Stock Market Breadth Study Shows Positive Developments and Gold

Stock-Markets / Investing 2009 Feb 10, 2009 - 07:34 AM GMTBy: Chris_Ciovacco

As outlined in an October 20, 2008 article Stocks Will Bottom Well Before Economy , we should not expect the stock market to wait for the "all clear" signal from an economic perspective before finding a bear market bottom. There is no doubt the economic news will get worse before it gets better. If we expect the technicals or charts to show improvement before the economy gets better, it makes sense to keep an eye on recent technical developments.

As outlined in an October 20, 2008 article Stocks Will Bottom Well Before Economy , we should not expect the stock market to wait for the "all clear" signal from an economic perspective before finding a bear market bottom. There is no doubt the economic news will get worse before it gets better. If we expect the technicals or charts to show improvement before the economy gets better, it makes sense to keep an eye on recent technical developments.

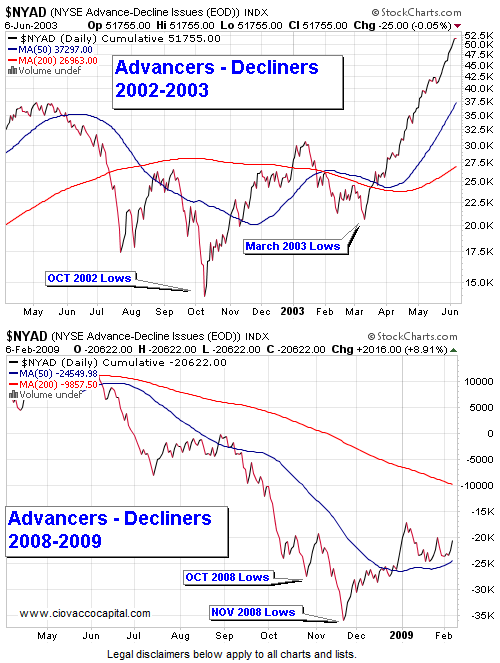

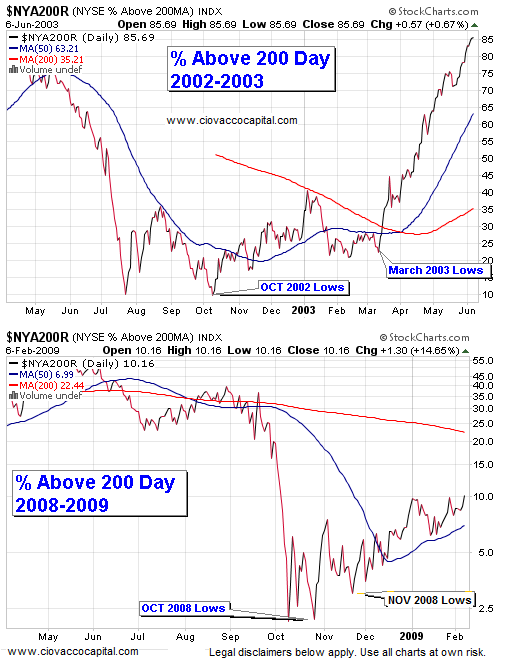

A study of stock market breadth since the November 2008 lows compares very favorably with the 2002-2003 bear market bottom. This means we have some observable evidence supporting the possibility of better days ahead for the stock market. Since only seventy-eight calendar days have elapsed since the November 2008 low, these results give us an early read on the strength of the current advance – an early read that could prove to be inaccurate. However, the results do remind us that it pays to keep an open mind and be prepared for all outcomes, including a sustained advance off the November 2008 lows. The study compares the first seventy-eight calendar days after the October 2002 bear market low to the last seventy-eight calendar days (2008-2009).

< the on trade that stocks all including by issue this address indicators Breadth stock. typical a with happening is what of picture true paint not may Dow result, As stocks. to compared when scope in ?narrow? are 500 S&P and as such indexes means which NYSE, trading 2,500 over There five-hundred based The thirty only Dow) (a.k.a Average Industrial Jones decline. or rally given participating percentage refers breadth Market .>

When the market makes gains with a high percentage of stocks participating in the move, it is bullish. Conversely, when the market indexes move higher with a lower percentage of stocks participating in the rally, it can often be a sign of impending weakness for the entire market. After a market bottom of significance, we would like to see broad and sustained participation in the subsequent rally. Market breadth helps us better understand how many stocks are participating in a given move up or down.

We studied observable evidence in market breadth indicators since the market low of November 20, 2008. Our results are not based on opinions or biases towards bullish or bearish outcomes. The breadth indicators studied were as follows:

- NYSE New Highs – New Lows

- NYSE Advancing Stocks – Declining Stocks

- NYSE Volume on Advancing Stocks – Volume on Declining Stocks

- NYSE Percent of Stocks Above Their 200-Day Moving Average

- NYSE Number of New 52-Week Highs

We examined when evidence of a possible trend change occurred in the breadth indicators above before and after the 2002 bear market bottom. We found when the following (see below) occurred for each breadth indicator relative to the day the market low was made in 2002 and when the bull market began in earnest in March of 2003.

Observable Changes In Market Breath Indicators:

- 50-Day Moving Average Became Flat – First Occurrence.

- 50-Day Moving Average Turned Up – First Occurrence (slope of line)

- 50-Day Moving Average Turned Up - Second Occurrence

- Crossed 50-Moving Average - First Occurrence

- Crossed 50-Moving Average - Second Occurrence

- 200-Day Moving Average Became Flat – First Occurrence

- 200-Day Moving Average Turned Up – First Occurrence (slope of line)

- Crossed Its 200-Moving Average - First Occurrence

- Crossed Its 200-Moving Average - Second Occurrence

- First Significant Higher-High After Lowest Low

- Second Significant Higher-High After Lowest Low

We compared the number of calendar days it took for the changes above to occur for each of the breath indicators after the October 2002 low. We then looked for the same evidence of possible trend changes in all the indicators before and after the November 2008 lows. Given the number of calendar days since the November 2008 low on the S&P 500, we would expect to have already seen twenty-one positive occurrences of a possible trend change as of the market's close on Friday, February 6, 2009. We are assuming the moves off the 2002 and 2008 lows occur in a similar manner. Of the twenty-one expected positive occurrences off the November 2008 lows, eighteen have in fact occurred. Therefore, we have seen 86% percent of the expected changes in the breadth indicators if the November 2008 lows followed a similar path to the 2002 lows. Based on observable evidence in these indicators, we have facts to support the possibility of the November 2008 lows being a significant bottom.

It is important to note, we are not making these statements based on how the market acted simply near the November 2008 lows. The evidence occurred over many months on the following dates (some on the same day):

- August 27, 2008

- September 17, 2008

- September 19, 2008

- September 24, 2008

- October 28, 2008

- December 8, 2008

- December 12, 2008

- December 16, 2008

- December 26, 2008

- December 30, 2008

- January 2, 2009

- January 5, 2009

- January 21, 2009

- January 23, 2009

- February 5, 2009

These positive pieces of evidence, which occurred over the last five months, point to a possible change in trend for U.S. stocks. The lowest low of the 2000-2002 bear market was made in October 2002. However, the stock market remained volatile and did not settle into a new bull market until March of 2003. Using the number of calendar days between the October 2002 low and the March 2003 "safe to get back in" date, we can estimate when the final low for this bear market should have occurred and when the “safe to get back in” date may occur. Based on the dates of occurrences in 2008 and 2009 listed above, if we followed a similar path off the bottom as in 2002, we would have expected the final low to have occurred near October 20, 2008. We would expect the "safe to get back in date" to occur somewhere near March 21, 2009. The stock market did make significant lows on October 27, 2008 and on November 20, 2008.

The positive evidence of a possible change in trend for stocks does not mean we are proclaiming November 20, 2008 will mark the lowest low for this bear market. Nor does it mean we will abandon our entry and stop-loss disciplines to manage risk. However, the results do help us better understand the possibility of better days ahead for investors. If we have observed 86% of the positive changes we would expect to have seen to date, it also means we have not seen 14% of them. The long-term trends for the U.S. stock market remain down. As this study demonstrates we have evidence of a possible trend change. "Possible" is quite different from "definite" .

Study Results Say "So Far So Good"

There are twenty-seven remaining positive technical signs to look for using these breadth indicators. If a bottom occurred on November 20, 2008, we would anticipate seeing these remaining positive signs surfacing in the coming weeks and months. We have not seen them yet , but this is to be expected since making a market bottom is more a process than a one day event. We need to see more to feel confident the November 2008 lows will hold. The study results tell us "so far so good", not , "we have all the evidence needed to declare a bottom is in place." Lower lows and an extended bear market remain quite possible give the severity of the credit crisis.

Our Investment Screening Models Also Show Some Positive Signs

In an effort to be prepared for the possible onset of a market with a better risk-reward profile, we have been maintaining a watch list of over 300 ETFs, stocks, bonds, and mutual funds. With several positive factors slowly beginning to surface in recent days, this weekend we updated our head-to-head ranking for all 300-plus investment options. Some encouraging signs from the latest results:

- Of the top 100 investments in the CCM rankings, 18% of them have passed a point which supports a possible positive change in trend.

- Of the top 100 investments in the CCM rankings, 68% of them are at least within 5% of a point which supports a possible positive change in trend.

- Of the top 100 investments in the CCM rankings, 65% of them are above their 200-day moving average, which is sometimes used as a basic definition of an uptrend.

- Of the top 100 investments, 48% have their 50-day moving average above their 200-day moving average, which also points toward the possibility of a more permanent change in trend.

Common Sense Accounting Says Many Banks Have Solvency Issues

Two administrations (Bush and Obama) have attempted to craft a plan to buy bad assets from banks in an effort to spur lending and restore confidence. The idea sounds good on paper. The recurring problem is determining how much to pay for the bad assets. Overpay and the taxpayers are left holding the bag. Pay what the market is willing to bear or "fair market value" and the banks will have to take a loss. If the taxpayers or private parties pay what the market will bear it creates "accounting problems for the banks". "Accounting problems" is the politically correct way of saying "solvency problems" for many banks. If a buyer pays what the market will bear for the securities, then it will become clear many banks are indeed insolvent. If that were not the case, then the government would have started buying bad assets a long time ago. The banks now want to change fair market value accounting rules in an effort to hide their insolvency from the public. Changing accounting rules will put us in the express lane to the Japanese “lost decade” scenario. Changing accounting rules will give us banks that appear solvent on paper, but will be insolvent in reality. The value of any asset (a car, a home, or a mortgage-backed security) is what the market is willing to pay for it at any given time. If we assign any other value to any asset then we are fooling ourselves. If these securities are worth so much more than "fair value" then why is no one willing to pay that for them?

Gold Still Has Some Hurdles To Cross

Gold is somewhat of a unique investment in that it can perform well in both during periods of price inflation and deflation. It has appeal as an alternative store of wealth to paper currencies. The supply of paper currencies can be rapidly expanded via the government's electronic printing press. Gold also serves as a safe haven in times of crisis. Deleveraging across the entire economy has contributed to gold's lower lows and lower highs since March 2008 (a downtrend).

Technical Cons: Referring to the labels on chart above: (1) Gold experienced a negative “death cross” in September 2008, (2) the slope of the 200-day moving average turned negative in October 2008, and (3) the downtrend from the March 2008 highs (see thick blue line) has not yet been clearly broken. These are all reasons we have remained patient despite the fundamental reasons to own gold.

Technical Pros: (a) Several higher-highs since the November 2008 lows, (b) price is above the 200-day moving average, and (c) slope of 200-day moving average is trying to make a turn for the better.

What we would we like to see? (a) A close above $906.50 (this has already happened – another positive), (b) an intraday high above $936.30 (not yet), (c) a clean break of the thick downtrend line from the March 2008 highs (close, but we still could fail and reverse course), (d) a reversal of the “death cross” where the 50-day moving average (thin blue line) rises back above the 200-day moving average(thin red line) - not yet, but close.

Why such a focus on the charts? We are looking for fundamental and technical alignment. We know there are numerous fundamental reasons to own gold. We just need the charts to help us with finding entry points with improved risk-reward ratios. Gold has made similar moves back to the trendline in July 2008 and October 2008. In both cases, significant declines followed the rally. This time we have impressively stayed around the trendline. We have also been able to hold the $906.50 level. Last time gold made a run like this, it fell from $936.30 to $679.90 - a loss of 27.3%. While the recent move is very encouraging, it pays to remain patient for a while longer. If gold is getting ready to make another leg higher, then everything we want to see happen will happen in short order. If gold can't break the downtrend, some of them will not happen and we will remain patient. Gold has not made a new high since March of 2000 – that may change in the coming weeks and months. We'll just have to pay attention and take action if needed. We do not care too much about gold's move from $900 to $940, but we do care about a move from $940 to $2,000.

When A New Bull Market Starts, There Will Be Plenty Of Time To Profit

With a close of 868 on February 6, 2008, the S&P 500 would still need to gain 81% just to get back to the October 2007 bull market high of 1,576. The markets have a continued tug-of-war going on between economic weakness and unprecedented government liquidity injections and stimulus programs. As we have done in this analysis, it is best to keep an eye on observable conditions and adjust your portfolio appropriately as conditions change. We are exploring the correlations between our top-rated investments and the S&P 500 Index. Our confidence in taking a position would be greater the lower the correlation to the general stock market.

By Chris Ciovacco

Ciovacco Capital Management

Copyright (C) 2009 Ciovacco Capital Management, LLC All Rights Reserved.

Chris Ciovacco is the Chief Investment Officer for Ciovacco Capital Management, LLC. More on the web at www.ciovaccocapital.com

Ciovacco Capital Management, LLC is an independent money management firm based in Atlanta, Georgia. As a registered investment advisor, CCM helps individual investors, large & small; achieve improved investment results via independent research and globally diversified investment portfolios. Since we are a fee-based firm, our only objective is to help you protect and grow your assets. Our long-term, theme-oriented, buy-and-hold approach allows for portfolio rebalancing from time to time to adjust to new opportunities or changing market conditions. When looking at money managers in Atlanta, take a hard look at CCM.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors and tax advisors before making any investment decisions. Opinions expressed in these reports may change without prior notice. This memorandum is based on information available to the public. No representation is made that it is accurate or complete. This memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned. The investments discussed or recommended in this report may be unsuitable for investors depending on their specific investment objectives and financial position. Past performance is not necessarily a guide to future performance. The price or value of the investments to which this report relates, either directly or indirectly, may fall or rise against the interest of investors. All prices and yields contained in this report are subject to change without notice. This information is based on hypothetical assumptions and is intended for illustrative purposes only. THERE ARE NO WARRANTIES, EXPRESSED OR IMPLIED, AS TO ACCURACY, COMPLETENESS, OR RESULTS OBTAINED FROM ANY INFORMATION CONTAINED IN THIS ARTICLE. PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

Chris Ciovacco Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.