Deflation Monster Coming as Credit Losses Far Exceed Capital Injections

Stock-Markets / Credit Crisis 2008 Oct 28, 2008 - 02:58 PM GMTBy: Mick_Phoenix

This week an Occasional Letter From The Collection Agency looks at what might be on the horizon as we peer into the macro-economic future. As ever we start with a reminder of the scenario that I have been following over the past 6 years or more:

This week an Occasional Letter From The Collection Agency looks at what might be on the horizon as we peer into the macro-economic future. As ever we start with a reminder of the scenario that I have been following over the past 6 years or more:

bubble, easy money, inflation in fiat money supply, inflation in commodities and hard assets, inflation, fear of inflation, rising rates, YC inverting, flattening, rising and inverting again, tightening, withdrawal of liquidity, corrections, crashes, talk of stagflation, FEAR, withdrawal of speculative funds, further corrections and crashes, demand collapse.......Deflation.

As you can see the scenario is nearing its conclusion as we see the final elements fall into place. I believe we have moved beyond fear and are suffering the results of the withdrawal of speculative funds and further corrections and crashes. There are signs that the beginning of the demand collapse has started on a global basis and at a speed that is beyond any Government or Central Bank to react to.

That means a deflationary recession or depression is looming in our near future, caused by those currently feted as the saviours of the capitalist system. In 6 months time I doubt the public will think of the current crop of politicians and central bankers as saviours.

To get some idea of why I blame government and central bank intervention for the final destination of the global economy you may wish to visit an article I wrote in March '08 in reply to John Mauldin here .

Enough of the past, now is the time to look forward, to see what will be waiting for us in the future. Let me start by saying I am at a bifurcation point, that is I have 2 views in play right now. My majority report says that we are staring into a very deep, dark abyss that will result in a new form of capitalism, regulated and governed in ways many have yet to fathom. My minority report says we are staring into a very deep, dark abyss that will destroy capitalism as the tool used to trade assets.

Is capitalism sacrosanct, will it endure as they only method of trading? That is a big question and worthy of very deep analysis but as I have limited time and resources I am not going to enter the debate. With the amount of intervention occurring and the efforts that will be made in the future to keep capitalism functioning it might be a moot point in the end, hence my minority tag.

Instead I want to look at a path that leads from our current circumstances which accepts that capitalism in a new form will continue to govern the macro-economic future.

Firstly I have to assume that the global economy is about to enter a very deep recession or depression. If this assumption is wrong then that doesn't mean the problems are fixed and we set sail for economic nirvana aboard the USS Bernanke. It just means that the inevitable arrival at a global financial conflagration is delayed until the system allows some idiot to invent a new financial innovation that will destroy the banks et al.

On a macro level we are already seeing the decoupling events, the G10 have the means to re-capitalise by accessing an enormous pool of centrally controlled cash liquidity. However beyond this group we are seeing major financial strains appearing as the reserves (especially $) of governments are stretched to cover the withdrawal of G10 based foreign investment. Only those who truly saved inward $ investment, such as China, possibly Russia and some Oil States have the ability to defend their own economies from the worst effects of what is to come.

This has created a real demand for the $, as countries, banks, corporations and increasingly smaller companies require $'s to service or repay $ denominated debt. The liquidation of the global carry trade and other $ or Yen based financial investments has caused a flight to cash, resulting in a strengthening of these 2 currencies at the expense of the rest of the world. It clearly shows that the 2 Central Banks that allowed monetary easing and credit creation to stave off previous rounds of financial crisis have been the main catalysts for the coming debacle.

As we can see, cash is king, we do not see the re-investment of $ or Yen in their domestic markets over the past 90 days:

(Courtesy of Stockcharts.com)

What we see is a typical confirmation of a deflationary effect, as a currency becomes stronger due to a lack of availability then the assets priced in that currency fall in price. This will continue until the appreciation of the currency is complete. Only then will the price of assets in those currencies stabilise and become more affected by supply and demand.

As I stated in the past the amount of money in circulation can be reduced by means other than government or central bank intervention, what we are seeing is "mattress stuffing" on a global scale. This is why the bail out attempts will fail. Rather than explain it again, here is a reply to a trading buddy at Livecharts.co.uk:

- Easy times - 4100 of 4102

CA, so the tracker mortgages will be a thing of the past with 2.5% base rates and 5 to 6% lending rates? Any ideas of when we'll see these rates of say 8%+ and how long they would remain at those levels. I'm locked in at 5.6% for 2 years but it's getting scary if after that they jump to say 10%. Means that mortgage payers are going to have to slash their mortgages by repaying capital as fast as possible.

collection agency - 4102 of 4102

Hi ET,

The banks will steepen the curve as much as possible, some have already raised rates this past week even after the base rate cut.

Borrow short and cheap and roll, lend long and high is still what they think will save them. This is just an income stream idea though, still ponzi related. The real worry for them is the capital depreciation on loans made. There comes a point were default on debt will mean higher Tier 2 and 3 assets, meaning Tier 1 will have to be re-capitalised....again.

When a bank makes a loan it becomes an asset because it earns income. So far we have seen the effects of what happens when the income on an asset (remember these assets are bundles of different grades of debt - MBS etc) is degraded, next up is when the assets become worthless in the face of mass default.

I am not surprised by the current behaviour of banks; they are after every penny they can get. If we go by the rate differentials seen in the US (and we seem to be following the same pattern) then the mortgage rate for prime will be 3%-4% above base, minimum. Anything else, if you can get it, will be 5-7% above base. However I suspect this will become a political hot potato with pressure being placed on banks to cap the steepening of their curve.

This is why the whole bail-out system adopted by Euro/UK/US will fail. If the Trillions had been used to offset the asset depreciation, i.e. lower the amount owed by direct government relief on debt (e.g. pay off a lump sum of each mortgage in a swap arrangement for a % ownership of the asset, which could be bought back over time or paid off when the property is sold) then the lower debt level could be serviced and the public would have had a direct monetary stimulus, without money going through the pricing mechanism, its non-inflationary. House prices could then re-set to realistic levels linked to real income.

This method would allow a deflation to occur without leaving the onerous debt burden in place that was set in an inflationary atmosphere. Whilst shared equity on houses sounds socialist (part-owned etc) it is a better alternative to mass default and renting a bed sit or B&B room to house families.....

Instead they gave the money to banks and others to bolster capital reserves and Tier 1 assets. That means the cash remains on the books and in the vaults, there is no virtuous circulation of cash and therefore no relief for the root cause of the problem, high debt servicing in a low income environment.

All the banks et al have done is add to their margin after a call, they have not adjusted the positions, just added to losing ones.

Most think that deflation is an evil to be avoided. It is a necessary method, in conjunction with debt relief, to restore the confidence and ability of a fiat monetary and fiscal system to re-set and remains viable.

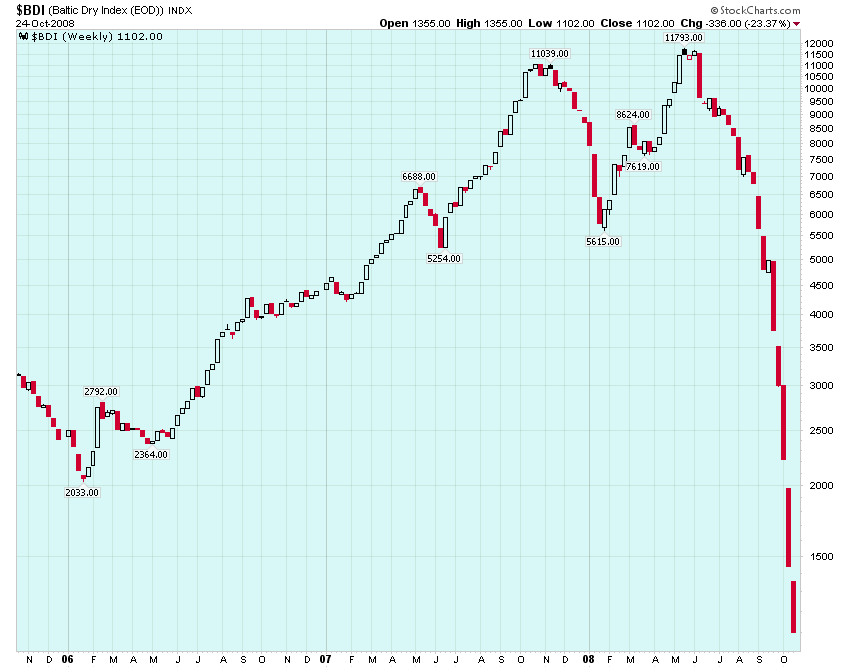

Therefore we can look for the effects of deflation, the unavailability of currency. However right now we are looking at the unavailability of the global reserve currency and its nearest competitor. Without access to the global reserve currency, the $, you either cannot trade or you have to use domestic currency to buy $'s to enable trade. In the current and future climate, very few domestic currencies will be accepted directly in exchange for goods. We already have anecdotal evidence that insurance, or lines of credit, to guarantee payment of exports upon delivery has dried up. Global trading is grinding to a halt:

(Courtesy of Stockcharts.com)

It closed at 1102, a 90% devaluation in 4 months.

Demand for shipping has collapsed and has yet to be reflected in the statistics governments and central banks use to forecast future actions. It is this that allows the minority report to have a breath of life. If mistakes are made at this juncture, if policy does not reflect the true need, then capitalism may indeed be doomed.

I expect to see many large scale bank failures as the bail outs fail. One of the lessons a wise trader takes on board is not to add to a losing position. There may be times when doubling up on a loser pays off but in the end it will go wrong and wipe out your account. Governments and Central banks have just doubled up on losing bank positions. This is not the first time they have done this and where in the past they may have got away with it, this time the position is so large, the margin so deep and the capital so expensive that the very nature of the intervention will worsen the crisis. We are seeing the trade of last resort.

We are going to see a severe slowdown in global trade in many assets and commodities. Only those companies and countries that are cash rich and able to use savings to invest in profitable enterprise will have the ability to produce and export goods. Attempting to use domestic currency to purchase imports will prove prohibitively expensive, unless you happen to be the US or Japan.

The lack of credit at sustainable borrowing rates will force a realignment of business funding. Reliance on credit has been the backbone of expansion but the global economy is now in a full nelson, screaming for submission as the cracking and popping of joints get louder.

We are going to see a protracted period of negative "growth" in nearly all corners of business. However those companies that followed sensible business strategies and continue to invest without using credit will be well placed for the future.

Banking will never be the same again. The use of depositor's funds to make investments will be heavily regulated, hopefully including rules such as equal maturity, where investments mature at the same time as deposits become released for savers. If banks can only operate using deposits then they must be fit for purpose, properly capitalised and transparent to ensure confidence is restored. We must be prepared to allow banks to fail, removing the safety net of nationalisation. That will encourage depositors to look carefully before entrusting funds, taking responsibility for their investment decisions.

Those Hedge Funds that are not in cash will be lucky to survive. With essentially the same bets in place that the defunct Investment/Broker Banks had but without the bail out facilities available to them the future looks bleak. Even if they have successfully de-leveraged the lack of returns will see a massive increase in redemptions.

The inability of many countries to import goods will lead to 2 results. Some will attempt to print more currency to purchase either $'s or $ (and yen) priced goods and we know where that will lead. Others will look inward and begin the process of rebuilding manufacturing and R&D to allow home grown substitutes to replace those imports that are no longer available.

Some countries will be better placed than others to make such a move, others will be rich in assets and poor in ability, new trading groups and partnerships will evolve. The Eurozone may not be able to survive such change; it is unlikely that the current membership of the Euro will remain in place. Weaker economies will not be able to support the requirements needed to comply with membership. Much of the Southern Mediterranean EU will be bankrupted, along with other countries in old Europe, Africa the Middle and Far East and Latin America.

I expect attempts to be made to peg smaller currencies to a $/Y basket. These 2 currencies will remain strong for the foreseeable future as long as demand for a reduced supply exists. Eventually there will a centrally controlled orchestrated move to develop regional currencies linked to a peg that is not a currency, such as the IMF SDR's (special drawing rights). The movement of currency from one region to another will be after a conversion to "SDR" and controlled by the Bank of International Settlements.

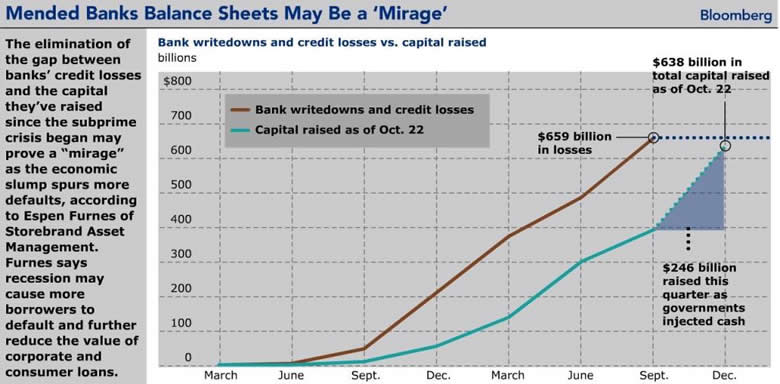

Finally in this part of What's That Coming Over The Hill is a chart from Bloomberg by Espen Furnes of Storebrand Asset Management that neatly sums up and displays why the credit crisis will morph into something much worse (I had a similar chart but not as good as this!):

(Courtesy of Bloomberg & Espen Furnes of Storebrand Asset Management)

Notice the lag in capital raised compared to losses sustained and remembering back to the summer of '07 how small the losses were compared to the damage wrought.

I haven't seen a better chart that shows why there is a need to suck wealth from the global economy to "save" the system and why the expansion of the bail out is not inflationary.

More next week.

By Mick Phoenix

www.caletters.com

An Occasional Letter in association with Livecharts.co.uk

To contact Michael or discuss the letters topic E Mail mickp@livecharts.co.uk .

Copyright © 2008 by Mick Phoenix - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Mick Phoenix Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.