U.S. Treasuries Massive Rally as Helicopter Ben Fires Buyback Bazooka

Interest-Rates / US Bonds Dec 02, 2008 - 05:04 AM GMTBy: Mike_Shedlock

Treasuries staged yet another massive rally today as Helicopter Ben imitates Paulson and pulls out his own bazooka. Inquiring minds are noting that Treasury Yields Drop to Record Lows as Bernanke Cites Buybacks .

Treasuries staged yet another massive rally today as Helicopter Ben imitates Paulson and pulls out his own bazooka. Inquiring minds are noting that Treasury Yields Drop to Record Lows as Bernanke Cites Buybacks .

Treasuries rose, pushing yields to record lows, as Federal Reserve Chairman Ben S. Bernanke said the central bank may purchase Treasuries and target long-term interest rates to combat the deepening recession.

Bonds rallied for a fourth day, sending yields on two-, 10- and 30-year debt to the lowest since the Treasury began regular sales of the securities. Bernanke said he has “obviously limited” room to lower interest rates further and may use less conventional policies, such as buying Treasury securities.

“The thing that was significant is the reminder that the FOMC can buy long Treasuries,” said Jamie Jackson, who oversees government and agency debt trading at Minneapolis-based RiverSource Investments, which manages $90 billion. “Bernanke explicitly said they still had more room to go in easing policy.”

Text Of Helicopter Ben's Speech - December 1, 2008

Here are some highlights of Bernanke's speech about Federal Reserve Policies in the Financial Crisis before the Greater Austin Chamber of Commerce, Austin, Texas.

The Outlook for Policy

Going forward, our nation's economic policy must vigorously address the substantial risks to financial stability and economic growth that we face. I will conclude my remarks by discussing the policy options of the Federal Reserve, focusing on the three aspects of policy that I laid out earlier: interest rate policy, liquidity policy, and policies to stabilize the financial system.

Regarding interest rate policy, although further reductions from the current federal funds rate target of 1 percent are certainly feasible, at this point the scope for using conventional interest rate policies to support the economy is obviously limited. Indeed, the actual federal funds rate has been trading consistently below the Committee's 1 percent target in recent weeks, reflecting the large quantity of reserves that our lending activities have put into the system.

In principle, our ability to pay interest on excess reserves at a rate equal to the funds rate target, as we have been doing, should keep the actual rate near the target, because banks should have no incentive to lend overnight funds at a rate lower than what they can receive from the Federal Reserve. In practice, however, several factors have served to depress the market rate below the target. One such factor is the presence in the market of large suppliers of funds, notably the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, which are not eligible to receive interest on reserves and are thus willing to lend overnight federal funds at rates below the target.1

We will continue to explore ways to keep the effective federal funds rate closer to the target.

Although conventional interest rate policy is constrained by the fact that nominal interest rates cannot fall below zero, the second arrow in the Federal Reserve's quiver--the provision of liquidity--remains effective. Indeed, there are several means by which the Fed could influence financial conditions through the use of its balance sheet, beyond expanding our lending to financial institutions. First, the Fed could purchase longer-term Treasury or agency securities on the open market in substantial quantities. This approach might influence the yields on these securities, thus helping to spur aggregate demand. Indeed, last week the Fed announced plans to purchase up to $100 billion in GSE debt and up to $500 billion in GSE mortgage-backed securities over the next few quarters. It is encouraging that the announcement of that action was met by a fall in mortgage interest rates.

Expanding the provision of liquidity leads also to further expansion of the balance sheet of the Federal Reserve. To avoid inflation in the long run and to allow short-term interest rates ultimately to return to normal levels, the Fed's balance sheet will eventually have to be brought back to a more sustainable level. The FOMC will ensure that that is done in a timely way. However, that is an issue for the future; for now, the goal of policy must be to support financial markets and the economy.

Footnotes

1. Banks have an incentive to borrow from the GSEs and then redeposit the funds at the Federal Reserve; as a result, banks earn a sure profit equal to the difference between the rate they pay the GSEs and the rate they receive on excess reserves. However, thus far, this type of arbitrage has not been occurring on a sufficient scale, perhaps because banks have not yet fully adjusted their reserve-management practices to take advantage of this opportunity.

The Theory and The Practice

The theory says ability to pay interest on reserves will prevent short term rates from dropping below the Fed Funds rates. In practice Bernanke states " We will continue to explore ways to keep the effective federal funds rate closer to the target ."

The irony is that Bernanke goes out of his way to tell banks to borrow from the GSE's to earn a sure profit on funds deposited on reserve.

And the silliness is he expects banks to take chances on lending when instead they can get sure profit by borrowing from the GSEs and parking the money as reserves. Amazing.

Bazooka Is Loaded

The bazooka is loaded and the helicopter drop has begun. Why anyone would be shorting the long bond when Bernanke is just doing what he said he would do in his famous helicopter drop speech Deflation: Making Sure "It" Doesn't Happen Here is beyond me. Here is the paragraph to consider from his November 21, 2002 speech:

So what then might the Fed do if its target interest rate, the overnight federal funds rate, fell to zero? One relatively straightforward extension of current procedures would be to try to stimulate spending by lowering rates further out along the Treasury term structure--that is, rates on government bonds of longer maturities.

There are at least two ways of bringing down longer-term rates, which are complementary and could be employed separately or in combination. One approach, similar to an action taken in the past couple of years by the Bank of Japan, would be for the Fed to commit to holding the overnight rate at zero for some specified period. Because long-term interest rates represent averages of current and expected future short-term rates, plus a term premium, a commitment to keep short-term rates at zero for some time--if it were credible--would induce a decline in longer-term rates. A more direct method, which I personally prefer, would be for the Fed to begin announcing explicit ceilings for yields on longer-maturity Treasury debt (say, bonds maturing within the next two years). The Fed could enforce these interest-rate ceilings by committing to make unlimited purchases of securities up to two years from maturity at prices consistent with the targeted yields. If this program were successful, not only would yields on medium-term Treasury securities fall, but (because of links operating through expectations of future interest rates) yields on longer-term public and private debt (such as mortgages) would likely fall as well.

Lower rates over the maturity spectrum of public and private securities should strengthen aggregate demand in the usual ways and thus help to end deflation.

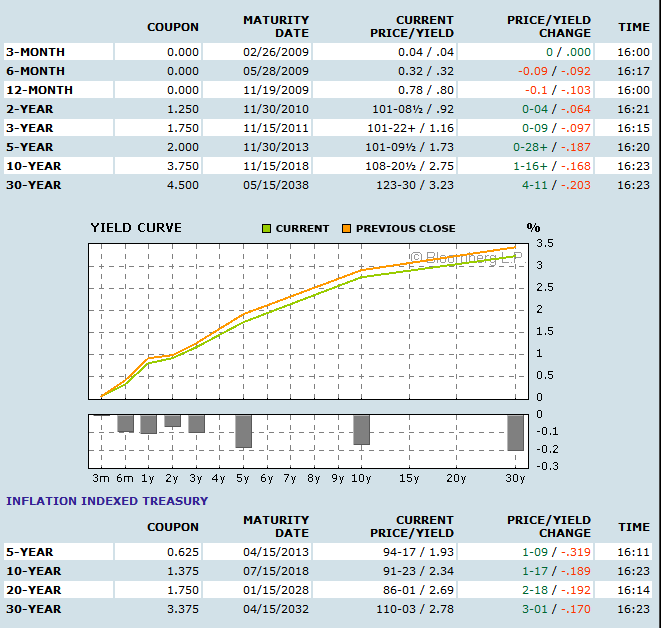

Treasury Yields

Sure enough. The effective Fed Funds Rate fell to zero, spurring Bernanke to pull out his bazooka, firing at the yield on the long bond. It was a direct hit.

Yield Curve as of December 1, 2008.

chart courtesy of Bloomberg .

Yield Curve Flattens

Since the lower bound of treasuries have been at 0% for quite some time, any further rally in treasuries could only come from a flattening of the curve.

Historical Yield Curve

The above chart shows why Bernanke has pulled out his bazooka. There is no more room to cut on the short end, except symbolically. He admitted as such in his speech today. Furthermore there is no recovery in sight which he also admitted. So... He is doing what he said he would do, attempting to force down yields on the long end.

Treasury Bubble?

With this action we are finally at the stage where it is reasonable to start discussing a treasury bubble. However, that does not mean short treasuries. It simply means that chart patterns suggest a blowoff move could be in the making.

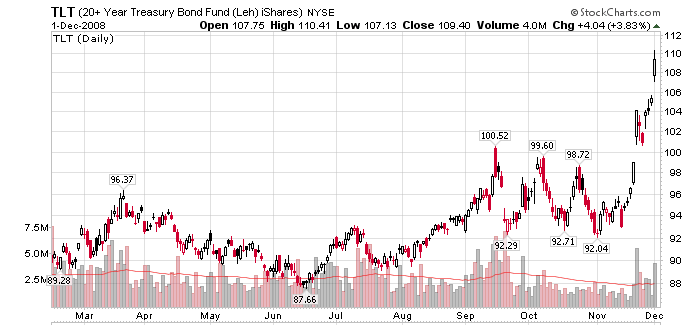

TLT Lehman 20+ Year Treasury Fund Daily

The above chart is indicative of the type of blowoff move we have seen in various stocks and commodities. However, let's not rush to judgment and instead look at other charts and ideas to quantify the bet against treasuries.

TLT Lehman 20+ Year Treasury Fund Monthly

Note that the monthly chart is just a tad overextended, not reflective of the hyperbolic move shown on the daily chart.

Furthermore, one betting on a sustained failure of the treasury rally at this point is pretty much betting on an economic recovery like we saw in 2003. Given stated expectations of rising unemployment, collapsing commercial real estate prices, and continued weakening of consumer spending, there is no reason at this point to think such an economic recovery is likely anytime soon.

Long dated treasuries are certainly not the screaming buy I thought they were a few months ago when nearly everyone was screaming bubble. However, that does not make them anything remotely close to being a good short.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2008 Mike Shedlock, All Rights Reserved

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.