US Dollar Doomed as Credit Crisis Turning into a Currency Crisis

Currencies / US Dollar Oct 03, 2008 - 02:18 PM GMTBy: Jennifer_Barry

When the precious metals were smashed out of nowhere and the dollar started climbing this summer I became very worried. I didn't question my conviction that commodities are in a bull market, or that precious metals in particular are undervalued. I felt something sinister was at work. Neither move was justified on a fundamental level. I assumed that something very bad was about to happen and the metals needed to be brought lower in advance of the bad news.

When the precious metals were smashed out of nowhere and the dollar started climbing this summer I became very worried. I didn't question my conviction that commodities are in a bull market, or that precious metals in particular are undervalued. I felt something sinister was at work. Neither move was justified on a fundamental level. I assumed that something very bad was about to happen and the metals needed to be brought lower in advance of the bad news.

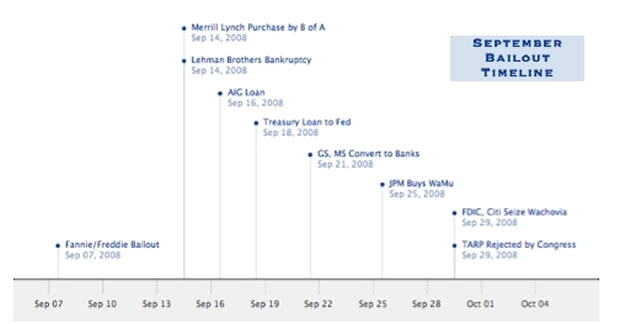

Now we have a glimpse at the ugly consequences foreseen by the Treasury Department and the Federal Reserve. In early September, Fannie Mae and Freddie Mac were nationalized with a financial commitment of USD$200 billion from the taxpayers. Incredibly, the loan limits at the former GSEs were raised from $417,000 to $729,750 in March when it was more than obvious these institutions needed to be reined in. Like most bailouts and bank failures, this one was announced on a weekend to limit the impact on the stock markets.

As I mentioned in last month's issue, Treasury Secretary Paulson was under severe pressure to act, as the Chinese started selling Fannie and Freddie bonds while threatening further retribution. Common shareholders were left with nothing, while bondholders like Pimco and Asian central banks benefited. The small investor was stung again, as taxpayer dollars were used to bail out foreigners and wealthy Americans in a policy that Jim Rogers terms “socialism for the rich.”

Unfortunately, $200 billion is just the tip of the iceberg. As the government has assumed responsibility for Fannie and Freddie's $5.4 trillion in liabilities, the Congressional Budget Office correctly states that these institutions “should be directly incorporated into the federal budget.” The Bush Administration has strongly opposed this move.

Many commentators claim that the former GSE's liabilities are not like usual government debt, as the mortgages are backed by homes. However, Catherine Austin Fitts indicates that many of the Fannie, Freddie and FHA loans are actually fraudulent, as the same property is sold repeatedly to phantom buyers or the property does not actually exist. At least $1 trillion of Fannie and Freddie's mortgages are already in trouble, and the data on mortgage resets indicates the problem will not end until 2012. This bailout effectively doubled America's publicly traded debt overnight.

On September 14, the Fannie and Freddie bombshell was followed by the sale of Merrill Lynch to Bank of America for $50 billion. Paulson admitted he was involved with the Merrill Lynch purchase at a steep premium to the market price. Bank of America is hardly a bastion of stability however, as over half its builders loans “are considered troubled.” The institution is a leading issuer of consumer credit cards, and with the U.S. in a recession, much of this debt will default. Bank of America already bought subprime lender Countrywide earlier this year in a curious deal where the firm refused to take on many of Countrywide's liabilities.

On the same day, the 158-year-old Lehman Brothers declared bankruptcy. After guaranteeing JPMorgan Chase's purchase of Bear Stearns in March and taking over the mortgage giants, the U.S. Government sternly insisted that Lehman should be allowed to fail. Not only did this bankruptcy spook the markets and cast doubt on the solvency of other investment banks like Goldman Sachs, but it opened up the Pandora's Box of counterparty risk. Holders of swaps and other derivatives who had won bets with Lehman could no longer collect, and these contracts reverted to their intrinsic value - zero. Investors in Lehman's stocks and bonds were wiped out as well, and institutions had new losses on their balance sheets that needed to be written off. Highly leveraged banks were unable to meet their derivative obligations, so they became insolvent. Fearing contagion, financial institutions sharply raised Libor rates and other measures of interbank lending as they lost faith in their peers' ability to repay loans, and credit began to freeze up.

After viewing the debacle caused by Lehman's failure, Paulson and Bernanke decided it was too risky to let another derivatives-laden firm go under. This time it wasn't even a bank they felt compelled to bail out. AIG was rescued due to its large size and involvement in all kinds of international markets, with the bulk of its business in reinsurance (insuring other insurers). Not surprisingly, the $85 billion loan to AIG prevented a $20 billion loss to Paulson's old firm, Goldman Sachs.

AIG's involvement in derivatives is consistent with their history of questionable behavior. The giant insurer had a pre- eminent role in precious metals trading, and was suspected to be one of the large silver shorts before its abrupt departure from the market in 2004. In 2005, then-CEO Maurice Greenberg was forced to resign over an accounting scandal that involved $1.7 billion in fraud. Curiously, no criminal charges were filed unlike a similar situation at Enron.

AIG was just one of many bailouts as this month just kept getting worse. A few days later, three money market funds administered by Reserve Management Corporation “broke the buck” due to investments in Lehman. Although money market funds had a reputation as an extremely safe investment, clients lost part of their principal and were unable to redeem their funds for a week. Not reassured by government officials or fund managers, consumers began fleeing the $3.4 trillion market. To prevent a full-blown panic, the U.S. Treasury decided to insure the funds for up to $50 billion for current investors.

On September 18, the Treasury announced it would issue $100 billion in new debt to replenish the Federal Reserve's balance sheet. The Fed needed the boost after “Helicopter Ben” dumped a huge load of dollars into the economy through unconventional means. In retrospect, this must have been preparation for the expansion of credit through the discount window. Borrowing by primary dealers and commercial banks exploded last week, doubling to over $262 billion.

I doubt it's a coincidence that on September 21, the Federal Reserve allowed Goldman Sachs and Morgan Stanley to convert to bank holding companies, easing the standards for collateral pledged in return for loans. Not only will these converted firms be able increase their liquidity on very favorable terms, they can court federally insured customer deposits for the first time.

In August, I published a chart of Washington Mutual, and predicted its imminent failure. WaMu was seized by the FDIC on September 25, and has filed for bankruptcy. The majority of branches and assets were sold to JPMorgan Chase. However, the bank refused to acquire WaMu's liabilities, leaving shareholders and bondholders out in the cold. The new CEO of WaMu, Alan Fishman received $20 million for less than three weeks of work. It's unknown what the burden on the U.S. tax base will be.

The bailouts continued this week, as the U.S. Senate passed a bill on September 28 awarding $25 billion in subsidized loans to automakers. The car companies will not have to make payments for five years. That was a modest giveaway compared to the FDIC's involvement in the Wachovia sale the following day. Citigroup took over the struggling Wachovia Bank, agreeing to absorb the first $42 billion in losses with the FDIC assuming the remainder. Fed chief Bernanke approved the FDIC's involvement, stating it will help stabilize the markets. In exchange for $12 billion in preferred shares and warrants in Citigroup, the FDIC became liable for losses up to $270 billion. As I predicted, the FDIC is running short of funds to repay depositors in failing banks and may need to borrow tax dollars from the Treasury.

Not surprisingly, the ever larger bailout packages proposed by the Bush Administration have created heavy backlash from the American public. While many citizens are losing their jobs and their homes, financial executives like John Thain receive multi-million dollar paydays as a reward for their spectacular failures. Although most media outlets neglected to report it, hundreds of protestors on Wall Street demonstrated against the bailouts last week, many holding signs reading “Jump!”

Despite fear-mongering by President Bush, the last scheme proposed was too much for Americans to bear. In the Troubled Asset Relief Program bill (TARP), Paulson effectively asked to be the financial dictator of the U.S. The Treasury Secretary insisted that he needed $700 billion to buy whatever toxic assets he chose, without oversight or input from any court or administrative agency. This bill was rejected by the House of Representatives this week under heavy pressure from angry constituents. However, a revamped bill with added sweeteners looks likely to pass soon.

Since Congress was not very cooperative, the Federal Reserve added $330 billion in bank swaps with foreign central banks to boost the availability of dollars worldwide. Bernanke also expanded the Term Auction Facility (TAF) by $300 billion for a new total of $450 billion. The TAF has even looser standards than the discount window which was was supposed to be the lender of last resort, but the TAF charges a premium to market rates. The Fed had already eased its lax standards on September 14, accepting a wider range of collateral for loans. So even as the Congress was rejecting a $700 billion bailout, the Fed was quietly conducting its own $630 billion bailout.

After the House rejected the TARP proposal on September 29, Paulson, Bernanke, and the rest of the Plunge Protection Team had to make their predictions of dire consequences look correct. They allowed the Dow to crash 777 points - a new record - while gold soared. However, the PPT is afraid of causing too much panic among the public, so they orchestrated a rally the following day. The dollar surged 1.58, and the precious metals were stomped to force investors out of hard assets into Treasuries and other paper.

This essay was one of the most difficult I have ever written as the situation was so dynamic. It seemed that no sooner did I explain a Bernanke statement or a Paulson tactic than my writing became out of date, and a fresh crisis would sweep the old one off the front pages. I believe that the speed of the bailouts indicates desperation in Washington. The Bush Administration is no longer able to plan far ahead, but must react to swiftly changing market conditions.

Despite Bernanke's assurances to the contrary, these bailouts mean tremendous inflation of the money supply. The U.S. can no longer avoid hyperinflation - it is here. The effects can hardly be overstated when the reserve currency of the world is debased so rapidly. Empires disintegrate and social upheaval occurs. Dollar depreciation is not apparent to the masses yet, but once the realization occurs, the social effect will be explosive. I believe this is why a U.S. Army brigade from the 3rd Infantry Division has been given orders to patrol America “to help with civil unrest and crowd control.

The dollar is doomed but most people don't know it yet. I recently spoke with a friend who was born in Mexico, and he agreed that the American public cannot imagine their currency failing. While U.S. citizens think that a currency crisis is the end of the world, Mexicans have experienced this multiple times. The central bank lops a few zeros off the currency and it's given a new name. The smart people have moved their wealth into a different form long before that happens. Even if Jim Sinclair is correct and the U.S. Dollar is rescued by linking it to gold in a Federal Reserve Gold Certificate Total Value Ratio, it will not be the same dollar we know today.

Americans will soon learn to change their mindset from focusing on their return on capital, to worrying about conserving the capital they have left. We have seen the beginning of this paradigm shift in the run on banks, and the flight to Treasury instruments. Investors need to insure their portfolio is full of precious metals and other commodity-related assets. While hard assets have suffered lately, that will inevitably change as mistrust spreads throughout the financial system. If you position yourself appropriately, your wealth can not only survive the currency crisis but also secure your future.

by Jennifer Barry

Global Asset Strategist

http://www.globalassetstrategist.com

Copyright 2008 Jennifer Barry

Hello, I'm Jennifer Barry and I want to help you not only preserve your wealth, but add to your nest egg. How can I do this? I investigate the financial universe for undervalued assets you can invest in. Then I write about them in my monthly newsletter, Global Asset Strategist.

Disclaimer: Precious metals, commodity stocks, futures, and associated investments can be very volatile. Prices may rise and fall quickly and unpredictably. It may take months or years to see a significant profit. The owners and employees of Global Asset Strategist own some or all of the investments profiled in the newsletter, and will benefit from a price increase. We will disclose our ownership position when we recommend an asset and if we sell any investments previously recommended. We don't receive any compensation from companies for profiling any stock. Information published on this website and/or in the newsletter comes from sources thought to be reliable. This information may not be complete or correct. Global Asset Strategist does not employ licensed financial advisors, and does not give investment advice. Suggestions to buy or sell any asset listed are based on the opinions of Jennifer Barry only. Please conduct your own research before making any purchases, and don't spend more than you can afford. We recommend that you consult a trusted financial advisor who understands your individual situation before committing any capital.

Jennifer Barry Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.