Risk of ‘World War’ between NATO and Russia on Ukraine as Yemen Bombed

Commodities / Gold and Silver 2015 Mar 27, 2015 - 12:52 PM GMTBy: GoldCore

- World sleep walking from ‘Cold War’ to ‘Hot War’ and new World War

- World sleep walking from ‘Cold War’ to ‘Hot War’ and new World War

- U.S. resolution to supply Ukraine with lethal weaponry passed

- Russia warns such moves would “explode the whole situation”

- Minsk agreement remains intact – little justification for escalation and ignoring EU allies

- US continues to act as only global superpower despite powerful Russia and China and new multi-polar world

- Hubris could lead to a new World War

Geopolitical risk has escalated sharply this week after the Saudi bombing of Yemen and the U.S. House of Representatives voting overwhelmingly for the President to provide offensive weaponry to the Ukrainian army.

Both are likely to result in sharp escalation in tensions between NATO and Russia and see an intensification of war in Eastern Europe and the possibility of a regional war in the Middle East.

The move is concerning as European countries who have a real interest in maintaining stability in Ukraine – Germany and France, who are Europe’s de facto leadership, and Russia – have already restored a degree of stability through the Minsk agreement. Germany and France pointedly excluded the U.S. from the process.

The resolution comes despite Russia’s Deputy Foreign Minister Sergey Ryabkov having previously warned in February that such a move would be a “major blow” to the Minsk agreements and would “explode the whole situation.”

The second Minsk Agreement – brokered between Germany, France, Russia and Ukraine last month – has remained largely intact. The head of the reasonably independent Organisation for Security and Co-operation in Europe said earlier this month the the ceasefire in Ukraine was holding. The OSCE confirmed, yesterday, that the withdrawal of heavy arms by both sides of the conflict was “ongoing” according to the Kyiv Post.

Therefore, there would appear to be little justification for the U.S. to send high tech arms to Ukraine at this time especially on the pretext of restoring stability.

The passing of such a resolution highlights the insulated nature of U.S. politics. U.S. policy makers continue to labour under the delusion that the U.S. is still the only global superpower.

The reality is that the U.S. grows more isolated by the day. While the rising superpowers of the East work tirelessly to forge international ties through trade and development agreements, the U.S. continues to act unilaterally and forcefully – as it has since the collapse of the Soviet Union.

The Eastern block does not need war. Its economic influence grows daily – as demonstrated most recently by a whole swathe of European allies joining the new Chinese-led Asian Infrastructure Investment Bank despite pressure from the U.S. not to do so.

On the other hand, it would seem that many U.S. policy makers regard war as an opportunity to re-exert their declining influence.

The U.S. may or not remain a superpower. It has the population, landmass and resources. It has friendly neighbours and is practically impenetrable to attack. However imperial overstretch has bankrupted many an Empire.

It needs to come to terms with the fact that there is a new world order emerging – and not necessarily the one that was envisioned following the collapse of the Soviet Union.

Until its politicians overcome their hubris the world will continue to grow more and more unstable as it lurches closer to another World War. What the catalyst will be which triggers another World War is difficult to tell. There are many options to choose from.

Gold is a safe haven asset and an essential store of value that has protected people from war and economic uncertainty throughout history. It remains prudent for investors and savers to have an allocation to physical, allocated gold.

HOW TO STORE GOLD BULLION – 7 KEY MUST HAVES

MARKET UPDATE

- Gold looks set for second consecutive week of gains

- Japan’s QE fails – Returns to zero inflation

- ‘Master of the universe’ central bank speeches today

- ETF and COMEX holdings fall as gold flows East

- JP Morgan to be part of new gold ‘fix’

- Greeks pull €8 billion from banks

- “No one knows how to solve the situation in Greece”

- Bundesbank warns debt in euro zone has entered “danger zone”

- UK and Irish house prices are falling … again

Today’s AM fix was USD 1,198.00, EUR 1,106.70 and GBP 805.32 per ounce.

Yesterday’s AM fix was USD 1,209.40, EUR 1,097.26 and GBP 809.23per ounce.

Gold climbed 0.65 percent or $7.80 and closed at $1,203.40 an ounce yesterday, while silver rose 0.47 percent or $0.08 at $17.05 an ounce.

Gold in U.S. Dollars – 1 Week

In the end of day trading in Singapore, gold prices climbed 0.3 percent to $1,199.95 an ounce after reaching a high on Thursday of $1,219.40. Gold surged after news of the bombing in Yemen but prices were capped at the $1,220 level prior to a retracement of much of the initial gains.

Oil prices jumped over 6 percent at one stage and stock markets worldwide slumped yesterday after Saudi Arabia and allies carried out air strikes, which fueled worries internationally that global energy shipments may be put at risk.

The U.S. claims that Saudi Arabia kept some key details of its military action in Yemen from Washington until the last moment. Saudi Arabia’s more aggressive role is said to be in order to compensate for perceived U.S. disengagement. U.S. President Obama’s Middle East policy increasingly relies on proxies rather than direct U.S. military involvement. He is training Syrian rebels to take on the government of President Bashar Assad and this week launched air strikes to back up Iraqi forces trying to retain the city of Tikrit.

All of this has the real potential for ‘blowback’ in the classic sense and risks leading to a hot war involving Russia.

Gold pulled back today as traders took profits after a seven-day rally in the yellow metal. In spite of the price dip gold is expected to rack up a weekly gain of around 1.5 percent. Gold looked overvalued after the 7 days of price gains and the final rally to over $1,219/oz. The last winning streak of 7 consecutive days in a row was in August 2012. Gold appeared overbought and was due a correction.

As tends to happen, gold is now testing previous resistance at $1,200/oz which may become support.

Gold may have a second week of gains today and if this happens we would be constructive on further price gains next week. Momentum is a powerful force in markets and the recent gains could see technical traders pile in the long side pushing prices higher next week.

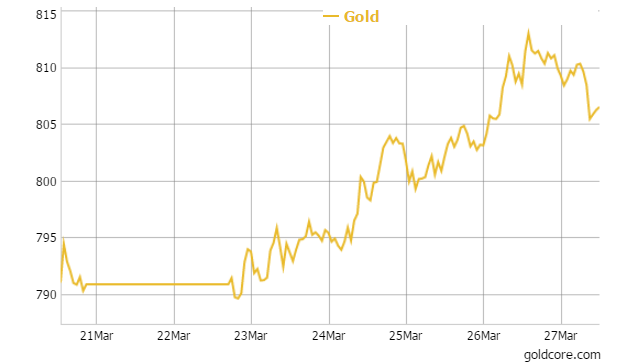

Gold in GBP – 1 Week

However, a lower weekly cose today could lead to sharp selling on futures markets near the close today and at the open in Asia which could push prices lower.

The question is whether the recent rally is another flash in the pan for gold or the start of a more meaningful rally in prices. We believe it is too soon to tell. However, we are confident that gold is in the process of bottoming prior to further gains in the coming months.

Japan has returned to zero inflation after recently emerging from recession, once again highlighting how ineffective QE has been at creating a real, sustainable economic recovery.

It’s a day of ‘master of the universe,’ central bank speeches as both Bank of England governor Mark Carney and Fed chief Janet Yellen preach their ultra loose policies and certain market participants lap up the ‘Gospel according to Mark’ … and Janet. Central bank believers will be watching for indications of their position on rate rise timings and their crystal ball view on the economies of the UK and US respectively.

U.S. GDP estimates for the fourth quarter are forecast for an upward revision from 2.2 per cent to 2.4 per cent on the back of an increase in consumer spending.

Yesterday saw a huge withdrawal of 5.97 tonnes from the world’s largest gold ETF, New York-listed SPDR Gold Shares. The nearly 6 tonne fall to 737.24 tonnes on Thursday, its lowest level since January.This month’s outflow from the SPDR has totalled just over 34 tonnes so far, the largest of any month since December 2013.

Over on the COMEX withdrawals continue. Earlier this year, the COMEX had 303 tonnes of total gold inventories. Yesterday the total inventory fell to 248.27 tonnes. This is a loss of 55 tonnes over that period and lately the withdrawals have been intensifying. Gold continues to flow from the West to East.

JPMorgan will be one of seven participants in the LBMA gold price according to ICE as reported by Eddie van der Walt in Bloomberg.

JPMorgan is to be among seven companies able to participate in LBMA Gold Price benchmark, ICE said today in statement published online. Other participating banks are Barclays, Goldman Sachs, HSBC, Bank of Nova Scotia, SocGen and UBS.

The new LBMA gold price has all the hallmarks of the old fix with just a few banks taking part in it and little participation from large players in the industry – miners, mints and refiners. Also it is noteworthy that there is no non Western banks taking part in the new gold fix. None from Africa, South America or Asia and none from China where there has been speculation of involvement in the new fix.

The crisis in Greece looks set to escalate in the coming days. Greek bank deposits plunged to an almost 10 year low in February as some €8 billion ($8.7 billion) were withdrawn from lenders, amid rising political uncertainty and worries over the country’s possible exit from the eurozone.

Total deposits fell to €152.4 billion euros in February, down from €160.3 billion in January, data from Greek central bank showed yesterday. This is the lowest level since June 2005.

Greece is hurrying to compile a list of economic overhauls that satisfies its creditors and secures desperately needed euros, as it runs increasingly low on cash and debt payments loom.

Officials in Greece’s new government, led by the leftist Syriza party, aim to submit a list of overhauls by Monday at the latest, officials have said. Greece hopes that eurozone finance ministers can meet and approve the country’s overhaul programme by next Wednesday.

Austria’s Finance Minister Hans-Joerg Schelling admitted today that “no one knows how to solve the situation in Greece”.

“We have a crisis of trust with Greece. Every day something is agreed upon and the next day it’s invalid,” Mr Schelling said speaking to the Klub der Wirtschaftspublizisten, a group of financial journalists in Vienna.

The head of Germany’s Bundesbank has warned debt in the euro zone had entered the “danger zone” and called for banks’ exposure to the debt of individual countries to be capped.

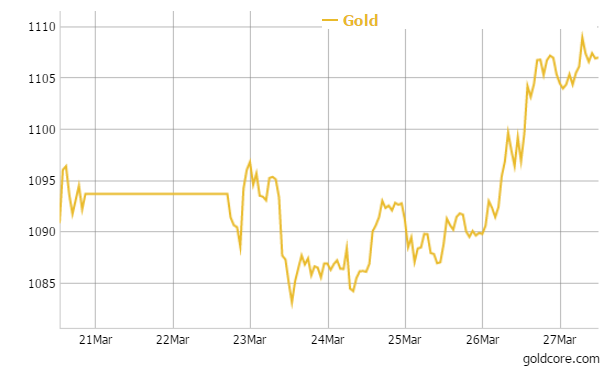

Gold in Euros – 1 Week

He is opposed to more emergency funding for Greece, accusing Athens of gambling away “a lot of trust”.

Speaking to the weekly Focus magazine Jens Weidmann said: “Until the autumn, an improvement in the economy had been discernible. But the new government has gambled away a lot of trust.”

“I am opposed to an increase in the emergency loans,” Mr Weidmann, who also sits on the European Central Bank’s decision-making governing council, said.

UK and Irish house prices are falling. The UK’s Nationwide house price index has revealed a seventh consecutive month of a slowdown in the UK property market. House price falls in central London have start to spread out across the capital to South West London.

In Ireland, property prices fell again in February. Residential property prices fell by 0.4 per cent nationally last month, with the decline in Dublin rising to 0.7 per cent, according to latest official figures. Results show more than 2 per cent has been wiped off the value of homes in the capital since the beginning of the year.

In London in late morning trading gold is at $1,201.73 or down 0.30 percent. Silver is at $17.24, up 0.23 percent and platinum is $1,142.70 down 0.72 percent.

This update can be found on the GoldCore blog here.

Mark O'Byrne

Director

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.