The Paradox of Savings and Spending Competing with Socialism 2009

Economics / Economic Stimulus Feb 01, 2009 - 01:36 PM GMT

“Words from the Wise” this week comes to you in a shortened format as pressure from my “day job” precludes me from doing my customary commentary. However, a full dose of excerpts from interesting news items and quotes from market commentators is provided. (For more discussion about economies and financial markets, also see my post “ Video-o-rama: Global economy - banked into submission “.)

“Words from the Wise” this week comes to you in a shortened format as pressure from my “day job” precludes me from doing my customary commentary. However, a full dose of excerpts from interesting news items and quotes from market commentators is provided. (For more discussion about economies and financial markets, also see my post “ Video-o-rama: Global economy - banked into submission “.)

Just a side note: As President Obama's economic stimulus package makes its way to the US Senate and the government crafts plans to create a “bad bank”, the Chinese celebrated the Lunar New Year to usher in the Year of the Ox. According to Jim Trippon ( China Stock Digest ), the Chinese believe good and bad follow each other closely.

After a year of financial meltdowns in 2008, it is comforting to learn that the Year of the Ox is a sign of prosperity and has been very rewarding in the history of China. Are we unnecessarily concerned about the economic slowdown in China, and will the country's vast foreign reserves come to the Western world's rescue? If only hope were an investment strategy!

Why does the cartoon below remind me of Margaret Thatcher's poignant observation: “The problem with socialism is that you eventually run out of other people's money”?

Bill King ( The King Report ) said: “The Paradox of Thrift (or saving) is a reductio ad absurdum by John Maynard Keynes that avers that if everyone saves, aggregate demand will decline, and this will imperil the economy. We'd like to contribute the ‘Paradox of Spending' to Econ 101. This maxim holds that if everyone spends, there are no savings; debt surges and the implosion of that debt collapses an economy.”

Next, a tag cloud of the text of all the articles I have read during the past week. This is a way of visualizing word frequencies at a glance. As the saying goes: A picture paints a thousand words …

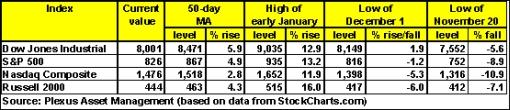

The US stock markets experienced their worst January in history, as seen from the movements of the major indices: Dow Jones Industrial Index -8.8%, S&P 500 Index -8.6%, Nasdaq Composite Index -6.4% and Russell 2000 Index -11.2%. This brings into question the January Barometer , stating “As January goes, so goes the year”.

Key resistance and support levels for the US indices are shown in the table below. The immediate upside target is the 50-day moving average, followed by the early-January highs. On the downside, the December 1 and all-important November 20 lows must hold in order to prevent considerable technical damage. As seen from the table, the Dow has already breached its January 2 low and closed the week only marginally above the roundophobia number of 8,000.

As far as the outlook for the stock market is concerned, I will suffice with a comment from Richard Russell ( Dow Theory Letters ): “The stock market often tries to confuse us by coming up with something new. Assuming that the Averages do better than their preceding January peaks, it would have occurred without the usual heavy buying on rising volume. It may be that the January peaks will have to be bettered before the ‘real' volume comes in. … we will have to monitor the stock market action carefully, to make sure we are not being sucked in to a fake rally as was the case following the 1929 crash.”

Also make sure to read my recent posts “ Albert Edwards: Back in the bear camp ” and “ Jeremy Grantham - The bear buys stocks “.

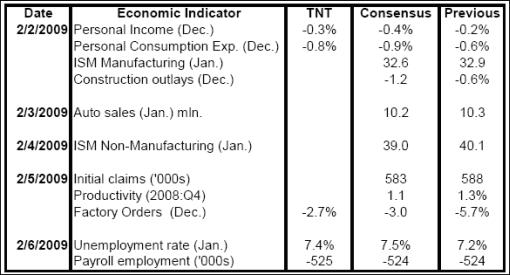

Week's economic reports

Click here for the week's economy in pictures, courtesy of Jake of EconomPic Data .

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Jan 26 | 10:00 AM | Existing Home Sales | Dec | 4.74M | 4.40M | 4.40M | 4.45M |

| Jan 26 | 10:00 AM | Leading Indicators | Dec | 0.3% | -0.5% | -0.3% | -0.4% |

| Jan 27 | 9:00 AM | S&P/CaseShiller Composite | Nov | -18.18% | NA | -18.4% | -18.06% |

| Jan 27 | 10:00 AM | Consumer Confidence | Jan | 37.7 | 39.0 | 39.0 | 38.6 |

| Jan 28 | 2:15 PM | FOMC Rate Decision | Jan. 28 | - | NA | NA | 0-0.25 |

| Jan 29 | 8:30 AM | Durable Orders | Dec | -2.6% | -2.2% | -2.0% | -3.7% |

| Jan 29 | 8:30 AM | Durable Orders , Ex-Tran | Dec | -3.6% | NA | -2.7% | -1.7% |

| Jan 29 | 8:30 AM | Initial Claims | 01/24 | 588K | 580K | 575K | 585K |

| Jan 29 | 10:00 AM | New Home Sales | Dec | 331K | 400K | 397K | 388K |

| Jan 30 | 8:30 AM | Chain Deflator-Adv. | Q4 | - | 0.5% | 0.6% | 3.9% |

| Jan 30 | 8:30 AM | Employment Cost Index | Q4 | 0.5% | 0.7% | 0.7% | 0.7% |

| Jan 30 | 8:30 AM | GDP -Adv. | Q4 | -3.8 | -5.5% | -5.5% | -0.5% |

| Jan 30 | 8:30 AM | Chain Deflator-Adv. | Q4 | -0.1 | 0.5% | 0.4% | 3.9% |

| Jan 30 | 9:45 AM | Chicago PMI | Jan | 33.3 | 33.5 | 34.9 | 35.1 |

| Jan 30 | 10:00 AM | Michigan Sentiment | Jan | 61.2 | 62.0 | 61.9 | 61.9 |

Source: Yahoo Finance , January 30, 2009.

In addition to interest rate announcements by the Bank of England and the European Central Bank (Thursday, February 5), the US economic highlights for the week include the following:

Source: Northern Trust .

Click here for a summary of Wachovia's weekly economic and financial commentary.

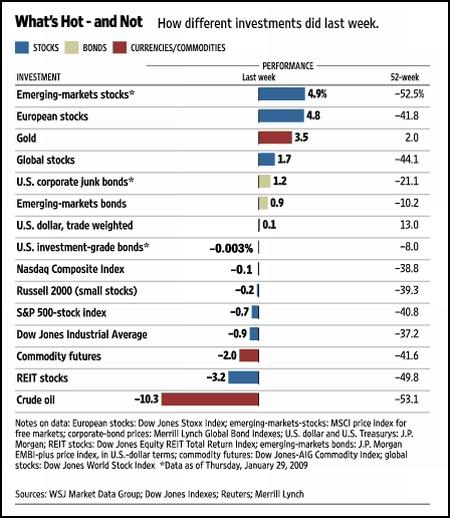

Markets

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , January 30, 2009.

Caution should be exercised, since the economic and earnings background remains precarious. And do remember Charles Darwin's words: “It is not the strongest of the species that survives, nor the most intelligent, but the one most responsive to change.”

That's the way it looks from Cape Town.

NBR: Warren Buffett one on one

SUSIE GHARIB, ANCHOR, NIGHTLY BUSINESS REPORT: Are we overly optimistic about what President Obama can do?

WARREN BUFFETT, CHAIRMAN, BERKSHIRE HATHAWAY: Well I think if you think that he can turn things around in a month or three months or six months and there's going to be some magical transformation since he took office on the 20th that can't happen and wouldn't happen. So you don't want to get into Superman-type expectations. On the other hand, I don't think there's anybody better than you could have had; have in the presidency than Barack Obama at this time. He understands economics. He's a very smart guy. He's a cool rational-type thinker. He will work with the right kind of people. So you've got the right person in the operating room, but it doesn't mean the patient is going to leave the hospital tomorrow.

SG: Mr. Buffett, I know that you're close to President Obama, what are you advising him?

WB: Well I'm not advising him really, but if I were I wouldn't be able to talk about it. I am available any time. But he's got all kinds of talent right back there with him in Washington. Plus he's a talent himself so if I never contributed anything for him, fine.

SG: But I know that during the election that you were one of his economic advisors, what were you telling him?

WB: I was telling him business was going to be awful during the election period and that we were coming up in November to a terrible economic scene which would be even worse probably when he got inaugurated. So far I've been either lucky or right on that. But he's got the right ideas. He believes in the same things I believe in. America's best days are ahead and that we've got a great economic machine, its sputtering now. And he believes there could be a more equitable job done in distributing the rewards of this great machine. But he doesn't need my advice on anything.

Click here for the full article.

Source: Susie Gharib, NBR , January 22, 2009.

CNN Money: House passes $819 billion stimulus bill

“The House on Wednesday evening passed an $819 billion economic stimulus package on a party-line vote, despite President Obama's efforts to achieve bipartisan support for the bill.

“The final vote was 244 to 188. No Republicans voted for the bill, while 11 Democrats voted against it.

“The Senate is likely to take up the bill next week.

“‘I hope that we can continue to strengthen this plan before it gets to my desk,' Obama said in a statement after the vote. ‘We must move swiftly and boldly to put Americans back to work, and that is exactly what this plan begins to do.'

“‘One week and one day ago, our new President delivered a great inaugural address … which I believe is a great blueprint for the future,' said House Speaker Nancy Pelosi. ‘With swift and bold action today, we are doing just that - with this vote today, we are taking America in a new direction.'

“Next week, the full Senate will vote on its version, which differs in some significant ways from the House bill. The two chambers will then need to reconcile their differences before each vote on the final version. To pass the package in the Senate, Democrats will need 60 votes - meaning at least two Republicans.

“Congress has put the legislation on a fast track, as many lawmakers on both sides of the aisle agree that swift action is needed to help pull the economy out of a deep recession. Both Democratic and Republican leaders have said they aim to get the bill to Obama's desk for him to sign before lawmakers' Presidents Day recess in mid-February.”

Source: David Goldman, CNN Money , January 28, 2009.

CEP News: US Government plans to set up “bad bank” to buy toxic assets

“The US government is crafting plans to create a “bad bank” to purchase toxic assets from financial institutions and strengthen the balance sheets of financial institutions, according to a report from CNBC on Tuesday evening.

“The concept of a ‘bad bank' is one which has been floated around by many countries across the globe as a means to add further stimulus to financial institutions and speed up market recovery. Nevertheless, the details of the plan have not been released.

“At the very least, CNBC quoted an unnamed Treasury official as saying that the government was planning a ‘major' announcement next week.

“In the aftermath of the announcement, Bloomberg News cited ‘sources familiar with the matter' that the Federal Deposit Insurance Corporation (FDIC) would be the likely candidate to run such an institution, arguing that Chairperson Sheila Bair has proposed issuing FDIC-backed debt to finance the project.

“Also on Tuesday, US Senator Chris Dodd, an active member in the crafting of recent financial legislation in the United States, said the creation of a ‘bad bank' sounded like a good idea and confirmed that he is aware that the Obama administration is looking into such a matter.”

Source: CEP News , January 28, 2009.

CNBC: Plan for banks' toxic debt may be unveiled next week

Click here for the article.

Source: CNBC , January 27, 2009.

Yahoo Finance: Good bank, bad bank or banana

“While the idea of the government becoming the de facto bad bank in a system-wide good bank-bad bank solution has some merit, there's a big problem with the ‘aggregator bank' idea that's gaining momentum in Washington DC, says Lawrence J. White Professor of Economics at New York University's Stern School of Business.

“‘Whether you call it a bad bank an aggregator bank or a banana doesn't change the basic problem: You've got to figure out what price is going to get paid for the assets that leave the financial system and end up in this government entity,' White says. ‘That's the hard part.'”

Click here for the article.

Source: Yahoo Finance , January 27, 2009.

CNBC: Barry Ritholtz - suggestions on how to restructure banks

“1. Stop interfering with the markets! : Nationalizing banks isn't market interference, keeping these mortally wounded banks alive is! Stop pussyfooting around and admit the truth. The market knows it, investors know it.

Let the FDIC do its job. That is:

2. Temporarily nationalize the banks : We know they are insolvent, and cannot survive without taxpayer money. Spending 150% of their market cap for an 8% share is absurd.

Wipe out the debt, liquidate bad common holders, fire the board and management, appoint new competent, risk sensitive management. They have six months to spin out a 10% stake in each of their holdings, followed by the rest within 5 years (10 at most).

3. Taxpayer owned : Once nationalized, that 10% spin out of the component parts would be in the form of preferred to taxpayers! For BAC, you would spin out Bank of America, Merrill Lynch, Countrywide, plus the ‘B/A Toxic Holdings I & II'. For Citi, it would be Travelers, Citi, Smith Barney, ‘Citi Toxic Holdings I & II', etc.

4. Now r ecapitalize: With the toxic waste off of the books, you can easily recapitalize the banks. Give the old creditors a ‘sweetheart' deal - they get a 10% stake also, but only if they buy a matching amount in the new bank.

5. Align compensation with long-term profitability : Stop rewarding traders for short term gains despite long term losses. Stop paying taxpayer monies out as dividends. Bonuses must be a function of the long term health of the company - not monthly volatility.”

Sources: CNBC and The Big Picture , January 29, 2009.

David Fuller (Fullermoney): What to do with bad assets

“The question of what to do about the bad assets on bank balance sheets has been circulating for some time. No one has yet come up with a sound method of valuing these assets and until they do, the uncertainty surrounding the situation will remain acute.

“US Aggregate Reserves for Depository Institutions in Excess of Required Reserves continue to climb to levels massively in excess of what is needed. Banks are doing everything they can to shore up their balance sheets because they do not know how they will be called upon to meet their outstanding obligations. The inability to value their assets is at the root of this problem.

“The de facto guarantees that have been put behind the major players in the banking system have helped to bring the TED spread down to much more reasonable levels. However, the difference between AA Bank spreads and BBB Bank spreads imply that investors continue to bet that high numbers of lower rated banks will default at some stage. This would seem to be common sense. A less leveraged, slimmed down banking sector will have less members and those either ‘too big to fail' or with the healthiest balance sheets are most likely to survive.

“Personally, I am in favour of a form of the ‘bad bank' solution. However, I see recapitalisation and the valuing of suspect assets as separate issues. If a ‘bad bank' takes possession of illiquid, hard-to-value assets, it should do so at prices well below what banks would deem as breakeven. This is the only fair way to make sure that the taxpayer is not paying up for duff assets. Recapitalisation should subsequently be considered only where any opacity in a firm's balance sheet has been cleared out; so that taxpayers know exactly what they are putting their money into.

“We know that a large number of hard-to-value assets have deep intrinsic value, which is not readily available to assess in today's conditions. Price discovery will only become apparent when an active secondary market for such assets is created. The ‘bad bank' will be key to creating and managing such a pool of liquidity. If the value of the bad assets turns out to be more than a bank received in bailout funds, they would have a justifiable cause to seek redress but that would be an issue for the courts subsequent to the financial crisis and not for now.”

Source: David Fuller, Fullermoney , January 29, 2009.

The New York Times: Sweden's fix for banks - nationalize them

“The Swedes have a simple message to the Americans: Bite the bullet and nationalize.

“With Sweden's banks effectively bankrupt in the early 1990s, a center-right government pulled off a rapid recovery that led to taxpayers making money in the long run.

“Former government officials in Sweden, many of whom come from the market-oriented end of the political spectrum, say the only way to solve the crisis in the United States is for the government to be prepared to temporarily take full ownership of the banks.

“Sweden placed its banks with troubled assets into a so-called bad bank, where they could be held and then sold over time when market and economic conditions improved. In the meantime, it used taxpayer money to provide enough capital to allow banks to resume normal lending.

“In the process, Sweden wiped out existing shareholders.”

Source: Carter Dougherty, The New York Times , January 22, 2009.

Bloomberg: Fannie to tap US for as much as $16 billion in aid

“Fannie Mae, the largest source of home-loan money in the US, said it will need to tap as much as $16 billion in emergency funds from the US Treasury Department to stay afloat as deterioration in the housing market persists.

“Fannie's planned request, announced today, follows Freddie Mac, which said on January 23 that it will need as much as $35 billion more in federal aid. Unprecedented mortgage losses drove the net worth of both companies below zero last quarter, they said in separate securities filings.

“This will be Washington-based Fannie's first draw on a $200 billion emergency fund set up by Treasury in September to keep the government-sponsored enterprises solvent. Fannie said losses on mortgage loans and a decline in the market value of its assets accounted for the shortfall in the fourth quarter.

“Fannie's Treasury request was “much worse” than expected, said Rajiv Setia, a fixed-income strategist at Barclays Capital in New York. Setia estimates taxpayers will have to shell out at least $50 billion for Fannie and $70 billion for Freddie this year. One or both, especially Freddie, may exceed the Treasury's backstop this year, he said.”

Source: Dawn Kopecki, Bloomberg , January 26, 2009.

Daily Mail: Revealed - day the banks were just three hours from collapse

“Britain was just three hours away from going bust last year after a secret run on the banks, one of Gordon Brown's Ministers has revealed.

“City Minister Paul Myners disclosed that on Friday, October 10, the country was ‘very close' to a complete banking collapse after ‘major depositors' attempted to withdraw their money en masse.

“The Mail on Sunday has been told that the Treasury was preparing for the banks to shut their doors to all customers, terminate electronic transfers and even block hole-in-the-wall cash withdrawals. Only frantic behind-the-scenes efforts averted financial meltdown.”

Source: Glen Owen, Daily Mail , January 24, 2009.

CEP News: IMF slashes global growth forecasts

“On the back of a $2.2 trillion loss on toxic US assets worldwide, the global economy is expected to contract in 2009 before recovering the following year, according to a report from the International Monetary Fund (IMF) on Wednesday.

“‘Unless stronger financial stains and uncertainties are forcefully addressed, the pernicious feedback loop between real activity and financial markets will intensify, leading to even more toxic effects on global growth,' read the report, which urged governments to continue taking action to rescue the financial system.

“‘We now expect the global economy to come to a virtual halt,' said IMF chief economist Olivier Blanchard at a press conference.

“As a consequence, the global economy is expected to grow 0.5% in 2009 rather than by 2.2% as previously estimated, and expand by 3.0% in 2010.

“To address the situation, the IMF report voiced support for the so-called ‘bad bank' approach where governments could set up a financial institution to purchase toxic assets, removing them from the balance sheets of banks.

“‘We think that more decisive action is needed now by both policy-makers and market participants, and with greater emphasis on balance sheet cleansing,' said Jaime Caruana, financial counsellor of the IMF.”

Source: CEP News , January 28, 2009.

Bloomberg: Gloom deepens among world's chief executives

“Gloom is deepening among business leaders, casting a pall over this year's World Economic Forum in Davos, Switzerland.

“Just one in five of 1,124 chief executives in 50 nations said they were very confident about prospects for revenue growth in 2009, down from half last year, and more than a quarter said they were pessimistic, a survey by PricewaterhouseCoopers showed. The sentiment was the worst since the accounting and consulting firm began tracking the CEO outlook in 2003.

“‘The speed and intensity of the recession has rocked the psyches of CEOs and created a global crisis of confidence,” Samuel DiPiazza, PWC's New York-based CEO, said in a statement.

“Such concerns are virulent as executives from JPMorgan Chase's Jamie Dimon to Stephen Green of HSBC Holdings join more than 2,500 counterparts, academics and policy makers in the ski resort for five days of soul-searching and deal-making. They meet as the world economy hurtles deeper into recession, banks add to more than a $1 trillion in writedowns and governments tighten their grip over the financial system.

“‘The outlook is pretty grim,' said Howard Davies, director of the London School of Economics and a former Bank of England policy maker who will be in Davos. ‘Things are not good and business surveys are coming out showing they're getting even worse.'”

Source: Matthew Benjamin and Simon Kennedy, Bloomberg , January 28, 2009.

The Wall Street Journal: YouTubing in Davos with Huffington and Forbes

“YouTube's Chad Hurley, Arianna Huffington and Steve Forbes share their views on Davos and the global economic crisis with WSJ's Andy Jordan.”

Source: The Wall Street Journal , January 28, 2009.

Bloomberg: Roubini - “nowhere to hide” from global slowdown

“‘There is nowhere to hide,' Nouriel Roubini, an economics professor at NYU's Stern School of Business who predicted the financial crisis, said from Zurich in an interview with Bloomberg Television. ‘We have for the first time in decades a global synchronized recession. Markets have become perfectly correlated and economies are also becoming perfectly correlated. This is not your kind of traditional minor recession.'”

Click here for the article.

Source: Bloomberg , January 27, 2009.

Financial Times: Nations turn to barter deals to secure food

“Countries struggling to secure credit have resorted to barter and secretive government-to-government deals to buy food, with some contracts worth hundreds of millions of dollars.

“In a striking example of how the global financial crisis and high food prices have strained the finances of poor and middle-income nations, countries including Russia, Malaysia, Vietnam and Morocco say they have signed or are discussing inter-government and barter deals to import commodities from rice to vegetable oil.

“The revival of these trade practices, used rarely in the last 20 years and usually by nations subject to international embargoes and the old communist bloc, is a result of the countries' failure to secure trade financing as bank lending has dried up.

“The countries have not disclosed the value of any deals, and some have refused even to confirm their existence. Officials estimated that they ranged from $5 million for smaller contracts to more than $500 million for the biggest.”

Source: Javier Blas, Financial Times , January 26, 2009.

Financial Times: Capital flows to developing world at risk

“Capital flows to emerging markets are in danger of collapsing this year as the financial crisis in advanced economies risks choking off the supply of credit to the developing world, an association of large banks warned on Tuesday.

“The Institute for International Finance forecasts net private sector capital flows to emerging markets will be no more than $165 billion this year, less than half the $466 billion inflow in 2008 and only one fifth of the amount sent in the peak year of 2007.

“The figures underscore the impact the banking crisis and risk-averse investors are having on emerging market economies, one of the central issues at this year's World Economic Forum in Davos.

“Bill Rhodes, a senior Citigroup executive who is vice-chairman of the IIF, urged leading economies to co-operate with each other and the private sector to address the problem. ‘This is a worldwide recession the like of which we have not seen since World War II,' he said. ‘There is no one country or group of countries that can do this on its own. The only way to solve it is co-ordination across the board.'

“Mr Rhodes also called on the International Monetary Fund to intensify its efforts to supply liquidity to emerging markets by extending the duration of the current facility from three months to more than a year. ‘The IMF's resources need to be expanded and its approaches modified to provide financing to emerging markets that have been caught in a crisis not of their making.'”

Source: Peter Thal Larsen, Financial Times , January 27, 2009.

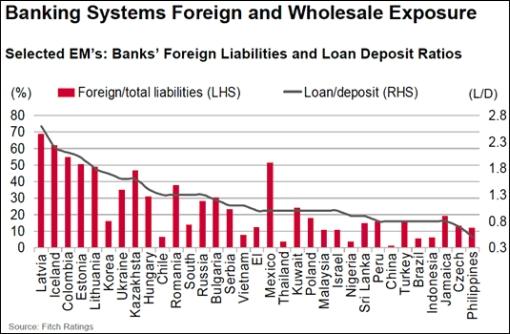

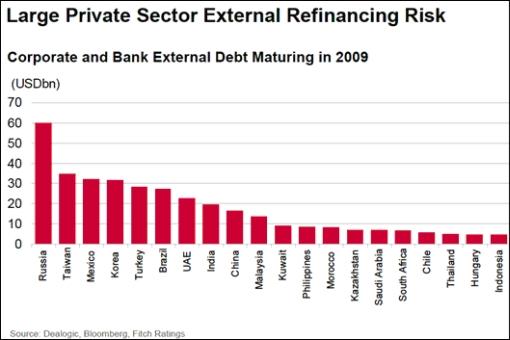

Paul Kedrosky (Infectious Greed): Fun with Fitch - sovereign hotspots

“Some slides from a useful new Fitch presentation on one of my favorite subjects: sovereign hotspots around the world.”

Source: Paul Kedrosky, Infectious Greed , January 29, 2009.

Asha Bangalore (Northern Trust): Fed reiterates support for credit markets

“The Federal Open Market Committee (FOMC) left the target federal funds rate unchanged at 0%-0.25%. Richmond Fed President Lacker cast the only dissenting vote as he would have preferred increasing the monetary base through purchases of Treasury securities rather than through the credit programs.

“The FOMC policy statement noted that the ‘Committee continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time'. This part of the message is identical to the December 2008 statement.

“Overall, today's [Wednesday] statement presented a broader picture of the economic situation and included some bullish expectations about the economy. By contrast, the December 16 policy statement focused largely on features of the Fed's new regime. In particular, six aspects of the policy statement were different from the December 2008 announcement.

“First, significantly slowing global demand was mentioned versus the December statement that did not mention the global economy.

“Second, today's statement noted that ‘conditions in some financial markets have improved, in part reflecting government efforts to provide liquidity and strengthen financial institutions.'

“Third, the FOMC predicts that ‘a gradual recovery in economic activity will begin later this year', and the statement indicated that ‘the downside risks to that outlook are significant'.

“Fourth, in December, inflation was expected to ‘moderate in coming quarters'. There is notable departure from this view because the Fed now ‘expects that inflation pressures will remain subdued in coming quarters'.

“Fifth, the FOMC indicated that it ‘is prepared to purchase longer-term Treasury securities if evolving circumstances indicate that such transactions would be particularly effective in improving conditions in private credit markets'.

“Sixth, today's statement has an explicit discussion about the Fed's balance sheet. As expected the Fed reiterated support of credit markets.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary , January 28, 2009.

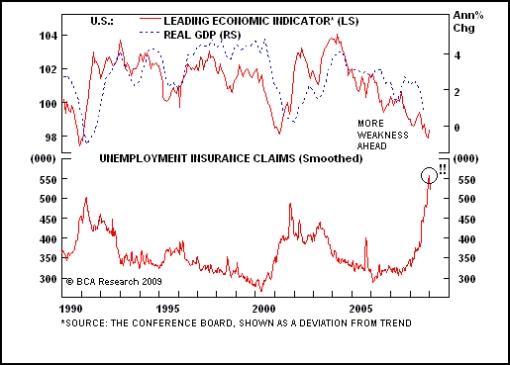

BCA Research: US LEI - uptick unsustainable

“The Conference Board's leading economic indicator (LEI) ticked up in December, but we do not view this as the beginning of a sustained economic recovery.

“The tick up in the LEI was mainly due to the large positive contribution from real money supply and the yield curve. Meanwhile, measures of the real economy continue to weaken: large declines occurred in building permits, employee hours worked, supplier deliveries, while initial unemployment claims are skyrocketing.

“It is still unclear that monetary and fiscal policy are effective (private sector borrowing rates have only marginally fallen) and the housing market is still very weak.

“True, existing home inventories fell in December, but seasonal factors played a large role (inventories always fall during the autumn and winter). Improved activity levels during the spring selling season, should they occur, would be a more accurate signal that the housing market is stabilizing.

“However, the unemployment rate is set to still rise sharply, which will further undermine consumer confidence and spending, particularly on big ticket items. Bottom line: Economic data will continue to be weak and the LEI will likely slide further before a sustainable bottom is made.”

Source: BCA Research , January 29, 2009.

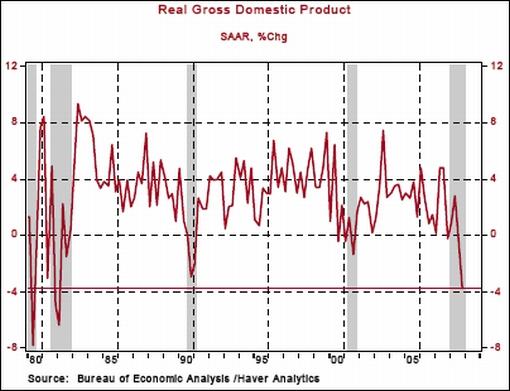

Asha Bangalore (Northern Trust): Q4 GDP Report - gain in inventories masks true weakness

“Real gross domestic product (GDP) declined 3.8% in the fourth quarter of 2008, the minus sign for GDP growth was not a surprise but a larger decline was widely expected. The increase in inventories (+$6.2 billion versus -$29.6 billion in Q3), which was largely unexpected, offset the weakness in demand and trimmed down the headline reading.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary , January 30, 2009.

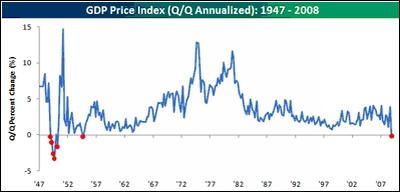

Bespoke: GDP price index enters the deflation zone

“While the markets have been focused on the better than expected GDP report for the fourth quarter, the GDP price index was potentially even more notable. While economists were looking for a quarter/quarter annualized increase of 0.4%, the actual level was a decline of 0.1%. This negative print is only the seventh time since the end of WWII (and the first time since 1954) that prices decrease based on this measure. For now at least, the Fed's view that ‘inflation pressures will remain subdued in coming quarters' appears to be right on target.

Source: Bespoke , January 30, 2009.

Richard Russell (Dow Theory Letters): Is inflation creeping back?

“Below is my inflation/deflation chart. This is simply the long T-bond divided by gold. When the ratio rise in favor of bonds, it's saying that the bonds are stronger than gold, which is deflationary. When the ratio declines in favor of gold, it tells us that gold is gaining in relative strength, and that's inflationary. Note the head-and-shoulders pattern just before the plunge - the plunge took the ratio below the rising trendline. This is the chart Bernanke has been waiting for.”

Source: Richard Russell, Dow Theory Letters , January 27, 2009.

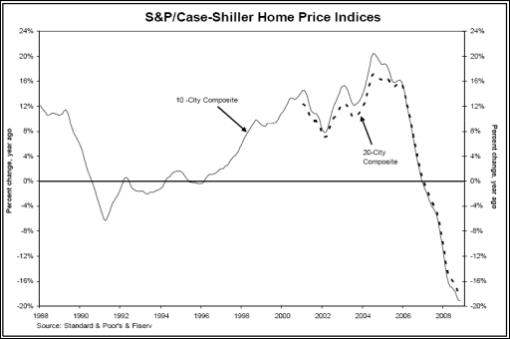

Standard & Poor's: S&P/Case-Shiller - home price declines continue

“Data through November 2008, released today by Standard & Poor's for its S&P/Case-Shiller Home Price Indices, shows continued broad based declines in the prices of existing single family homes across the United States, with 11 of the 20 metro areas showing record rates of annual decline, and 14 reporting declines in excess of 10% versus November 2007.

“‘The freefall in residential real estate continued through November 2008,' says David Blitzer, Chairman of the Index Committee at Standard & Poor's. ‘Since August 2006, the 10-City and 20-City Composites have declined every month - a total of 28 consecutive months.'”

Source: Standard & Poor's , January 27, 2009.

Asha Bangalore (Northern Trust): Existing home sales - inventories remain at elevated levels

“Sales of existing homes rose 4.7% in December after two monthly declines, inventories remain at elevated levels, and the median price of an existing single-family home fell in December. The gain in home sales is noteworthy while other aspects of today's report are much the same as we have seen for several months. The important take-away in this report is that inventories of unsold existing homes remain at elevated levels. Although mortgage rates have moved up slightly, they remain at significantly favorable levels.

“The seasonally adjusted inventory-sales ratio of existing single-family homes fell to a 9.6-month supply from an 11.4-month supply in November. This appears impressive at the outset, but digging deeper it appears that the November reading was probably an aberration because the quarterly averages for 2008 range between a 9.8-month supply and a 10.26-month mark. Inventories of unsold homes need to shrink considerably more for home prices to stabilize.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary , January 26, 2009.

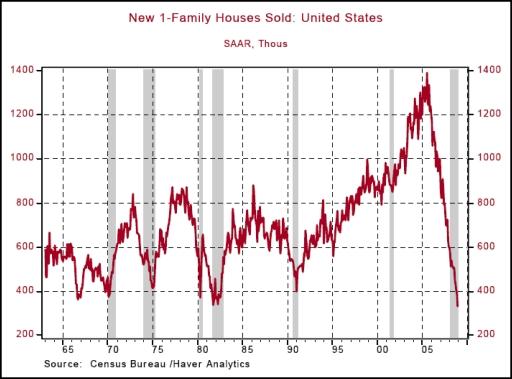

Asha Bangalore (Northern Trust): New home sales plunge

“In December, sales of new homes declined, prices fell, and inventories were the highest on record. The main message from the December report is that homebuilders will continue to reduce production of new homes.

“The inventory of unsold new homes rose to a 12.9-month supply in December, the largest on record.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary , January 29, 2009.

The Wall Street Journal: An upside to plunging home prices

“John Lonski, CEO of Moody's Capital Markets Research Group, discusses the latest decline in home prices. He tells WSJ's Kelly Evans that although it highlights plunging home prices and the deterioration of mortgage-backed securities, it's promoting the stabilization of home sales.”

Source: The Wall Street Journal , January 27, 2009.

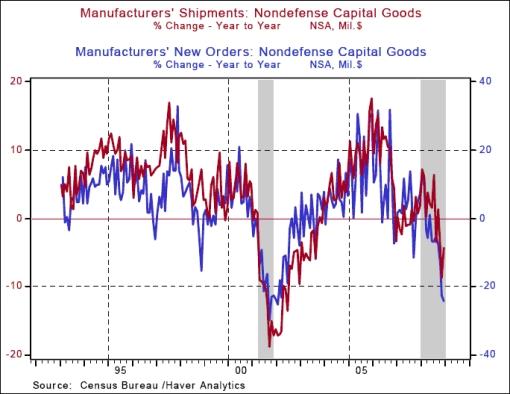

Asha Bangalore (Northern Trust): Durable goods orders post sharp drop

“Orders and shipments of durable goods fell in 2.6% in December, after a downwardly revised 3.7% drop in November. The declines in orders of durable goods were widespread.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary , January 29, 2009.

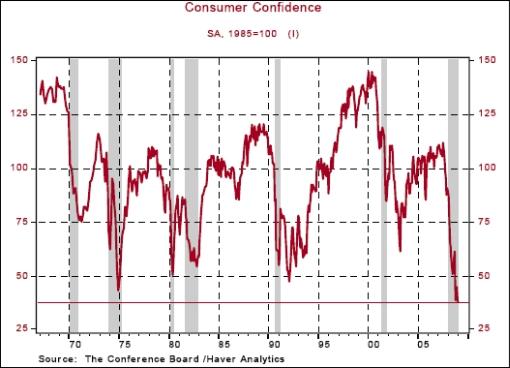

Asha Bangalore (Northern Trust): Consumer confidence posts new low

The Conference Board's Consumer Confidence Index fell to 37.7 in January from 38.6 in December. This is a new record low for the series which dates back to February 1967. The grim headlines and media coverage of the financial and economic turmoil and staggering layoff announcements justify the sober consumer outlook.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary , January 27, 2009.

The Wall Street Journal: Lending drops at big US banks

“Lending at many of the nation's largest banks fell in recent months, even after they received $148 billion in taxpayer capital that was intended to help the economy by making loans more readily available.

“Ten of the 13 big beneficiaries of the Treasury Department's Troubled Asset Relief Program, or TARP, saw their outstanding loan balances decline by a total of about $46 billion, or 1.4%, between the third and fourth quarters of 2008, according to a Wall Street Journal analysis of banks that recently announced their quarterly results.

“Those 13 banks have collected the lion's share of the roughly $200 billion the government has doled out since TARP was launched last October to stabilize financial institutions. Banks reporting declines in outstanding loans range from giants Bank of America and Citigroup, each of which got $45 billion from the government; to smaller, regional institutions. Just three of the banks reported growth in their loan portfolios: US Bancorp, SunTrust Banks Inc. and BB&T Corp.

“The overall decline in loans on the 13 banks' books - from about $3.36 trillion as of September 30 to $3.31 trillion at year's end - raises fresh questions about TARP's effectiveness at coaxing banks to reopen their lending spigots.

Source: The Wall Street Journal , January 26, 2009.

Richard Russell (Dow Theory Letters): Will new primary bull market be signalled?

“The Dow Theory to the fore. On January 20, the DJ Transportation Average broke below its November 20 bear market low of 2,988.99. The new low was not confirmed by the Industrial Average, which held above its own November 20 bear market low of 7,552.29. This non-confirmation set up the potential for a Dow Theory bull signal. If the Industrials and Transports can now muster the strength to rally above their preceding January peaks, (Industrials on January 6 at 9,015.10 and Transports at 3,717.26), a new primary bull market will be signaled.

“There are two concepts about this that bother me.

(1) If a new bull market is signaled, it would mean that the bear market of November 2007 to November 2008 ended in only one year. Since the preceding bull market (1982 to 2007) lasted 25 years, a one-year bear market (no matter how severe) seems too short in time to correct one of the greatest bull markets in history.

(2) Based on the Lowry's figures, it appears that most of the upside progress since the November 20 bear market lows has been the result of a decline in selling pressure. Historically, the beginning of a new bull market has been characterized by not only a drastic drop in Lowry's Selling Pressure Index, but also by heavy buying and strong upside volume (neither of which has been present).

“The stock market often tries to confuse us by coming up with something new. Assuming that the Averages do better their preceding January peaks, it would have occurred without the usual heavy buying on rising volume. It may be that the January 6 peaks will have to be bettered before the ‘real' volume comes in. In other words, even if a new bull market is signaled in the weeks ahead, we will have to monitor the stock market action carefully, to make sure we are not being sucked in to a fake rally as was the case following the 1929 crash.”

Source: Richard Russell, Dow Theory Letters , January 29, 2009.

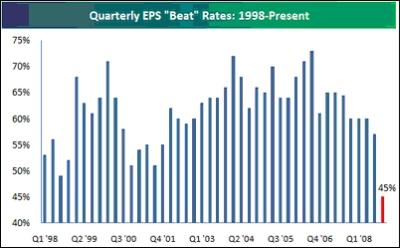

Bespoke: Fourth quarter earnings “beat rate” below 50%

“There's still a long way to go before the fourth quarter earnings season comes to an end, but the first batch of reports indicate just how bad of a quarter it was. Since Alcoa kicked off earnings season earlier this month, only 45% of US companies have beaten analyst EPS estimates. As shown in the chart below, this would be the lowest reading since at least 1998. Even though analysts have been cutting estimates sharply over the past few months, companies still haven't been able to beat at a better than 50% clip. Hopefully this ‘beat rate' gets better as earnings season chugs along, but we wouldn't count on it.”

Source: Bespoke , January 26, 2009.

Bloomberg: Earnings may slump 45%, Socgen says

“Analysts have cut their estimates for company earnings worldwide by $1 trillion since October, suggesting profits may tumble as much as 45% this year amid the global recession, according to Societe Generale SA.

“A profit slump of that magnitude would mean stocks are trading at 20 times future 12-month earnings, according to calculations by the quantitative analysis team at France's third- largest bank, led by Andrew Lapthorne in London. The MSCI World Index currently trades at 10.7 times its members' estimated earnings after plummeting 42% in 2008 and 11% so far this year, according to Bloomberg data.

“‘Global earnings forecasts are disintegrating as companies and analysts struggle to adjust to rapidly declining commodity prices, continuing financial sector losses and, of course, a crumbling global economy,' wrote Lapthorne's team in a report today. ‘There is little sign of this pace of downgrading abating. Equities will struggle.'”

“Analysts estimate companies on the Standard & Poor's 500 Index will report a 28% drop in fourth-quarter profits, according to data compiled by Bloomberg. That compares with a 55% increase forecast in March 2008. Analysts currently predict earnings will decline 2.3% in 2009, the data show.

“SocGen's strategy team estimated the 45% profit decline by extrapolating the pace of downgrades to earnings predictions since October. The team was ranked first by investors in Europe this year, according to Thomson Reuters Plc's Extel survey.”

Source: Alexis Xydias, Bloomberg , January 23, 2009.

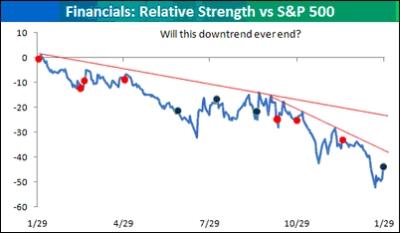

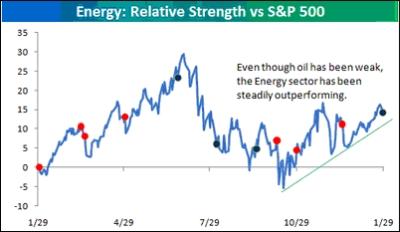

Bespoke: Sector relative strength - financials still lagging

“In our relative strength charts, we highlight how each sector has performed versus the S&P 500 over the last year. For each sector, rising lines indicate the sector is outperforming the S&P 500, while falling lines indicate underperformance. In each chart, we also note each Fed meeting over the last year. Red dots indicate meetings where the Fed lowered rates, while black dots indicate meetings where the Fed left rates unchanged.

“While the Financial sector has led the recent rally, a look at the sector's long-term relative strength shows that they are nowhere near breaking the downtrend they have been in for at least a year now.

“While everyone is focused on the Financials, the Energy sector has been enjoying its position out of the spotlight. While the sector was killed in the summer and fall when the decline in oil kicked into high gear, since then, energy stocks have been steadily outperforming even as oil remains near its lows. Just imagine what could happen if oil actually started to rally.”

Source: Bespoke , January 29, 2009.

Bespoke: 10-year Treasury yield reaches key juncture

“Even with the Fed's reiteration that they were considering outright purchases of US Treasuries, the yield on the 10-year has been climbing steadily higher from its lows in December. At 2.77%, the 10-Year is approaching yields that it traded at before the bottom dropped out in early December. How we trade in the next few days will go a long way in determining whether the current sell-off is simply profit-taking after a massive rally, or the beginning of the end of the latest bubble in asset classes (stocks, real estate, commodities, etc.).”

Source: Bespoke , January 29, 2008.

David Fuller (Fullermoney): Treasuries - a dangerous game

“The promise (threat?) by the Fed to purchase US long-dated securities has deterred me from shorting them to date, despite some very good sell signals …

“However I have also described the Fed's frequent hints of its apparent willingness to buy US debt as akin to a con artist's shell game. However in the Fed's version, instead of trying to guess under which of three rapidly moving cups the pea lurks, we are guessing how and when we might see their bond purchases.

“I do not question the Fed's word that it would be prepared to buy Treasuries to keep long-term rates low, if necessary. Instead, my point is that they may hope to avoid purchases if they persuade the market to do their work for them. In other words, I wonder how many people, from hedge fund managers to foreign governments, have bought or at least retained their Treasuries, despite historically low yields and rapidly increasing supply.

“This is a dangerous game. Financial history is full of instances where investors have been persuaded to pay record high valuations for assets, usually because: ‘It is different this time.' Perhaps … for a while, but the bubble always bursts in a mean reversion process which usually ends in an overshoot of its own.

“The only way I can envisage significantly lower long-term yields for US Treasury bonds, would be if the economy slid into a lengthy deflation, as we saw with Japan in the late 1990s and earlier this decade, causing real interest rates to rise. This is a risk, but one that the Bernanke Fed has vowed to avoid. It has the means to do so.

“At Fullermoney, we think gold is replacing US Treasuries as the safe haven investment.”

Source: David Fuller, Fullermoney , January 30, 2009.

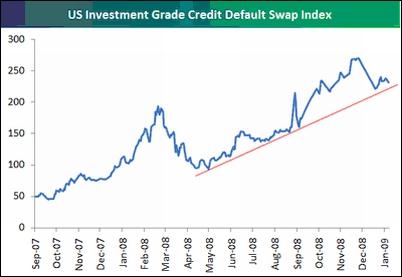

Bespoke: Credit default risk down but still high

“Below we highlight a chart of an index that measures the default risk of investment grade credit in the US. Throughout the credit crisis, default risk has risen sharply, although it has ticked lower since peaking in December. Any decline in default risk is a good sign, but it needs to fall much more before anyone can make the claim that things are ‘settling down'. As shown, the index has still not broken below the bottom of its uptrend line that formed back in April 2008.”

Source: Bespoke , January 27, 2009.

Bloomberg: Soros stopped betting against pound

“Billionaire investor George Soros, who made $1 billion selling the pound in 1992, said he is no longer betting against the UK currency after it reached $1.40.

“‘I did actually foresee the fall in sterling and that was one of the positions we carried,' he told reporters at the World Economic Forum in Davos, Switzerland. Below $1.40 ‘it seemed to me the risk-reward was no longer clear'.

“Soros said today that he has made money from the financial crisis. The British government's efforts to protect the banking system from the turmoil last week led to a drop in the pound to the lowest level against the dollar since 1985.

“‘We did have a short position in sterling, but it doesn't mean I'm bearish on sterling today or bullish,' Soros said. ‘It will continue to fluctuate.'

“Soros's comments contrast with those of Jim Rogers, who co-founded the Quantum Fund with him and is now chairman of Singapore-based Rogers Holdings. Rogers said on January 20 that the pound was ‘finished' because of turmoil in the banking system and a decline in North Sea oil output.”

Source: Simon Kennedy, Bloomberg , January 28, 2009.

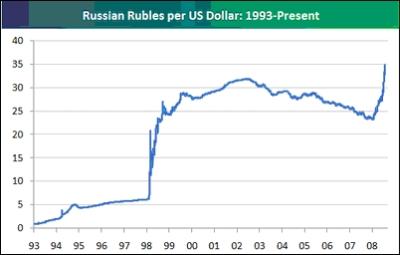

Bespoke: Russian troubles

“Russia's currency made news today for having its biggest two-day decline versus the dollar in a decade. For those interested, below we provide a long-term chart of the Russian ruble versus the US dollar. As shown, the amount of rubles that one dollar will get you has spiked significantly in recent months, going from about 23 rubles per dollar last May to its current level of 34.84 rubles per dollar.”

Source: Bespoke , January 29, 2009.

BBC News: Zimbabwe abandons its currency

“Zimbabweans will be allowed to conduct business in other currencies, alongside the Zimbabwe dollar, in an effort to stem the country's runaway inflation.”

Source: BBC News , January 29, 2009.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2009 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.