Stock Market Staving Off Risk-Off

Stock-Markets / Stock Market 2022 Jan 05, 2022 - 07:21 PM GMTBy: Monica_Kingsley

Another daily rise in yields forced S&P 500 down through tech weakness – the excessive selloff in growth didn‘t lead buyers to step in strongly. More base building in tech looks likely, but its top isn‘t in, and similarly to the late session HYG rebound, spells a day of stabization and rebalancing just ahead. I‘m not looking for an overly sharp move, even if the very good non-farm employment change of 807K vs. 405K expected could have facilitated one. Friday though is the day of the key figure release – till then a continued bullish positioning where every S&P 500 dip is being bought, would be most welcome.

The same goes for high yield corporate bonds not standing in the way, and for credit markets to reverse yesterday‘s risk-off slant. Likewise the compressed yield curve could provide more relief by building on last few days‘ upswings in the 10- to 2-year Treasury ratio. VIX has been repelled above 17 again, and keeps looking ready to meander near its recent values‘ lower end.

That‘s all constructive for stock market bulls, and coupled with the fresh surge in commodities (and precious metals), bodes well for the S&P 500 not to crater soon again. Another positive sign comes from the dollar, which wasn‘t really able to keep intraday gains in spite of the rising Treasury yields. Cryptos though remain cautious (unlike precious metals which moved nicely off Monday‘s oversold levels – on a daily basis oversold), so we‘re in for a muddle through with a generally and gently bullish bias this week… until non-farrm payrolls surprise on Friday (and markets would probably interpret it as a reason to rise).

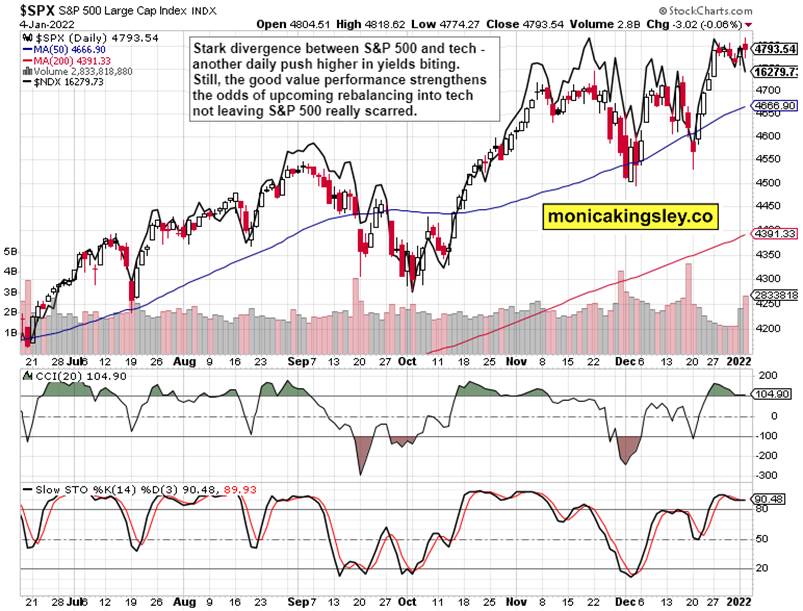

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

S&P 500 and Nasdaq Outlook

S&P 500 keeps respectably treading water, waiting for Nasdaq to kick in – odds are we won‘t have to wait for a modest upswing in both for too long.

Credit Markets

HYG is the key next – holding above yesterday‘s lows would give stocks enough breathing room, and so would however modest quality debt instruments upswing.

Gold, Silver and Miners

Gold and silver are leading miners, but the respectable daily volume makes up for this non-confirmation. The table is set for the floor below gold and silver to hold, while a very convincing miners move has to still wait.

Crude Oil

Everything is ready for the crude oil upswing – even if oil stocks pause next, which can be expected if tech stages a good rally. Until then, it‘s bullish for both $WTIC and $XOI.

Copper

Copper is keeping the upswing alive, and any pullbacks don‘t have good odds of taking the red metal below 4.39 lastingly. Still, copper remains range bound for now, and the pressure to go higher, is building up.

Bitcoin and Ethereum

Bitcoin and Ethereum lost the bullish slant, but didn‘t turn bearish yet – this hesitation is disconcerting, but it would be premature to jump the gun. It‘s still more likely that cryptos would defy the shrinking global liquidity, and try to stage a modest rally.

Summary

S&P 500 internals reveal tech getting hurt yesterday, and at the same time getting ready for a brief upswing of the dead cat bounce flavor. And if HYG kicks back in, odds increase dramatically that the tech (and by extension S&P 500) upswing won‘t be a dead cat bounce (please note that I‘m not implying vulnerability to a large downswing) – that‘s my leading scenario, which should materialize by Friday‘s market open. Yes, I‘m looking for non-farm payrolls to be well received once the dust settles. Till then, commodities are paving the way for further stock market gains, with precious metals turning out not too shabby either.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for both Stock Trading Signals and Gold Trading Signals.

Thank you,

Monica Kingsley

Stock Trading Signals

Gold Trading Signals

www.monicakingsley.co

mk@monicakingsley.co

* * * * *

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.