S&P 500 Cyclical Relative Performance: Stocks Nearing Fully Valued

Stock-Markets / Stock Markets 2024 May 23, 2024 - 07:46 PM GMTBy: Submissions

The S&P 500 index of large cap U.S. stocks has rallied +49% since the October 2022 lows, and +28% since the most recent October 2023 lows. Bulls argue that the equity rally has much more time to run. Typical bull markets last about 5 years. If we consider the January to October 2023 correction to have been a significant bear market that reset the excesses from the prior bull market, then the bull market longevity argument makes senses. Recall that the S&P 500 fell -26% from January to October 2023 following the post-Covid “bull market”, resulting in +108% equity gains. On the other hand, if we argue the bearish case, Covid distortions likely mean that the typical lengths (and magnitudes) of the bull and bear phases can’t be applied today. Bears could argue that the 2022 correction/bear market represented a mid-cycle correction or just a cooling of the excessive movement from April 2000 to December 2021. In any case, whether this is year 4 of a bull market that begin in 2020 or year 2 of a bull market that begin in 2022 would seem to have little predictive power of how much longer equities will rally, assuming again that Covid distortions will skew historical trends.

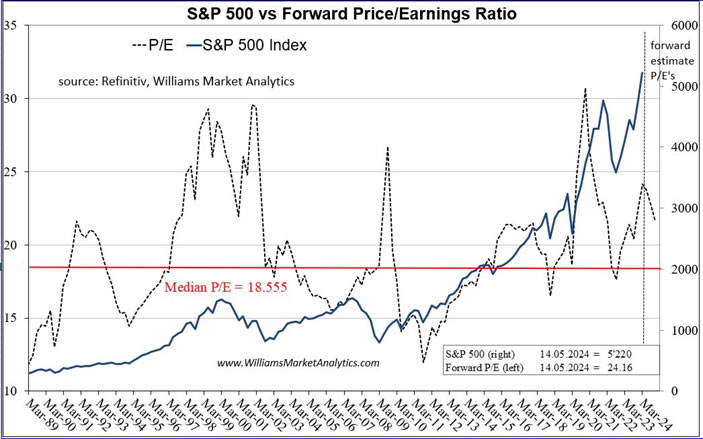

Our objective today is to determine have much of our portfolios to allocate to risky assets versus monetary products/bonds. The title of this research note, “Stocks Nearing Fully Valued”, is not a call on equity valuations according to price-to-earnings. Valuations “don’t matter” when investors and fund managers are buying stocks as a hedge against inflation and the devaluation of the dollar. Remember, stock prices should float higher, all else equal, to maintain the real prices of stocks constant. Jay Powell’s lackadaisical attitude to fighting inflation and Janet Yellen’s desire to devalue the dollar to fund ever increasing U.S. debt expense also explains the performance of bitcoin and gold. Investors need to be in risky assets to protect purchasing power of their savings. That said, we’d argue that stocks are also fully valued by fundamental measures. Below is our S&P 500 P/E chart.

At over 24x forward (optimistic) earnings forecasts, we’d can’t say that stocks are cheap today. The median P/E since 1988 has been 18.55x. It is said that price-to-earnings is not a good timing indicator, but a quick inspection of our chart shows that an investor’s long-term returns would be greatly improved by waiting until P/E’s come down to (or fall below) the median historic P/E.

Instead of considering U.S. stocks as “fully valued” versus traditional valuation metrics, we look at the relative valuation of the S&P 500 compared to alternative investments. Our analysis suggests that U.S. large capitalization stocks are generally over-valued of a relative basis. We begin by looking at the S&P 500 versus its own trend cycle, then compare the S&P 500 to bonds, commodities, and to the ex-U.S. world stock markets.

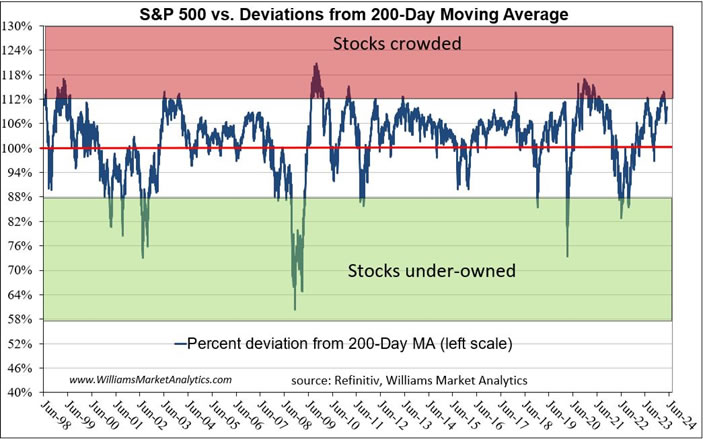

One indicator that we like is comparing an index to its 200-day moving average. The 200-day moving average is a popular reference point for traders and investors. Whether the market is in a long-term up-trend or a down-trend, prices do tend to have a mean-reverting tendency to this line.

The red line in the chart shows the S&P 500 price trading at its 200-day moving average. We used 12% bands around the 200-day moving average, which have historically represented extreme deviations from this trend line. The S&P 500 last touched its 200-day moving average last October 2023. Before moving back into the “red zone” in early April 2024. While we have seen the S&P hold above its 200-day for more than 7-months in the past, these occurrences are not frequent. Even in a roaring uptrend, it has paid to lighten up after extreme (+12%) deviations and re-invest after breaks then reversals back above the red line. The equity selling seen in April did not bring the S&P 500 even close to the red line, suggesting that U.S. equities are still extended, at least in the short-term.

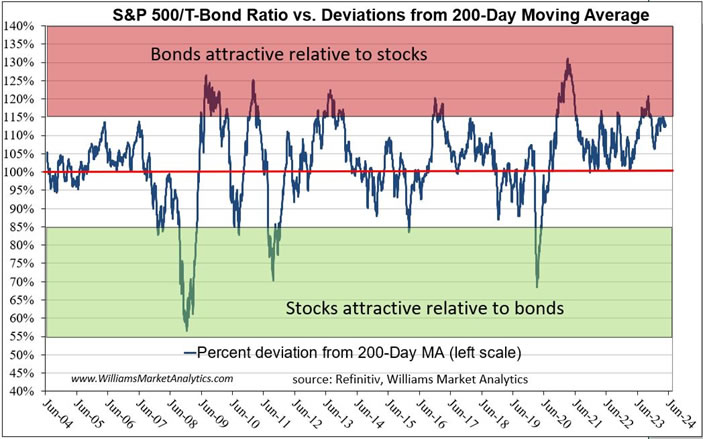

Our next indicator of relative valuation takes the ratio of the S&P 500 to the Treasury Bond. Again, the red line demarks the ratio of equities-to-bonds trading at its 200-day moving average. We use 15% bands to denote extreme divergences here. Stocks have been in a massive uptrend versus bonds since the Covid collapse. The ratio of stocks/bonds did come down to its rising 200-day moving average several times during the 2022 bear market. Since the October 2022 bottom, however, stocks have enjoyed a long period of outperformance. The S&P 500 correction ending last October 2023 did not push the stock/bond ratio back to its rising 200-day moving average.

Even with the negative inflation headwind eroding bond returns, earning coupon interest today seems more attractive than gambling on how long stocks can diverge from their uptrend versus bonds.

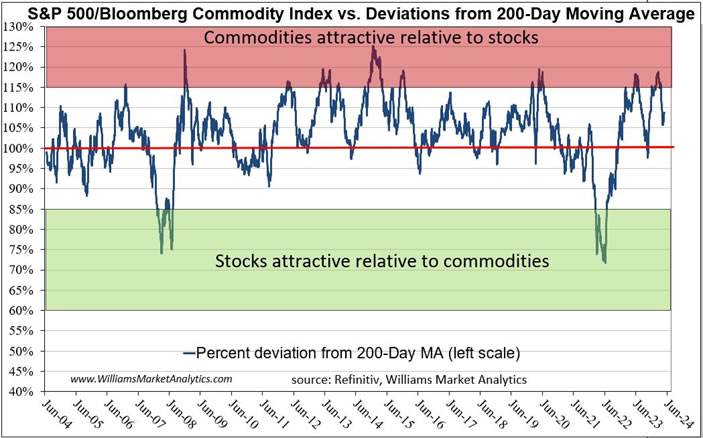

Next we looked at relative valuations of stocks versus commodities, using the Bloomberg Commodity Index. Commodity prices, like equities, serve as inflation-hedging assets. We used 15% bands around the 200-day moving average of the stock/commodity ratio to denote excesses. Stocks have mostly outperformed commodities outside of bear markets (2007-2009, 2022). We have not seen the stock/commodity ratio come down to the 200-day moving average since last October. However this ratio has, on several occasions, remained above the 200-day trend line for over a year, so we don’t have a strong case for stocks to mean revert immediately based on this metric.

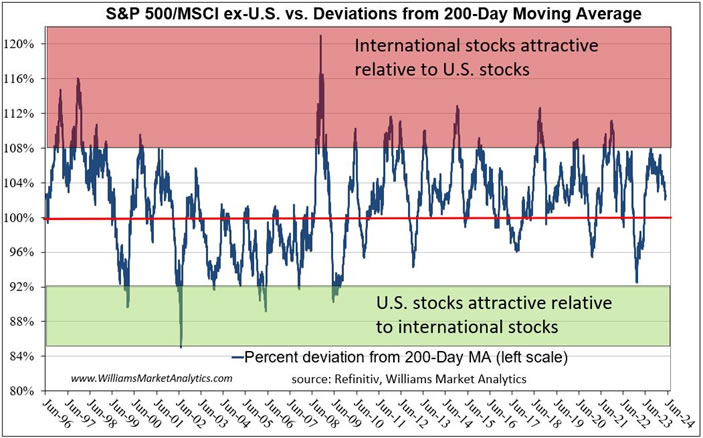

Our final look at S&P 500 relative valuation compares the U.S. stock index to the MSCI All-World ex-U.S. Index. The U.S. stocks outperform (1995-2000, 2009-2024) or underperform (2000-2009) for long multi-year periods. Our indicator attempts to catch shorter cycles by taking the ratio of the S&P 500 to the MSCI All-World ex-U.S. and then looking for deviations from trend. The divergences of this ratio from the 200-day trend resemble an oscillator such as the RSI. We used 8% deviations to denote “over-bought” or “over-sold” levels of the S&P 500.

S&P 500 relative outperformance peaked last summer, with international stocks beating U.S. stock for about 9-months now. Typically U.S. stocks become relatively attractive during periods of turmoil, as seen by the spikes down towards the green zone (2008-09, 2020, 2022). Right now with the ratio sliding lower, we could interpret this as a broaden out into more risky international stocks. The Nikkei, DAX, and FTSE 100 have all had even more extraordinary run-ups over the past couple months than U.S. stocks. In sum, U.S. stocks are no longer at an extreme versus international stocks but are still far from being relatively attractive in comparison to international stocks.

Conclusion

U.S. stocks have resumed their melt-up following profit-taking in April. While fundamental valuation metrics, such as P/E remain stretched, we see that S&P 500 relative valuations compared to other asset classes suggests that U.S. stocks are crowded, but not currently at extremes. Long-term investors can probably wait for a pull-back to find a more attractive entry level into U.S. stocks.

By Owen WIlliams

Owen Williams is professor of finance at the EM Lyon Business School. He holds a PhD in finance from the Grenoble Ecole de Management and is a CFA charterholder. His research interests include asset pricing, currency markets, and portfolio theory.

© 2024 Copyright Owen WIlliams - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.