Federal Debt of the United States - Q and A (Part II)

Interest-Rates / US Debt Jan 12, 2011 - 03:24 PM GMTBy: Asha_Bangalore

[Part I, question 1-3] published on Jan 11, 2011.

[Part I, question 1-3] published on Jan 11, 2011.

4. Will Congress entertain not raising the statutory debt limit?

Congress will increase the statutory debt limit prior to the deadline. There is not even an inkling of doubt about this eventuality. But, unfavorable posturing by politicians, prior to taking the appropriate action, is nearly certain and tentative market concern will prevail. The terms of the deal the Republicans will strike to raise the debt limit is the source of uncertainty not whether they will raise the borrowing limit. The Treasury Department estimates that the national debt will hit the statutory limit between March 31 and May 16. In the meanwhile, Treasury Secretary Geithner has indicated that the Treasury could take "exceptional actions" to delay the deadline by suspending the sale of state and local government securities, which would buy time for a few weeks.

5. What are the implications of the growth in federal debt?

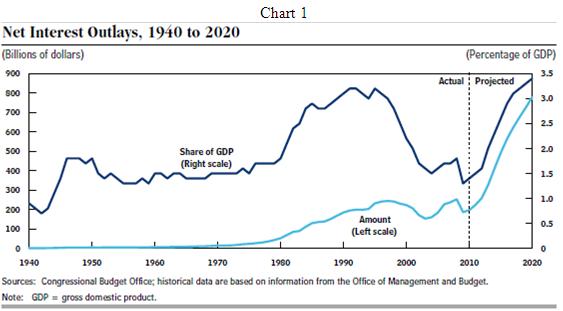

First, interest costs have to be considered. Net interest outlays in 2010 amounted to $197 billion or 1.4% of GDP (see Chart 1). The Congressional Budget Office's estimates focus only on the publicly held debt. Most of the difference between total federal debt and that held by the public is accounted for securities held in the Social Security Trust Fund. The low interest rate environment helped to contain interest costs despite a large increase in federal debt. Going forward, interest costs as a share of GDP are expected to double reflecting growing debt and higher interest rates.

Second, the United States has a small window to repair the strategy to tackle the imbalance. For now, financial markets have not questioned the status of U.S. federal debt and they continue to view these securities as a "safe haven" in situations of market upheaval. Future interest rates and deficits are uncertain and will be determined by the economic growth trajectory and future legislative actions. Recent projections of the federal deficits and debt (see Charts 2 and 3 in Part I, comment of January 10, 2011) suggest that the current market assessment of the U.S. debt situation will be subject to reconsideration if there is no effort to contain the growth of federal debt. The United States has a small window between now and when the economic and market environment return to normal conditions to address the severe fiscal imbalance. Third, each percentage point in the U.S. debt-to-GDP ratio translates into higher interest costs, with additional economic costs such as "crowding out" of private investment. This in turn lowers the size of the economic pie and erodes the standard of living of future generations. In the near-to-medium term, financial markets will focus on the policy changes implemented to address reduction of federal debt.

6. What are the reasons for growth of federal debt?

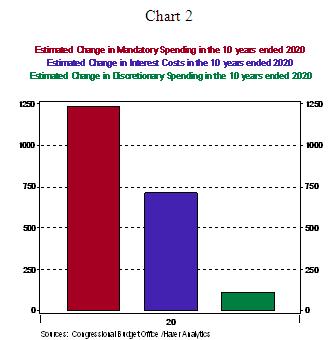

A major part of the increase in the federal deficit, following the financial crisis and the Great Recession, reflects a severe loss of tax revenue, a jump in outlays, partly from an increase in expenditures from automatic stabilizers and partly due to legislative action to stabilize financial institutions and the economy. These deficits translated into a sharp increase in publicly held debt from 36% at the end of 2007 to 62% by 2010. It is important to note that the projected increase in federal debt during the decade ahead is due to entirely different reasons. Medicare, Social Security, and interest costs are the three major factors accounting for the growth of public debt. Therefore, these costs need to be addressed after self-sustained economic growth becomes evident. Contrary to common understanding, discretionary outlays are predicted to show only a small increase in the next decade (see Chart 2).

Small Business Optimism Index Declines, Poor Sales Persists as the Foremost Problem

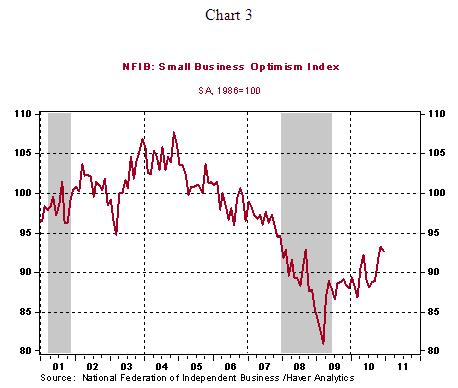

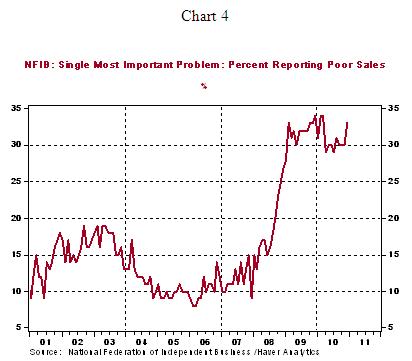

The Small Business Optimism Index edged down to 92.6 in December from 93.2 in the prior month (see Chart 3). More importantly, a significantly large percentage of respondents (33%) continue to indicate that poor sales are the foremost problem (see Chart 4) in December compared with tally in the September-November (30%) period.

Asha Bangalore — Senior Vice President and Economist

http://www.northerntrust.com

Asha Bangalore is Vice President and Economist at The Northern Trust Company, Chicago. Prior to joining the bank in 1994, she was Consultant to savings and loan institutions and commercial banks at Financial & Economic Strategies Corporation, Chicago.

Copyright © 2011 Asha Bangalore

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.