The Fed Is Playing The Biggest Game Of Chicken In History

Stock-Markets / Financial Markets 2021 Sep 21, 2021 - 09:29 PM GMTBy: Avi_Gilburt

Yeah, I know everyone is so certain that inflation is what we will be battling for the foreseeable future. The main reason why many of you are so certain we are battling inflation is because you are seeing prices rise on food and other items for which you shop. But, do rising prices really mean we are dealing with the true economic definition of inflation?

To be honest, I really don’t care what you call it. It makes no difference to me since our analysis tells me when to get in and out of the market. You see, I and many others correctly recognize that the stock market leads the economy. So economic definitions have no bearing upon our forward-looking expectations regarding the stock market. And, I have explained why this is the case in past articles:

How To Analyze Market Sentiment Along With Market Fundamentals

Many have vigorously argued with me about this over the past decade during which I have been writing on Seeking Alpha. Yet, none of them have been able to tell you accurately where the market is headed, while we have been quite accurate in our stock market analysis for many years.

In fact, at the time we were bottoming at my target of 2200SPX, a commenter to one of my articles at the time challenged me and suggested that I was 100% wrong in my expectation that the bull market would carry us back to 4000SPX. And, he based his perspective on the “economy.”

He strongly exclaimed that the bull market was dead as it was deeply into bear market territory, and that it was not possible for it to take us to 4000SPX. His argument was that the economy was going to pull the market down a lot further and the 4,000 region was a lot further away than my charts ever suggested. He viewed the market as finally following the economy, from which it was supposedly long divorced according to him. He viewed this as “common sense,” and urged readers to avoid believing that my “chart magic” would take us up to 4000SPX.

Yet, those that have followed my “chart magic” for the last decade know just how well it has performed in the real world, whereas his “common sense” view has been quite misleading and wrong for some time.

Interestingly, this commenter's erroneous belief was representative of the beliefs held by most market participants in March of 2020. Yet, as I have explained, the market leads the economy. And, the market was telling me to prepare for a large stock market rally off the 2200SPX region, wherein it would lead the economy out of the doldrums. In fact, the market usually bottoms when we are seeing the worst news about the economy. This picture from Jim Cramer’s television program probably evidences this best:

Now, that we have moved beyond my minimum stock market target that I outlined in March of 2020, many of these same folks that were bearish at the market lows and missed this entire rally have now shifted into arguing about inflation. Since they were so wrong about the market, they feel the need to be right about inflation.

The funny thing is that many of them have no clue about where the market is going. Yet, they think it is much more important to know whether we have inflation or not. But, what the heck is the point of getting the appropriate economic definition correct if you are clueless about the direction of the market? Is not the point of all our research to be on the correct side of the market trend?

Consider that economists had us classified as being in a recession while the market rallied from 2200SPX to 4000SPX. And, this is exactly why the members of ElliottWaveTrader.net and The Market Pinball Wizard on Seeking Alpha thank me for pointing them in the right direction:

“I no longer read any news about "the economy" and I am much, much more profitable with my investments now.”

At the end of the day, most of these people arguing about inflation MAY win a battle if they are right about inflation, but they have lost the war since they have been bearish of the stock market for some time. But, I can assure you they will pound their chest about their inflation views. In fact, many already have begun to do so, despite their being bearish during this entire market run.

So, while we have been right about the market, allow me to present a few paragraphs to explain my views on the inflation argument. But, I want to state up front that this discussion is absolutely meaningless to my views on the market, as it has absolutely no bearing on our ability to retain on the correct side of the market. In other words, this is purely an academic exercise which is meaningless to making money in the market.

First, I want to start with an economic definition of inflation, which I wrote years ago in one of my first articles on Seeking Alpha:

“Explanation of Inflation/Deflation

I want to take a moment to define inflation and deflation one more time:

Inflation is a persistent increase in the level of consumer prices or a persistent decline in the purchasing power of money (this is the result of the cause of inflation) caused by an increase in available currency and credit beyond the proportion of available goods and services (this is the cause of inflation).

In its simplest form, inflation is caused by credit/monetary base expansion, whereas deflation is caused by credit/money base contraction. If you think about it, if everyone has more ability to buy goods because there is more money/credit available for them to do so, then the cost of the limited number of goods available must go up based upon the law of supply and demand. Of course, the opposite is true as well.

Although most people only focus on the “result”/price-side of the definition of inflation to determine if there is actual inflation, the true key to determining if inflation exists is if there exists a cause for true systemic inflation, and not simply certain sector price increases. So, the ultimate question is if there is an expansion in the money/credit supply which will put pressure on the cost of ALL goods and services, and not just selected goods and services.”

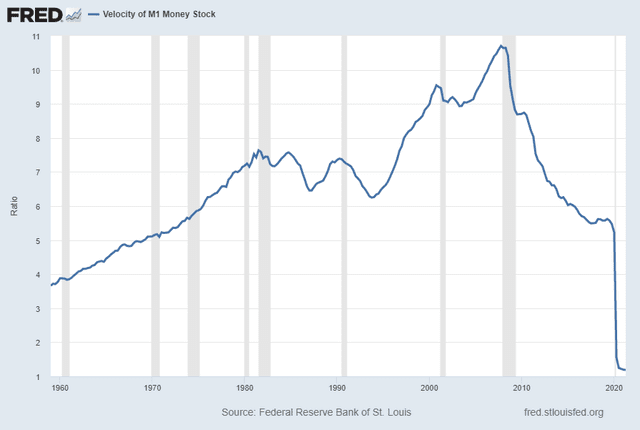

What I left out was the effect that velocity of money has upon this equation. Velocity of money is a measurement of the rate at which money is exchanged in an economy. You see, the Quantitative Easing process has increased the supply of money by making more debt available to the public. But, if there is no demand for that increase in debt available, then we will not see an increase in the velocity of money. That means that the increase of the money supply will not actually make it into the market and will, therefore, be unable to “cause” an inflationary reaction.

For those that want to have a better understanding of how the QE process works and why it only creates more available debt, feel free to read this article:

An Explanation of Quantitative Easing For The Uninformed - And Mr. Armstrong

But, again, I want to stress that the QE process only makes more debt available to the public. And, unless the public has an appetite to take on further debt, that newly available debt will not make it into the economy and will not increase the velocity of money. Therefore, we can have a rise in the money supply through the QE process, and still not have inflation, as per the economic definition outlined above.

I think that is what this chart of the velocity of money is saying even though the money supply has significantly increased over the last number of years:

Now, I know this is a very technical discussion regarding inflation. And, I am quite sure that many of you that have made purchases over the last year are certain that the rising prices you are seeing must be due to inflation.

While the result of inflation is rising prices, keep in mind the inverse is not necessarily true. There are many reasons as to why prices can rise, so rising prices do not necessarily mean we have inflation. And, again, this is based upon the pure economic definition of inflation, which I outlined above.

Again, it is entirely possible that prices can rise and we still do not have inflation. In fact, if we really had inflation, we would see a rise in prices across the entire marketplace, and not just in certain pockets of the economy. In fact, there are segments of the market which do not support the inflation argument such as copper, lumber, metals, the US Dollar, and bonds. When we take into account these segments of the marketplace, along with the lack of increase in the velocity of money, it truly weakens, if not completely destroy, the inflation argument.

Again, I am going to repeat that it is entirely possible to see rising prices and not have inflation, as per the purist economic definition. Some of the other reasons we can see a rise in prices include a supply shock, such as that which may have been created due to the Covid shutdowns.

But, what this highlights is the fact that the Fed is playing the biggest game of chicken in market history. It has been adding trillions of dollars in liquidity and available debt, yet it may still not have been able to create an inflationary result. Consider that the Covid debacle may have masked this issue, and likely has caused most market participants to look the wrong way. If not for the Covid shutdowns, we may not have seen the rise in prices we are currently experiencing. And, at the end of the day, I still believe that deflation is the Boogieman that is lurking around the corner.

Moreover, when taking all these facts together, it means that the Fed has truly been powerless to cause a rise of inflationary pressure. The reason is that we do not have a commensurate rise in willingness by the public to increase their debt holdings relative to and commensurate with the increase in debt being made available through the QE process.

So, while the Fed will undoubtedly continue to fight market declines with further QE, it likely means that the Fed will lose the game of chicken that it is playing with market participants for as long as the market has no appetite to increase its debt holdings by a commensurate degree. Resultingly, I still maintain the view that deflation will ravage the markets in the coming years once this bull market runs its course over the next two years, and the Fed will ultimately be powerless to prevent or stop it.

I want to conclude this missive with a repeat of the warning noted throughout: Arguing about inflation is an academic exercise which has no bearing on the direction of the stock market. If you want to know the direction of the stock market, following the economic definitions or labels will often mislead you and not accurately direct you. Many learned this the hard way in 2020-2021.

Fool me once, shame on you. Fool me twice, shame on me. Do not allow yourself to be fooled or shamed and do not be sucked in by the shiny object being dangled before you in the form of an inflation debate.

Avi Gilburt is a widely followed Elliott Wave analyst and founder of ElliottWaveTrader.net, a live trading room featuring his analysis on the S&P 500, precious metals, oil & USD, plus a team of analysts covering a range of other markets. He recently founded FATRADER.com, a live forum featuring some of the top fundamental analysts online today to showcase research and elevate discussion for traders & investors interested in fundamental rather than technical analysis.

© 2021 Copyright Avi Gilburt - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.