Gold Golden 'Moment of Truth' Is Upon Us: $1,400-Plus or Not?

Commodities / Gold & Silver 2019 Jun 18, 2019 - 06:18 PM GMTBy: The_Gold_Report

With the precious metals markets range-bound and driven by forces beyond his control, sector expert Michael Ballanger turns his contrarian eye to the past. With gold enjoying its best week of the year, with the Daily Sentiment Index charging northward, with the Relative Strength Index (RSI) pressing 72 for the GLD, with the RSI for GDX pushing 75, and finally, with the newsletter community all falling on top of themselves with self-laudatory backslaps, I think it is time to adopt the contrarian view and step back.

With the precious metals markets range-bound and driven by forces beyond his control, sector expert Michael Ballanger turns his contrarian eye to the past. With gold enjoying its best week of the year, with the Daily Sentiment Index charging northward, with the Relative Strength Index (RSI) pressing 72 for the GLD, with the RSI for GDX pushing 75, and finally, with the newsletter community all falling on top of themselves with self-laudatory backslaps, I think it is time to adopt the contrarian view and step back.

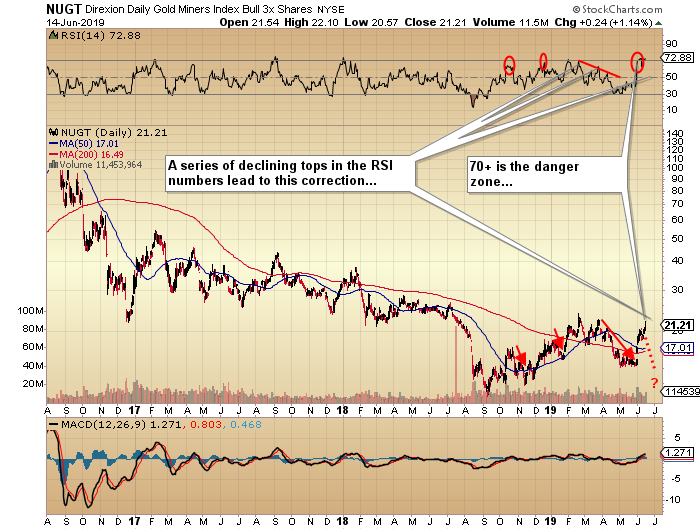

It was less than five weeks ago, with gold and the miners all coming off sharply oversold conditions (RSI in the mid-high 30s), that I wrote that "carpe diem" in reference to ownership of GLD calls and my two favorite leveraged miners, NUGT and JNUG. Sure enough, JNUG has moved from $6.50 to $9.50 and NUGT from $14.50 to $22.10, while the GLD July $120 calls rocketed from $2.20 to $7.60. (Note: I did not get "top tick" for any of them, but did bank yet another decent 40% return on the miners, and a double and a half on the GLD calls).

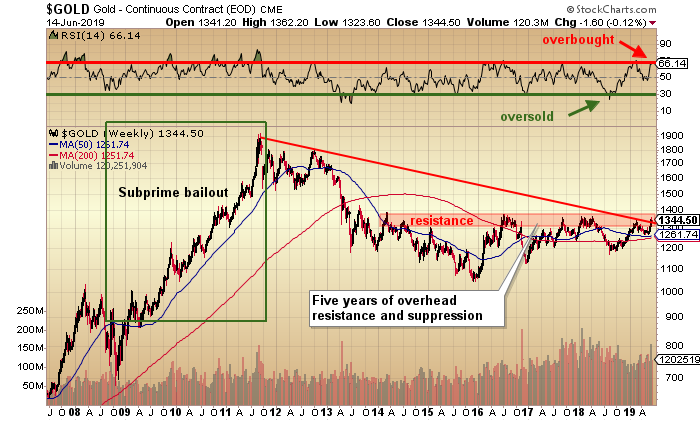

The point is that while I would love for gold to break out of this bullion bank headlock at the $1,350–$1,375 band of resistance, history has proven it to be a formidable obstacle and one that you absolutely must face.

Here are a few charts illustrating my point:

First, the GLD, hated by many, traded by most, and an excellent proxy for the "paper gold" market, the second-most corrupt market in the world and runner-up to the most corrupt market in the world, the Comex ("Crimex") futures market in Chicago. Right up there beside it is the HUI, the unhedged gold miners index that represents the vast universe of gold mining entities around the world, and another great proxy for a vastly hated group of companies whose collective market cap losses in the past eight years has been colossal.

Many, many new millionaire investors have sprung up from owning these lifestyle-preserving dinosaurs, having been formerly billionaire investors prior to taking the gold miner plunge. The HUI has had no fewer than six rallies since the top in August 2016, but each rally was followed by new lows, with the most recent low coming last September. The RSI and moving average convergence-divergence (MACD)/histogram combo currently reside in "overbought" territory, and if history proves as reliable today as it was at every other visit to the $1,350–$1,375 resistance zone, we should don the personalities of the hideous bullion bank traders and sell that which we own in the paper markets to adopt their illicit yet enormously profitable tactics and executions.

The next two charts are my favorite vehicles for dice-rolling. . .er. . .speculation in the miners because they are extremely liquid and they report to oversold and overbought conditions appropriately to the extent that you can buy 100,000 shares with an RSI around 30, as I did in May with JNUG and NUGT, and then let it fly when the RSI exceeds 70, as I did last week. Because I subscribe to the view that most successful traders earn their stripes by always selling too soon, I was a week early in pulling the JNUG and NUGT triggers, but as I never buy 100% positions in one fell swoop, I also never sell 100% positions in the same manner. I scale in and I scale out because no one indicator is infallible. All data is freely available to literally everyone, but I have learned over the many years of trading (and losing) that it is the interpretation of the indicator, as opposed to the level, that defines the trade's set-up. Please allow me to elaborate.

George Soros once wrote that he would experience back pain whenever he entered a trade that was suspect. Rather than rejecting it as a psychosomatic illusion, he learned to trust the back pain as a definable premonition of unfavorable outcome. It was his brain telling him to exit the trade by way of his body and despite the voodoo-ism in the explanation, I totally agree with him.

On Friday the 14th, I arose from slumber at roughly 5 a.m. and proceeded to check the markets while luxuriating in some lovely new 400-thread sheets recently introduced to me by my partner. As I had already started to exit my leveraged gold and gold miner positions, I was stricken with a sharp pain of panic as gold was trading in the $1,355–$1,360 range. Not only had I gone on record as a seller of the move to $1,350, I was tweeting out all week warning after warning in the $1,340–$1,350 range. So to say that the June 14 3:00 a.m. Globex print at $1,361.20 was problematic is an understatement.

Nevertheless, here is the tweet I sent out: Initiating 50% position in GLD July $127 puts @ $1.42...Lord hates a coward.

That was delivered at 11:30 a.m.. By 3:00 p.m. gold had dropped $14 per ounce and my puts traded up to $1.94, finally closing at $1.85. I am currently looking for a $40–$60 drop in gold and an RSI in the high-20s/low-30s by mid-August. If that occurs quickly, the puts will trade $4.50–$6.50 and I will be a reluctant hero. Repeat—a reluctant hero, and here is why.

If you had asked me in 2001 what I thought would drive gold to $5,000 per ounce, I would have responded with a list of economic, financial and geopolitical events such as terrorist attacks, war, debt defaults, stock market volatility, currency crises, accelerating inflation rates and fraud, all driving investors to the time-tested safe havens of precious metals. It all started with the 9/11 Twin Towers attack in NYC, and then escalated from there, taking us through nearly two decades of turmoil in all of the aforementioned areas.

Well, ladies and gentlemen, we have had multiple historical price drivers for precious metals during that period but what we have also seen is a massive, coordinated and fraudulent campaign to control investor appetites across a wide spectrum of asset classes, demographics and borders. The new rock stars of the 2000s are now central bankers, whose mega-maniacal actions move markets and create or destroy trillions of dollars of citizenry wealth with their utterances, written words and, more recently, social media "bulletins." It is as if central bankers from all Western nations met in Basel in 2001 and decided where they had the greatest collateral exposure (think real estate and bonds), then proceeded to map out a plan designed to foster confidence in stocks, bonds, U.S. dollars and real estate while crushing investor demand for hard assets like silver and gold and finally cryptocurrencies, whose fate was sealed in late 2018 with its listing on the "Crimex," fully endorsed by the Commodity Futures Trading Commission (CFTC).

I fully expected this turmoil back in 2001, after the dot.com bubble popped, sending an entire tech-loving generation to the poorhouse. But the problem was that the playbook, which had included fifty years of knowledge, omitted the new rules concerning cause and effect. By example, if you think it is going to rain, you take steps to stay dry by way of rain gear and umbrella; if you think that the U.S. banking system is going to be vaporized through greed and malfeasance, you load up on gold.

However, if it starts to rain and an invisible hand removes your rain gear and destroys the umbrella, you are suddenly drenched. You correctly predicted and prepared for the event (rain), thus identifying the cause, but despite such preparations protecting you for the past fifty years every time it rained, you got wet. The effect was distorted by forces over which you had no control. Similarly, despite correctly identifying multiple causes that should have driven gold to $5,000/ounce, forces over which I had no control conspired to distort investor demand, and instead of stocks crashing and precious metals soaring, the exact reverse occurred, beginning in 2011 and continuing to this very day.

So when I use the term "reluctant hero," it is because I have trained myself to think and act like a bullion bank trader, complete with unregulated license and unrelenting bravado. Aligning one's trade setups to coincide with the Commercials is by no means a guarantee of profit, but refusing to take the other side of a bullion bank trade setup does, at the very least, dramatically improve one's probability of success.

The downside is that acting and behaving like a bullion bank thief is an unhealthy and unrewarding exercise. You run the risk of assuming that 5,000 years of history confirming the wondrous utility of gold ownership will never return, and that the only history that matters is that which began on December 23, 1913, on Jekyll Island. The financial risk is borne out the moment you wake up and gold is at $1,450, and there are no offers and your trade alignment with the bullion banks has suddenly and viciously bankrupted you. And with what is happening today around the world, it is a serious risk.

This chart is an illustration of the massive response by gold to the subprime bailout in 2009, and the subsequent smothering of any type of response whatsoever from 2011 until today. As of the close of business on Friday, June 14, gold went out just below that formidable band of resistance at $1,350–$1,375, and I expect it will be a battle for the ages as pro-gold forces wage war with the bullion bank behemoths. Judging from the open interest surge late last week, it appears as though it is more than likely a repeat of past interventions, with downside risk to $1,315–$1,320. However, gold is going higher over the longer term and that's why I maintain positions in the portfolio shown below.

The cash position currently at around 27% is the total profits from trades made in 2019 less two hedges put on last week, the most impactive to date being the purchase of 100 Goldman Sachs July $180 puts in May for $2.20, and then sold in June at $6.60 for a 200% return or $44,000 (U.S.) in profits. You will note that I do not trade physical gold and silver, and I rarely trade the unleveraged ETFs (GDX and GDXJ), while using the leveraged ETFs (JNUG and NUGT) as trading vehicles and the DUST as a hedge. The remaining cash will be deployed on a correction in gold, which I expect next week, or in the event that the bullion banks get caught short and we scream through $1,375.

As can be seen from the GGMA portfolio, I stand to benefit far more on a gold breakout that lasts rather than from a corrective move favoring the bullion banks.

Damn the torpedoes and pass the tequila. Let's see what this week brings.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Getchell Gold Corp. My company has a financial relationship with the following companies referred to in this article: Getchell Gold Corp. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold Corp., a company mentioned in this article.

Charts courtesy of Michael Ballanger.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.