Obama Victory Flashing a Stock Market Buy Signal

Stock-Markets / US Stock Markets Nov 09, 2008 - 11:02 AM GMT

Welcome to Wall Street, Barack Obama. His victory signaled a change in US political direction, but the biggest election day rally ever – a surge of 4.1% in the S&P 500 Index on Tuesday – was quickly overshadowed by the grim realities of the worsening economic and earnings picture, resulting on Wednesday and Thursday in the S&P 500's biggest two-day loss (-10.0%) since 1987.

Welcome to Wall Street, Barack Obama. His victory signaled a change in US political direction, but the biggest election day rally ever – a surge of 4.1% in the S&P 500 Index on Tuesday – was quickly overshadowed by the grim realities of the worsening economic and earnings picture, resulting on Wednesday and Thursday in the S&P 500's biggest two-day loss (-10.0%) since 1987.

Mr Obama gave his first press conference as President-elect on Friday afternoon, summarizing a discussion he had had with his economic advisory team. He pledged to confront the US's economic crisis “head on” and said he wanted to see “a rescue plan for the middle class” that would include a new fiscal stimulus package. The week closed on a positive note as a late rush of buying on Friday left the stock market indices higher for the day, although still in the red for the week.

BCA Research said: “While Obama has a laundry list of policy objectives, fixing the economy will be his top priority and will dominate the legislative agenda in 2009. A fiscal stimulus package to support consumers is already being drawn up in Congress, and Obama is likely to propose additional infrastructure spending programs shortly after taking office. But fiscal policy will be hamstrung – the budget deficit is already large, while aggressive tax increases would be inappropriate in the current economic climate and there is little scope for significant spending cuts in other areas.”

“I don't know how successful Obama will be in bringing back prosperity to the US, but his amazing victory in rising to the US Presidency has inspired billions of people around the world. It has also lifted America in the eyes of the world …,” commented Richard Russell ( Dow Theory Letters ). The newspaper headlines tell the story …

Underscoring economists' concerns about the depth of the global economic slowdown was a warning from the International Monetary Fund (IMF) that developed economies as a whole would shrink by 0.3% next year. It would mark the first overall contraction in developed economies since World War II. Aggressive interest rate cuts by a number of major central banks only partly assuaged investors' fears.

Nouriel Roubini ( RGE Monitor ) said: “Deterioration in the health of the financial sector and related severe strains in funding markets have increased the tail risk of deflation for the real economy.”

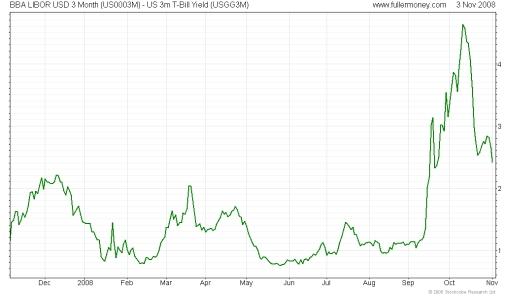

Although the banking system remains in the grips of a massive deleveraging process, there are early signs that the various central bank liquidity facilities and capital injections are beginning to have the desired effect. Restoring confidence will take a significant amount of time, but the narrowing of financial sector spreads such as the TED spread (i.e. three-month dollar Libor less three-month Treasury Bills) shows that the healing process is under way.

Next, a tag cloud of the text of the articles I have read during the past week. This is a way of visualizing word frequencies at a glance. The key words include the usual suspects.

Relying on his 50 years' market experience, Richard Russell questioned whether we were perhaps dealing with another fake-out advance. “One item that bothers me a bit is this – have we seen enough black pessimism to believe that this bear market has bottomed? My guess is that we will see more pessimism next year as unemployment climbs and as it becomes almost impossible to find a good job.”

However, John Bogle, founder of the Vanguard Group, said in an interview with Reuters on Tuesday that the fundamentals of the US stock market had “improved radically” and declines in valuations were overblown.

Across the pond, European equities received a boost from Morgan Stanley's European strategist Teun Draaisma saying that stocks were now flashing a “full house” buy signal after these markets have priced in an earnings recession, and retail investors, purchasing managers and sell-side analysts have all capitulated. Draaisma's prior calls were on the money.

Albert Edwards of Société Générale is less sure. “It has been a house of cards waiting to fall,” Edwards said according to the Financial Times . “The market has to slide much further down the slope of hope into Dante's inferno.” He believes markets are currently in the eighth of Dante's nine circles of hell.

The stock market is likely to see a lot of back-and-forth churning as it tries to map out a bottom. A 90% down-day is normally followed by a rally of two to seven days. In this instance we are dealing with two consecutive 90% down-days that occurred last week. For a year-end rally to materialize, it is essential that the recent lows (8,176 on the Dow Jones Industrial Index and 849 on the S&P 500 Index) not be taken out and that credit spreads continue to contract. But for confidence to return, sustained moves above 10,000 for the Dow and 1,000 for the S&P 500 are required.

Before highlighting some thought-provoking news items and quotes from market commentators, let's briefly review the financial markets' movements on the basis of economic statistics and a performance round-up.

Economic reports

“Global business confidence fell again at the end of October to a new record low,” said the Survey of Business Confidence of the World conducted by Moody's Economy.com . “The financial panic has been a body blow to global business confidence and the global economy is now in recession. Sentiment is extraordinarily negative in North America and Europe and measurably weaker in Asia and South America.”

Economic reports released in the US during the past week confirmed the dire economic conditions and included the following:

• Payroll employment fell by 240,000 – the 10th consecutive decline – and there was a net downward revision of 179,000 jobs to the previous two months. The unemployment rate increased by 0.4 of a percentage point to 6.5%, a figure above the peak reached in the last cyclical downturn. The economy has lost 1.2 million jobs this year, with about half the decline coming in the last three months as businesses respond to shrinking demand and tighter credit by cutting costs.

• The ISM Non-manufacturing Survey plunged to 44.4 in October from 50.2 from the previous month. This indicator had been one of the few not to show recession-like behavior, but that quickly changed with this release.

• The Institute for Supply Management's Manufacturing Index fell 4.6 points to 38.9 for October. The larger-than-expected decline puts the Index at its lowest level since the early 1980s – consistent with an economy in a severe recession.

• Credit conditions tightened during the third quarter across most of the major credit and loan categories reported in the Federal Reserve's Senior Loan Officer Opinion Survey.

• US vehicle sales fell sharply in October to 10.5 million units on a seasonally adjusted annualized basis. This pace of sales was last seen in the early 1980s.

US interest rate futures are fully pricing in a 25 basis point cut by the Federal Reserve next month, and accord a 64% chance to a 50 basis point easing.

Commenting on the outlook for US interest rates, Asha Bangalore ( Northern Trust ) said: “At this point in the economic crisis, the severity of the malaise points to expectations of a lower Federal funds rate, which the Fed may deliver sooner rather than later. We need to step back and ponder about the benefit of additional easing of monetary policy.

“There are strong expectations that a significant stimulus program will be implemented shortly. A fiscal stimulus program may be more effective in stimulating demand and bringing about a recovery than additional easing of monetary policy. Also, the recapitalization of banks that is under way should eventually erase the credit crunch and revitalize lending to the private sector, which is the key to a full-fledged economic recovery.”

Elsewhere in the world, major central banks were following up the October 8 coordinated interest rate reductions with cuts of their own, often larger than expected.

The European Central Bank eased monetary policy and cut its key monetary policy rate by 50 basis points to 3.25%. With inflationary pressures easing, it seems the Bank has shifted its bias towards monetary loosening to support the rapidly deteriorating Eurozone economy.

The Bank of England has stunned markets and cut its main policy rate by 150 basis points as the UK's recession is deepening. The rate is now 3% versus 5.5% at the start of the year and a cyclical peak of 5.75% a year ago.

Central banks in Switzerland, Denmark, Australia and India have also slashed benchmark interest rates.

The November 15 G20 meeting in Washington will be the next of a series of summits to assess global responses to the financial crisis. Discussion will likely focus on assessing short-term stabilization efforts, specific regulatory and capital market reforms, and institutional structures (including the role of the IMF).

Week's economic reports

Click here for the week's economy in pictures, courtesy of Jake of EconomPic Data .

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Nov 3 | 10:00 AM | Construction Spending | Sep | -0.3% | -0.8% | -0.8% | 0.3% |

| Nov 3 | 10:00 AM | ISM Index | Oct | 38.9 | 43.0 | 42.0 | 43.5 |

| Nov 4 | 12:00 AM | Auto Sales | Oct | - | 4.5M | NA | 4.3M |

| Nov 4 | 12:00 AM | Truck Sales | Oct | - | 5.5M | NA | 5.3M |

| Nov 4 | 10:00 AM | Factory Orders | Sep | - | -1.0% | -0.8% | -4.0% |

| Nov 5 | 8:15 AM | ADP Employment | Oct | - | - | -100K | -8K |

| Nov 5 | 10:00 AM | ISM Services | Oct | - | 47.0 | 47.0 | 50.2 |

| Nov 5 | 10:35 AM | Crude Inventories | 11/01 | - | NA | NA | NA |

| Nov 6 | 8:30 AM | Initial Claims | 11/01 | - | 475K | 476K | 479K |

| Nov 6 | 8:30 AM | Productivity -Prel | Q3 | - | 1.0% | 1.0% | 4.3% |

| Nov 7 | 8:30 AM | Average Workweek | Oct | 33.6 | 33.6 | 33.6 | 33.6 |

| Nov 7 | 8:30 AM | Hourly Earnings | Oct | 0.2% | 0.2% | 0.2% | 0.2% |

| Nov 7 | 8:30 AM | Nonfarm Payrolls | Oct | -240K | -200K | -200K | -284K |

| Nov 7 | 8:30 AM | Unemployment Rate | Oct | 6.5% | 6.4% | 6.3% | 6.1% |

| Nov 7 | 10:00 AM | Pending Home Sales | Sep | - | - | -3.4% | 7.4% |

| Nov 7 | 10:00 AM | Wholesale Inventories | Sep | -0.1% | 0.0% | 0.3% | 0.6% |

| Nov 7 | 11:30 AM | Pending Home Sales | Sep | -4.6% | - | -3.4% | 7.5% |

| Nov 7 | 3:00 PM | Consumer Credit | Sep | $6.9B | $5.0B | $0.0B | -$6.3B |

Source: Yahoo Finance , November 7, 2008.

Next week's US economic highlights, courtesy of Northern Trust , include the following:

1. International Trade (November 13): The trade deficit is predicted to have narrowed to $57.0 billion in September from $59.1 billion in August.

2. Retail Sales (November 14): Auto sales fell sharply in October (10.6 million units versus 12.5 million units in September). Non-auto retail sales surveys show significant weakness. Based on this information, retail sales probably declined by about 2.0% in September. Consensus : -1.9%% versus -1.2% in September; non-auto retail sales: -1.0% versus -0.6% in September.

3. Other reports : Inventories, Import prices, Consumer Sentiment Index (November 14).

Click here for a summary of Wachovia's weekly economic and financial commentary.

Markets

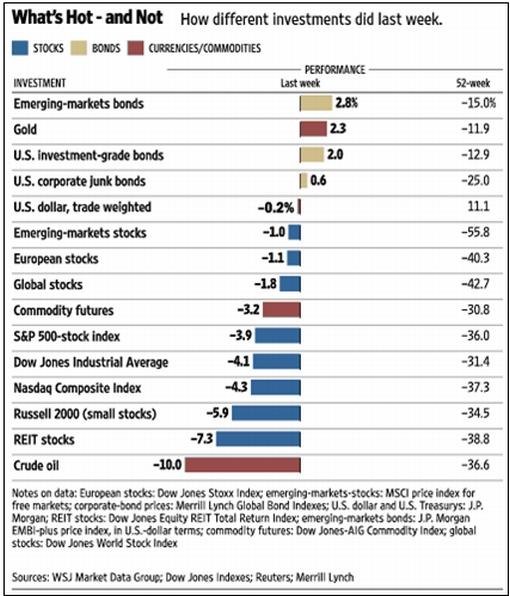

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , November 7, 2008.

Equities

Stock markets experienced a volatile week on the back of large swings in sentiment as investors digested Barack Obama's election victory, worsening economic reports and central bank interest rate cuts. Although the major global indices closed the week with losses – MSCI World Index -1.9% and the MSCI Emerging Markets Index -1.0% – the performances of individual markets varied greatly.

Among developed markets, Italy (+2.4%), New Zealand (+0.7%), Australia (+0.6%), the UK (+0.3%) and Japan (+0.1%) recorded positive returns, whereas the US markets, Canada (-1.7%), Germany (-1.0%) and France ( 0.5%) were under the water.

As far as emerging markets are concerned, Singapore (+3.9%), Hong Kong (+2.0%), South Korea (+1.9%), India (+1.8%) and China (+1.1%) all registered gains. On the other hand, Turkey (-4.3%), Mexico (-3.1%), Taiwan (-2.6%), Russia (-1.7%) and Brazil (-1.6%) did not give investors much to smile about.

The table below by Finviz summarizes the past week's performances (in US dollar terms, whereas all the gains/losses referred to elsewhere in this post are in local currency terms) for various stock markets. Click here or on the thumbnail for a large table.

The table below by Finviz summarizes the past week's performances (in US dollar terms, whereas all the gains/losses referred to elsewhere in this post are in local currency terms) for various stock markets. Click here or on the thumbnail for a large table.

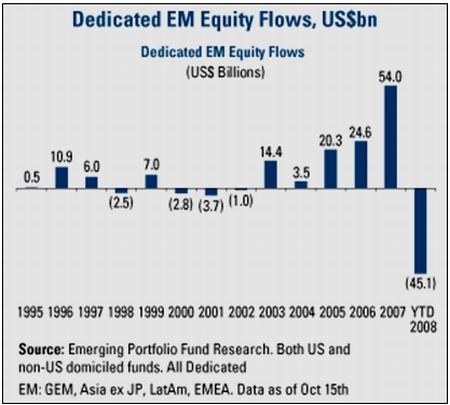

For the week ended November 5 there were net inflows of $413 million into emerging-market stock funds, according to US Global Investors . This is a significant improvement from the previous week when there were net redemptions of $1.6 billion. For the year to date, the outflows are estimated at $45 billion, nearly 40% of the cumulative inflows from 2003 through 2007.

The US stock markets all declined over the week as shown by the major index movements: Dow Jones Industrial Index -4.1 (YTD -32.6%), S&P 500 Index -3.9% (YTD -36.6%), Nasdaq Composite Index -4.3% (YTD -37.9%) and Russell 2000 Index -5.9% (YTD 34.0%).

The Dow needs to increase by 12.2% to reach its 50-day moving average and 29.9% to get to the key 200-day line.

The Dow needs to increase by 12.2% to reach its 50-day moving average and 29.9% to get to the key 200-day line.

Click here or on the thumbnail below for a market map, obtained from Finviz.com, providing a quick overview of the performance of the various segments of the S&P 500 Index over the week.

The automobile group (-14%) was among the underperformers for the week. On Friday both General Motors (GM) and Ford (F) reported losses and substantial cash burns during the third quarter – Ford used $7.7 billion cash and General Motors $6.9 billion. Both firms are seeking financial assistance from Government.

Fixed-interest instruments

Yields on government bonds declined during the past week, spurred on by mounting economic woes and interest rate cuts in a number of countries.

The 10-year US Treasury Note declined by 18 basis points to 3.78%, the UK ten-year Gilt dropped by 34 basis points to 4.19% and the German ten-year Bund fell by 24 basis points to 3.67%. Emerging-market bonds fared even better as the risk premium eased from elevated levels.

A number of commentators are of the opinion that government bonds are topping out. “… further deflation and economic decay will induce more inflation-stoking nationalization, socialism and monetary promiscuity – so sell bonds. Cascading global bond markets would be the next big crisis,” said Bill King ( The King Report ).

US mortgage rates also declined, with the 30-year fixed rate falling by 42 basis points to 6.14% and the 5-year ARM by 7 basis points to 5.92%.

The cost of buying credit insurance for US and European companies eased as shown by the narrower spreads for both the CDX (North American, investment grade) Index (down from 200 to 188) and the Markit iTraxx Europe Crossover Index (down from 765 to 762).

Money-market rates declined as a result of easier monetary policy and the ongoing provision of liquidity. The three-month dollar Libor rate declined by 74 basis points to 2.29% during the week – 103 basis points above the Fed's target rate of 1.0%. The spread was 43 basis points at the start of the year.

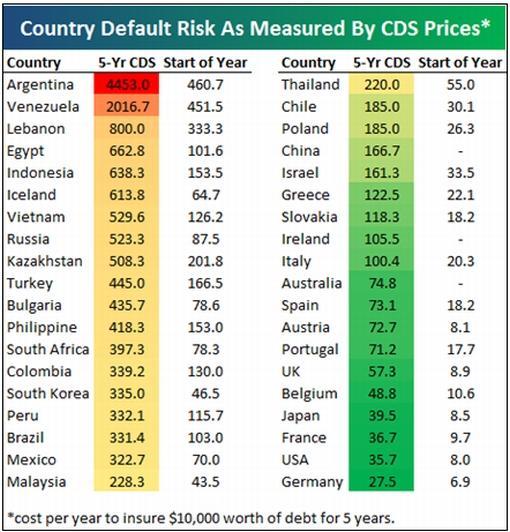

Bespoke provided an interesting table of the credit default swap prices for individual countries. These prices represent the cost per year to insure $10,000 of debt for five years. Argentina is in the most trouble, with a cost of $4,453 per year to insure just $10,000 of debt, followed by Venezuela, Lebanon, Egypt and Indonesia. Of the G8 countries, Russia has by far the highest default risk with a CDS price of $523. Japan, France, the US and Germany have the lowest default risk of the group of countries, but they have all spiked more than 200% this year.

Currencies

Interest rate reductions by a number of central banks, especially much larger-than-expected cuts by the Bank of England and the Reserve Bank of Australia, together with the expected impact of the lower rates on a specific country's economy, influenced currency movements during the past week.

Over the week the US dollar gained against the euro (+0.2%), the British pound (+2.7%) and the Swiss Franc (+1.8%), but lost ground against the Japanese yen (-0.3%), the Canadian dollar (-1.8%), the Australian dollar ( 1.2%) and the New Zealand dollar (-0.7%).

Commodities

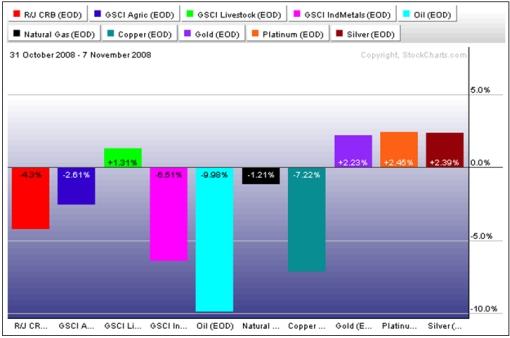

The negative implications of the deteriorating global economic situation on demand resulted in commodities remaining under pressure during the past week, with the Reuters/Jeffries CRB Index falling by 4.3%.

Precious metals bucked the trend and edged higher, with gold, silver and platinum all up by more than 2%. Platinum benefited from the closure of a South African smelter by Anglo Platinum, reducing global supply by 3%. The charts (gold shown below) seem to indicate that a rally could be in store for precious metals.

The following graph shows the past week's movements for various commodities:

Now for a few news items and some words and charts from the investment wise that will hopefully assist in keeping our portfolios afloat in the treacherous waters characterizing the investment landscape. Also remember what Elroy Dimson of the London Business School said: “Risk means more things can happen than will happen.”

That's the way it looks from Cape Town.

Source: Chicago Tribune

Financial Times: Obama and Biden take the stage

“President-elect Barack Obama was joined by Vice President-elect Joe Biden in Chicago's Grant Park, minutes after Obama clinched the presidency in a historic win.”

Source: Financial Times , November 6, 2008.

Charlie Rose: A conversation with Floyd Norris (The New York Times) about Obama and the economy

Source: Charlie Rose , November 6, 2008.

The New York Times: Obama seeks speedy action on economy

“President-elect Barack Obama called on Friday for the Bush administration and Congress to enact an economic-stimulus package, and he pledged to confront the country's economic crisis ‘head on' the moment he is sworn in on January 20.

“‘I do not underestimate the enormity of the task that lies ahead,' Mr. Obama said at his first news conference since his victory over Senator John McCain on Tuesday. He said he was certain that ‘some difficult choices' will have to be made.

“‘It's not going to be quick, and it's not going to be easy to dig ourselves out of the hole that we're in,' Mr. Obama said, declaring that he wants to see ‘a rescue plan for the middle class' and a further extension of unemployment-insurance benefits.

“The news conference here came immediately after Mr. Obama, Vice President-elect Joseph Biden and his newly named chief of staff, Representative Rahm Emanuel, met with the transition's economic advisory board – and as a fresh wave of news from Wall Street and Washington deepened the gloom hanging over the country's financial situation.

“The president-elect said he and his advisers would try to find ways to help the struggling automobile industry, and that he hoped to see enactment of an economic-stimulus package either before or soon after Inauguration Day.

“Mr. Obama announced his selection on Thursday of Mr. Emanuel as his White House chief of staff, a choice he said he made because Mr. Emanuel had ‘deep insights into the challenging economic issues that will be front and center for our administration.'

“In a long list of forthcoming appointments, aides said, Mr. Obama is acting with the greatest urgency toward choosing a Treasury secretary and is said to be considering Lawrence Summers, who held the post during the Clinton administration, and Timothy Geithner, president of the New York Federal Reserve Bank.”

Source: Jeff Zeleny and Jackie Calmes, The New York Times , November 7, 2007.

Bloomberg: Steve Forbes likes Volcker as next Treasury Secretary

“Steve Forbes, chief executive officer of Forbes Inc. and a former Republican presidential candidate, talks with Bloomberg in New York about US President-elect Barack Obama's top priorities, the possibility Paul Volcker will be named Treasury Secretary and outlook for an economic recovery.”

Source: Bloomberg , November 5, 2008.

The New York Times: A towering economic to-do list for Obama

“The dismal state of the economy helped decide Tuesday's presidential election. And it almost certainly will dominate the early days of the Obama administration.

“Few presidents have entered office with an economy in such turmoil. Reflecting worries that the worst may not be over, the stock market continues to languish, with a 5% decline on Wednesday, leaving it 35% below its peak last fall.

“The reasons are myriad: the financial system, though back from the brink, remains deeply troubled. Housing may no longer be in free fall, but plummeting values and rising defaults have impoverished many homeowners and burdened states with widening budget deficits. The once-mighty auto industry is on the verge of implosion.

“Consumers who piled up credit card debt are pulling back, a major concern because their spending helped power economic growth in recent years. And with unemployment widely expected to increase to 8% or higher, from 6.1%, consumers are likely to tighten their belts even more.

“Moreover, with upward of $1 trillion already pledged by the federal government to bail out the banking and housing industries, financing a growing deficit to address the problems could be difficult — and saddle the Treasury Department with high levels of debt for years to come.

“But even before President-elect Obama takes the oath of office, Democrats are likely to push his agenda with urgency, because the economy otherwise could worsen quickly — complicating the task ahead. ‘The cost of allowing an economy to flounder is very high in lost output and rising unemployment,' said James Glassman, chief domestic economist at JPMorgan.

“Click here for some of the crucial issues that economists say will test the new administration, and how it might address them.”

Source: The New York Times , November 5, 2008.

Bloomberg: Obama may spend on roads, bridges to stimulate US economy

“President-elect Barack Obama may put spending on roads and bridges at the top of his agenda for stimulating US economic growth.

“‘He's identified infrastructure as one of the ways to strengthen the American economy,' Janet Kavinoky, transportation infrastructure director for the US Chamber of Commerce, said in an interview. ‘So we would expect it to be on his list of actions both for the stimulus and longer term.'

“Obama was elected yesterday amid a global credit crisis and with the US in or heading into a recession that may be the deepest in more than 20 years. He promised during his campaign he would use infrastructure spending to create jobs.

“‘We'll create 2 million jobs by rebuilding our crumbling roads, schools and bridges,' Obama said in an October 13 speech in Toledo, Ohio, where he outlined his plan for reviving the economy.

“Obama has urged Congress to pass an economic stimulus bill immediately after the election. House Speaker Nancy Pelosi, a California Democrat, has said she wants spending on highways and other transportation infrastructure included in the next stimulus package.”

Source: Angela Greiling Keane, Bloomberg , November 5, 2008.

Jim Sinclair (Mineset): The future of markets with Obama at the helm

“There will be many forecasting market results of the election of President Obama. I suggest we wait to see his cabinet in order to look to the future with any degree of accuracy.

“What we do know is:

1. Many of the evil money ruler geniuses are out of the lime light.

2.Even if Wall Street is still pulling strings, this Administration will not have Paulson who jiggled every market on the planet fairly well.

3. The PTT team, if it exists, will be made up of lesser lights because the past Administration ruled that.

4. All the problems are still out there as virulent cancers that have spread out of control in the financial market and are not operable. Thank you all you OTC derivatives that up to now have not been singled out to accept blame. This could change but do not count on it.

5. You can count on fiscal stimulation as it is a tenet of how the Democratic mind moves.

6. You can count on higher taxes for Daddy Warbucks and reductions for the ordinary man who carries the Federal Budget money-wise.

7. You can count on an interesting period in terms of geopolitical challenges to the USA from their many enemies in order to size up the new leadership.

8. You can count on meaningless dialog with all those about to test the new Administration geopolitically.

9. You can count on gold at $1,200 and then $1,650.

10. You can count on the US dollar trading at USD .72, .62 and .52.

11. You can count on the reestablishment of social and economic safety nets.

12. You can count on the now shredded Constitution remaining shredded. Once power comes into an Administration it stays their permanently.”

Source: Jim Sinclair, MineSet , November 5, 2008.

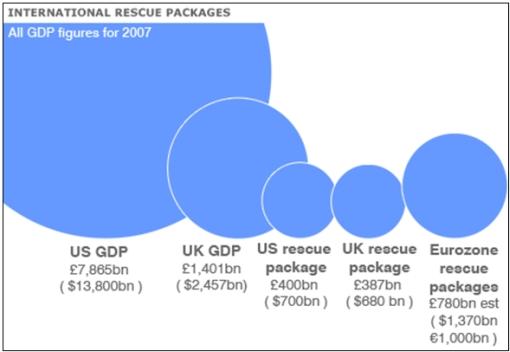

BBC News: Billion-dollar bail-outs

“Governments have spent billions of dollars on rescue packages, led by the US with its $700 billion rescue package.”

Source: BBC News , November 3, 2008.

Chicago Tribune: Programs taking shape to aid those facing foreclosure

“A month after passing a $700 billion bailout designed to benefit the reeling financial sector, the federal government is grappling with how best to directly help strapped consumers at risk of losing their homes to foreclosure.

“At the end of the third quarter, one in every 500 homes in Illinois was in some stage of the foreclosure process, according to RealtyTrac. The number of homes in foreclosure was almost 50% higher than in the same period last year.

“That pattern is playing out nationally, creating a sense of urgency because foreclosures not only affect troubled borrowers but also their neighbors, whose home values are reduced by distress sales.

“However, the complicated structure of mortgage financing, the fragile state of the lending industry, the voluntary participation by lenders in most programs and the fact some can't afford their homes regardless of the terms has delayed implementation of a rescue plan.

“For the past two weeks, the Federal Deposit Insurance Corp., Treasury Department and White House have discussed various programs but said little publicly.

“One proposal floated by the FDIC would assist 3 million homeowners in danger of foreclosure by offering up to $50 billion in government guarantees to lenders who modify mortgages. A plan was expected last week, but none was announced.”

Source: Chicago Tribune , November 5, 2008.

The Wall Street Journal: US weighs purchasing stakes in more firms

“The Treasury Department is considering using more of its $700 billion rescue fund to buy stakes in a broad range of financial companies, not just banks and insurers, after tentative signs of the program's success, according to people familiar with the matter.

“In focus are companies that provide financing to the broad economy, including bond insurers and specialty finance firms such as General Electric's, CIT Group and others, these people said.

“The possible expansion shows how much Treasury's rescue plan has morphed since it was first proposed in September. Treasury Secretary Henry Paulson originally unveiled a complex plan to buy up financial institutions' hard-to-sell assets such as mortgage-backed securities.

“That proposal has yet to get up and running, stymied by operational delays and beset by criticism. People familiar with the matter say Treasury may scrap part of that early plan – purchasing assets through an auction process – and instead purchase some of these distressed assets directly.

“Of the original $700 billion made available to Treasury, officials set aside $250 billion for equity investments. It has already invested $163 billion in a range of banks including some of the nation's largest, such as Goldman Sachs and Bank of America. That number will likely expand at the expense of the asset-purchase plan, but by exactly how much is unknown.

“‘We are looking at many ideas for strengthening the financial system and for restoring lending,' said Jennifer Zuccarelli, a Treasury spokeswoman. ‘We are weighing ideas and have made no decisions.'”

Source: Deborah Solomon, The Wall Street Journal , November 4, 2008.

Green Light Advisor: Hugh Hendry – don't bank on the bailout

Hugh Hendry, CIO of Eclectica Asset Management was invited to host Channel 4's Dispatches, a UK TV program ,‘Don't Bank on a Bailout', about the fallout from the credit debacle. Hendry travels throughout the City Financial District and then Wall Street.

Click here or on the image below for Part 1 of the video.

Click here for Part 2 of the video.

Click here for Part 3 of the video.

Source: Green Light Advisor , November 2, 2008.

Financial Times: Europe sets deadline to draw up reforms

“European leaders on Friday agreed the task of preventing future financial crisis should fall to the International Monetary Fund, but failed to set out any details of possible changes to the agency's role.

“Meeting at an informal summit in Brussels in preparation for next weekend's meeting of the G20 group of advanced industrial and emerging countries in Washington, they also set a 100-day deadline to draw up ambitious reforms to the financial system.

“These, they agreed, should be built around five principles: one of which would be that ‘no market segment, no territory and no financial institution should escape proportionate and adequate regulation, or at least oversight'.

“Gordon Brown, the British prime minister, used the summit to press other EU leaders to back fiscal stimulus measures to support recent interest rate cuts by the European Central Bank, the Bank of England and other central banks.

“France's president Nicholas Sarkozy, hosting the Brussels meeting, insisted afterwards European countries were united in advance of the G20 summit on how to reform the global financial system. ‘We will be defending a common position, a vision … for reforming our financial system,' he said.”

Source: Nikki Tait and George Parker, Financial Times , November 7, 2008.

BBC News: IMF cuts economic growth forecast

“The International Monetary Fund (IMF) has become even gloomier about the prospects for the world's economies.

“It is predicting that developed economies as a whole will shrink by 0.3% next year, having predicted growth of 0.5% less than a month ago. It would be the first time there has been an overall contraction in developed economies since World War II.

“Worst hit will be the UK, shrinking 1.3%, followed by Germany at 0.8% and the US and Spain contracting by 0.7%.

“Emerging economies have also been downgraded, with the forecast of Chinese growth down from 9.3% to 8.5%, India down from 6.9% to 6.3% and Russia down from 5.5% to 3.5% growth.

“The IMF is still expecting the overall global economy to grow in 2009, but it has cut its growth forecast to 2.2% from the previous estimate of 3%.

“‘Prospects for global growth have deteriorated over the past month, as financial sector deleveraging has continued and producer and consumer confidence have fallen,' the IMF said in its report.”

Source: BBC News , November 6, 2008.

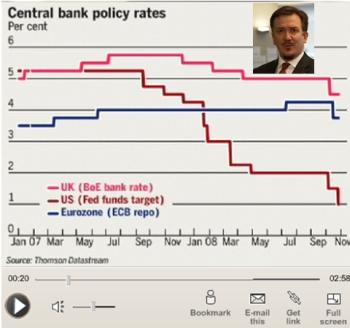

John Authers (Financial Times): Interest rate cuts all around

Click here for the full article.

Source: John Authers, Financial Times , November 6, 2008.

ABC: Shiller – “more tough times ahead for US”

Source: ABC , November 4, 2008.

Bloomberg: Fed's Fisher says US economy may slump through 2009

Source: Bloomberg , November 3, 2008.

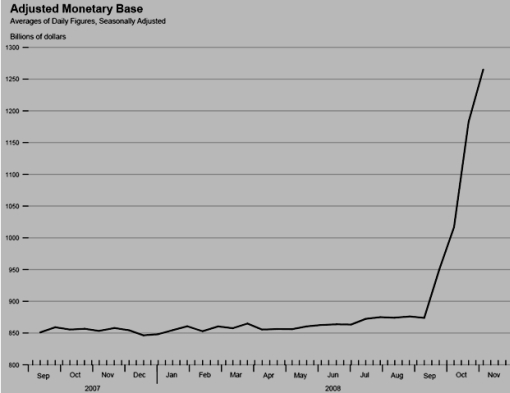

Bill King (The King Report): Fed's balance sheet

“The Fed's balance sheet continues to explode. For the week ended Wednesday it surged $182.91 billion to $2.111 trillion! Three months ago it was less than $900 billion! Now it is over 230% higher. Annualized this is Wiemar (more than 2600%)!

“Adjusted monetary base growth is Weimar-like, 785.7% annualized for two maintenance periods (four weeks).”

Source: Research Division, Federal Reserve Bank of St. Louis

Source: Bill King, The King Report , November 7, 2008.

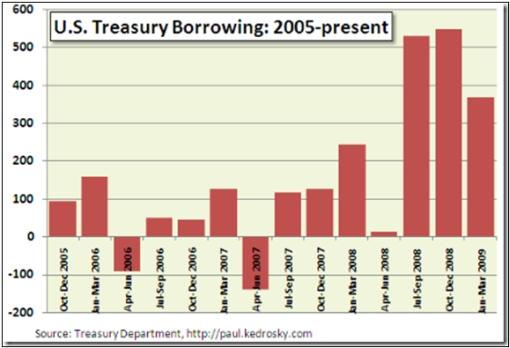

Paul Kedrosky (Infectious Greed): Treasury has huge capital needs

“While the US Treasury's current capital needs are undeniable, its just-announced Q4 fund-raising plans are epochal. Is it trying to fully pre-finance current plans, knowing full well that yields are going to rise as struggling US creditors find other, higher uses for the same capital over the coming months?”

Source: Paul Kedrosky, Infectious Greed , November 4, 2008.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.