Exorbitant Privilege, Deficit and Debt Damaging the US Brand

Politics / US Debt Oct 21, 2013 - 10:15 AM GMTBy: John_Mauldin

There is no doubt that the image – what I will refer to in this letter as the "brand" – of the United States has been damaged in the past month. But what are the actual costs? And what does it matter to the average citizen? Can the US recover its tarnished image and go on about business as usual? Is the recent dysfunction in Washington DC now behind us, or is it destined to become part of a bleaker landscape? In this week's letter we try to answer those questions and more, as I step firmly into politically incorrect territory and offer a little advice to my junior senator from Texas. If nothing else, we will look at the problems we face in a different light.

There is no doubt that the image – what I will refer to in this letter as the "brand" – of the United States has been damaged in the past month. But what are the actual costs? And what does it matter to the average citizen? Can the US recover its tarnished image and go on about business as usual? Is the recent dysfunction in Washington DC now behind us, or is it destined to become part of a bleaker landscape? In this week's letter we try to answer those questions and more, as I step firmly into politically incorrect territory and offer a little advice to my junior senator from Texas. If nothing else, we will look at the problems we face in a different light.

The term exorbitant privilege refers to the alleged benefit the United States receives due to the US dollar's being the international reserve currency. The term was coined in the 1960s by Valéry Giscard d'Estaing (not Charles de Gaulle, as many think), then the French Minister of Finance, later President of France, and an early and major proponent of a United States of Europe. This was prior to the gold window's being shut by Nixon. Giscard saw the Bretton Woods monetary system not simply as a way to balance international payments but as something that was giving the United States a significant advantage in the world. He was right.

Under Bretton Woods, the US would never face a balance of payments crisis, because it purchased imports in its own currency. That exorbitant privilege could not redound to a country whose currency had only a regional reserve currency role, but in the postwar era the US dollar reigned supreme around the world.

Academically, the exorbitant privilege literature analyzes two empiric puzzles, the position and the income puzzle. The position puzzle consists of the difference between the (negative) U.S. net international investment position (NIIP) and the accumulated U.S. current account deficits, the former being much smaller than the latter. The income puzzle consists of the fact that despite a deeply negative NIIP, the U.S. income balance is positive, i.e. despite having much more liabilities than assets, earned income is higher than interest expenses. (Wikipedia)

What that means in practical terms is that the United States can purchase more with its currency than it produces and sells. In theory those accounts should balance. But the world's reserve currency, for all intent and purposes, becomes a product. The world needs dollars in order to conduct its trade. Today, if someone in Peru wants to buy something from Thailand, they first convert their local currency into US dollars and then purchase the product with those dollars. Those dollars eventually wind up at the Central Bank of Thailand, which includes them in its reserve balance. When someone in Thailand wants to purchase an imported product, their bank accesses those dollars, which may go anywhere in the world that will take the US dollar, which is to say pretty much anywhere.

Other currencies can also function as reserve currencies if there is sufficient trade between countries. The euro, the Canadian dollar, the Aussie dollar, and the yen are examples; but the US dollar is the 800-pound gorilla.

There have been other global reserve currencies. The British pound sterling served as a global currency prior to the ascendance of the dollar. In most ways, we in the US act as if our dollar will always be the world's reserve currency. History suggests, however, that reserve currencies come and go. The US dollar will remain the dominant reserve currency only as long as we respect the responsibility that comes with our exorbitant privilege.

That privilege allows US citizens to purchase goods and services at prices somewhat lower than those people in the rest of the world must pay. We can produce electronic fiat dollars, and the rest of the world accepts them because they need them to in order to trade with each other. And they do so because they trust the dollar more than they do any other currency that is readily available. You can take those dollars and come to the United States and purchase all manner of goods, including real estate and stocks. Just this week a Chinese company spent $600 million to buy a building in New York City. Such transactions happen all the time.

And there is one other item those dollars are used to pay for: US Treasury bonds. We buy oil and all manner of goods with our electronic dollars, and those dollars typically end up on the reserve balance sheets of other central banks, which buy our government bonds. It's hard to quantify the exact amount, but these transactions significantly lower the cost of borrowing for the US government. On a $16 trillion debt, every basis point (1/10 of 1%) means a saving of $16 billion annually. So 5 basis points would be $80 billion a year. There are credible estimates that the savings are well in excess of $100 billion a year. Thus, as the debt grows, the savings also grow! That also means the total debt compounds at a lower rate.

Just as an aside, $80-$100 billion a year will buy a lot of healthcare. Hold that thought as we continue to look at currency trading and reserve currency status.

Let's return to our example of trade between Peru and Thailand. There is presumably little reason for a furniture manufacturer in Thailand to take Peruvian money (which is called the nuevo sol). Let's assume this piece of furniture sells for 32,300 Thai baht or about $1000. So the buyer in Peru takes 2,764 nuevo sols, buys 1,000 US dollars, sends them to Thailand, and voila! his teak table comes in on the next boat.

Except that it isn't quite that simple, as anyone who has done a substantial foreign transaction knows. You have to go to your local bank, which probably goes to its correspondent intermediary bank, which in turn deals with a large international investment bank, which then sends the money on to an intermediary in Thailand and then to a local Thai bank. At every step along the way there is a "toll" charged. While much smaller than it was a few decades ago, those tolls – that "friction" – can add up to a sizable sum. Depending on whom you ask and what you count, the total amount of currency traded per day is as much as $4 trillion, and just a few "pips" taken out to grease the skids tally up to a rather tidy sum.

(For the curious, a "pip" stands for "percentage in point" and is the smallest increment of trade in foreign exchange [FX] currency trading. In the FX market, prices are quoted to the fourth decimal point. For example, if a bar of soap in the drugstore is priced at $1.20, in the FX market the same bar of soap would be quoted at 1.2000. The change in that fourth decimal point is called 1 pip and is equal to 1/100th of 1%.)

Currently, there are only about seven currencies that are traded in serious amounts, although theoretically every currency is trading in some manner. When I was traveling around Africa, I would often come across a street in a city where currencies were being traded. The rates were much better than you could get at the local bank. Going with an "official" rate often means suffering a real loss in local buying power, and thus the spreads on some currencies are much wider than on others. No one wants to get stuck with an Argentine peso for very long outside of Argentina, and even inside Argentina the locals exchange money into pesos only when they need local currency. When I was last there, using a credit card cost anywhere between 10-15% more (if a local establishment took credit cards at all), because the store would have to cash in at the official rate rather than the street rate.

And while the "friction," or transaction cost, of trading a euro for a dollar and vice versa is a much smaller percentage, it is there. And thus the need for dollars to grease the wheels. To trade goods between Peru and Thailand, intermediaries usually have to find dollars.

But the key word in that sentence is usually. This week, London and Hong Kong agreed to begin trading in Chinese renminbi. The "extra" friction once incurred in converting to the US dollar will disappear, and the cost of doing direct transactions will fall. This absolutely makes sense for the two countries, and over time it will make sense on an ever-larger scale. Currencies are increasingly becoming mere electronic blips. For young traders, sitting at an FX desk is just another computer game, but if they are good at it, they get paid real money. Killing pips can be more profitable than killing zombies ever was.

The dollar is the world's reserve currency because it is a no-brainer trade. You don't have to think about your risk. If you take a ruble, you need to think about your risk and maybe buy some insurance. You ask yourself if you can trust Putin with your money. Even today, if you begin to stockpile renminbi, what can you do with them? You need to find something to import from China. There is risk to that trade. Not as large a risk as in the past, but more than if you deal in dollars.

Unless we damage our brand. Unless we start making that 27-year-old trader sitting at an investment bank in London think for a fraction of a second before he hits the button. He is in the business of killing pips, and if you increase his cost, even by 1/1000, the difference shows up in his bonus.

You scoff? Then why did credit default swaps on the US Treasury market rise over the last month? If you are buying US Treasury bonds, you are by definition seeking to avoid risk. You want zero risk, and last week the world markets decided – while watching CNN, CNBC, Bloomberg, and Al Jazeera, and reading the running commentary in the Wall Street Journal and the Financial Times, on Reuters, and in gods-know-how-many blogs – that there was indeed some small risk, and so they wanted to be paid more for holding Treasuries.

The world looked at the US, and unlike in the dozens of debt-ceiling games of chicken our politicians have played in the past, this time the fight at the edge of the cliff made the rest of the world nervous. In the past, you "knew" that the adults were playing a serious game over budgets, but there was always the sure sense that they would do the right thing and not risk the brand.

You can call it media spin or whatever you like, but this time there was a real sense that the adults had left the room. I totally understand why it happened, but the reaction from around the world was akin to watching your parents fighting and not being sure what would happen. I mean, you get used to your parents quarreling from time to time, but when they threaten to shut down the marriage and blow up the house, you might start to worry.

A Small Percentage of Americans

I read a note from my friend Barry Ritholtz about the recent events, which I found amusing in its viewpoint. I cut Barry a lot of slack, as he is one of only three or four Jacob Javits Republicans still in existence and should probably be preserved somewhere as a historical curiosity. (For those of a younger persuasion, or from outside the US, Jacob Javits, was a very liberal Republican Senator from New York. Yes, there was a day when the Republicans had a significant and decidedly liberal branch.) Barry wrote:

Amongst all of the background nonsense since October 1, the noise about the deficits was not really about budget deficits at all. Rather, it was about a decidedly narrow ideology held by a small percentage of Americans. Their belief is that government should be much smaller. This is a legitimate political ideology, one that has persisted over the centuries.

Actually, Barry, it is only a small percentage of the people on the island where you work (Manhattan). Out here in "flyover land," it can be a sizeable majority. And as Barry agreed in a conversation today, it really depends on how you frame the question.

If you asked people in 2008 whether they wanted access to more affordable healthcare, a majority said yes. A large majority also did not want to see their taxes raised. Sizeable majorities want smaller government and also want to preserve Social Security and receive more Medicare benefits. The fact that these desires are not consistent with one another is not a trivial issue. In fact, it is the source of our political divide.

The Republicans got into trouble when they made the recent debt-ceiling crisis about the trees rather than the forest. I would agree that Obamacare is a rather sizeable tree, but the forest is our unmanageable deficit and growing debt.

The questions the American people are ultimately going to have to answer are, "How much healthcare do we want, how much do we want to pay for it, and how will we pay for what we want?" Everything else in the national budget can be accommodated rather easily, as such things go, at least from a deficit perspective. Take a little here, give a little there. But with healthcare, there are no small gives and takes.

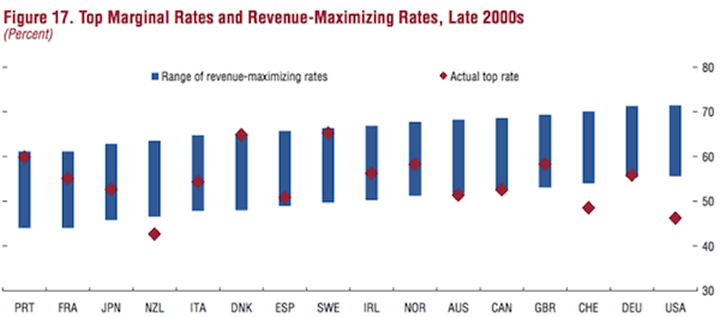

Barry cited a study by the IMF showing that we in the US pay lower taxes than people do in other OECD member countries. The study is both revealing and misleading. Here is the chart that suggests, according to Barry, that Americans are undertaxed:

The misleading part is that this chart does not include state and local taxes but rather focuses on top marginal federal income tax rates. But the top marginal rate in some states can be much higher, depending on local property taxes and whether there is a state (and even local!) income tax.

In general, the OECD countries have some form of universal healthcare. But most of them also assess a value-added tax, or VAT, which is basically a consumption tax. A VAT means that everyone pays a substantial tax on every purchased item. This is how these nations finance their large government budgets. Marginal rates in the US have been pushed about as high as they can be. The only remaining source of real revenue is the middle class, and raising taxes on them is a non-starter. The only other way to raise enough to pay for universal healthcare is with a VAT. But that approach brings on another whole set of problems, too many to get into today.

Most everyone knows that the budget deficit cannot be sustained indefinitely. There must be significant entitlement cuts, significant tax increases, or some combination of the two. If we continue along the same path without some serious compromise, we will replay the debt-ceiling crisis again and again. It will not go away unless both sides are willing to compromise. Either that or the voters will have to make a firm decision one way or the other. Right now, the people we have elected to federal office do not appear to see compromise as their mandate. Until that dynamic changes, we are going to continue to put the brand of the US dollar at risk, something which must not be allowed. The cost in cold hard dollars of trashing that brand is a budget buster in and of itself.

The one thing the US dollar has going for it right now is that other candidates for the world's major reserve currency all have even more serious problems than the dollar does in the near term. Most are just too small. If Canada were about ten times bigger, its dollar would be formidable. The euro is still an experiment. If Marie le Pen is France's answer, someone is asking the wrong question. Ditto for many other countries in Europe. The jury is still out; that said, if the euro still exists in five years, it will begin to take on a much larger role.

But the idea of some basket of currencies appearing on computers as tradable reserve currencies is not out of the question, technologically. It would not be convenient, at least at first – but if the dollar loses its luster? When that buyer in Peru wants a table made in Thailand, he does not care how the transaction is facilitated. He has neuvo sols and wants a table. And foreign exchange traders exist to make a few pips by helping him make that happen. They really just want the easiest and safest way to trade. In our own self-interest, we do not need to make the world look beyond the dollar.

An Open Letter to My Senator, Ted Cruz

While it is difficult to hide the fact that I am a Texas Republican, I try to keep politics out of this letter except as politics affect economics and investment; and generally I think I succeed. At one point in my life I was heavily involved in Texas politics; but that was well over ten years ago, and I have no intention of ever getting more than casually involved again. But that doesn't mean I do not have an interest in what is happening on the state and federal levels. I have sat down with many politicians over the years, and I still do, though I meet with more Democrats these days than I did in the past, in my current role as economic commentator. Politics is where the realm of ideas is fleshed out into legislation that we all have to live with. More and more, I wonder what sort of world my adult children and their children will be left with. And while longtime readers know I am optimistic about the future, the paths to get us there are many and twisting.

So, for those who want to forego my thoughts on Republican Party inside politics, I suggest you move on now, as this is going to be one Texas Republican talking to another. And I get that I risk being seen by many as someone who is willing to use the word compromise. I recently had dinner with my friend Ron Paul, who for years gave no quarter in Congress. I get the value of staking your reputation on a set of principles. But I also think I see the nature of the task in front of us, as well as the political realities that will pull us down if we don't meet the challenges they pose. So, with that, let me offer some unsolicited advice to Ted.

Dear Senator Cruz,

Congratulations on getting through a rough primary and on to the Senate. Not that it makes much difference now, but I did support you in the primary, not for the reasons most people reading this letter might think, but because your opponent committed an unforgiveable sin while in office. He raised taxes in a particularly offensive way (the corporate gross receipts tax), which I regarded as a barely legal fiction to get around our state constitution. That is something I do not think should be encouraged in Texas politics.

I should note that I met your wife Heidi last week and got to spend some time with her. She is your best asset. If you ever decide to go back to private life, there is another Cruz I might vote for in Texas.

As you might guess from the lead-in to this letter, I am quite concerned that your latest effort to roll back Obamacare might not have been as benign as you thought for the long-term "brand" of the US. Hopefully, there will be no real long-term damage. Perhaps, when the dust settles, your misguided tactics will amount to no more than a political version of New Coke. When Coca-Cola rolled out New Coke, the market rejected it, and the company recovered and moved on. New Coke is now merely an interesting footnote in the business school curriculum.

But that brings up the question of what to do now. Let me offer a few thoughts. First, you are right to be concerned about the effects of Obamacare on the public, and you have correctly gauged public angst. I totally get the polls that say something like 60% would like to see the law repealed or significantly changed.

But we need to remember that a majority in the country also want some type of better healthcare system. They are not for a return to what we had back in 2008. There was a reason Obamacare passed, and there was a reason Obama was re-elected even though his healthcare law was unpopular. The simple fact is that a majority (even if a small one) of the country did not trust Romney to manage a new healthcare system. Yes, I know there were lots of other reasons, but that was clearly a leading one.

While you can likely get broad agreement that the country should balance its budget and that the debt is a growing concern, the manner in which you go about dealing with Obamacare is critical. All the country heard during this last debt-ceiling fight was that a sizeable number of Republicans wanted to defund Obamacare. While most people might agree that Obamacare needs to be fixed, simply going back to where we were is not what they want either. They may not know what they want, but 2008 is definitely not it.

President Obama is never going to agree to a dismantling of the Affordable Care Act. It is just not in his DNA. I am convinced he will walk away from any deal if that is the price. And you should be walking away, too. Here's why.

We can see how Obamacare is rolling out. It's a train wreck in the making. It doesn't matter whether Obama throws (Health and Human Services Secretary Kathleen) Sebelius under the bus, the structure is fatally flawed, at least from our perspective. The program amounts to a huge middle class tax increase, and when healthcare rates go up – and you and I believe they will – the tax will be even more onerous. Hospitals are going to see their budgets cut and will be forced to lay off personnel even as their workload increases. The vast majority of people are going to be shocked at how much healthcare will still cost with Obamacare.

There is going to be a real opportunity to fix the problems in the future. If we are right about what will happen, the demand for change will be overwhelming. Even the Dems will be scrambling to make major changes to the program. But right now, in the wake of the recent congressional debacle, I wonder whether the public would be willing to trust us to manage that change. It's very possible, even likely, that the Dems will run on a strategy of "the problem with Obamacare is that the Republicans won't let us fix things." I would, in their place. Right now, they still think that they just have a programming problem and that a few software patches will make everyone happy – but a year from now? It is going to be all about whom voters trust to fix the problems.

Healthcare is a very personal issue. It is probably the most contentious topic I run into when I am out on the road talking to people. There is a sizeable contingent of the country that agrees with you, but it is unlikely to ever be a majority. The majority wants healthcare to change, not simply revert, but not until they feel they can trust the agents of that change.

Right now, why not focus on the things you can get real agreement on? Reduce the deficit and make some entitlement reforms. If a chance for something like real tax reform offers itself, then take it. Forget the all-or-nothing strategy. It is all well and good to talk that way, but it is a terrible way to actually govern. Think back to Reagan and Tip O'Neil. Or Gingrich and Clinton. Few men could talk a better fight than those gentlemen did, but then they sat down together and talked and governed. And the country was better off for it.

Why not show that you can find solutions? Obama and Reid are going to need some help in the near future. Everyone knows there are some obvious fixes to the (so-called) Affordable Care Act that would make us all better off. So give them those fixes, and get some things we want in exchange. Show that you can govern. Show the country that you will do the right and necessary thing in the short term, even while keeping your eye on the long term.

If Obamacare becomes the political problem we both think it will, then we can get the votes to fix it, because the people will give us the votes if they think they can trust us to make the changes. If on the other hand Obamacare works well enough that a majority prefer it, then we will have to work on changing things gradually, as the Dems did for 50 years with regard to their desire for universal healthcare.

You are now the de facto leader of the Tea Party movement. The Republican Party needs those votes if they are going to promote change. But the Tea Party needs the rest of the Party's voters as well if they want to see change. You don’t want to chase the at-the-margin independent who normally leans Republican over to the other side by scaring them.We must create a strong coalition of people willing to work for change, or the Party will become a semi-permanent minority party that is unable to effect substantive change, however compelling its ideals. The GOP had been a minority in the House for 40 years when Gingrich was swept in on a wave of desire for change.

The big battle that will come later in this decade is not going to be over healthcare but over the debt and entitlements. If we don't deal with the deficit and run-away entitlement spending, we are going to be forced to make very unpleasant choices. We will face losing a great deal of what our forebears have bequeathed us in terms of our place in the world if we don't answer these big questions correctly. There will be no greater economic or political battle in our lifetimes. The challenge will require statesmen who are philosophically grounded and who understand the ramifications of the decisions that will be made. When that battle comes, we need to be a credible political force if we want to be able to determine the outcome and make sure the future is secure for our children and grandchildren. A minority party that knows it is right is still a minority party in a democracy.

The Dems are digging a very deep hole for themselves, but right now we're down in that hole with them: the approval rating of Congress is at an all-time low (which is really saying something), and the Republicans are taking the brunt of the public's displeasure. Only one party is going to climb out of the hole and fill it, and it will be the party the public thinks is credible and reasonable with its arguments and programs.

I want the winner of that battle to be the smaller-government team. So do you. But if we don't lay out a plan that can convincingly demonstrate how to fix the problems we face, then simply saying there is a problem won't be enough. We have to show that we can govern, and we have to demonstrate that we can keep our eyes on the whole forest rather than focusing solely on axing the ailing healthcare tree, if we don't have the votes to do it.

Yours for the long run, John

Code Red, Science Saves the Future, New York, Florida, Geneva, Saudi Arabia, and Canada

Next week I am off to NYC to do a week of media as we roll out my new book, Code Red. I will see my first copies when I get to the hotel on Monday, and it will be shipping to bookstores and Amazon during the week. I am truly excited about it, and the advance reviews are coming in even better than I expected. I always get nervous about these things.

I will be with Tom Keene Tuesday morning on his radio show and other outlets throughout the week, with more getting booked as I write. My co-author, Jonathan Tepper, and I will be speaking on Tuesday the 22nd for the World Policy Institute at 6 pm, in Manhattan, as part of their occasional World Economic Roundtable. There will be a wine reception. Space is limited, so if you wish to attend, please RSVP to dugan@worldpolicy.org. Venue details will be included in your RSVP confirmation.

Then the next night, October 23rd, there will be a book-launch party from 5:30-7:30 at the Hyatt Union Square, 134 Fourth Ave., in The Fourth-Botequim restaurant. There will be light hors d'oeuvres and a cash bar. As one of my closest friends, you are of course invited.

Science Saves the Future – the "virtual conference" I recently hosted with my newest colleague, Transformational Technology Alert editor Patrick Cox – came together even better than I thought it would, and I had high hopes to begin with. If you watched the event, then you'll probably agree that while the ideas we discussed may seem shocking now, they're likely to be old hat in 15 or 20 years. What you witnessed during the event was akin to hearing Henry Ford lay out his vision for changing transportation before the first Model T rolled off the production line. Instead of transportation, though, the guests you heard were talking about the biggest potential transformation of all: life extension. Patrick did a wonderful job summing up all the arguments and explaining the opportunities in simple terms. And he has just released a report on three companies he thinks have the most near -term potential in this space. I urge you to read his report by clicking here.

I will be back in NYC on November 12 for a special event (details to come). I will then fly down to be with my good friend Cliff Draughn at Ponte Vedra, Florida (south of Jacksonville), on November 14. You can find out more by going to Cliff's website at http://www.excelsia.com. And then it's back to NYC in early December and later that month to Geneva. In January I will visit sunny Saudi Arabia for the first time and am open to other speaking engagements in the region. I go from there to a speaking trip that will take me through three cities in Western Canada, where the weather will be quite the opposite.

Yesterday my doctor and good friend Mike Roizen was in town for a speaking event, and we got to spend some time together. I showed him my new apartment, which is under construction. They are putting in the floors, and admittedly there is a lot still to be done. When he asked when I would get to move in, I responded, "I am promised November 14." He laughed and said, "If you had told me December 14 I might have believed you, but I think November is a tad on the optimistic side." That has been the response of late, but if you can't trust your contractor's spreadsheet, what can you trust? You have to believe in the model, right? Don't tell my contractor, but just in case, I have not given up the lease on my temporary living quarters. I am sure that's an unnecessary precaution. Surely.

This has been a very difficult letter to write for some reason – perhaps because I think the issues are so very important – but now it's time to hit the send button. Have a great week.

Your nothing if not an optimist analyst,John Mauldin

subscribers@MauldinEconomics.com

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2013 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.