The American Dream Built on Debt, Living in Beverly Hills

Politics / US Debt Sep 08, 2009 - 01:49 AM GMTBy: James_Quinn

For the last three decades millions of Americans have been living in Beverly Hills. How can this be? Only 35,000 people reside in Beverly Hills, California. Millions have acted like they live in Beverly Hills, where the median household income is $125,000. The median household income in the United States is $50,000. There are 116 million households in the United States. Only 12 million households have income of $125,000 or more. There are 60 million households making less than $50,000.

For the last three decades millions of Americans have been living in Beverly Hills. How can this be? Only 35,000 people reside in Beverly Hills, California. Millions have acted like they live in Beverly Hills, where the median household income is $125,000. The median household income in the United States is $50,000. There are 116 million households in the United States. Only 12 million households have income of $125,000 or more. There are 60 million households making less than $50,000.

Why shouldn’t the 60 million households be entitled to live like the top 10%? This is America, where the American Dream of wealth and riches is achievable. Just one small problem. Millions chose to live like the privileged Beverly Hills elite without doing the difficult work to earn their way into the top 10%. They made these dreadful decisions of their own free will. No one forced millions of Americans to borrow and spend like drunken soldiers.

Why shouldn’t the 60 million households be entitled to live like the top 10%? This is America, where the American Dream of wealth and riches is achievable. Just one small problem. Millions chose to live like the privileged Beverly Hills elite without doing the difficult work to earn their way into the top 10%. They made these dreadful decisions of their own free will. No one forced millions of Americans to borrow and spend like drunken soldiers.

It appears that the psychology of the nation transformed in the early 1980’s. Was it the optimistic message of “Morning in America” preached to the country by Ronald Reagan? Was it the fact that the youngest Baby Boomers were turning 35, entering their prime spending years? Or, was it the long-term decline in interest rates from 18% to 1% over two decades? Whatever the rationale, millions are now drowning in deep pool of debt.

Auto Nation

Where I come from isn't all that great

My automobile is a piece of crap

My fashion sense is a little whack

And my friends are just as screwy as me

Living in Beverly Hills - Weezer

I spend 500 hours per year in my car commuting on the Schuykill Expressway to and from work. In my spare time, I’ve calculated that I will spend at least a year of my life in traffic before I retire. While commuting at 5 mph on the Schuykill, I can’t help but survey the cars I’m sharing the road with. There are thousands jamming the highways in the Philadelphia area. There are 230 million cars in the U.S. and approximately 200 million drivers. We are a car crazed nation, with the number of cars per person 40% higher than Europe, 500% higher than China and 6,200% more than India. In 1970, when I was seven years old, the number of cars per 1,000 people was 529. Today it is 765, a 45% increase in three decades. Suburban dwellers have a love affair with their cars.

The average price of a new car exceeds $30,000 today. That is a nice chunk of change. I have a mental block paying that much money for an asset, that losses 20% of its value in the 1st year of ownership. My price limit is $20,000. I finance my cars over 4 years and try to get 10 years out of them. The 6 years of no payments goes directly into savings. My frugality regarding cars probably harks back to my father buying used cars during my entire childhood. Cars were a means of transportation, not a symbol of success. It appears to me that expensive luxury cars are an attempt at filling a psychological or emotional void in people’s lives. We spend half our lives in cubicles or offices and the other half in our shielded houses with gates and fences to keep people at a distance. The only time we are seen by others is on the highways and byways. An expensive sports car tells the world you are a success. A luxury car is a futile attempt at increasing your perceived happiness. Your fashion sense may be a little whack, but your car isn’t a piece of crap.

This brings me to the conundrum that has confounded me as I drive to work each day. There appears to be many more BMW and Mercedes vehicles on the road than people with enough income to own one of these vehicles. How can this be? I was befuddled. After a little research it became quite clear. The graphs below tell the whole sordid story. Borrow today, live like a Beverly Hills hotshot, roll the loan or lease into the next loan or lease in 3 years, and don’t be troubled about the future. According to the Federal Reserve, consumer non-revolving debt grew from $300 billion in 1980 to $1.6 trillion today. About $1 trilion of this is auto loans. The average automobile loan today is for 63 months, with some going as high as 84 months, compared with an average of less than 48 months in the early 1990s. In 1997 banks financed an average 89% of a new vehicle's price. The average loan amount was $17,000. In 2007 banks financed 101% of a new vehicle’s price, since consumers borrowed to cover the amount they were upside down on their trade-in. The average loan amount is now $29,000. A full 40% of all trade-ins involve upside-down car loans. The average American car “owner” is in debt up to their eyeballs and upside down on their loan, but at least they look like a million bucks in the eyes of their neighbors and co-workers. Looking marvelous is what passes for achievement today.

Of course, it takes two to tango. A car buyer with no money wouldn’t be able to drive that beautiful BMW X5 or that Mercedes ML350 unless someone loans them the money to do so. This is where the creative geniuses from Wall Street entered the picture. Auto loans were securitized into packages and sold off to investors. The banks and finance companies who initiated the loans did not care if the loans went bad. Their sole intent was to move cars off the lots, not lose sleep about silly details like credit scores, income, or ability to pay back the loan. It worked wonders for the car companies. Annual sales rolled along at a 16 million per year clip. Car executives and bankers made ungodly salaries and bonuses. Then reality set in. Many borrowers couldn’t really afford their loans. Delinquency rates have soared to all time highs in the 10% range and are headed higher. The securitization market froze and annual sales have plunged below 10 million units. Another Wall Street success story.

The ability of car companies to make payments extremely low through long-term loans and leases is the reason an average Joe making $50,000 per year can drive a BMW and resemble someone making $150,000 per year. Chrysler and Ford generated 20% of their car sales through leases, while GM led the pack at 40% of their sales. Many of these leases were for SUVs and other giant gas guzzlers. When gas prices soared in 2008, the residual value of these gas guzzlers plummeted as the resale market disappeared. Ford and Chrysler have written off billions. The king of the hill, GMAC accumulated $33 billion of lease assets and is slowly but surely writting off $14 million of these “assets”, while the taxpayer funds their future bad leases.

Leases have made it possible for millions of Americans to drive the hottest luxurious wheels their limited cash budgets would not permit them to buy. Auto makers loved leases because they could sell higher-priced vehicles, which generate a gusher of profits in the short-term. By piling on inducements of their own, such as rebates or 0% financing deals, auto makers were able to subsidize consumers' lease payments further. As a result, Americans have been able to have access to vehicles their parents never envisioned driving. Leases allowed anyone to look like a rock-star, driving luxury sedans, sports cars and Hummers costing $40,000 to $60,000. The Wall Street Journal describes a common scenario:

For Richelle Babcock, a mother of two young boys in Ann Arbor, Mich., leasing has made it possible to get new cars every couple of years. A few years ago, she took advantage of a trade-in deal and other incentives Chrysler was offering and got a $180-a-month lease on a 2006 Jeep Commander with a sticker price of about $35,000. There's "no way," Ms. Babcock says, that she would have bought the Commander outright. "I don't want to have to own it and drive it forever." Indeed, in December she turned it in and instead leased a new 2008 Commander. Her payment roughly doubled, but that's mainly because the lease is much less restrictive about her annual mileage.

I’d like to ask Ms. Babcock a couple questions. Does she have college education funds set up for her two young boys? Does she have an emergency fund of 6 months of living expenses? How much does she have in her retirement account? I’m sure she would be offended by such questions. It’s her right to get a brand new car every two years. These are the people who can’t distinguish a need from a want.

This brings me to the chapter in this horror story that really sticks in my craw. I drive through West Philadelphia every day. The neighborhoods are decrepit, with boarded up houses, trash strewn vacant lots, grade schools that resemble prisons, and a substantial number of unemployed folks shuffling about from morning to night. These neighborhoods appear to have five times as many BMWs and Mercedes as my suburban upper middle class neighborhood. According to the U.S. Census, West Philly is a predominantly Black neighborhood, with a large proportion of unmarried high school dropouts living in poverty, occupying dilapidated houses with Direct TV dishes on their roofs. According to the U.S. Census, my neighborhood is occupied by people who are five times higher on the income scale.

The August unemployment figures from the BLS show that the unemployment rate for Black men is 17.0% versus 10.6% last August and versus 9.3% for White men. The unemployment rate for Black teenagers is 34.7%. With these figures, you would expect unrest, looting, and riots in West Philly. The civil unrest hasn’t happened in West Philly or anywhere else. I think I’ve figured out why. Just picture a 20 year old unemployed Black man calling his homies on his iPhone urging them to drag themselves away from staring at their 52 inch HDTVs with 600 stations on their Direct TV network, hop into their BMW X5, and drive over to the comprehensive healthcare riots. It’s not happening. Our elected officials, Federal Reserve and banking cartel have chosen to buy off the poor at the expense of the middle class, so the rich can get richer.

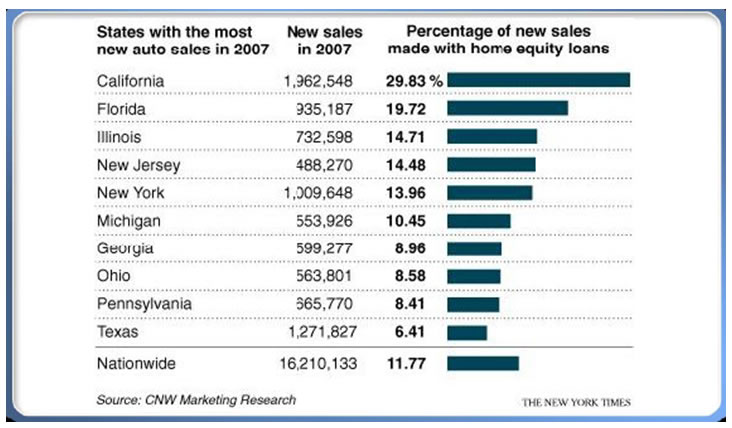

Easy money allows the poor to live like the rich. This explains why people in West Philly are able to drive $50,000 one year old BMWs, while I choose to drive an 8 year old CRV with 130,000 miles. My choice was to finance my $20,000 car over 4 years at 7%. I had a $500 monthly payment for 4 years and then was able to save $500 per month for the next 6 years, banking $36,000 in savings. The auto financing companies GMAC, Ford Credit, and Chrysler Credit offer rebate incentives, 7 year loans, and 0% interest to entice everyone to drive BMWs and Mercedes for a monthly payment below $500. The poor are more likely drawn to three year leases with even lower monthly payments. You can lease a BMW for $399 per month or lower. Once you are lured into 3 year leases or 7 year loans, you are ensnared in a lifetime car payment, never saving a dime. Over 4 decades, my method will leave me with $200,000 of savings. A perpetual car payment will leave you with $0 of savings. Millions have chosen this negligent path. Not only did they pursue this path, they hurtled themselves down the path with gusto by borrowing against their houses to buy cars. The numb-nuts in California and Florida were the worst offenders.

A drug addict still needs a dealer to get their fix. Politicians in Washington with their cohorts in crime, the Federal Reserve and the banking cartel, provided the drug of easy money. The unholy combination of a psychological need to appear successful and easy money has created a deadly recipe for those in the middle class who drive their modest cars for 10 years and save for the future. The black magic of securitization has allowed banks and finance companies to bestow credit card cards and car loans to high school dropouts making $20,000 per year in West Philly with no concern about getting repaid. They packaged this future bad debt, paid off Moody’s and S&P to rate it AAA, and dumped it on suckers throughout the world. Now, auto loan delinquency rates are at all time highs, 1.7 million cars were repossessed in 2008, with another 2 million likely to be repossessed in 2009.

The underprivileged people in West Philadelphia don’t comprehend that politicians and bankers are actually keeping them entrapped in poverty by providing them with easy credit and persuading them that making perpetual payments for cars, TVs, and other material goods is a normal lifestyle. When reality sets in and these people stop making their payments, no trouble for them. As the financial system came crashing down due to the millions of bad loans made by the banking cartel, their protectors Hank (Goldman) Paulson and Ben (Helicopter) Bernanke funneled TRILLIONS of your tax dollars and your children’s tax dollars and their children’s tax dollars to the banks that committed these crimes. The poor people in West Philly don’t pay taxes, so they got to drive BMWs and watch 52 inch TVs for awhile, and are left relatively unscathed. The middle class is paying the bill, losing millions of jobs, while seeing their 401ks drop by 40% and they are still driving their 10 year old cars. Government now wants you to pay more so the poor will have health insurance when they get injured in a BMW accident.

What’s My Payment?

I didn't go to boarding schools

Preppy girls never looked at me

Why should they, I ain't nobody

Got nothing in my pocket

Living in Beverly Hills - Weezer

For the last three decades you didn’t need anything in your pocket to attract a preppy girl. You just needed to whip out one of your 10 credit cards and act like a Beverly Hills hotshot. Cash was for suckers. Credit cards are so easy to use. You just pull it out, buy whatever you desire at that moment and make a minimum payment every month until infinity. We’ve become a minimum payment nation. If you can handle the minimum payment, it’s yours. In 2006, the Census Bureau determined that there were nearly 1.5 billion credit cards in use in the U.S. A stack of all those credit cards would reach more than 70 miles into space -- and be almost as tall as 13 Mount Everests. Consumer credit debt has risen from $400 billion in 1980 to $2.5 trillion today. Consumers have an average of 5.4 credit cards with $973 billion outstanding. The average outstanding credit card debt for households that have a credit card was $10,679 at the end of 2008. The average American with a credit file is responsible for $16,635 in debt, excluding mortgages, according to Experian. The most fascinating fact is that the top 10 U.S. credit card issuers held an 87.55% market share of $973 billion in general purpose card outstanding in 2008. These 10 banks are coincidently the same banks that brought down the financial system (Bank of America, Citicorp, JP Morgan Chase, Wells Fargo, Capital One, HSBC, American Express, Discover, US Bank, USAA).

Consumer Credit Debt

It has taken Americans three decades of overspending and under-saving to get into this pickle. As you may notice, consumer credit debt is $2.5 trillion and has barely budged downward. The pundits and economists predicting a strong economic recovery are blind to the truths of consumer debt. With actual unemployment exceeding 16.8%, 9 million people forced to work part-time wanting to work full-time, the work week at all time lows, and banks shutting down credit lines, consumers will be reducing or defaulting on their debt for years. With 70% of the economy dependent on consumer spending, there is absolutely no chance of a strong recovery. Household debt service payments as a percentage of disposable income reached a peak of 14.2% in 2007 and have plunged all the way to 13.5% today. Disposable income is plunging as people without jobs don’t have anything to dispose of.

A paradigm shift is occurring and the mainstream media, mainstream economists, and clueless politicians running this country do not understand the implications. Three decades of debt accumulation is not resolved in two years. It will take decades of reduced spending, paying down debt, and writing off debt. The Federal Reserve, banking cartel, and politicians are franticly attempting to make consumers borrow and spend with TARP, TALF, Cash for Clunkers, and numerous other debt increasing gimmicks. The consumer is tapped out. The median 401k balance in the U.S. is $26,000. Boomers realize they are 60 years old and have $50,000 of retirement savings and $30,000 of credit card debt. They are learning the brutal lesson of needs versus wants. The implications are disastrous for those dependent on a consumer spending society (i.e. retailers, restaurants, hotels, car makers, homebuilders).

There are 25% of households in the U.S. with no credit cards. Of those with a credit card, 30% pay off their balances each month. These are the people that have chosen to live within their means. They understand the difference between needs and wants. They appreciate the notion of delayed gratification. You buy things when you can afford them. You live a life of thrift and frugality, save for your family’s future, and live within the parameters of a budget. What a concept. The TARP accepting banks that control 87% of the credit card market are recording losses on an unprecedented scale. But no need to worry, the middle class tax payers come to the rescue again. Orwell must be rolling in his grave at the government originated Troubled Asset Relief Program. “Troubled” is an Orwellian word to describe debt that was knowingly issued by banks to people who would never pay it back in order to generate outrageous fees and bonuses for the executives issuing the debt. When the debt predictably went bad, “Relief” was provided to the criminal bankers on the backs of the taxpaying middle class. Bank of America, Wells Fargo and JP Morgan are bigger than they were before the financial crisis, their executives are still making millions, their “assets” are still “troubled”, and we continue to pay the bill, as will our children and grandchildren. Don’t worry. Ken Lewis, Vikram Pandit and Jamie Dimon’s grandchildren will inherit hundreds of millions of your tax dollars from their banker grandpas.

I Wanna Be Just Like A King

Beverly Hills... That's where I want to be! (gimme, gimme)

Living in Beverly Hills...

Beverly Hills... Rolling like a celebrity! (gimme, gimme)

Living in Beverly Hills...

Look at all those movie stars

They're all so beautiful and clean

When the housemaids scrub the floors

They get the spaces in between

I wanna live a life like that

I wanna be just like a king

Take my picture by the pool

Cause I'm the next big thing

Living in Beverly Hills - Weezer

The 8,000 square foot castle-like McMansions are the symbol of extravagance and excess that represent the worst of America’s hyper-consumerism culture. Even though the family unit has gotten smaller since 1970, the average home size has grown from 1,400 sq ft to 2,500 sq ft. McMansions are clearly not necessary due to family size. Essentially, it is another example of Boomers attempting to show the world they are successful. The bigger and gaudier the house the more flourishing you appear. This psychological need for approval combined with the big lie pushed by the National Association of Realtors that a house is always a great investment to generate the biggest housing bubble in history. One glance at Robert Shiller’s chart showing home prices versus population growth and CPI, proves beyond a shadow of a doubt that we have experienced a manic increase in house prices. It is also unambiguous that the downward spiral is not nearly complete. The housing cheerleaders continue to forecast a housing recovery that is still 5 years in the future.

It is mind boggling that home prices could have surged that high while owner’s equity has plunged from 70% in 1980 to 45%. People didn’t earn the McMansions, they borrowed them. The Federal Reserve created spiral in prices upward has trapped millions of late comers in houses that are worth 20% to 30% less than the mortgage debt that is strangling them. Over 16 million home occupiers (not homeowners) are underwater in their mortgage. The decisions to buy houses with nothing down, using option ARM loans, were free choices made by people who should have known better. The decisions to make subprime loans to people making $30,000, to make no-doc loans, and to not verify income or assets were purposefully done to enrich the bankers, mortgage brokers, and real estate agents. The $10.5 trillion of mortgage debt will need to be paid down or written off over many years, before the housing market will reach equilibrium again.

The dream of living like a king in Beverly Hills has come to a shattering conclusion. As mortgage delinquencies soar to all-time high levels, the kings are being led kicking and screaming to the foreclosure guillotine. Neighborhoods of McMansions in California, Phoenix, Florida, and Las Vegas are weed infested crime ridden high end ghettos. The American dream of home ownership spouted by George Bush and legislated through Fannie Mae and Freddie Mac has turned into a debt induced nightmare.

MORTGAGE DELINQUENCIES

The Alt-A reset crisis which will begin in 2010 and not crest until 2013 is coming down the tracks at a swift pace. The credit criteria used by the banks that doled out Alt-A loans were as lax as the subprime loans that precipitated this crisis. These loans already have delinquency rates of 33%, even before these resets kick in. There is no evading this calamity. There is also no doubt how the Federal Reserve, Treasury, and government politicians will handle this next emergency. If you have lived in a modest home, made your mortgage payments, didn’t use your home equity to buy a Mercedes ML350, and pay your taxes, the government will seize your taxes again and dispense them to the profligate borrowers and criminal bankers. You will pay your mortgage and the mortgages on millions of other houses.

Alt-A Loan Resets

Give Me Something I Need

No I don't - I'm just a no class, beat down fool

And I will always be that way

I might as well enjoy my life

And watch the stars play

Beverly Hills... That's where I want to be! (gimme, gimme)(gimme,gimme)

Living in Beverly Hills...

Beverly Hills... Rolling like a celebrity! (gimme, gimme) (gimme,gimme)

Living in Beverly Hills...

Living in Beverly Hills – Weezer

The era of excess, gluttony, and overindulgence is coming to a wretched ending. The unraveling is complete. We have entered an epoch of crisis that will last for two decades. The coming winter will be cold, bitter and harsh on most Americans. Millions are learning that living in Beverly Hills was just a delusionary dream. They are just no class, beat down fools and I will always be that way. It is time to enjoy the more basic aspects of life: family, friends, enjoying what you’ve got, and leaving the world a better place for our children and grandchildren. It comes down to choices. It is time for Americans to grow up and take responsibility for their actions and their futures. They must realize that the Federal Reserve and the banking cartel are the only ones profiting from ever expanding debt. The Rising Debt Era has not benefited the borrowers as they borrowed toys they couldn’t afford. The beneficiaries were Bank of America, Citicorp, Wells Fargo, JP Morgan and the other members of the cartel. The 10 biggest banks in the country control 48% of all deposits, 50% of the mortgage market, and 87% of the credit card market, supported and protected by the Federal Reserve and Treasury Department. The “too big to fail” continue to get bigger, as the FDIC will shutter 500 smaller banks in the next year.

The banking cartel has no intentions of relinquishing power. It will be left to average Americans to make the right choices. Government will continue to push Keynesian Cash for Clunkers publicity stunts to keep their debt civilization going. The consumer society needs to be put to rest. Americans must ask themselves a few questions. Do you really need a $35 Aeropostale tee shirt when you can get an identical tee shirt at Kohl’s for $6? They were both made in the same Chinese sweatshop by 13 year old children. The difference is that Aeropostale will say it is a “green” shirt because there was no air conditioning used in the sweatshop ruining the ozone layer. What exactly does a pair of $345 Botticelli shoes do that a pair of $35 shoes from Payless Shoe Source won’t do? Does a $10,000 Rolex watch tell time better than a $50 Timex? Will an $85,000 BMW 750LI get you to the supermarket better than a $15,000 Honda Civic?

When I started researching this article, I came across a Heritage Foundation report called How Poor Are America's Poor? Examining the "Plague" of Poverty in America. The article makes it clear that the poor in America do not fit the portrayal of living in poverty when compared to real poverty in Africa and much of the developing world. The report concludes:

The typical American defined as "poor" by the government has a car, air conditioning, a refrigerator, a stove, a clothes washer and dryer, and a microwave. He has two color televisions, cable or satellite TV reception, a VCR or DVD player, and a stereo. He is able to obtain medical care. His home is in good repair and is not overcrowded. By his own report, his family is not hungry and he had sufficient funds in the past year to meet his family's essential needs. While this individual's life is not opulent, it is equally far from the popular images of dire poverty conveyed by the press, liberal activists, and politicians.

The main causes of child poverty in the United States are low levels of parental work, high numbers of single-parent families, and low skill levels of incoming immigrants. By increasing work and marriage, reducing illegal immigration, and by improving the skill level of future legal immigrants, our nation can, over time, virtually eliminate remaining child poverty.

The Heritage Foundation report missed one key aspect of being poor in America. The politicians and banks have taken advantage of the poor’s lack of education and ignorance regarding the perils of debt and have enslaved them in a monthly payment plantation. The poor don’t own the cars, electronics, homes and appliances. They are renting them until they can no longer make the payments. The politicians have colluded with the Federal Reserve and banks to provide bad money to the poor in order to keep them satiated and pliable. When the debt predictably goes bad, the banks are compensated by their bought government cronies with middle class’ tax dollars.

"When I was a child I spoke as a child I understood as a child I thought as a child; but when I became a man I put away childish things." I Cor. xiii. 11.

Americans, led by the Baby Boom Generation, have been living like spoiled children for thirty years. They have thought like children, with instant self-gratification as their sole aspiration. It is time to put away childish things. Hard times have arrived. There is no easy way out. We have kicked the can down the road for a generation. Tomorrow has arrived. Our long-term structural problems have now collided with our current debt induced tragedy. Current policies that further the expansion of debt will ultimately lead to the collapse of our economic system. The timing is all that is in doubt.

Give me something that I need

Satisfaction guaranteed to you

What's the consolation prize?

Economy sized dreams of hope

When I was a kid I thought

I wanted all the things that I haven't got

Oh. I learned the hardest way

Then I realized what it took

To tell the difference between

Thieves and crooks

A lesson learned to me and you

Give me something that I need

Satisfaction guaranteed

Because I'm thinking about

A brand new hope

The one I've never known

Cause now I know

It's all that I wanted

Macy’s Day Parade – Green Day

Materialism has not provided what we needed. As our current crisis deepens, luxury cars and Rolex watches will seem so phony. Childish symbols like yellow rubber wristbands and yellow, pink, and rainbow ribbon stickers on our SUVs do nothing to change the world. When you are walking down the street, look people in the eye and say hello rather than staring at your feet or checking your latest email or text message on your “crackberry”. Deeper personal relationships with family and friends will become crucial. The thieves and crooks occupy Washington DC and Wall Street. We do not need what they are selling. Economy sized dreams of hope will sustain the citizens of this great country. Instead of accumulating stuff, give your stuff to people who need it. Donate your stuff to Purple Heart, the Salvation Army, or any other worthy charity. Donate your time to Manna, Habitat for Humanity, or any other worthy cause. Don’t delegate your role in caring for your fellow citizens to the government. Americans will soon realize that what they wanted was not what they needed.

To join the discussion of how to take back our country from the banking cartel and government central planners, go to www.TheBurningPlatform.com.

By James Quinn

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer, and are not sponsored or endorsed by his employer.

© 2009 Copyright James Quinn - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

James Quinn Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.