Japanese Currency Intervention, How Does Disaster Promote a Strong Currency?

Currencies / Japanese Yen Mar 23, 2011 - 01:34 PM GMTBy: Robert_Murphy

After the catastrophic earthquake, the tsunami, and the nuclear-reactor scares, the Japanese currency ironically strengthened quite sharply. In response, the Bank of Japan and other major central banks last week launched a coordinated "intervention" into the currency markets in order to intentionally weaken the yen.

After the catastrophic earthquake, the tsunami, and the nuclear-reactor scares, the Japanese currency ironically strengthened quite sharply. In response, the Bank of Japan and other major central banks last week launched a coordinated "intervention" into the currency markets in order to intentionally weaken the yen.

In this article I'll explain why the yen strengthened in the first place, and the problems with the central-bank maneuvers.

How Does Disaster Promote a Strong Currency?

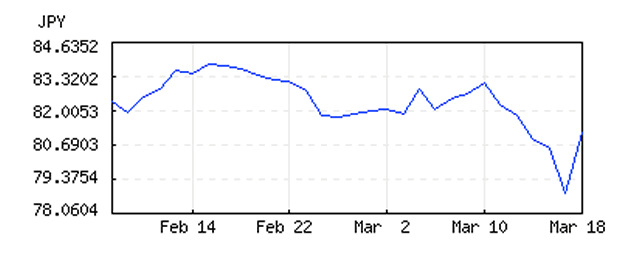

As the chart below illustrates, the Japanese yen appreciated very strongly against the US dollar (as well as other currencies) following the March 11 earthquake:

Keep in mind that the chart above shows how many yen it takes to buy one US dollar, so that a lower value means a stronger yen. Also, the sharp spike upward on March 18 was presumably in response to the central-bank intervention.

Many people were surprised that the yen would strengthen following a natural disaster that disrupted the Japanese economy, but we should remember that a currency is not really a proxy for a country's economy. No, the price of the yen is set by supply and demand in the currency markets.

The reason the yen strengthened is that speculators thought it would, and so they began selling other currencies in order to buy yen. For example, a currency speculator who held $10,000 in US dollars could enter the foreign exchange market and try to get somebody else (holding yen) to sell his yen for the dollars. If lots of speculators start doing this, the increased demand for yen pushes up the dollar-price of yen, just as an increased demand for toasters would push up the dollar-price of toasters. The one twist is that the exchange rate of yen is usually quoted as a yen-price for dollars, and so a higher-priced yen shows up as a falling number in the graph above.

Of course, we've just pushed back the question one step: Why did speculators think the yen would strengthen after the earthquake? The standard answer in financial circles is repatriation. Specifically, speculators guessed that lots of money from around the world would be flowing to Japan over the coming months. This might be because of charitable contributions, or because Japanese-based insurers have to liquidate their foreign holdings in order to raise cash with which to pay claims to their Japanese policyholders.

Whatever the reason, speculators expected that there would be a lot of people in the coming months trying to turn their own local currencies into yen. Therefore, because there will be more people trying to sell other currencies and buy yen, that would tend to push up the price of the yen, quoted in these various other currencies.

The G7 Doesn't Like What It Sees

As various financial articles announced, late last week the central banks of the G7 nations announced a coordinated intervention to push down the strengthening yen. Specifically, the central banks have begun selling yen and buying other currencies, in an attempt to counteract the moves of the speculators.

The Bank of Japan of course can create yen out of thin air if it wishes, just as Ben Bernanke has an unlimited power to write checks (denominated in dollars) and buy assets. The other six central banks, however, don't have the ability to create yen. For their role in the intervention, they have to at least stand by and watch as the BOJ prints yen and makes their own currencies appreciate.

Going further, these banks can actively help in pushing down the yen by selling off their previously acquired stockpiles of it. (For example, last Friday the New York Fed reportedly sold yen-denominated assets in order to buy $50 million in dollar-denominated assets, drawing on the Fed's total yen holdings worth about $11.9 billion.)

Promoting Stability?

The ostensible reason for the currency interventions was to promote stability. According to David Mann, head of research for the Americas at Standard Chartered Bank. "This is about limiting volatility and reducing uncertainty."

However, if stability is the goal, then fighting speculators is the exact wrong approach. Speculators actually reduce volatility, insofar as they are profitable. After all, the goal of the speculator is to "buy low, sell high," or (for an overpriced asset) "short-sell high, cover low." Either way, the speculator acts to push an asset price to its future level, and the entire price path is smoother because the speculator grasps the situation earlier than others.

It is laughable to think that the G7 intervention is promoting stability, because investors don't know exactly what the central banks will do. This excerpt from a financial news account of the New York Fed's intervention last Friday illustrates the problem:

The initial intervention from the Fed came right at 8 a.m. EDT, the start of the New York trading day. Three U.S. banks familiar with the intervention told Dow Jones Newswires the Fed's trades early in the New York day totaled about $50 million.

The initial intervention by the Fed was symbolic to show the central bank stood with the Bank of Japan in the coordinated effort, said Michael Woolfolk, senior currency strategist at Bank of New York Mellon in New York. But he added that it was also a "warning shot across the bow" of speculators trying to fight the intervention. …

Based on the price action, the Fed and Bank of Canada could be intervening in a more sustained manner, as opposed to a "one-shot deal," said Brian Kim, currency strategist at UBS in Stamford, Conn.

"It could be maybe they're going to spread it out," Kim said of measures to curb yen strength. "Or maybe that was it."

When all is said and done, the dollar may be propped to Y82, Kim said, which could be a psychologically significant number and would bring the dollar back to pre-earthquake levels.

Now, in addition to the natural disasters and their various ramifications, speculators and other market participants have to anticipate the moves of the central bankers. If the central banks — running low on their yen reserves — decide at some point to throw in the towel, they will simply have delayed the market's adjustment to the new realities. Their moves would be as futile as those of a South American dictator who tries to artificially prop up the exchange value of his currency in the face of a speculative "attack."

The one player in the game who can permanently keep the yen weak is the Bank of Japan, because its "reserves" are infinite. In other words, rather than pressuring the market to stay away from the new yen strength justified by the fundamentals, the Bank of Japan could alter the fundamentals themselves, by flooding the world with newly created yen. In the next section, I'll outline the drawbacks of this strategy.

Market Prices Matter

Whenever a central bank decides it doesn't like the market price, and so decides to print a bunch of money, we should point out that prices mean something, they are not arbitrary. Often what happens is that the central bankers, backed up by the financial pundits, diagnose a certain trend as obviously "bad for the economy," relying on a crude Keynesian approach. Yet if we adopt an Austrian view, in which markets are very complex and yet nimble, then the central bank interventions simply sow confusion.

When it comes to the current Japanese situation, there are lots of stories one could tell. But suppose something like the following is what would have happened, had the G7 central banks minded their own business: Following the earthquake and tsunami, millions of people around the world wanted to send billions of dollars worth of donations to Japanese relief efforts.

Initially, these donations were all denominated in dozens of other currencies. At some point in their path to Japan, each currency was converted into yen in the foreign-exchange market. The spike in demand caused the yen to appreciate sharply against all other currencies.

Armed with the influx of donations, the Japanese relief agencies begin buying all sorts of supplies, many of which are produced abroad. If a relief team needs a tractor made in the United States, for example, it will take some of its yen and buy dollars, which it then uses to import the tractor. When all is said and done, much of the yen's initial strengthening is reversed, as Japan imports far more than it normally would. This makes sense (in a world of fiat currencies), because the real way to help Japan is for people around the world to send them physical goods. But of course, sending money is far more efficient, because it allows the recipients to purchase the exact items they need.

The above story obviously leaves out many details, but it probably captures an important part of what is going on. Now if the Bank of Japan and other central banks purposely try to interrupt the above process, then they interfere with the world's ability to ship goods into Japan. By weakening the yen, the G7 central banks are making foreign goods more expensive to buyers based in Japan.

Depending on the specifics, the Bank of Japan is arguably stealing some of the incoming charitable contributions, because they are using the upswing in the yen as an excuse to expand their own balance sheet. By doing so, the Bank of Japan is hurting the aid agencies (and Japanese consumers in general) for the benefit of Japanese exporters, because in the short run exporters benefit from a weaker yen.

Conclusion

At best, the G7 currency intervention will simply postpone the inevitable adjustment of world currencies to a change in demand for yen. At worst, the Bank of Japan can enforce a permanent depreciation through money creation, which will redistribute wealth from Japanese relief agencies and average citizens into the pockets of manufacturers.

Robert Murphy, an adjunct scholar of the Mises Institute and a faculty member of the Mises University, runs the blog Free Advice and is the author of The Politically Incorrect Guide to Capitalism, the Study Guide to Man, Economy, and State with Power and Market, the Human Action Study Guide, and The Politically Incorrect Guide to the Great Depression and the New Deal. Send him mail. See Robert P. Murphy's article archives. Comment on the blog.![]()

© 2011 Copyright Robert Murphy - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.