California Debt Crisis, Muni Bonds At Real Risk of Default

Interest-Rates / US Debt Feb 10, 2010 - 10:36 AM GMTBy: Richard_Shaw

California’s finances are a mess. Credit default swap rates put California among the top ten most likely to default among major governments worldwide.

California’s finances are a mess. Credit default swap rates put California among the top ten most likely to default among major governments worldwide.

If you are a California resident and think California can solve it’s own budget problems, or if you think the US government will bail them out, then you might want to own California municipal bonds for the best fit tax shelter and the higher nominal yield. However, if you doubt either of those, you may be better off owning a national or non-California muni fund, and accept a less tax efficient holding with a somewhat lower nominal yield, but with superior credit quality.

Since national muni funds tend to hold California as their largest position (perhaps around 20%), California residents might even want to consider a single state muni fund other than California, instead of a national muni fund, to avoid the California credits altogether.

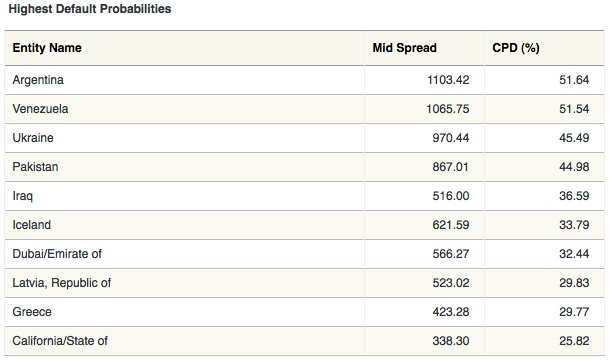

California Default Probability Among The Worst In the World

According to CMA, which is a leading credit default swap data service, California is the tenth most likely to default major government in the world, with a 26% chance of default. They are in poor company with the likes of Argentina, Venezuela, Pakistan, Latvia, Iceland, Dubai and Greece. — Brother can you lend me a dime?

California ranks near Greece, which sent the world’s stock markets into a tail spin last week, and which only relieved that stock price pressure this week when the EU began talking about some sort of assistance. Just imagine if California was seen as on the ropes like Greece.

That’s a big deal. California has the largest state economy in the US, and it’s economy is larger than all but the top 7 to 10 sovereign nations — bigger than Greece.

California, according to CMA, has roughly five times the probability of default as the US (roughly 25% to roughly 5%).

Several countries have lower default probabilities than the US, such as Hong Kong [China SAR] (4.4%) Germany (3.6%), Netherlands (3.5%) and Norway (1.8%).

That’s what the derivatives market says. What does the press say?

Bankruptcy Bloodbath May Hit Muni Bond Owners Next

(Feb. 10, Bloomberg)The biggest financial crisis since the Great Depression is squeezing municipalities across the country. Since Vallejo, California, successfully petitioned for bankruptcy protection in May 2008, California’s towns, Detroit’s schools and Pennsylvania’s capital city of Harrisburg have all talked about Chapter 9.

That should make bondholders nervous because it “questions whether a local government’s labor contracts would be surgically undone with bondholders’ rights left intact,” Fitch [Ratings] said.

… Local governments have been reluctant to reduce headcount during the recession. Since employment peaked at 115.6 million in December 2007, businesses have cut 8.5 million jobs, a 7.4 percent reduction. Local governments, by contrast, continued adding employees through September 2008, to a high of 14.6 million and have since fired 141,000 workers, or 0.96 percent, according to the U.S. Bureau of Labor Statistics.

… Chapter 9 bankruptcy is rare, according to the American Bankruptcy Institute in Alexandria, Virginia.

Only six occurred during the first three quarters of 2009, the latest period for which data is available. There were four in 2008. Since 1980, we’ve seen 227 instances, the peak year being 1991, with 18. Most have involved utilities or special districts … not cities or counties.

States can’t enter Chapter 9 bankruptcy … That hasn’t stopped municipalities from talking about it more than they have since 1994, when Orange County, California, suffered through the country’s biggest municipal bankruptcy. Bondholders have to worry if it’s more than just talk”

Muni Funds Are a Mixture of Credits

Muni-funds, whether state specific or national, include a mixture of state and local general obligations and revenue bonds. Local governments in California are not prohibited from bankruptcy. Revenue bonds, whether state or local, are at risk if the revenue streams on which they are based become inadequate.

States haven’t gone bankrupt yet, but we wonder what to call payment in IOUs by California. Wouldn’t payment of interest and/or principle in IOUs be default? Is that a possibility? Wouldn’t deferral of payments be default? Is that a possibility?

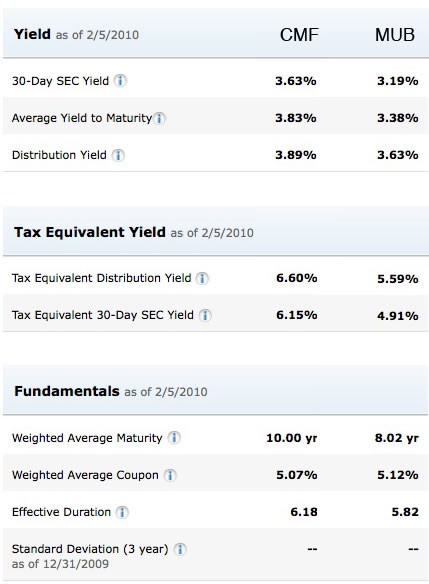

California Muni Fund vs National Fund Attributes

This table compare the attributes of CMF and MUB, the California and national muni funds from iShares. You get a little less than 1/2% more nominal yield for the extra credit risk.

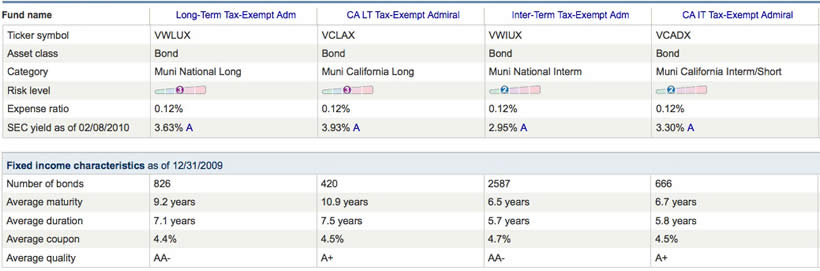

This table compares the attributes of an intermediate-term California and an intermediate-term national muni mutual fund, plus a long-term California and a long-term national muni mutual fund, each from Vanguard.

You get about 30-35 basis points for the extra risk of the California funds over the national funds.

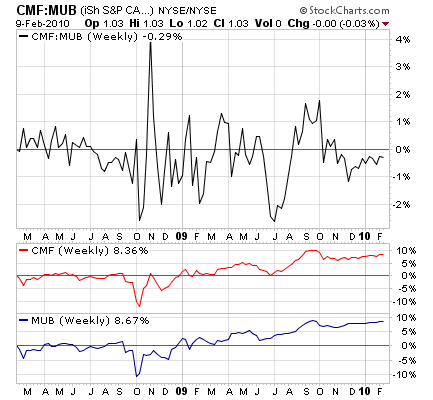

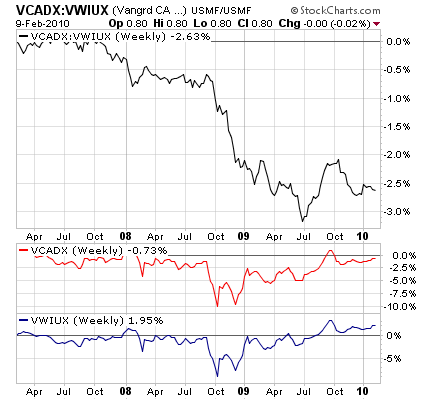

How Has the Performance Differed?

This chart shows the percentage performance for 2-years for the ratio of the price of CMF to MUB, as well as the percentage performance of each fund alone.

With the ETFs, the performance was quite similar and the California holders may have experienced a slightly better return. That seems a bit odd in light of the bad press about California’s budget, political process and prospects.

These two chart of the same dimensions for the intermediate-term and long-term muni mutual funds from Vanguard tell a different story. Note that the Vanguard funds are massively larger than the ETFs and they trade at NAV (don’t go to premium or discount as ETFs do). They are probably a better indicator of the larger reality than the smaller, newer ETFs.

These charts make it clear that California holders generally suffered an opportunity loss in nominal yield terms over holding a national fund.

Whether that translates to an opportunity loss in after-tax terms, is an individual matter.

Conclusion:

The real question is not about splitting hairs over nominal yield and after-tax yield. The big issue is whether you think there is a risk of default by the local governments and by the revenue bonds in a California fund, and whether you think the State would defer payments, or whether a court or federal order would “haircut” State GO holders contractual rights in the event of even more dire financial circumstances in California.

Two years ago, we might have opted for the risk. Today, having seen the unfair treatment of bond holders orchestrated by the US government in the auto industry bankruptcies; and having heard the hawkish talk, by Representative Franks and Senator Dodd during the height of the banking crisis, about the need for bondholders to share the pain, we would opt for better credits.

Call us worry-warts, alarmists, chickens, or “Chicken Littles”. That’s OK.

Because our clients generally have irreplaceable assets, and are currently or will soon be relying on their assets to support lifestyle, we tend to put a higher priority on risk management than on gain pursuit.

If California did default, and maybe even if it had to be bailed out, the adverse ripples in the US stock market, and maybe around the world, could possibly be quite severe. We hope the 26% probability of default posted by CMA is only a bad dream.

Holdings Disclosure:

As of February 9, 2010, we have positions in VWIUX in some managed accounts, and by client mandate we have VCADX in some other managed accounts. We do not have positions in any other securities discussed in this document in any managed account.

Disclaimer:

Opinions expressed in this material and our disclosed positions are as of February 9, 2010. Our opinions and positions may change as subsequent conditions vary. We are a fee-only investment advisor, and are compensated only by our clients. We do not sell securities, and do not receive any form of revenue or incentive from any source other than directly from clients. We are not affiliated with any securities dealer, any fund, any fund sponsor or any company issuer of any security. All of our published material is for informational purposes only, and is not personal investment advice to any specific person for any particular purpose. We utilize information sources that we believe to be reliable, but do not warrant the accuracy of those sources or our analysis. Past performance is no guarantee of future performance, and there is no guarantee that any forecast will come to pass. Do not rely solely on this material when making an investment decision. Other factors may be important too. Investment involves risks of loss of capital. Consider seeking professional advice before implementing your portfolio ideas.

By Richard Shaw

http://www.qvmgroup.com

Richard Shaw leads the QVM team as President of QVM Group. Richard has extensive investment industry experience including serving on the board of directors of two large investment management companies, including Aberdeen Asset Management (listed London Stock Exchange) and as a charter investor and director of Lending Tree ( download short professional profile ). He provides portfolio design and management services to individual and corporate clients. He also edits the QVM investment blog. His writings are generally republished by SeekingAlpha and Reuters and are linked to sites such as Kiplinger and Yahoo Finance and other sites. He is a 1970 graduate of Dartmouth College.

Copyright 2006-2010 by QVM Group LLC All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Richard Shaw Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.