Speculators Return to Stocks, Commodities and Resource Currencies

Stock-Markets / Investing 2009 Apr 02, 2009 - 01:19 PM GMTBy: Gary_Dorsch

There are times when it pays to be a contrarian, to think outside-the-box, to bet against the conventional wisdom of the crowd, and ignore the chatter of the media. Usually at key turning points, and the beginning of important new market trends, the fundamentals do not explain the behavior of the market. It is at these critical junctures, where sudden shifts in price trends can occur, - big percentage gains or losses are registered.

There are times when it pays to be a contrarian, to think outside-the-box, to bet against the conventional wisdom of the crowd, and ignore the chatter of the media. Usually at key turning points, and the beginning of important new market trends, the fundamentals do not explain the behavior of the market. It is at these critical junctures, where sudden shifts in price trends can occur, - big percentage gains or losses are registered.

Sometimes, traders begin to notice that price swings in the marketplace are reacting contrary to what the news headlines are conveying. For instance, on April 1 st , the Dow Jones Industrials futures surged 550-points higher from their lowest level of the day, following news from ADP, that 742,000 American workers had lost their jobs in March, a staggering decline, with 5.7-million workers collecting jobless benefits. April Fools!

Yet some of the most dramatic trends in market history have begun with little or no perceived change in the economic forces which cause commodity or stock prices to move higher, or lower, or stay the same. By the time these economic mega-changes become recognized by the mainstream media, a new trend is already far underway.

The world is mired in a “Great Recession,” said IMF chief Dominique Strauss-Kahn, after a recent flurry of negative economic news. “This recession may last a long time unless the policies we're expecting are put in place, in which case 2010 can be a year of return to growth.” The world economy has not contracted since 1945, because usually, a recession in some countries is balanced-out by economic growth from elsewhere.

Kahn warns this recession would be deeper and more wide-spread. “The IMF expects global growth to slow below zero in 2009, the worst performance in most of our lifetimes. Continued de-leveraging by world financial institutions, combined with a collapse in consumer and business confidence is depressing domestic demand across the globe, while world trade is falling at an alarming rate and commodity prices have tumbled.” Yet judging by the recent 25% surge in global stock markets, perhaps Mr Kahn is looking at the economic situation thru the rear-view mirror, and not the front windshield.

The latest 23% surge in the Dow Jones Industrials towards the psychological 8,000-level, is its seventh significant rally of 1,000-points or more, since October 2007. During the bear market from 1929 to the bottom in 1932, the Dow Industrials fell by almost 90-percent. There were six bear-market rallies during that stretch, with returns of more than 20%, each one fueling a sense of renewed optimism. Yet each counter-trend rally ultimately fizzled-out and unraveled, before market indexes skidded to new lows.

The latest 23% surge in the Dow Jones Industrials towards the psychological 8,000-level, is its seventh significant rally of 1,000-points or more, since October 2007. During the bear market from 1929 to the bottom in 1932, the Dow Industrials fell by almost 90-percent. There were six bear-market rallies during that stretch, with returns of more than 20%, each one fueling a sense of renewed optimism. Yet each counter-trend rally ultimately fizzled-out and unraveled, before market indexes skidded to new lows.

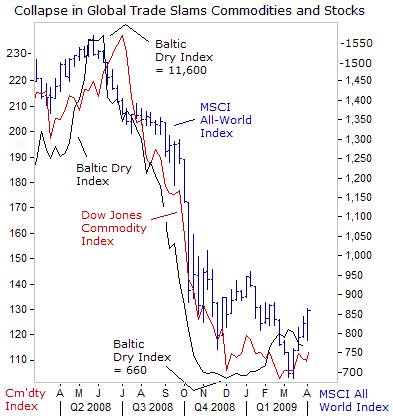

As 2009 opened, three weeks before Barack Obama took office, the Dow Jones Industrials closed at 9,034 on January 2 nd , its highest level since the autumn panic. The Dow Industrials melted down to as low as 6,500 on March 6 th , for an overall decline of 30% in two months, and to its lowest level in 12-years. The Dow Jones Commodity Index skidded to a six-year low, after tumbling by 57% since last July.

Commodity indexes suffered the biggest rout in five-decades, tumbling in tandem with global stock market meltdowns for the first time since 2001. After Lehman Brothers defaulted on $270-billion of debt in mid-September, the American and European banking cartels responded by cutting-off credit to hedge-fund traders dealing in commodities. In turn, many traders were forced into liquidations of base metals, crude oil, and grains, at bargain-basement prices . Others were forced into commodity and stock sales in order to meet obligations in the credit default swap market.

Commodity indexes suffered the biggest rout in five-decades, tumbling in tandem with global stock market meltdowns for the first time since 2001. After Lehman Brothers defaulted on $270-billion of debt in mid-September, the American and European banking cartels responded by cutting-off credit to hedge-fund traders dealing in commodities. In turn, many traders were forced into liquidations of base metals, crude oil, and grains, at bargain-basement prices . Others were forced into commodity and stock sales in order to meet obligations in the credit default swap market.

Tight-fisted bankers crushed the global shipping industry by suspending “letters of credit” that importers and exporters rely upon to finance overseas trade. Of the $14-trillion of goods and materials that are shipped across the high-seas each year, roughly 90% of the cargo is financed with “letters of credit,” issued by bankers, guaranteeing payment to the shipper, once the goods are delivered to the buyer. With banks cutting-off “letters of credit,” the wheels of global shipping ground to a halt.

The Baltic Cape-Size Index, which measures the cost of shipping coal, iron ore, and steel, plunged 95% in just five-months. At the market's peak in June, daily charter rates for 170,000-ton Cape-Size bulk carriers cost $234,000. In November, it was available for $3,000 /ton, - and below break-even. Amid the worst credit crunch since the Great Depression of the 1930's, roughly $ 30 -trillion was erased from world stock markets from the peak in October 2007, adding to the doom and gloom in the commodity sector.

Still, commodities have evolved into a fashionable asset class, with the development of commodity futures indexes. Portfolio managers plowed as much as $280-billion into commodity indexes, over the past several years, intrigued by their diversification benefits, especially their historic negative correlations to bonds, while providing a viable hedge against inflation, and a devaluation of the US-dollar. The Dow Jones AIG Commodity Index returned a 24% annualized gain, compared to a scant 0.6% rate of return for the S&P-500 Index, over the seven-year period, ending June 30, 2008.

Tokyo Traders bet on Global Recovery in H'2,

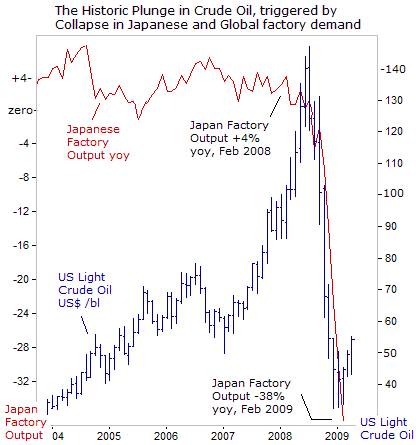

The latest string of dismal data from Japan underlines the unraveling of world demand for industrial commodities. Japanese industrial production fell -9.4% in February, following a record -10.2% plunge in January, contracting for a fifth straight month, the longest losing streak since 2001, as exports collapsed -49% from a year ago. Toyota Motor plans to cut thousands of jobs and slash domestic production by half this quarter.

Japan 's economy contracted at an annualized rate of -12.1% in the first quarter, the country's worst performance since World War II. Economics and Fiscal Policy chief Kaoru Yosano told the media, “We're in a very grave situation. Japan is being hit by a wave of weakening global demand.” Bank of Japan Policy Board member Atsushi Mizuno was more direct, “It's not too much to say falling exports are triggering a downward spiral of production, incomes and spending. It looks as if the Japanese economy is falling off a cliff. There's really nothing out there to drive growth,” he warned.

Japan 's economy contracted at an annualized rate of -12.1% in the first quarter, the country's worst performance since World War II. Economics and Fiscal Policy chief Kaoru Yosano told the media, “We're in a very grave situation. Japan is being hit by a wave of weakening global demand.” Bank of Japan Policy Board member Atsushi Mizuno was more direct, “It's not too much to say falling exports are triggering a downward spiral of production, incomes and spending. It looks as if the Japanese economy is falling off a cliff. There's really nothing out there to drive growth,” he warned.

Exports to the US tumbled by a whopping -58.4% from a year earlier, led by a sharp drop in automobile exports, which slid 71-percent. The record drop in exports is forcing Japanese companies to fire workers, and is depressing wages, -3.5% lower from a year ago. Consumer prices will probably begin showing year-over-year declines as soon as next month, and the declines could accelerate, portraying an economy that is caught in the thicket of a deflationary spiral and an outright depression.

Yet market contrarians, who trade the Nikkei-225 index in Tokyo , argue that the collapse in Japanese factory activity is now at rock-bottom levels, and is already discounted in the marketplace. The Nikkei-225 closed above the 8,700-area on April 2 nd , roughly 25% above its March 10 th lows, and Tokyo traders are ignoring the negative news on the Japanese economy, such as the latest Tankan survey, indicating the worst business sentiment in 30-years, and instead, are betting on an export recovery in the second half of this year.

Japan is the world's third-biggest oil consumer, and due to its sluggish industrial output, the country imported 14% less crude oil in March, (4.26-million barrels a day), compared with a year ago. US oil demand is 5% lower than a year ago, the Energy Information Administration said on April 1 st , at 19.1-million bpd. But signs of a recovery in the global stock markets could signal a revival of the G-7 and emerging industrial sectors, bolstering demand for crude oil and energy commodities in the months ahead.

Copper Climbs above $4,000 /ton in London ,

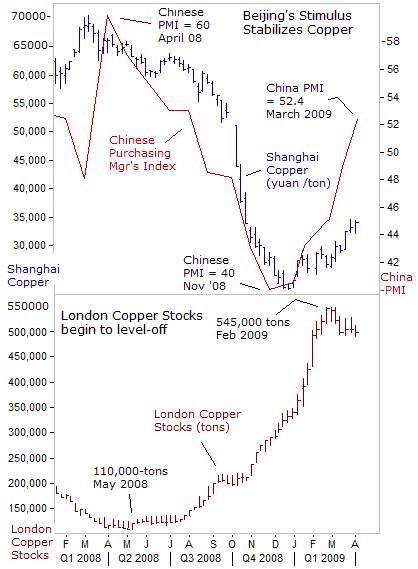

So far, the metal which has outperformed to the upside this year - is copper, and it's attracted the strongest investor portfolio flows in the mining sector of global equity markets. London copper prices are up 35% this year, the biggest quarterly rise in three-years. Shanghai copper's 40% quarterly surge is the biggest on record. The premium for Shanghai copper above the London benchmark, widened to 1,670 yuan per ton, enough to encourage local merchants to start importing the red-metal into the country.

So far, the metal which has outperformed to the upside this year - is copper, and it's attracted the strongest investor portfolio flows in the mining sector of global equity markets. London copper prices are up 35% this year, the biggest quarterly rise in three-years. Shanghai copper's 40% quarterly surge is the biggest on record. The premium for Shanghai copper above the London benchmark, widened to 1,670 yuan per ton, enough to encourage local merchants to start importing the red-metal into the country.

Traders estimate that Beijing's State Reserves Bureau, which manages the country's strategic stockpiles, is buying 300,000-tons of copper, and speculate that it could buy up to 1.2-miilion tons this year. The flow of copper from the London into the Shanghai Futures Exchange has begun to make a noticeable dent in the unsold supply held in London Metal Exchange's warehouses, whittled down by 10% since mid-February. The SRB has been the big driver behind rising copper prices this year, while industrial demand outside of China has played little part in the copper price rally.

Output at Chile's Codelco, the world's #1 copper miner has tumbled 10% to 383,000-tons in February, compared with a year earlier, the eighth straight monthly drop, as production fell at its biggest mines, and falling ore grades at aging mines at dented output. In response to the deepest economic downturn in decades, copper miners worldwide have cutback output by 550,000-tons this year, or 3.5% of annual supply.

On March 25 th , Chinese central bank adviser Fan Gang, said the government's accelerating investment in the economy was showing signs of boosting growth. China 's Purchasing Manager's Index, which measures activity in the factory sector, jumped to a reading of 52.4 in March from 49.0 in February. Beijing 's factory survey has perennially come under the suspicion of fraud by outside analysts, who say government apparatchiks manipulate the numbers. In sharp contrast, a private survey of Chinese manufacturers found the PMI slipping 0.3-points to a reading of 44.8 in March.

Still, with urban populations in China currently standing at 40%, compared with 81% in the US, more steel is needed to build railways, more coking coal is needed to smelt the steel, more energy is needed to power autos, and more copper to build new homes. All of this has little to do with the short-term effects of credit crunches, recessions, and belt-tightening around the world, as they are largely government mandated projects. Chinese premier Wen Jiabao has also vowed to “significantly increase” investment this year, to meet an 8% economic growth target.

Emerging nations with growing populations recognize the need to continue spending on infrastructure, irrespective of short-term blips. Commodity markets will always be volatile over the short term, but copper miners are cautiously optimistic, that China will keep the red-metal above the break-even point of $2,100 /ton thru 2009, when the eye of the credit crunch storm is expected to pass, and followed by an economic recovery in 2010.

Emerging nations with growing populations recognize the need to continue spending on infrastructure, irrespective of short-term blips. Commodity markets will always be volatile over the short term, but copper miners are cautiously optimistic, that China will keep the red-metal above the break-even point of $2,100 /ton thru 2009, when the eye of the credit crunch storm is expected to pass, and followed by an economic recovery in 2010.

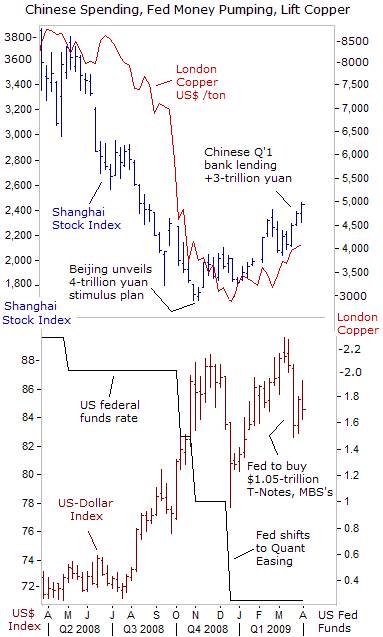

The Shanghai red-chip index posted a 30% gain in the first-quarter, closing above its February peak of 2,400-points, to its highest level in seven-months. If the Shanghai red-chip index confirms a break-out above the 2,400-point resistance, it may target the next major technical level, seen at 2,600-points. Massive new loans extended by Chinese banks in the first quarter, estimated at 3.5-trillion yuan, flooded Chinese markets with liquidity, and are nearly equal in size to the government's 4-trillion yuan stimulus program.

China 's capital markets might be awash with liquidity in the second quarter and excess money could reach 1-trillion yuan ($146 billion), leaving a huge pool of money sloshing in the markets, if the People's Bank of China doesn't drain funds via bill or bond sales in the months ahead. By artificially inflating the Shanghai red-chip index, which is rising despite a 37% collapse in industrial profits, Beijing creates the illusion of a recovery in the Chinese economy, which attracts speculators to copper and other commodities.

Renewed Appetite for Aussie /Canadian dollar

The mining industry has been a key contributor to Australia 's economic growth and its budget revenues during the past decade. But slumping commodity prices and falling demand from Australia 's big Asian customers has seen mining companies shelve expansion plans or close projects entirely. Australian miners including BHP Billiton and Rio Tinto are expected to receive less revenue from their top-2 export items, iron ore and coal, once new annual contracts come into effect. Iron-ore is expected to sell for $52-$57 /ton starting April 1 st , representing a 30%-to-40% drop from 2008's level.

Steelmakers and electric power companies will pay 60% less for Aussie coking and thermal coal from April 1 st , the first reduction for annual contracts since 2003. In the coking coal market, Japan 's Nippon Steel, Mitsubishi Corp, the Japanese trading company, and Australian miner BHP Billiton agreed to a price of $128-$129 a ton. Last fiscal year, steel producers paid a record $300 /ton for coking coal, which is one of the two primary raw materials for steel alongside iron ore. In the thermal coal market, Xstrata , the Swiss mining group, and Chubu , the Japanese power company, agreed to a price of $70 /ton for the year starting in April, down 44% from this year's $125 a ton.

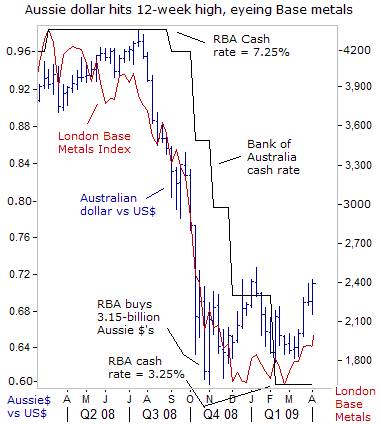

The sharp slide in coal and iron-ore was expressed by a precipitous fall of the Australian dollar. The commodity-based currency, the sixth-most-traded in the world, and widely regarded as a indicator of trends in global trade, fell to 60-US-cents in late October, a five-year low, and down from 98-US-cents in mid-July, a decline of nearly 40-percent. In a similar vein, the Australian stock market fell 55% below the November 2007 peak, wiping-out A$900-billion of value, a little less than Australia 's annual GDP.

The sharp slide in coal and iron-ore was expressed by a precipitous fall of the Australian dollar. The commodity-based currency, the sixth-most-traded in the world, and widely regarded as a indicator of trends in global trade, fell to 60-US-cents in late October, a five-year low, and down from 98-US-cents in mid-July, a decline of nearly 40-percent. In a similar vein, the Australian stock market fell 55% below the November 2007 peak, wiping-out A$900-billion of value, a little less than Australia 's annual GDP.

BHP-Billiton's decision to abandon its much-publicized bid for Rio Tinto, was seen as yet another indication that the “Commodity Super Cycle” had collapsed. Mining analysts were predicting that slumping commodity markets would result in the slashing of up to $A30 billion of Australia 's coal and iron ore exports. Australia 's central bank cut its benchmark interest rate 400-basis points since September to 3.25%, the lowest level in 45-years and the government announced it would spend A$42-billion, accounting for 2% of gross domestic product to ward-off a recession.

Yet today, the Australian dollar is rebounding to a 12-week high of 71.70-US-cents, as the speculative appetite for commodities and global stocks is revived, on optimism that China can pull Asia out of its slump, and the global credit crunch will ease, once FASB eases the mark-to-market rules for toxic mortgages, held by US-banks. G-20 central bankers are monetizing trillions of dollars worth of government debt, engaging in full-scale currency devaluations, and working feverishly to re-inflate commodity and asset markets.

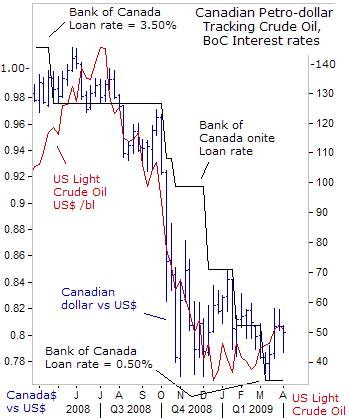

Contrarians haven't forgotten the hyper-inflation psychology that gripped the commodity markets just one year ago, when the US$ dollar Index was plunging to a 26-year low. The Canadian petro-dollar has lost nearly 20% of its value since last July, to around 80-US-cents today, tracking the historic slide in crude oil prices. The Loonie was also undercut by the Bank of Canada's rapid fire rate cuts, to a historic low of 0.50-percent.

Contrarians haven't forgotten the hyper-inflation psychology that gripped the commodity markets just one year ago, when the US$ dollar Index was plunging to a 26-year low. The Canadian petro-dollar has lost nearly 20% of its value since last July, to around 80-US-cents today, tracking the historic slide in crude oil prices. The Loonie was also undercut by the Bank of Canada's rapid fire rate cuts, to a historic low of 0.50-percent.

The OPEC cartel has slashed its oil output by 3.4-million barrels per day since August, with half the cuts initiated by Saudi Arabia , the central banker of oil, to defend the crude oil price at $40 per barrel. West Texas Sweet has rebounded to $53.50 /barrel today, invigorated by the surge in global stock markets, and the devaluation of the US-dollar. There are other key factors lurking in the background that can greatly impact oil prices in the year ahead, - highlighted in the April 3 rd edition of Global Money Trends.

Meanwhile, Bank of Canada chief Mark Carney signaled on April 1st , he's unlikely to cut the overnight loan rate below its current level of 0.50%, and won't engage in “Quantitative Easing” to combat the recession. He hinted the BoC could stimulate the economy by simply holding down rates at 0.50% for an extended period of time, without cutting further. “Duration matters. By keeping rates low for longer, additional stimulus can be provided,” he said. Compared to the central bankers of England , Japan , and the United States , the Bank of Canada chief looks like a hard-line hawk.

The upcoming April 3 rd edition of Global Money Trends will present its Q'2 prediction for the global stock markets, plus an analysis and forecast of the crude oil market, and expectations for foreign currencies versus the US-dollar, and much more.

This article is just the Tip-of-the-Iceberg of what's available in the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2009 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.