Bernanke Burns More Tax Payer Billions in Banks Capital Assistance Program

Politics / Credit Crisis Bailouts Feb 26, 2009 - 03:45 AM GMTBy: Mike_Shedlock

Bernanke has fired yet another misguided missile to stabilize the banking system. His new program is called the Capital Assistance Program and supposedly it will restore confidence in banks and get them to lend. Here is a description of the program:

Bernanke has fired yet another misguided missile to stabilize the banking system. His new program is called the Capital Assistance Program and supposedly it will restore confidence in banks and get them to lend. Here is a description of the program:

The purpose of the CAP is to restore confidence throughout the financial system that the nation's largest banking institutions have a sufficient capital cushion against larger than expected future losses, should they occur due to a more severe economic environment, and to support lending to creditworthy borrowers.

Terms

- Capital provided under the CAP will be in the form of a preferred security that is convertible into common equity at a 10 percent discount to the price prevailing prior to February 9th.

- CAP securities will carry a 9 percent dividend yield and would be convertible at the issuer's option (subject to the approval of their regulator).

- After 7 years, the security would automatically convert into common equity if not redeemed or converted before that date.

- The instrument is designed to give banks the incentive to replace USG-provided capital with private capital or to redeem the USG capital when conditions permit.

- With supervisory approval, banks will be able to request capital under the CAP in addition to their existing CPP preferred stock.

- With supervisory approval, banks will also be allowed to apply to exchange the existing CPP preferred stock for the new CAP instrument.

CAP Facts

1) Amazingly CAP fact sheet states the securities will yield a 9% dividend. However, any bank troubled enough to need the CAP is likewise too troubled to be able to pay a 9% dividend. Banks can't get a 9% return on borrowed money everyone knows it. Instead, expect preferred shares to be converted to common at inflated prices.

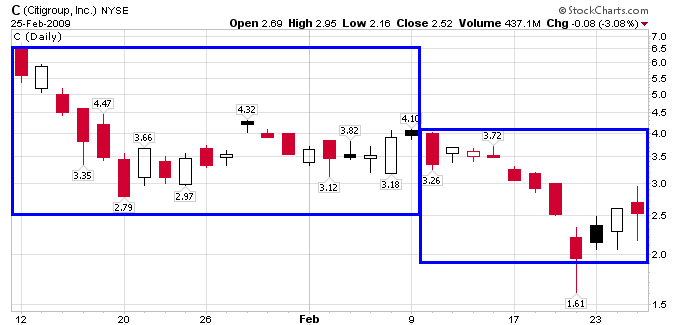

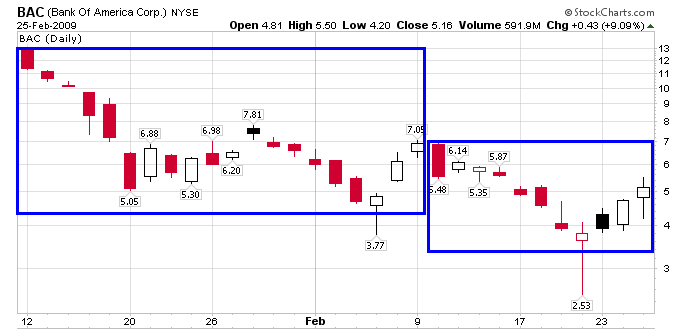

2) Digging a bit deeper into the fact sheet we see the " Conversion price is 90% of the average closing price for the common stock for the 20 trading day period ending February 9, 2009. "

Think February 9 was selected at random? Think again. The first box in the charts below is the 20 days ending February 9. Compare to what has happened since.

Citigroup Chart For February

Bank of America Chart For February

Bernanake Reassures Investors

The CAP plan White Paper goes on to say ...

"By reassuring investors, creditors, and counterparties of banking institutions--as well as the institutions themselves--that banks have capital in a sufficient amount and quality to withstand even a considerably weaker-than-expected economic environment, the CAP instrument should improve confidence and increase the willingness of banking institutions to lend."'

Those assurances amount to a promise to continually stick it to taxpayers, no matter what the cost.

Citi Near Deal to Boost U.S. Stake to as Much as 40%

The Wall Street Journal is reporting Citi Near Deal to Boost U.S. Stake to as Much as 40% .

Citigroup Inc. may announce a deal with the U.S. as soon as tomorrow that could raise the government's stake to as much as 40 percent, the Wall Street Journal reported, citing unidentified people familiar with the matter.

The deal may cause Citigroup to sell part of the company's stake in Grupo Financiero Banamex, the Mexican bank, because Mexico prohibits companies with a more than 10 percent ownership by a foreign government from running a bank in Mexico, the newspaper said.

Based on the above, expect taxpayers to be forced into supporting Citigroup at substantially above market prices. Remember, taxpayers are on the hook for $300 billion in debt guarantees for which we got a lousy $7 billion in preferred shares. Those shares are about to be diluted further.

Bernanke Rejects ‘Anything Like' Bank Nationalization

It appears the nationalization train has run into a brick wall, perhaps because there was never any agreement as to what "nationalization" means. Let's tune into Bernanke Rejects ‘Anything Like' Bank Nationalization .

Federal Reserve Chairman Ben S. Bernanke said while the U.S. government may take “substantial” stakes in Citigroup Inc. and other banks, it doesn't plan a full- scale nationalization that wipes out stockholders.

Nationalization is when the government “seizes” a company, “zeroes out the shareholders and begins to manage and run the bank, and we don't plan anything like that,” Bernanke told lawmakers in Washington today.

In the case of Citigroup Inc., the government may end up with a “substantial” share of the lender's stock, he said. Oversight of the company would be accomplished through regulators and by exerting “shareholder rights,” Bernanke said.

The Treasury Department, Federal Reserve and other banking regulators said in a joint statement on Feb. 23 that they stood ready to pump more capital into banks, or convert some of the government's outstanding preferred shares into common, to prevent their failures. The stress tests are scheduled to begin today, according to that statement.

“We will see how their test works out, and we will see what evolves,” Bernanke said. “If in fact they have to convert even the existing preferred into common, then there could be a more substantial share of ownership of Citi by the U.S. government.”

Somehow taking a a “substantial” share in banks and injecting more money over time is nothing "like nationalization".

Mysterious Plans

Very seldom do I completely agree with Krugman. In fact, this is the first time that I can recall. Please consider Mysterious plans

I'm trying to be sympathetic to the various plans, or rumors of plans, for bank aid; but I keep not being able to understand either what the plans are, or why they're supposed to work. And I don't think it's me.

So the latest is that we're going to convert preferred stock held by the government to common stock, maybe.

Here's my stylized picture of the situation:

What Treasury now seems to be proposing is converting some of the green equity to blue equity — converting preferred to common. It's true that preferred stock has some debt-like qualities — there are required dividend payments, etc.. But does anyone think that the reason banks are crippled is that they are tied down by their obligations to preferred stockholders, as opposed to having too much plain vanilla debt?

I just don't get it. And my sinking feeling that the administration plan is to rearrange the deck chairs and hope the iceberg melts just keeps getting stronger.

Tangible Common Equity for Beginners

Inquiring minds are reading Tangible Common Equity for Beginners .

The initial government investments in Citigroup, back in October and November, were in the form of preferred shares. Between the two bailouts, the government put in $45 billion in cash and got $52 billion in preferred stock (the $7 billion difference was the fee for the guarantee on $300 billion of Citi assets). That preferred stock was designed to be much closer to debt than to equity: it pays a dividend (5% or 8%), it cannot be converted into common stock (so it cannot dilute the existing shareholders), it has no voting rights, and it carries a penalty if it isn't bought back within five years. In fact, it is hard to distinguish from debt, except perhaps for the fact that, if Citi defaults on it (cannot buy the shares back) we don't need to worry about systemic instability, because the government can absorb the loss. As preferred stock, these bailouts boosted Citi's Tier 1 capital, but not its TCE.

Because of the newly perceived need for TCE, the bailout plan under discussion is to convert some of the preferred stock into common stock. Citi wouldn't actually get any new cash from the government, but it would be relieved some of the dividend payments (currently close to $3 billion per year), and of the obligation to buy back the shares in five years.

The trick is deciding what price to convert the shares at. All of Citi's common shares today are worth around $12 billion, so if you converted $52 billion of preferred shares into common, the government would suddenly own over 80% of Citi. (In the conversion, you divide the value of the preferred stock you are converting by the price of the common stock, and that yields the number of common shares the government now owns.)

The Geithner team is still continuing the Paulson policy of avoiding anything that looks like nationalization, so the talk is that the government ownership will be capped at 40%; that means the government could only convert about $8 billion of its preferred stock. There will probably be some clever manipulation of the numbers to say that the preferred stock is actually worth less than $52 billion, or that it should be converted at a higher price than the current market price of the stock.

(This seems like a blatant subsidy to me, since new investors buying large blocks of stock in a public company typically pay less than the current market price.) There is also talk of trying to get some of Citi's other preferred stock holders to convert as well, because the more they convert, the more common shares, and hence the more the government can have without going over the 40% limit.

The Amazing, Shape-Shifting Convertible Preferred

Minyan Peter has an interesting take in The Amazing, Shape-Shifting Convertible Preferred .

I have been asked whether there was anything in Chairman Bernanke's speech yesterday that changed my outlook on the prospects of nationalization for some of our largest financial institutions. In a word: “No.”

Knowing that there are teams of professionals on Wall Street dedicated to giving new hybrid securities cute names, let me suggest that the government henceforth refer to these incremental investments as “Maybetorily” Convertible Preferreds - as in, maybe they're straight preferred stock, maybe they're common stock, maybe they're gone altogether - it all depends on how bad the economy gets from here.

How these Maybetorily Convertible securities can in any way provide the impetus for further private-sector investment into the common stock of our banking system confounds me. As I see it, if implemented, existing common shareholders have at best the same upside they previously had, with exponentially larger downside.

So rather than throwing the frogs (banks) into nationalizing boiling water immediately, the government is going to place them in a tepid bath and watch, suggesting, at least this week, that while they may have to turn up the temperature a little bit (“temporarily”), no one will ultimately get burned.

Maybe, maybe not.

I'm sticking with my version of the story: The Fed Is Clueless and Banks are Zombified .

The only reason banks are not on an "out-of-control course to nationalization" is Bernanke is on an "out-of-control" mission to rescue banks regardless of what it costs taxpayers. The Fed clearly has no idea what it is doing and is making things up along the way.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2009 Mike Shedlock, All Rights Reserved

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.