Eerily Serene Risk off Financial Markets

Stock-Markets / Financial Markets 2021 May 28, 2021 - 03:04 PM GMTBy: Monica_Kingsley

S&P 500 had a mixed day, and the credit market underlines the shift to risk-off. Halfway shift, to be precise – the high yield corporate bonds recovered the intraday downside but value sold off all the way to the closing bell. Well, rising yields used to add to tech‘s problems since mid Feb, and retreating yields don‘t breathe enough life into the sector now. It‘s clearly visible that the high beta segments are facing the yields‘ headwinds while $NYFANG is in the black, but more than a little lagging.

The Treasury market reprieve I announced on May 18 to last more than a good few weeks, is here. While it works to lift tech and hamper value, the days of value doing fine are far from over as the VTV:QQQ ratio illustrates:

(…) We‘re still in the value outperforming growth environment (reflation and reopening themes), it‘s just right now (last few days) that tech is pulling stronger ahead than value. ... Value‘s reaction to the yields trajectory ahead would be telling, and I have no doubts there is quite some more juice left in the long value trade (and that the Russell 2000 isn‘t rolling over to the downside here).

Emerging markets are welcoming the dollar woes and yields reprieve, and the Russell 2000 isn‘t too much of a drag either. VIX refused further downside yesterday, and is hedging off bets as much as the option players do – no change in prior trends here, just a move away from the complacent end of the spectrum. The stock bull run is still about dips being bought.

The key move is in the debt markets, and concerns inflation (expectations). For now, it appears that the Fed trial baloons (Kaplan, even Yellen – thinking about talking taper, suggesting rate hikes) have worked in dialing back the inflation trades to a degree (stock market correction isn‘t thus necessary for players to pile into Treasuries) – more about the Fed‘s „coming soon“ taper bluff:

(…) The market simply isn‘t convinced the Fed is serious about taking on inflation through (gradual) removal of the punch bowl – or about shaping its forward guidance credibly this way (yet). Inflation expectations are cooling down a little, and the Treasury market is tracking them closely. But this doesn‘t mean that bonds are taking the central bank seriously – this move is part and parcel of the transitory vs. getting (practically permanently unless a Fed game changer arrives – still unlikely) elevated inflation readings debate.

While I think that the red hot CPI inflation would die down a little (i.e. not keep rising ever as steeply as was the case with Wednesday‘s data) once the year on year base to compare it against normalizes, a permanently elevated plateau of high and rising inflation would be a reality for more than foreseeable future simply because the Fed would be as behind as Arthur Burns was in fighting the 1970s inflation, and upward price pressures in the job market pressures would kick in.

The much awaited Jun 10 CPI readings would likely come on the hotter side of the spectrum, but would be part and parcel of a continued move to a higher inflation environment where commodities‘ pressures are amplified by job market ones – not that the distortions and disincentives to work wouldn‘t be there.

Gold and silver are set to benefit, either way you look at it. Be it through the Fed or market‘s perceptions of the Fed (i.e. buying into its bluff), nominal rates are retreating while real rates remain very constructive for continued precious metals run. The only short-term warning sign comes from miners that aren‘t surging higher. Open gold and silver profits can keep growing at their own pace but I wouldn‘t be surprised by a brief setback first either:

(…) The charts and macroeconomics speak in favor of continued bullish consolidation before a spurt higher in all three assets. And as the Fed isn‘t perceived in the least as about to get tough(er) (whatever that means, cynics would say), the path of least resistance remains up as the copper to 10-year yield ratio confirms. No, not too much cream has come off in commodities.

Crude oil traded with little volatility yesterday, but the bulls are a little short-term exposed as the oil index ($XOI) shows. Downswing attempt, however modest, shouldn‘t be surprising.

Bitcoin and Ethereum are recovering in fits and starts, and the picture is turning bullish especially for the latter. With Bitcoin, the upper border of the $38,000 - $40,000 zone hasn‘t been cleared yet, but the signs from both Ethereum and Cardano are bullish already. It surely seems the market doesn‘t want to crash some more right now as the rally hasn‘t run out of steam yet.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

S&P 500 Outlook

S&P 500 wavered a little yesterday, with signs pointing to more significant overnight deterioration not materializing. Nasdaq 100 is likewise probably going to consolidate its gains next – unless the value trade kicks in again, disregarding the yields‘ growing calm.

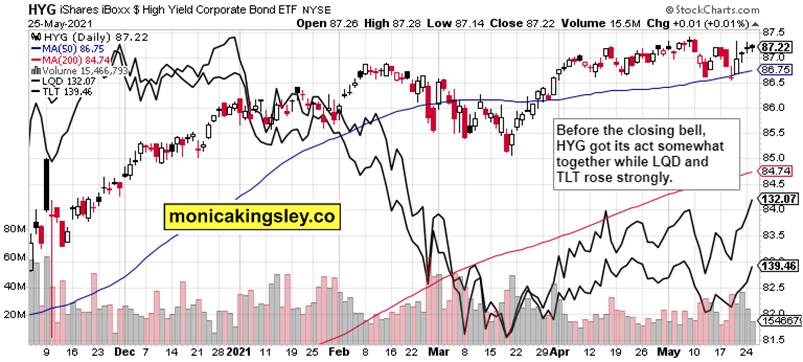

Credit Markets

- The debt markets recovery is on, and I am looking at high yield corporate bonds for clues as to the S&P 500 upswing veracity.

Technology and Value

Tech was driven just by $NYFANG yesterday, pointing to the strong risk-off nature of yesterday‘s session.

Inflation Expectations

Bond yields and inflation expectations are turning down relatively sharply, continuing to track each other closely. It certainly looks like we‘re in for a calm summer (my prior words).

Gold, Silver and Miners

Gold and silver rising while miners keep lagging behind, isn‘t a truly bullish sign. Wait and see is the right course of action as there hasn‘t been any reversal (let alone attempt at it), protecting sizable open profits.

The weekly perspective offers mixed view of miners to gold ratio‘s breather while the copper to 10-year yield isn‘t budging – yet (see above what I wrote about taking the cream off commodities).

Crude Oil

Black gold is a little extended here, and consolidation of recent sharp gains is the most likely outcome, the oil index says so too.

Summary

Yesterday‘s S&P 500 posture deterioration is likely to remain temporary unless the credit markets move down, taking Nasdaq 100 with them. Muddle through seems most likely for today.

Gold and silver upswing would be on sounder footing when the miners decide to join, and do away with the stark non-confirmation.

Crude oil has reached the top of its recent range, expecially when the oil sector is considered – an opportunity after readjustment to no Iranian sanction news, is in the making.

Bitcoin and Ethereum are likely to continue their recovery, overcoming the key resistance zone in the first, and reasserting upside momentum in the latter (the overnight price action has been very positive).

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for both Stock Trading Signals and Gold Trading Signals.

Thank you,

Monica Kingsley

Stock Trading Signals

Gold Trading Signals

www.monicakingsley.co

mk@monicakingsley.co

* * * * *

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.