Debt Fuelled Zombie Capitalism, Bernanke "Marching Ignorantly Forward"

Economics / US Debt Dec 01, 2009 - 01:20 AM GMTBy: Mike_Shedlock

Australian economist has another blockbuster post on the dynamics of debt deflation and the Great Financial Collapse. Please consider Debtwatch No 41, December 2009: 4 Years of Calling the GFC.

Australian economist has another blockbuster post on the dynamics of debt deflation and the Great Financial Collapse. Please consider Debtwatch No 41, December 2009: 4 Years of Calling the GFC.

During a debt-driven financial bubble, which is the obvious precursor to a debt-deflation, rising levels of debt propel aggregate demand well above what it would otherwise be, leading to a boom in both the real economy and asset markets. But this process also adds to the debt burden on the economy, especially when the debt is used to finance speculation on asset prices rather than to expand production–since this increases the debt burden without adding to productive capacity.

When debt levels rise too high, the process that Fisher described kicks in and economic actors go from willingly expanding their debt levels to actively trying to reduce them. The change in debt then becomes negative, subtracting from aggregate demand–and the boom turns into a bust.

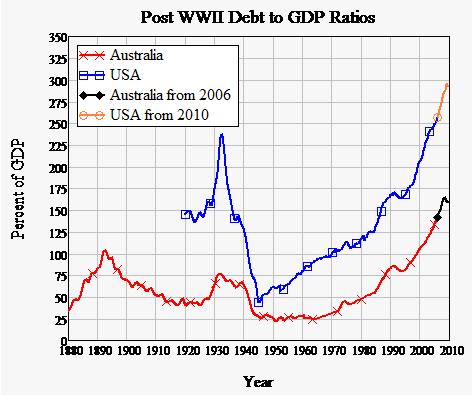

So could the global economy get out of the global financial crisis the same way it got out of the 1990s recession–by borrowing its way up? That’s where the sheer level of debt becomes an issue–and it’s why I stuck my neck out and called the GFC, because I simply didn’t believe that we could borrow our way out of trouble once more. Debt did continue rising relative to GDP for several years after I called the GFC, but it has now reached levels that are simply unprecedented in human history.

For the “borrowing our way out” trick to work once more, we would need to reach levels of debt that would make today’s records look like a picnic. What are the odds that that could happen again?

Australia and US Debt to GDP

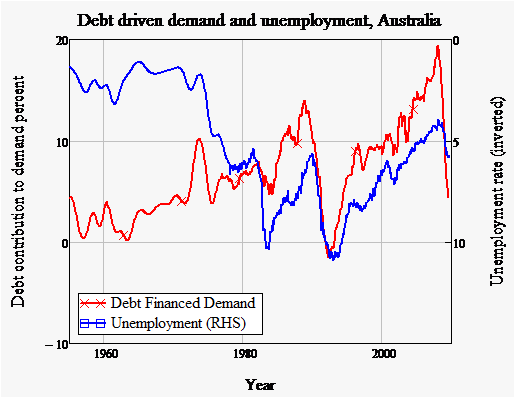

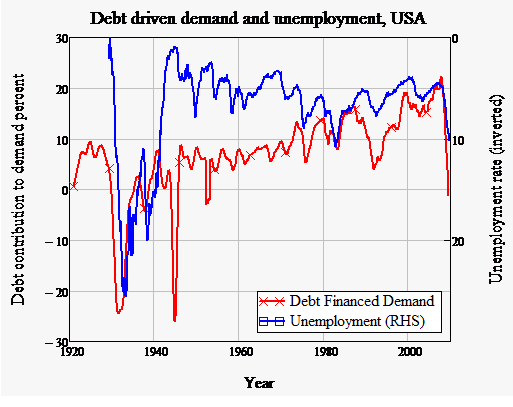

Debt has little impact on demand when the debt to GDP ratio is low–such as in Australia in the 1960s, or the USA from the start of WWII till the early 60s. But whenever the debt to GDP ratio becomes substantial, changes in debt come to dominate economic performance, as can be seen in the next two charts.

Debt vs. Inverted Unemployment Australia

Debt vs. Inverted Unemployment US

A “schoolboy error”?

In 2008 I spoke at a seminar in Adelaide that was also addressed by Guy Debelle, an Assistant Governor (Financial Markets) of the RBA. After my talk he commented that he couldn’t understand why I compared debt to GDP, since that was comparing a stock to a flow.

In dynamic terms, the ratio of debt to GDP tells you how many years it would take to reduce debt to zero if all income was devoted to debt repayment. That is an extremely valid indicator of the degree of financial stress a society (or an individual) is under.

I find that members of the general public understand this easily. Only economists seem to have any trouble comprehending it–not because it is difficult but because their own training pays almost no attention to dynamic analysis, and therefore they don’t learn–as systems engineers do–that stock/flow comparisons can be extremely important indicators of the state of a system.

Marching Ignorantly Forward

With such ignorance about the dynamics of debt, academic economists and Central Banks around the world are hoping that the crisis is behind them, even though the cause of it–excessive levels of private debt–has not been addressed. They are recommending winding back the government stimulus packages in the belief that the economy can now return to normal after the disturbance of the GFC.

In fact “normal” for the last half century has been an unsustainable growth in debt, which has finally reached an apogee from which it will fall. As it falls–by an unwillingness to lend by bankers and to borrow by businesses and households, by deliberate debt reductions, by default and bankruptcy–aggregate demand will be reduced well below aggregate supply. The economy will therefore falter–and only regular government stimuli will revive it.

This however will be a Zombie Capitalism: the private sector’s reductions in debt will counter the public sector’s attempts to stimulate the economy via debt-financed spending. Growth, if it occurs, will not be sufficiently high to prevent growing unemployment, and growth is likely to evaporate as soon as stimulus packages are removed.

The only sensible course is to reduce the debt levels. As Michael Hudson argues, a simple dynamic is now being played out: debts that cannot be repaid, won’t be repaid. The only thing we have to do is work out how that should occur.

Since the lending was irresponsibly extended by the financial sector to support Ponzi Schemes in shares and real estate, it is the lenders rather than the borrowers who should feel the pain–which is the exact opposite of the bailout mentality that dominates governments around the world.

Robbing the Poor to Bailout the Rich

Although that is a lengthy snip I left out many charts and further analysis. Inquiring minds will want to read Steve Keen's entire article.

I certainly agree with Keen on the cause of this crisis (I have been harping about the same thing for years) as well as the solution: winding down debt and letting bondholders take their share of the hit.

Instead we bailed out Fannie Mae, Freddie Mac, Citigroup, and Bank of America bondholders while raping the GM bondholders (the latter so that Obama could appease the unions). In other words, Paulson, Geithner, Bernanke, Obama, and Congress effectively conspired to rob the poor to bail out the wealthy.

Supposedly this was done so that banks would start lending, and the economy would get the Fractional Reserve benefit (using the word benefit loosely) of debt expanding 10-1.

It did not work that way, nor will it because consumer and corporate debt remain, unemployment is high and rising, debt levels are intolerable, and consumer (and bank) attitudes towards debt and credit reached a secular peak and the pendulum to deleveraging has begun.

Why Consumers Won't Borrow

Cash strapped boomers headed into retirement are finding they do not have enough money on which to retire. They are traveling less, spending less, and have too much of their assets tied up in illiquid real estate investments. Moreover, banks will not lend because there are too few qualified borrowers.

Peak Credit is in. The Effect of Household Deleveraging on Housing, Consumption and the Stock Market is massive.

Moreover, please note that the Fed cannot control sentiment of either borrowers or lenders. The Fed can merely encourage.

There is virtually no evidence consumers want to borrow. Likewise, there is virtually no evidence, none, that banks are about to go on a lending spree. Moreover, there is no evidence the Fed is attempting to force banks to lend. And finally, there is no evidence the Fed is considering charging banks a fee to keep excess reserves with the FED, or that if they did, that it would accomplish anything other than a deflationary collapse.

Bernanke's Flawed Model

The idea that excess reserves will lead to increased lending is flawed from the beginning.

What actually happens is that lending occurs and the Fed expands money supply fast enough to match reserves. Please see Fiat World Mathematical Model for details.

Factors Affecting Banks Unwillingness To Lend

- Rising unemployment will cause ...

- Rising credit card defaults

- Rising home equity loan defaults

- Rising mortgage loan defaults

- Rising commercial loan defaults

On top of that there is an increased demand for money by cash starved boomers headed into retirement who finally realize they do not have enough savings.

Excess Reserve Mirage

Factor all of upcoming defaults and much of those so called excess reserves are pure fantasy!

Bernanke Pleads For His Job

The Fed is powerless to stop this even as Bernanke is bragging about preventing another depression. Meanwhile, please consider (if you have not yet done so) Ben Bernanke Pleads For His Job; My Response to Bernanke

Bernanke: The Fed played a major part in arresting the crisis, and we should be seeking to preserve, not degrade, the institution's ability to foster financial stability and to promote economic recovery without inflation.

Mish: Ben, you sound like an arsonist taking credit for helping put out a fire, before the fire is even out, after you lit the match and tossed on the gas in the first place. For all the problems you have caused, don't you at least have the decency to show a little humility?

Stop Bernanke

Bernanke is incompetent and his self-serving whining is simply further proof of it.

Email From Yves Smith

Yesterday evening I received an Email from Yves Smith at Naked Capitalism. Yves writes:

Mish,

Your post on Bernanke last night was terrific.

FYI, Bernanke's confirmation hearing is this week. Rallying your readers could make a difference. The Internet effort that opposed the Watt amendment (which would have neutered the Paul/Grayson bill) worked. The Watt amendment would have passed otherwise.

Tell Your Senator No On Bernanke has links to the committee members and a site that has a petition. Please encourage your readers to call their senators.

Cheers,

Yves

Thanks Yves.

Please do as she suggests. Her post has a list of the members of the Senate Banking Committee.

At the very least, please PHONE your own senators ASAP.

Here is the Online Directory For The 111th Congress. Please contact your Senators! They are the ones who decide Bernanke's fate, not the House of Representatives.

I encourage you to fax them, as well. please see Speak Out - Audit the Fed, Then End It! for a list of fax numbers for every senator.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2009 Mike Shedlock, All Rights Reserved

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.