Bankrupt European Banks Sitting on $23 Trillion of Impaired Assets

Companies / Euro-Zone Mar 03, 2009 - 01:48 AM GMTBy: John_Mauldin

This week we look at the European bank markets through the eyes of my London partner Niels Jensen, head of Absolute Return Partners. I continue to believe that this is a brewing crisis which could have far more significant implications for the global economy than the Asian Crisis of 1998. In this week's Outside the Box, Niels has compiled a sobering set of data that suggests that only massive government involvement in Europe on a scale that is unprecedented will keep the wheels from coming off in Europe and the global economy.

This week we look at the European bank markets through the eyes of my London partner Niels Jensen, head of Absolute Return Partners. I continue to believe that this is a brewing crisis which could have far more significant implications for the global economy than the Asian Crisis of 1998. In this week's Outside the Box, Niels has compiled a sobering set of data that suggests that only massive government involvement in Europe on a scale that is unprecedented will keep the wheels from coming off in Europe and the global economy.

I have worked closely with Niels for years and have found him to be one of the more savvy observers of the markets I know. You can see more of his work at www.arpllp.com and contact them at info@arpllp.com.

John Mauldin, Editor, Outside the Box

Europe On the Ropes

The Absolute Return Letter March 2009

"Many of today's policy proposals start from the view that "greed" and "incompetence" and "poor risk assessment" are the ultimate source of what went wrong. In fact, they were not the true cause at all. Moreover, even if they had been, it is fatuous to think that we will now create a post-crash generation of bankers and traders who are not greedy, much less a new generation of quants who will be able to assess and manage risks much better than "the idiots" who have brought us to the current abyss. Greed cannot be exorcised. Nor can the inherent inability of any quants to determine the "true" probability distributions of all-important events whose true probabilities of occurrence can never be assessed in the first place." - Woody Brock, SED Profile, December 2008

Policy mistakes 'en masse'

The last few weeks have had a profound effect on my view of politicians (as if it wasn't already dented). All this talk about capping salaries for senior bank executives is quite frankly ridiculous. It is Neanderthal politics performed by populist leaders. That Gordon Brown has fallen for it is hardly surprising but I am disappointed to see that Barack Obama couldn't resist the temptation. The mob wants blood and our leaders are delivering in spades. The stark reality is that we are all guilty of the mess we are now in. For a while we were allowed to live out our dreams and who was there to stop us? Policy mistakes – very grave mistakes – permitted the situation to spin out of control. From the U.S. Federal Reserve Bank under the stewardship of Alan Greenspan being far too generous on interest rates to the British Chancellor of the Exchequer -who now happens to be our Prime Minister - advocating 'Regulation Light'.

Policing must improve

If you really want to prevent a banking crisis of this magnitude from ever happening again, the focus should be on the way banks operate and not on how much they pay their staff. And, within that context, any discussion must start and end with how much leverage should be permitted. The French have actually caught onto that, but their narrow-mindedness has driven them to focus on hedge funds' use of leverage which is only a tiny part of the problem. It is the gung ho strategy of banks which brought us down and which must be better policed. And guess what; if banks were better policed - and leverage restricted - then profits, even at the best of times, would be much smaller and there would be no need to regulate bankers' compensation packages.

It is pathetic to watch our prime minister attacking the bonus arrangements of our banks when the UK Treasury, on his watch, spent £27 million pounds on bonuses last year as reward for delivering a public spending deficit of 4.5% of GDP at the peak of the economic cycle. Even my old mother understands that governments must deliver budget surpluses in good times, allowing them more flexibility to stimulate when the economy hits the wall. What Gordon Brown has done to UK public finances in recent years is nothing short of criminal.

So, with that in mind, let's take a closer look at the European banking industry. The following is not pretty reading. I have rarely, if ever, felt this apprehensive about the outlook. So, if the crisis has made you depressed already, don't read any further. What is about to come, will make your heart sink.

More leverage in Europe

Let's begin our journey by pointing out a regulatory 'anomaly' which has allowed European banks to take on much more leverage than their American colleagues and which now makes them far more vulnerable. In Europe, unlike in the US, it is only risk-weighted assets which matter to the regulators, not the total leverage ratio. European banks can therefore apply a lot more leverage than their US counterparties, provided they load their balance sheets with higher rated assets, and that is precisely what they have been doing.

That is fine as long as you buy what it says on the tin. But AAA is not always AAA as we have learned over the past 18 months. Asset securitisations such as CLOs proved very popular amongst European banks, partly because they offered very attractive returns and partly because Standard & Poors and Moodys were kind enough to rate many of them AAA despite the questionable quality of the underlying assets.

Now, as long as the economy chugs along, everything is dandy and the AAA-rated assets turn out to be precisely that. But we are not in dandy territory. Many asset securitisation programmes are in horse manure to their necks, so don't be at all surprised if European banks have to swallow further losses once the full effect of the recession is felt across Europe. The two largest sources of asset securitisation programmes are corporate loans and credit cards. Senior secured loans are still marked at or close to par on many balance sheets despite the fact they trade around 70 in the markets. The credit card cycle is only beginning to turn now with significant losses expected later this year and in 2010-11.

Not much of a cushion left

Citibank has calculated that it would only take a cumulative increase in bad debts of 3.8% in 2009-10 to take the core equity tier 1 ratio of the European banking industry down to the bare minimum of 4.5%1. By comparison, bad debts rose by a cumulative 7% in Japan in 1997-98. One can only conclude that European banks are very poorly equipped to withstand a severe recession. Seeing the writing on the wall, they are left with no option but to shrink their balance sheets. Despite talking the talk, banks will use every trick at their disposal to reduce the loan book. No prize for guessing what that will do to economic activity.

The wheels are coming off

But that is not the whole story. It is not even the most worrying part of the story. For the true horror to emerge, we need to turn to Eastern Europe for a minute or two. Nowhere has the credit boom been more pronounced than in Eastern Europe. And nowhere is the pain felt more now that credit has all but dried up. One measure of the credit fuelled bonanza is the deterioration of the current account across the region. Credit Suisse has calculated that in four short years, from 2004 to 2008, Eastern Europe's current account went from +6% to -6% of GDP2. That is a frightening development and is likely to cause all sorts of problems over the next few years.

Meanwhile Western European banks, eager to milk the opportunities in the East after the iron curtain came down, have acquired many of the region's banks (see chart 1). Now, with many Eastern European countries in free fall, ownership could prove disastrous for an already weakened banking industry in the West.

The problem is widespread

To make matters worse, the problems in the East are beginning to look systemic. Credit Suisse has produced an interesting scorecard where they rank a number of countries around the world on factors usually taken into consideration when assessing the credit quality of sovereign debt (see chart 2). At the top of the tree (i.e. the worst credit score) you find Iceland – hardly surprising considering their current predicament. More importantly though, of the next 14 countries on the list, 8 are Eastern European – not what you want to hear if you are an already undercapitalised European bank with huge exposure to Eastern Europe.

Swedish banks are already reeling from their exposure to the Baltic countries. Austrian banks are in even worse shape, having been the most acquisitive of any European banks. Some Italian banks could be dragged under by their Eastern European exposure and even the conservative banking sector in Switzerland doesn't look like it can escape the mayhem.

Worst of all, the problems in the East are just about to unfold at a point in time where the European banking industry is bleeding heavily from massive losses already incurred in other areas. With no access to private funding, banks find it virtually impossible to re-build their capital base with anything but tax payers' money.

US banks are better off

US banks are in less of a pickle. Unlike the subprime debacle which hit both the US and the European banks hard, US banks have little exposure to Eastern Europe. To prove my point, according to the IMF, European banks have 75% as much exposure to US toxic debt as American banks, but 90% of all cross border loans to Eastern Europe originate from Western European banks. And, to add insult to injury, European banks have been much slower than US banks in terms of recognising their losses. Write-offs now total about $750 billion in the US and only about $325 billion in Europe.

The great mortgage show

The problems in Eastern Europe begin and end with their large external debts. In recent years, ordinary people all over the region have converted their traditional mortgages to EUR- or CHF-denominated mortgages. Some have even switched to JPY mortgages. Who can possibly resist 3% mortgages? Didn't anyone inform them of the risk? As currencies across the region have fallen out of bed in recent months, these mortgages have suddenly become 30-50% more expensive. No wonder the local economy is suddenly tanking.

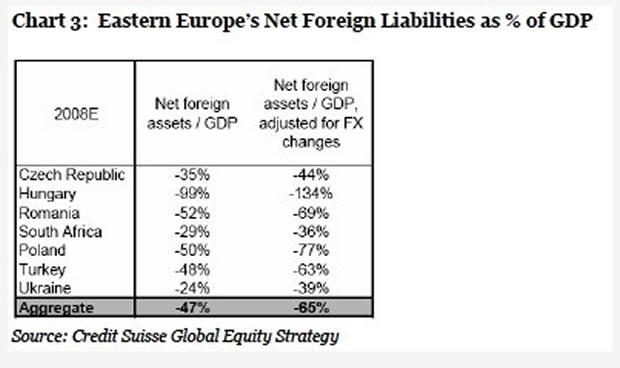

Credit Suisse has calculated that net foreign liabilities (as a % of GDP) have risen from 47% to 65% in recent months as a direct result of the loss of local currency values (see chart 3 – and don't ask me why Credit Suisse has included South Africa in Eastern Europe!).

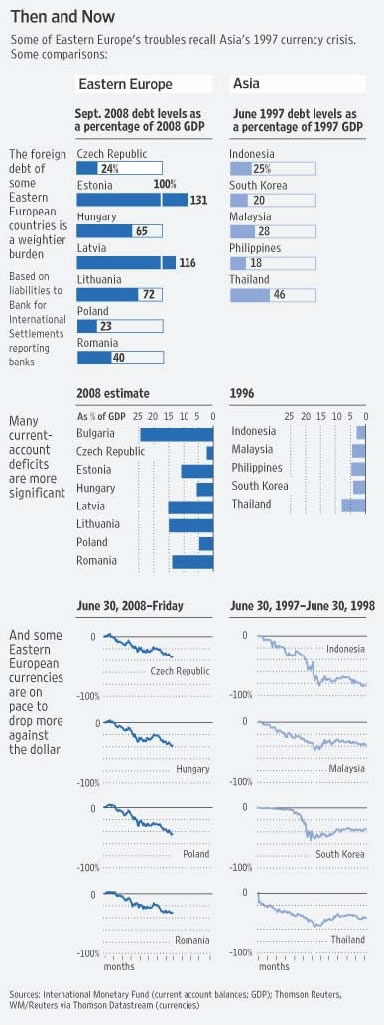

Chart 4: Eastern European vs. Asian Crisis

Source: Wall Street Journal

Back in 1997-98 Asia went through a similar currency crisis. However, as you can see from chart 4, Asian current account deficits were much smaller than Eastern European deficits are now. So were debt levels. Despite that, the Asian crisis did enormous damage to the local economy. Eventually Asia came good, primarily because the devalued currencies allowed the Asian countries to export more. Eastern Europe does not share this luxury. With over 90% of the world's GDP in recession, who are they going to export to anytime soon?

Austria is in greatest trouble

According to the latest estimates from BIS, Eastern European countries currently borrow $1,656 billion from abroad, three times more than in 2005 and mostly denominated in foreign currencies (ouch!). 90% of that can be traced to Western European banks. About $350 billion must be repaid or rolled over this year. Not an easy task in these markets. Austrian banks alone have lent about $300 billion to the region, equivalent to 68% of its GDP according to the Financial Times. A default rate of 10% on its Eastern European loans is considered enough to wipe out the entire Austrian banking system. EBRD has gone on record stating that defaults in Eastern Europe could end up as high as 20%3.

An extra $250bn to the IMF

Hungary, Latvia and Ukraine have already received emergency loans from the IMF and both Serbia and Romania are reportedly considering asking for help. Meanwhile the IMF's coffers are draining quickly and it has asked leading industrial nations for new funding. At their summit a week ago, EU leaders coughed up an extra $250 billion but nobody said where the money is going to come from. Even if they find the money, it is likely to prove hopelessly inadequate. Our leaders must grow up. Measuring everything in billions is so yesterday. Trillions are the new billions, like it or not.

Conspiracy or...?

On the 11th February the Daily Telegraph's Brussels correspondent Bruno Waterfield wrote an article under the header: "European banks may need £16.3 trillion bail out, EC document warns." In the article, the reporter revealed that he has seen a secret document produced by the EU Commission which briefed the union's finance ministers on the true extent of the banking crisis. Less than 24 hours later, the article's header was changed to "European bank bail-out could push EU into crisis" and two paragraphs had mysteriously disappeared. Here they are:

"European Commission officials have estimated that "impaired assets" may amount to 44pc of EU bank balance sheets. The Commission estimates that so-called financial instruments in the 'trading book' total £12.3 trillion (13.7 trillion euros), equivalent to about 33pc of EU bank balance sheets.

In addition, so-called 'available for sale instruments' worth £4trillion (4.5 trillion euros), or 11pc of balance sheets, are also added by the Commission to arrive at the headline figure of £16.3 trillion."

Do yourself a favour - read those two paragraphs again. Newspaper editors do not change content light-heartedly. Did the Telegraph editor receive a call from Downing Street? Or Brussels? Did he have second thoughts about the avalanche that he could possibly instigate? I don't know and I probably never will. But one thing is certain. If the EU Commission's estimate of £16.3 trillion of impaired assets is correct, then the crisis is far worse than any of us could ever imagine. Not only would we have to get used to the prospects of a systemic meltdown of our banking system, but entire nations may go down as well.

Public debt to rise and rise

Even if actual losses prove to be much, much smaller (and I sincerely hope so), the banking sector cannot, in the current environment at least, raise sufficient capital to stay afloat, so more, possibly a lot more, tax payers' money will have to be put forward. This can only mean one thing. Public debt will rise and rise. The official estimate for the UK for next year is already approaching 10% of GDP, an estimate which will almost certainly rise further. We probably have to get used to running 10-15% deficits for a few years, a fact which seriously undermines the notion of government bonds being next to risk-free.

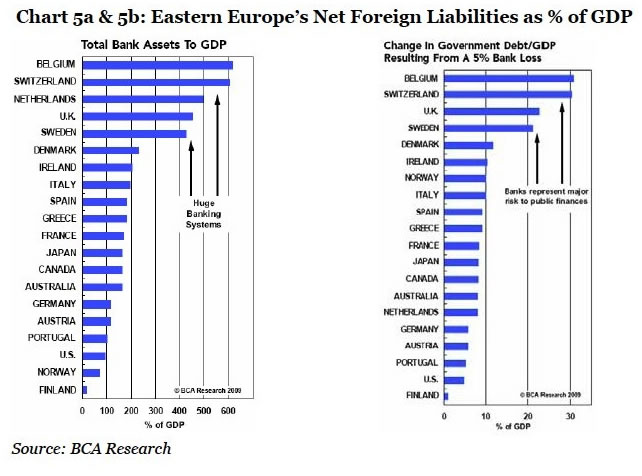

BCA Research has calculated the effect on public debt in a number of countries, as a result of further bank losses being underwritten by tax payers. Obviously, those countries with the largest banking industries (as a % of GDP) will be hit the hardest (see charts 5a and 5b).

For that very reason, and as pointed out in last month's Absolute Return Letter, there is a real risk that investors will demand much higher risk premiums on government debt. Only a few days ago, Ireland issued 3-year bonds at almost 250 basis points over corresponding Bunds. As more and more debt is transferred to sovereign balance sheets, we will likely see the spreads between good and bad paper rise further but we will also witness increasingly desperate measures being applied by the men in power. If they could prohibit short-selling of banks on the stock exchange (which didn't work), why wouldn't they consider prohibiting short-selling of government bonds? Not that it would necessarily work any better, but desperate people do desperate things.

Can Germany rescue us?

Most investors remain convinced that Germany will come to the rescue - in my opinion not as simple a solution as widely perceived given the enormity of the crisis. One possible solution which has been mentioned frequently in recent weeks is for all the eurozone nations to get together and start issuing joint bonds. This would undoubtedly help the weaker nations, but the idea was shot down by the German Finance Minister only a few days ago when he said that closer economic harmony across the eurozone would be needed before Germany would be prepared to entertain such an idea.

The most obvious trick left in the book, therefore, is to inflate us out of this mess. With the enormous amounts of public debt being created at the moment, years of deflation a la Japan would be catastrophic. You will never get a central banker to admit to it, but a healthy dose of inflation is probably our best prospect of surviving this crisis.

Given this outlook, do you really want to be long euros?

Niels C. Jensen

© 2002-2009 Absolute Return Partners LLP. All rights reserved.

--------------------------------------------------------------------------------

Footnotes:

1 Citibank, Credit Outlook 2009

2 Ex Russia. Source: Credit Suisse Global Equity Strategy

3 "Failure to save East Europe will lead to wordwide meltdown", Daily Telegraph

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.