U.S. Shale Oil is the New Swing-Producer: Output Forecast to 2020 Will Make Saudi Arabia Very Happy

Commodities / Fracking Dec 01, 2014 - 11:15 AM GMTBy: Andrew_Butter

According to Reuters and CNN...and others, “OPEC” has declared war on shale-oil drillers in America.

According to Reuters and CNN...and others, “OPEC” has declared war on shale-oil drillers in America.

http://www.reuters.com...

That’s a serious accusation. In the not too distant past whole countries were bombed back into the Stone Ages for lesser transgressions!! Saudi Arabia was the only OPEC member to forcefully advocate not cutting back, so for “OPEC” read “The Saudi’s”. Bomb-Bomb-Bomb aside, it’s hard not to wonder whether or not a collective schizophrenia has descended on the talking-heads....“Saudi’s pumping more so America pays less...that’s terrible news, because shale oil will suffer**!!”....”Saudi’s pumping less...that’s terrible news, because hard-working -taxpayers will pay more for gasoline, and we will have to borrow more money from foreigners**!!” Can’t win.

What a lot of people don’t know...apparently, is the shale oil business model is completely different from traditional oil-fields where development takes three-to-five years; and payback on CAPEX is six-years after you start pumping, if you are lucky...but the well can deliver for thirty-years. By contrast here is how shale-oil wells deplete:

Source: The Shale Oil Boom: A U.S. Phenomena, Leonardo Maugeri,

Harvard Kennedy School, BELFER CENTER, June 2013

http://belfercenter.ksg.harvard.edu/files/The%20US%20Shale%20Oil%20Boom%20Web.pdf

With shale-oil, production is all about drilling intensity. Payback on CAPEX for a productive well at $90 Oil Price is typically one-to-two years and the selling price for the first two years is normally hedged before you drill.

The big difference is that decisions on GO/No-GO on a new well have a two year horizon. It’s a relatively low-risk play apart from the fact blowouts are much more common than conventional drilling. The more you drill in an area, and you drill a lot, the more you know about the geology; and the up-front costs of each decision are miniscule compared to BIG OIL. Leonardo Maugeri puts it this way (I paraphrase), BIG OIL is like deploying an army – shale oil is guerilla war.

So what is likely to happen to the U.S. shale-oil industry if oil prices hover around $70 for some time?

Well first of all, what’s NOT going to happen is they will turn off the taps and sulk. “Payback” on a shale oil play is hedged. Right now the owners of wells that have not paid-back don’t care what the price of oil is. And with an OPEX of about $10 per barrel, sure they would prefer $110 but they’ll settle for $70, or even $40 for the oil that comes out of holes that did pay-back.

What matters is how many new wells get drilled?

Break-even for drilling a new (or catch-up) shale oil well has fallen to an average of about $57 WTI according to IHS, a research company. Continental Resources says it can make a profit at $50 and IEA says Bakken remains profitable at $42. What does that mean? In BIG OIL “break-even” is the price at which you get pay-back in six to ten years, for shale oil it’s the price you get payback in one-to-two, max three, years. Allowing for a margin on top, that says perhaps 50% of what could profitably be drilled at a $100 oil price will be drilled at a $65 oil price.

Running Leonardo Maugeri’s numbers on the depletion against EIA numbers for monthly shale-oil output, it looks like in 2014 the total amount of new production brought on line was about 1.7 million barrels per day per year. Do multivariate analysis of the past ten years with {Oil-Price} and {Total Production Last Year} as explanatory variables (last-years production is a measure of how much land was grabbed and the amount of investment in infrastructure that was done), and you get a pretty decent model (units are new production in thousand barrels per day in the year in question):

Prediction #1: In 2015 total new shale oil wells in U.S. will deliver average 2.3 million barrels per day, and total U.S. shale oil output will be 6.0 million barrels per day....regardless of what is the price of oil...unless it goes down below the OPEX which is about $10.

So once all the wells currently being drilled (and hedged); have been drilled; new production is likely to come on-stream at a rate of about half of what made sense in 2015 (after hedging), if oil prices stay in the range $60 to $70. In other words about 1.15 million barrels per day.

So the next big imponderable is how long will that be?

Prediction #2: Oil prices will average about $70-to-$80 (Brent) until November 2018, at which point they will climb up to $95-to-$100 (Brent) depending mainly on the growth of world GDP (nominal). The logic for that is explained in an article put out in December 2010 which correctly predicted that if oil prices went to $110 (Brent) that would be followed by a slump to $67 (Brent)...that’s what happened...and it also predicted that the time-scale of the slump would be about the same time as prices stayed above $90, which is what this prediction says: http://www.marketoracle.co.uk/Article24849.html

Run the numbers and this is what you get, disaggregated by “vintage”, so when the chart says “2012” that’s the production of wells drilled in 2012:

That says U.S. shale oil producers will pump 2.0 million barrels more in 2015 than they did in 2014; which is about how much oil Venezuela wanted OPEC to take off the table!!

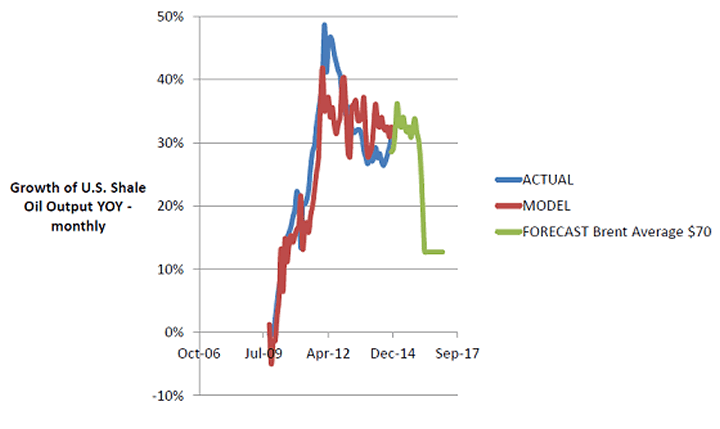

Looking at that another way, this is a plot of Year-on-Year change in U.S. shale oil output (source EIA), the model is simply Brent-lagged-one year, the R-Squared on that is 75% (P<0.0001).

The correlation underscores how important the price of oil is to U.S. shale oil drilling...and because of the rapid depletion – production. If the drillers can hedge, they drill, if they can’t they traipse down to the saloon and play country-music to each other.

The projection says after a year or so – growth with drop to about 13% of Brent averages $70, that’s a slightly higher output number than the previous analysis.

So U.S.A., the world’s shale-oil expert, is now the world’s “swing” producer.

If prices goes down, production goes down...automatically; if prices go up; production goes up. So U.S.A can be “oil-independent” so long as the price stays more than $90 and the shale-oil drillers can hedge at that price for two years. And so what, if the price is $65, who cares, U.S. will spend $100 billion less a year importing oil.

The Saudi “conspiracy”?

Leaving aside the popular press’s antipathy to Saudi Arabia, it is eminently possible the reason oil prices finally crashed from their unreasonably high level, was not a Machiavellian scheme instigated by Saudi Arabia, and more likely had something to do with the increasing demand from U.S. shale-oil producers to hedge the part of their production that was necessary for their payback on CAPEX.

No one can blame the Saudi’s for that. And, by way of a reality-check, although everyone likes to say they are the “swing-producer”, they haven’t played that game, at least with any real sense of enthusiasm, since they got completely burnt in 1988. That’s ancient history, a fairy story. Here is a chart of Saudi annual oil production compared with the oil price since 2000:

You can squint at that graph whichever way you like. But even if you hold it upside-down it’s hardly a smoking gun for the theory that the Saudi’s have been manipulating the price. Here’s a plot of a multivariate regression with {World-oil production} and {Saudi percentage share} as explanatory variables for “Predicted Saudi Oil Production in Thousand Barrels per day”:

That says over the past fifteen years, you could predict what the Saudi’s would produce with an accuracy of 10% at the 95% confidence limit (P<0.0001*) from just two variables. And significantly “Price” is not a statistically significant explanatory variable either the year before, the year in question, or the year ahead (t= 0.4). In other words – for the past fifteen years, the Saudi’s have just pumped 13% of the world’s oil production – come rain or shine.

Saudi Arabia got its reputation as a “Swinger” in the 1980’s – the history of that is illustrated below:

In brief – in the mid-eighties the rest of OPEC persuaded the Saudi’s to “swing” – then they (OPEC) cheated. By 1986 Saudi was producing less than half what it could. Then the North Sea started coming on line, the Iran-Iraq War ended, and the world was swimming in oil. In 1992 the Saudi’s said – “this “swinging” thing is a real bad idea”, and they told OPEC to take a running jump, and started pumping to get 13% of the World market share. Yes – once-upon-a-time, Saudi Arabia was a “swinger”; then they grew up. But still, the talking-heads keep repeating like a mantra, that the Saudi’s are “swingers” and they are manipulating the market. Their theory is presumably that if they keep saying that, over and over again...it will become the truth.

If the talking-heads are suggesting “someone” should push up oil prices by limiting production, GREAT!! All they need to do is persuade ALL of the oil producers in the world to cut production by...5%...or 10%....or 15%. If they or “someone” manages to do that, then based on the hard historical evidence of the past fifteen years, the Saudi’s will gladly follow suit.

What the Saudi’s are not doing, which is why everyone is accusing them of “conspiracy”, is making any effort to persuade ALL the other oil producers in the world to cut production. That’s not going to happen; because the only producer that will be cutting back production will be U.S.A. and that’s only a cut in what they “could” have been producing, in 2016, if oil prices stayed at $100.

Here’s a “helpful suggestion”... perhaps U.S.A. should consider joining OPEC so they can sit on the same side of the table as the Venezuelans and the Iranians and lambast Saudi Arabia for not being a “team-player”? That way they can re-start the exponential growth of the shale-oil industry which was set, if the trend-line is correct, to be producing easily 15 Million barrels per day by 2020.

Meanwhile in Saudi Arabia

The Saudi’s have been remarkably open and consistent about their position. For ten-years, they have been telling anyone and everyone who would listen what they think is the correct price of oil; that (a) their customers can afford and (b) provides a reasonable incentive for bringing-on new oil to replace what got pumped.

- When it shot to $145 in 2008 They said the correct price was $75

- When it plunged to $35 in 2009 They said the correct price was $80

- When it jumped to $85 in 2010 They said that’s about right

- When it rocketed to $110 They said the correct price was $90

- Now They are saying the correct price is $95

It is (perhaps) reasonable to ask, “If the Saudi’s think the correct price of oil today is $95 then why is it $65?” The reason is that four-years of prices being higher that what Warren Buffet calls the intrinsic value, accountants call Fair Value, and others call the Fundamental, leads like day follows night to what the Austrian Economists call mal-investment.

That’s another word for making an investment without doing proper research or doing your sums properly....which is another word for incompetent, bonkers, or both. That’s what the Saudi’s are worried about.

The Saudi’s are not worried about shale-oil drillers, because by definition a shale-oil driller is neither incompetent, nor is he bonkers. He needs a one-to two year payback to make money – so he can’t dress up his business-model with fancy dreams of what might happen in fifteen years. If he can hedge, he can get the finance; if he can’t then he’s sitting on the bench.

Not so with traditional oil-fields, in that business model, regardless of what were your planning assumptions for the price of oil over the fifteen-years you will get payback on your CAPEX from when you start to spend big money, once you spent the money, there is no turning-back, you have to pump, regardless of what the price is, until you paid off the loans. And you can’t hedge the oil price fifteen years down the road.

That’s what happened with North Sea oil which was planned and initially developed when oil prices were made artificially high because of the Iraq-Iran War. Then as soon as they were up and running; and the big part of the CAPEX had been spent, the war stopped. And for the next twenty years they pumped oil pretty-much at break-even when prices dropped through the floor due to a huge over capacity, as is explained here: http://www.marketoracle.co.uk/Article24849.html

That was, in retrospect a “Mal-investment” on a huge scale, and that is what the Saudi’s are worried about. The only news worth reporting at the OPEC Meeting on Thursday was (a) the Saudi’s didn’t change their minds for ten years, and (b) forget about ancient history, since at least 2000, they never changed their oil production to “swing” the prices. So why should they start now?

So what’s their game?

What they are acutely worried about is incompetent and often completely corrupt state-owned oil companies, making stupid investments based on the notion that “Oil Prices Never Go Down”, and that the only way from $110 Brent is up.

There are four good reasons why the correct price for oil (Brent) today, is $95:

- That’s what the Saudi’s say it is – they should know, after all they have a reputation as “swingers”

- That is the marginal break-even cost plus profit of the latest technology for replacing oil (shale-oil)

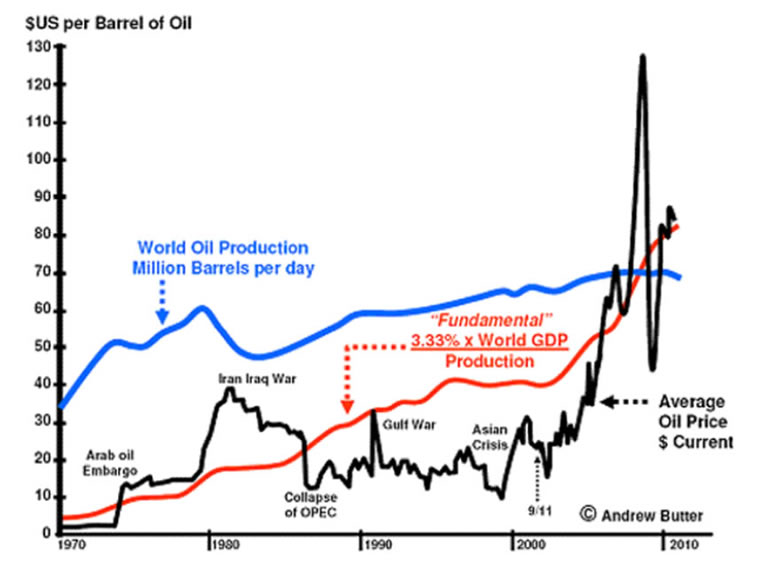

- That represents a total oil bill for the world of 3.3% of GDP which is what it has averaged over fifty years. The logic of that is explained here: http://www.marketoracle.co.uk/Article24849.html

- That is exactly equal to adjusted for now. That’s called BUBBLEOMIX

So how come oil is $65 when the “correct price” is $95? The proof for why that is, is that was predicted, in glorious Technicolor four years ago, the only thing that was wrong with that prediction was the timing (although that was “hedged”), but like Milton Keynes said “the market can stay irrational longer than you can stay solvent”, which is another way of saying – no one can predict when a bubble will pop. What is predictable is what happens after the pop. Here’s that up-to date, four years “up” means there will be four years “down”, because according to The General Theory of the Pebble in the Pond... bubble & pop is zero sum.

By Andrew Butter

Twenty years doing market analysis and valuations for investors in the Middle East, USA, and Europe. Ex-Toxic-Asset assembly-line worker; lives in Dubai.

© 2014 Copyright Andrew Butter- All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Andrew Butter Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.