What is Going on in Washington?

Interest-Rates / US Debt Aug 30, 2010 - 01:57 PM GMT

What if you earned half of what you spent in a month and put the other half on your credit card? What if you did that month after month, year after year until your debt was six times your annual income? Would you consider yourself to be in deep financial trouble?

What if you earned half of what you spent in a month and put the other half on your credit card? What if you did that month after month, year after year until your debt was six times your annual income? Would you consider yourself to be in deep financial trouble?

As daunting as that might seem, it is precisely the situation in which the U.S. federal government finds itself as we enter the second decade of the 21st century. It spends roughly twice what it collects in tax revenues.* Most of that difference is raised by selling government debt obligations, but unlike the ordinary citizen, what the government is unable to borrow it covers by printing the money. Now with a wave of the hand, the Federal Reserve has institutionalized printing money (monetizing the debt) as part of public policy. At this juncture, the projected monetization is small compared to the overall additions to the national debt, but whatever the amount it sets a bad precedent.

As daunting as that might seem, it is precisely the situation in which the U.S. federal government finds itself as we enter the second decade of the 21st century. It spends roughly twice what it collects in tax revenues.* Most of that difference is raised by selling government debt obligations, but unlike the ordinary citizen, what the government is unable to borrow it covers by printing the money. Now with a wave of the hand, the Federal Reserve has institutionalized printing money (monetizing the debt) as part of public policy. At this juncture, the projected monetization is small compared to the overall additions to the national debt, but whatever the amount it sets a bad precedent.

So let’s consider for a moment the prospect of repealing the Bush tax cuts. When it sinks in that government is spending twice what it brings in, it also sinks in that the government would need to double its revenue to balance the budget. That would mean everyone’s taxes would need to double. Thus, repealing the Bush tax cuts amounts to the equivalent of launching a pea at a charging bull moose. It isn’t going to get us anywhere and amounts to another meaningless political exercise aimed at garnering support in the upcoming mid-term elections.

Since doubling everyone’s taxes essentially would amount to bankrupting the citizenry in order to make the federal government whole (for just a single year), the next option would be to raise money from our trading partners, the two largest being China and Japan. That door seems to be closing slowly. China has become a net seller of U.S. Treasury paper and Japan has markedly slowed down its purchases. The rest of the world has displayed a marginal appetite for U.S. debt -- at least when compared to what has become a monumental need.

Thomas Hoenig of the Kansas City Federal Reserve, who was the lone dissenter on the Federal Reserve Board’s recent decision to leave rates at near zero and monetize a portion of the government’s debt, calls current Fed policies a “dangerous gamble” and suggests Wall Street banks have been the biggest beneficiary of near zero interest rates. “Of course the market wants zero rates to continue indefinitely,” he said. “They are earning a guaranteed return on free money from the Fed by lending it back to the government through securities purchases.”

Now, with the economy teetering on the edge of further decline, the financial press is filled with speculation that the Fed will buy more mortgage-backed securities (it purchased $1.3 trillion worth through March, 2010) and government debt (it purchased $300 billion worth in 2009) and, as a consequence, inject even more printing press money into the economy through the federal government. For those of us who remember the Jimmy Carter years, Federal Reserve policy under Ben Bernanke looks like the Arthur Burns’ chairmanship on steroids. In all the years I have tracked Federal Reserve policy, I cannot remember a time when printing money was presented to the public as the economy’s saving grace and brought front and center as a national policy. Even when it was done in the past, it was done discreetly with the hope that no one would notice. Helicopter Ben is certainly living up to his reputation.

____________________________________________________________________________________________

* In fiscal year 2009, U.S federal government on-budget outlays totaled $2.32 trillion. Its on-budget receipts were $1.085 trillion. In addition, an off-budget surplus from the social security fund of $148 billion was added to receipts. The resultant deficit was over $1.086 trillion. Thus, spending in real terms actually exceeded revenues by more than twice. Source: Monthly Treasury Statement of Receipts and Outlays of the United States Government.____________________________________________________________________________________________

Gold and the new Fed policy

At the moment, concerns center around the disinflationary -- even deflationary -- tendencies of the economy, but inflation could take the limelight overnight if policy makers a

At the moment, concerns center around the disinflationary -- even deflationary -- tendencies of the economy, but inflation could take the limelight overnight if policy makers a

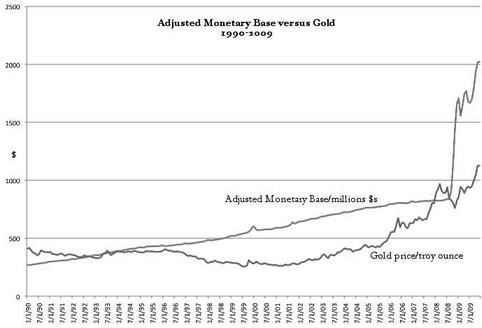

re not careful. The latent potential for inflation can be seen readily in the monetary base statistics which many economists consider one of the most reliable indicators of future inflation.

Since the beginning of the financial crisis in October 2008, the Federal Reserve has added roughly $1.5 trillion to its balance sheet mostly in the form of Treasury paper and mortgage-backed securities nearly tripling the asset side of the central bank’s ledger. Of that, the Fed still holds about $1.1 trillion in mortgage-backed securities which, at least theoretically, could be converted at some point to Treasury paper. It also holds nearly $780 billion in U.S. Treasuries, i.e., debt that has already been monetized. At this juncture, it is difficult to project the volume and pace at which mortgage-backed securities will be converted to Treasury paper, but some reports peg the conversions at about $150 billion per year, not a small sum.

The sheer volume of Fed-owned mortgage-backed securities is daunting. Now that the Federal Reserve Board has broken the ice, so to speak, the process could take on a life of its own. Recently there have been rumblings that the Fed might purchase even more mortgage-backed securities as part of a renewed quantitative easing program -- an enterprise akin to stocking up for future monetization.

We ran a similar chart to the one above in our June newsletter and decided to emphasize it again in light of the Fed’s latest policy change. As you can see by the chart, there is a direct long-term correlation between increases in the monetary base the price of gold.

“ [I]f the Fed is holding $1.25 trillion in MBS [mortgage-backed securities] formerly held by the private sector, the credit previously supplied to the MBS market by the private sector is available to purchase government debt. Hence, as long as the amount of credit supplied by the private sector is not affected by the Fed’s actions, the implications of the Fed’s actions for federal finance will be much the same as if the Fed had purchased government securities—a central bank does not have to purchase government securities to monetize debt.” (Emphasis added.)

Daniel Thornton, vice president St. Louis Federal Reserve, “Monetizing the Debt”

If you would like to broaden your view of gold market news and analysis, please feel welcome to join our free NewsGroup to receive by e-mail periodic gold news alerts, USAGOLD Market Updates, and relevant commentary like this one!

By Michael J. Kosares

Michael J. Kosares , founder and president

USAGOLD - Centennial Precious Metals, Denver

Michael Kosares has over 30 years experience in the gold business, and is the author of The ABCs of Gold Investing: How to Protect and Build Your Wealth with Gold, and numerous magazine and internet articles and essays. He is frequently interviewed in the financial press and is well-known for his on-going commentary on the gold market and its economic, political and financial underpinnings.

Disclaimer: Opinions expressed in commentary e do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. Centennial Precious Metals, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD - Centennial Precious Metals does not warrant or guarantee the accuracy, timeliness or completeness of the information found here.

Michael J. Kosares Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.