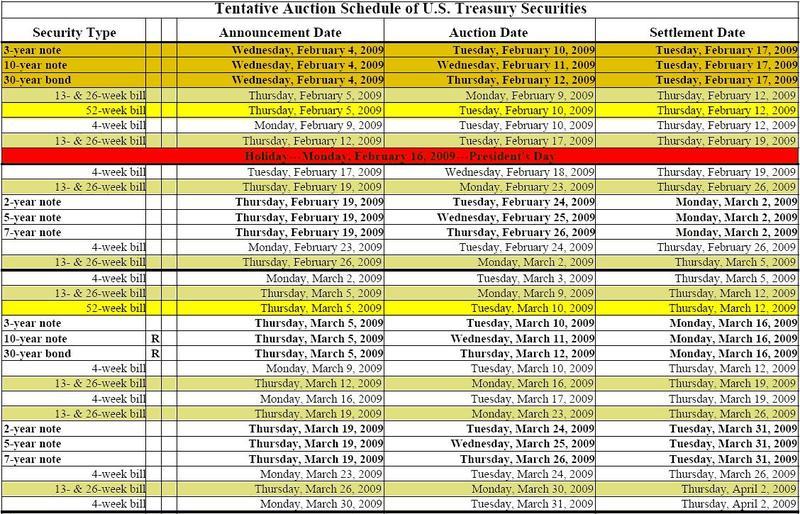

The US Treasury :

- Washington, DC - Treasury is announcing the following changes to the issuance calendar:

A new monthly 7-year note, with the first auction occurring in February 2009.

A regular reopening of the quarterly 30-year bond in the month following the initial new offering, with the first reopening occurring in March 2009.

Details of the February Refunding

We are offering $67 billion of Treasury securities to refund approximately $36.3 billion of privately held securities maturing or called on February 15 and to raise approximately $30.7 billion. The securities are:

A new 3-year note in the amount of $32 billion, maturing February 15, 2012;

A new 10-year note in the amount of $21 billion, maturing February 15, 2019;

A new 30-year bond in the amount of $14 billion, maturing February 15, 2039.

During the last several months, changes in economic conditions, financial markets, and fiscal policy, as well as a decline in nonmarketable debt issuance have contributed to an increase in Treasury's marketable borrowing needs.

Treasury has responded to the increase in marketable borrowing requirements by raising issuance sizes of regular weekly and monthly bills, increasing the frequency and issuance sizes of cash management bills, increasing the issuance sizes of nominal coupon security offerings, and adjusting the securities offering calendar, including adding monthly 3-year notes, a second reopening of 10-year notes, and introducing newly issued 30-year bonds on a quarterly basis.

Introduction of a monthly 7-year note: Treasury is announcing the addition of a monthly new-issue 7-year note. The monthly 7-year notes will have an end-of-month settlement along with the 2-year and 5-year notes. The first auction of the 7-year notes will occur on Thursday, February 26, 2009

Introduction of a regular 30-year bond reopening: Treasury is announcing the addition of a regular reopening of the 30-year bond in the month following the initial quarterly offering. This will result in eight 30-year bond auctions a year. The first auction of the reopening of 30-year bonds will occur on Thursday, March 12, 2009

With the increase of debt issuance upward pressure will be exerted upon yields. This counter-acts the Feds attempts to keep both short term rates and those further out along the curve at a level the Fed perceives as conducive to encouraging credit markets to allow the flow of funds to re-start. The real test of course is whether buyers turn up at the auctions. A failure will force the Fed to enact its statement from the last FOMC minutes:

- "The Committee also is prepared to purchase longer-term Treasury securities if evolving circumstances indicate that such transactions would be particularly effective in improving conditions in private credit markets."

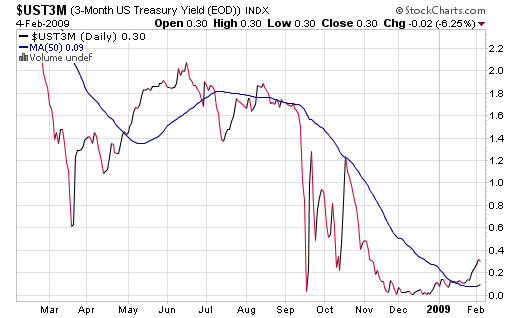

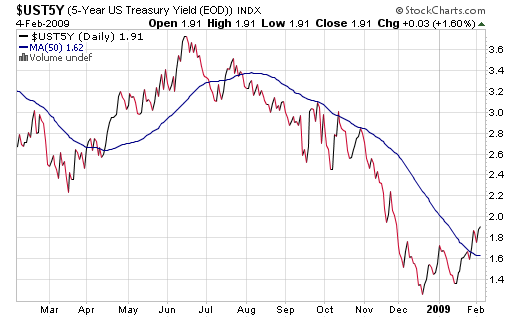

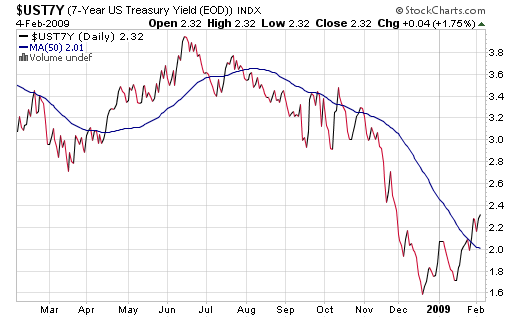

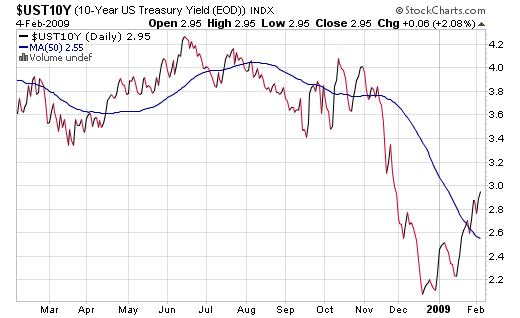

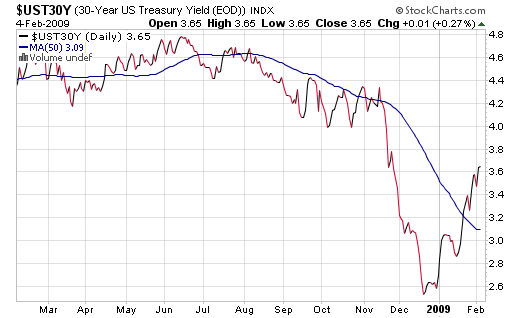

To control rates the will have to step up to the plate and bid at prices that keep yields within its targeted band. We don't know exactly what the boundaries of the band are but we can look at recent yield levels to garner some idea from previous support and resistance levels:

Bond yields are in a move higher as you would expect, bond buyers know what the increase in market supply will do to prices if no one (in essence foreign buyers) turns up for the auctions and bond yields are acting accordingly as long positions are closed.

The Fed will end up reacting to the results of the auctions; if buyers insist on higher yields (by setting lower prices) the Fed will step in and start buying across the curve, indeed if they are looking at the yields across the curve now they may well be feeling some concern that the plan to hold rates at low levels may already be under attack.

If the Fed fails to react to higher yields or failed auctions (when not enough bids are received to cover the issuance) bond markets will take fright as the Feds credibility to back up the words from the FOMC minutes is destroyed. Without a buyer of last resort supporting the market then a bout of panic selling, even dumping could take place. In some ways this would suit the Fed as it would begin its intervention at a lower price level and if the policy is successful the balance sheet would benefit from appreciating prices as yields fall back.

Why do I think Fed intervention is inevitable?

IMF

The ability of Foreign Central Banks to buy US issued debt has been a function of increasing dollar flows taken in payment for exports to the US and re-circulated back (to stop domestic inflation) by buying US debt.

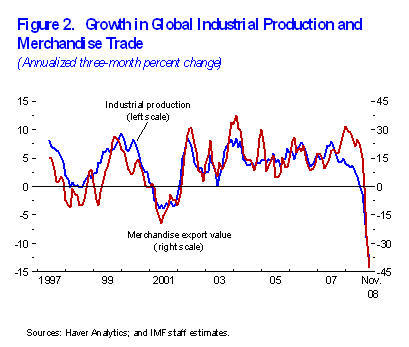

As the IMF says "Global output and trade plummeted in the final months of 2008". The requirement to re-circulate dollars back into US debt will also be severely curtailed just at the time when the US wishes to raise debt issuance. The need for the re-circulation of dollars is not going to increase anytime soon:

Indeed a further contraction of "available" dollars, produced in exchange for goods imported into the US, is more likely that the chart above suggests. The IMF has a tendency to be optimistic in its views. To enable the US Treasury to issue new and increasing amounts of debt in an environment of decreasing need, when world trade has almost halved, leaves the Fed no alternative but to put its words into action.

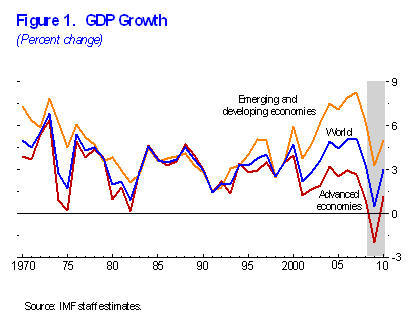

If however the Fed decides not to deploy the printing presses and its unconventional policies then the result will be as the IMF states:

- "Downside risks continue to dominate, as the scale and scope of the current financial crisis have taken the global economy into uncharted waters. The main risk is that unless stronger financial strains and uncertainties are forcefully addressed, the pernicious feedback loop between real activity and financial markets will intensify, leading to even more toxic effects on global growth.

In addition, the risks of deflation are rising in a number of advanced economies, while emerging economies' corporate sectors could be badly damaged by continued limited access to external financing. Furthermore, while fiscal policy is providing important short-term support, the sharp increase in the issuance of public debt could prompt an adverse market reaction, unless governments clarify their strategy to ensure long-term sustainability."

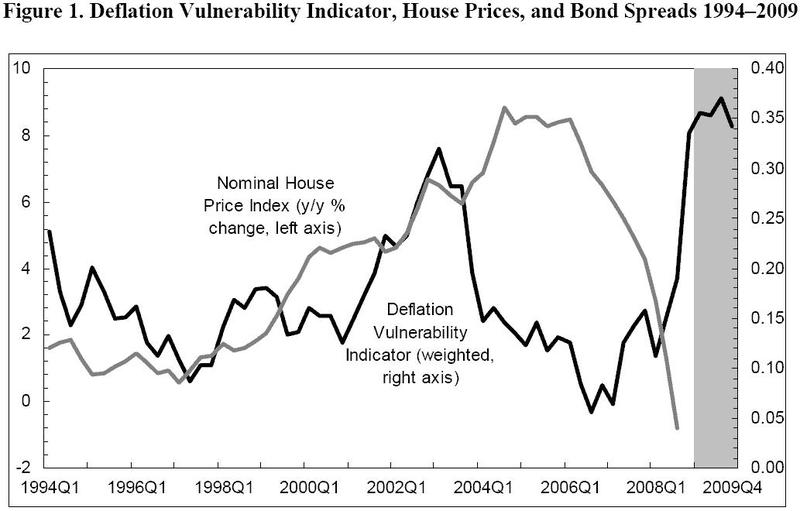

In the IMF paper, " Gauging Risks for Deflation " the work of Kumar and others is reproduced, showing the overall vulnerability to deflation for the world:

The IMF have the risk indicator flattening off in 2009, again this seems optimistic considering that the downside risks are much, much greater than any possible upside to the current situation. As it happens, the IMF do have an important caveat to the indicator, which may:

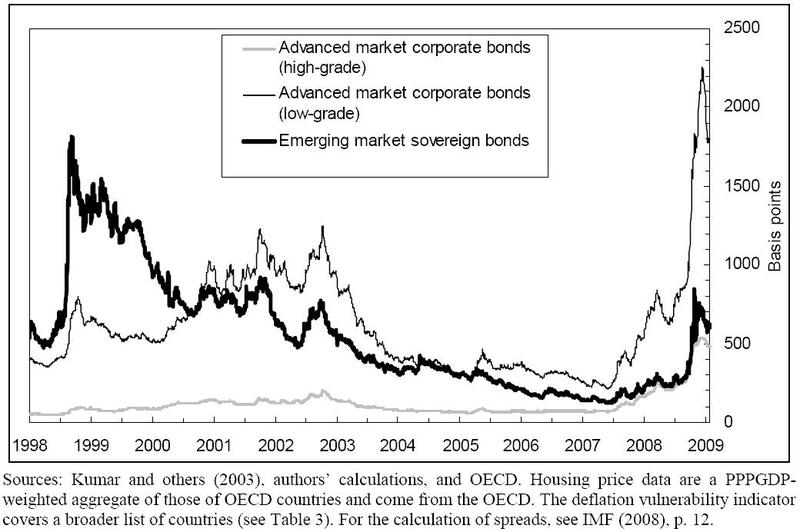

- "underestimate the risks today relative to those for earlier episodes, as it does not consider house prices. In 2002/03, housing markets were very strong, with low interest rates boosting prices and construction, helping pull the global economy out of its weak patch. Also, the indicator does not do full justice to the credit crisis because it does not consider quantitative indicators of financial conditions other than bank credit, which is being buoyed by temporary forces. Spreads on bonds, for example, are much wider today than during 2002-03 in advanced economies and have reached levels similar to those prevailing in 2002-03 in emerging economies."

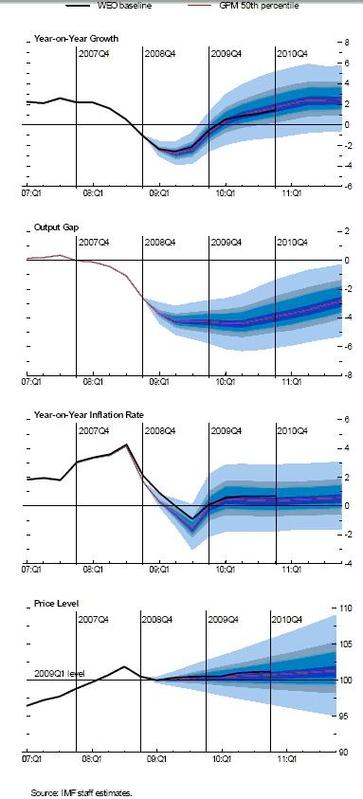

- "This section proposes to analyze deflation vulnerability with the help of the IMF staff's Global Projection Model (GPM), which explicitly considers the implications of the zero interest floor (ZIF) for monetary policy. The most intractable deflation problem occurs when policy interest rates reach the ZIF for a prolonged period of time because if a zero interest rate fails to close the output gap, downward pressure on prices is reinforced.

Unless other policies are implemented to raise aggregate demand, this could result in a downward deflationary spiral. The model incorporates three country models, for the United States, the euro area, and Japan (the G-3); and it covers output and unemployment, the rate of inflation, the exchange rate, and, with a modified Taylor rule, the monetary policy interest rate.

26. Figure 4 shows the current World Economic Outlook (WEO) baseline outlook (black line) and GPM-based fan charts for the G-3 economies (see also IMF, 2009a).

- To sum up, the WEO baseline projection, in itself, does not contain an unduly serious deflation problem. However, the GPM-based fan charts reveal a significant probability of much more negative deflationary outcomes, and hence a deeper and more prolonged recession in the G3."

I see nothing that supports a hyperinflationary environment in the G3 in the medium term. If the IMF red projection line (mid 50th percentile) is accurate, inflation, growth and price levels will not engender a credible expectation of future inflation and monetary and fiscal stimulus will fail. That failure will lead to a period of extended deflationary forces acting upon the global economy.

The initiation of increased debt issuance by the US Treasury begins next week. Any sign of weakness in the Fed's response to low prices or failure at the auctions will cause major disruption in the bond market. However such disruption should be short term as long as the Fed responds vigorously to put right its previous inaction.

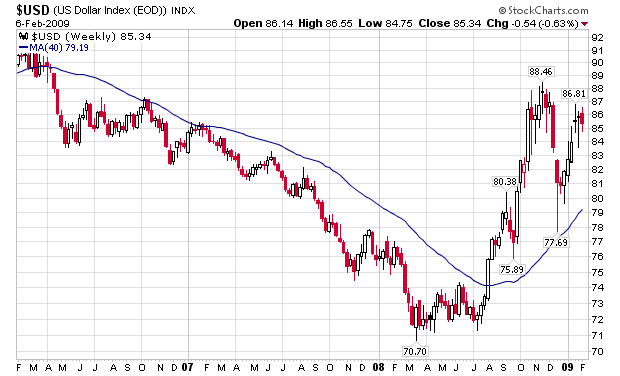

Even if the Fed is successful and keeps interest rates along the curve artificially low, there is no guarantee that the expected result of increased inflation expectations will occur in the future. Without the future threat of inflation business and consumer spending patterns will remain "tight" and a continuing hoarding of cash and cash like assets will remain attractive, even in an environment where real interest rates are negative. Only when a point is reached when cash, held as an asset , shows a depreciation will it become viable to swap cash for other assets that will give a higher return. This is why many schemes are failing, the dollar has become an asset in its own right:

Coutesy of StockCharts.com

Looking at the chart, is it just me or is the Dollar waiting for news?

Some have put forward an idea that US taxes should be cut for Businesses who wish to repatriate overseas profits, allowing an injection of cash into the US domestic economy. However with the main theme of investing already focused on highly liquid uptrends (see US Treasuries until recently) the increase in demand for Dollars as profits are converted from other currencies would cause further appreciation of the Dollar. This would make the hoarding of cash more attractive and negate the attempts to loosen the flow of funds. Indeed the suggestion of such a repatriation, especially from the US Treasury, would cause longs to take positions prior to the event occuring, pre-emptively causing the uptrend to strengthen, encouraging an acceleration of savings. Thus such a scheme would encourage the very conditions that the Fed and US Treasury are attempting to thwart.

Until economic conditions are conducive to the deployment of savings to allow profitable investment then the hoarding of cash and cash like assets will continue. I very strongly suspect we will have to live through a global depression before such economic conditions appear.

Subscribers only section

By Mick Phoenix

www.caletters.com

An Occasional Letter in association with Livecharts.co.uk

To contact Michael or discuss the letters topic E Mail mickp@livecharts.co.uk .

Copyright © 2009 by Mick Phoenix - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Mick Phoenix Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.