Cameco Crash, Uranium Sector Won’t Catch a break

Commodities / Uranium Sep 16, 2019 - 05:15 PM GMTBy: Richard_Mills

One week ago Cameco announced it will maintain low output levels until uranium prices recover. The Canadian uranium miner also said it might cut production further, having already closed four mines in Canada and laid off 2,000 of its workers in the uranium mining hub of Saskatchewan.

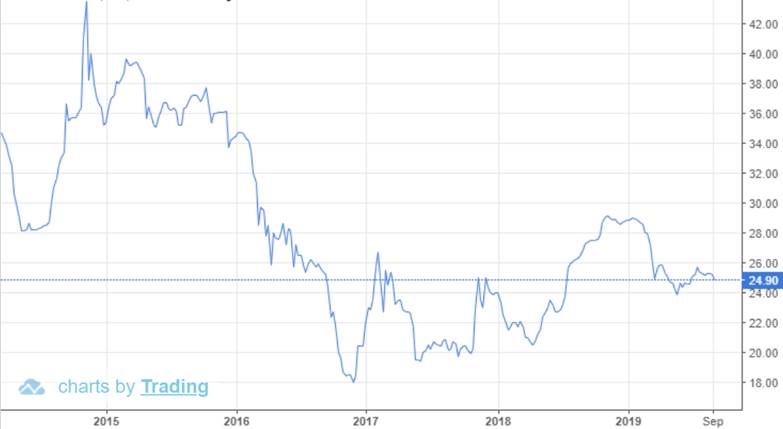

Cameco share price

News like this has stalked the uranium market for years, and while 2018 was a great year for the nuclear fuel, hope for a price pick-up is dim; once an important commodity at resource investing shows, uranium is now mostly ignored. Uranium bulls are as rare as white unicorns, having switched allegiance to metals that support Ahead of the Herd’s electrification of the transportation system thesis, like lithium, nickel and cobalt.

Fortunately, there is a way to be both a supporter of nuclear energy - still one of the safest and most efficient means of baseload power generation - and ditch uranium, which is quickly becoming a dinosaur of a commodity we think best left alone. We’ve been banging the drums of thorium-based nuclear reactors for awhile. In this article we present thorium’s case viz a viz a sick and dying uranium market.

No end to supply glut

“We are not restarting mines until we see a better market and we may close more capacity, although no decision has been taken yet,” Cameco CEO Tim Gitzel told Reuters recently at the World Nuclear Association’s annual conference.

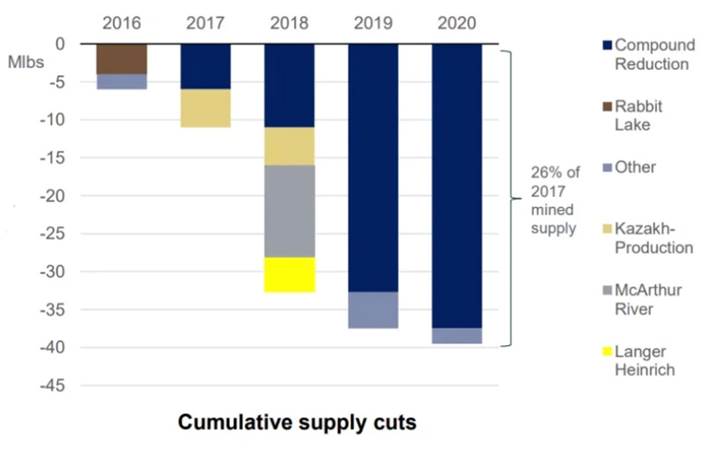

Just over a year ago Cameco made the difficult decision to close its MacArthur River and Key Lake mines, in response to low uranium prices, leaving the company’s flagship Cigar Lake facility as its only operating mine left in northern Saskatchewan, home to the world’s highest grade uranium deposit.

The mine closures by Cameco were preceded by 20% production cuts in Kazakhstan, the number one uranium-producing country. The former Soviet bloc country has said 2020-21 output will not rise above 2019 levels. In Canada, the second largest U producer, 2018 production was cut in half to 7,000 tonnes.

An estimated 35% of uranium supply has been stripped from the market since Kazakhstan’s supply reductions in December 2017.

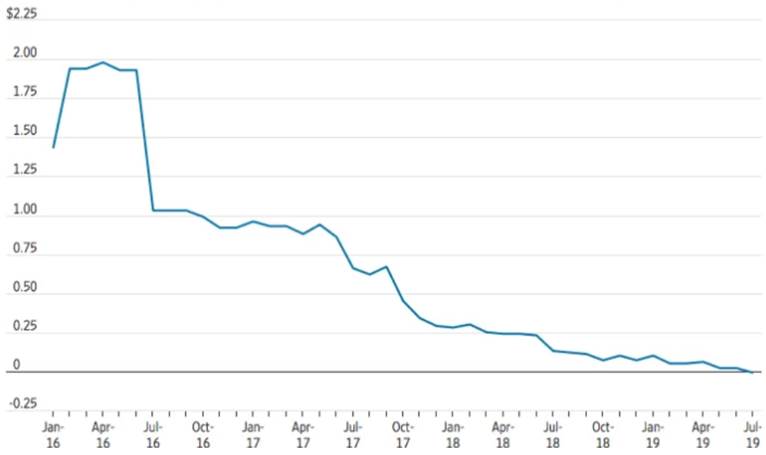

Uranium spot price

While the mine closures kicked up the price of uranium in 2018, they haven’t been enough to build momentum. Spot uranium finished last year up just over 20%. Year to date 2019, triuranium octoxide, or U3O8, is down a disappointing 11.9%, trading at $25.10 per pound, as of Sept. 11.

The downward spiral of production and prices can be blamed on a supply glut. When uranium crashed after the 2011 nuclear meltdown at Fukushima, Japan, producers thought they could weather the storm by producing more to compensate for lower prices. The unsurprising result was to create a supply glut that pushed spot to a record low of $17.75 a pound on Nov. 28, 2016. By 2018 the price had recovered to around $20, but that meant around 95% of producers were operating at a loss. Uranium miners were left with a grim choice: go bankrupt, or significantly cut production, until prices return to a profitable level. And so we wait.

According to the World Nuclear Association Kazakhstan’s uranium production went from 5,000mt in 2006 to over 24,000mt in 2016. That country is now the leading low-cost producer. Renowned investor Marin Katusa believes uranium will stay low because the world’s largest uranium producer, Kazatomprom, will continue to produce at high levels - the Russians and Kazakhs plan to position themselves as the dominant source of uranium over the next 20 years.

Uranium demand and China

In response to the supply glut/ low price argument, uranium bulls like to present China as the country that will save the day and float everyone’s long-sunken uranium stock boats. It’s true that, of 453 operating nuclear reactors and 55 new reactors under construction, globally, China has the most reactors in the pipeline including 43 operating, 15 under construction and 179 planned or proposed.

China then, will demand millions of tonnes of yellowcake, that it will have to import, right, pushing up the price? In fact, China has been working to reduce its dependence on imported uranium, and fossil-fueled power generation, by developing domestic uranium deposits and either partnering with or buying mine properties overseas. The Asian superpower has started building its own uranium supply chain, such as starting the Husab mine in Namibia. In November 2018, China National Uranium Corp bought the Rossing mine in Namibia from Rio Tinto.

According to the World Nuclear Association, China has become self-sufficient in most aspects of the nuclear fuel cycle: China aims to produce one-third of its uranium domestically, obtain one-third through foreign equity in mines and joint ventures overseas, and to purchase one-third on the open market.

The China Nuclear International Uranium Corporation (SinoU) set up the Azelik mine in Niger and has agreed to buy a 25% stake in Paladin’s Langer Heinrich mine in Namibia for $190 million. In 2007 SinoU bought a share in the Zhalpak mine in Kazakhstan, through a joint venture with Kazatomprom.

Prospects in Kazakhstan, Uzbekistan, Mongolia, Namibia, Algeria and Zimbabwe, Canada and South Africa are also seen as potential suppliers for SinoU, writes WNA.

In other words, China is well on its way to figuring out how it will supply uranium to all the new nuclear reactors it plans to build; it probably doesn’t need the West to discover new uranium deposits and ink more offtake agreements.

Another expert body, the Nuclear Energy Agency, states that an expected increase in demand for U3O8 needed for competitively priced baseload electricity derived from nuclear power plants, particularly in developing countries, will adequately be met by current uranium supplies.

In a bi-annual report known as the ‘Red Book’, the NEA points to the public’s fear of nuclear power post-Fukushima, and low-cost natural gas, as the two main factors that have dampened the prospects for growth in nuclear generating capacity, and are likely to keep uranium prices depressed:

[T]he Fukushima Daiichi accident has eroded public confidence in nuclear power in some countries, and prospects for growth in nuclear generating capacity are thus being reduced and are subject to even greater uncertainty than usual. In addition, the abundance of low-cost natural gas in North America and the risk-averse investment climate have reduced the competitiveness of nuclear power plants in liberalized electricity markets…

“The currently defined resource base [6.1 million tonnes of recoverable insitu uranium] is more than adequate to meet high case uranium demand through 2035, but doing so will depend upon timely investments to turn resources into refined uranium ready for nuclear fuel production. Challenges remain in the global uranium market with high levels of oversupply and inventories, resulting in continuing pricing pressures.

Nuclear demand shrinking

Of course the entire investment case for uranium is anchored on the idea of healthy demand for nuclear power especially as the world moves off fossil-fueled power generation to cleaner forms of power like hydro-electric and renewables.

A key piece of that argument has been Japan re-starting its nuclear reactors that were shut down for safety checks and refurbishment following Fukushima. Before the 2011 earthquake and tsunami caused three reactors at Tokyo Electric Power’s Fukushima plant to overheat, Japan was the world’s third largest consumer of nuclear power, behind the US and France, operating 54 nuclear reactors.

Eight years later, only nine of 33 remaining reactors have been re-started, and Japan’s nuclear operators are reportedly starting to sell their uranium fuel, as the chances fade of more reactors coming online, and adding to the six currently operating. Long-term contracts are also being canceled.

In another blow to the industry, Japan’s new environment minister, Shinjiro Koizumi, has said he wants all reactors shuttered to avoid a repeat of the Fukushima catastrophe that leaked radiation and forced 160,000 people to flee the area, many of whom have not returned.

As reactors close in the United States, Germany, Belgium and other countries, “traders and specialists say the market is likely to remain depressed for years,” Reuters reported in August.

Germany has pledged to shut down all its reactors by 2022 and the Belgian government has agreed to a new energy pact that will see nuclear power phased out over the next seven years. Germany currently gets nearly half (47%) of its energy from renewable sources, although 30% is generated from coal - needed to replace the gap in the energy grid left by nuclear power plant closures.

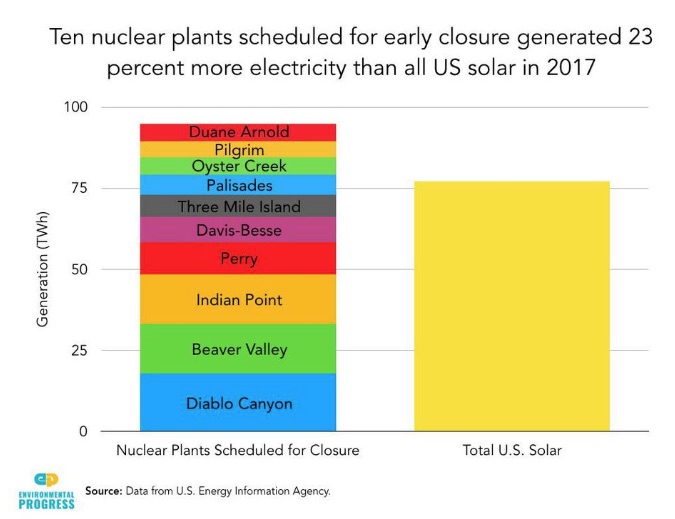

When the Duane Arnold nuclear plant in Iowa shuts down in 2020, and assuming other planned closures occur, it will mean 10 less reactors in the United States - from 99 to 89 - by 2025. To put that into perspective, the energy lost from those 10 reactors amounts to 23% more than all the solar electricity generated by the United States in 2017.

Uranium/ nuclear consequences

Nobody needs to warn the Japanese about the potentially deadly impacts of uranium-fueled nuclear reactors if something goes wrong. Nor the good people of Chernobyl, Russia, many of whom are suffering the long-term effects of radiation exposure.

Russians were reminded in August of what can happen, after a failed missile test resulted in an explosion that killed five scientists. The scientists were reportedly working on a small-scale nuclear reactor, located on an oil platform in Russia’s White Sea near the Arctic Circle, when the blast occurred.

While “only” 31 people were directly killed in 1986 at Chernobyl, the United Nations predicts another 4,000 could eventually die from diseases such as thyroid cancer linked to radiation exposure.

The Guardian reports there was in fact an epidemic of thyroid cancer after Chernobyl, while in Japan following Fukushima, children screened for radioactive iodine were found to have been exposed to dangerous levels of radiation:

An initial ultrasound survey of thyroid glands two years after the accident – well before any cases of thyroid cancer from radiation would be expected to show up – found large numbers of cysts and nodules on thyroid glands. There were 113 cases of thyroid cancer, compared with the four that doctors would expect to diagnose in a normal population of the same size without screening.

Nuclear accidents not only hurt people, but the environment.

After Fukushima, millions, perhaps billions, of tonnes of radioactive water - generated in a process to cool melted nuclear fuel at the three damaged reactors - flowed into the Pacific Ocean, putting fisheries and other marine life at risk.

The utility in charge of the complex, Tokyo Electric Power Company Holdings, tried to block contaminated water from entering the ocean, by building an underground ice wall. However, the wall has only managed to reduce the flow of groundwater from about 500 tonnes a day to about 100 tpd.

Last year, a study found that radioactive water continued to flow into the ocean at a rate of about 2 billion becquerels a day. While that sounds bad, it is in fact a dramatic improvement from 2013, when 30 billion bequerels a day leaked cesium 137, a radioactive isotope.

A rate of 0.02 bequerels per liter of seawater, considered safe for the local fishing industry, was measured in samples collected from a coastal town 8 km from the Fukushima No. 1 plant, Japan Times reported.

But the plant continues to have problems dealing with contaminated water. The Guardian reported on Thursday that Tokyo Electric Power will have to dump a huge amount of contaminated water that has been accumulating, into the ocean.

Over a million tonnes is being stored in close to 1,000 tanks but the utility has warned it will run out of space by 2022. According to one study, it could take 17 years to safely discharge the water, after it has been sufficiently diluted.

The case for thorium

Fukushima has soured the world on nuclear, and started scientists looking more closely at thorium as a “greener” alternative. Some scientists believe thorium is key to developing a new version of cleaner, safer nuclear power.

While conventional nuclear power plants are only able to extract 3-5% of the energy in uranium fuel rods, in molten salt reactors (MSR) favored by thorium proponents, nearly all the fuel is consumed. Where radioactive waste from uranium-based reactors lasts up to 10,000 years, residues from the thorium reaction will become inert within 500.

A key advantage of MSRs is the reactor cannot melt down, as we saw in Japan’s Fukushima when electric pumps were inundated by the tsunami, failing to cool the fuel rods, which overheated and caused radiation emissions. MSRs can also be made cheaper and smaller than conventional reactors, since they do not have large pressurized containment tanks, meaning they could be used in factory settings.

Where radioactive waste from uranium-based reactors lasts up to 10,000 years, residues from the thorium reaction will become inert within 500. Nuclear waste (ie. plutonium) from uranium fueled reactors can be recycled to recover the fissile materials needed to create the nuclear reaction. In this way, thorium reactors not only generate less waste than conventional reactors, but also help to rectify the nuclear waste disposal problem.

Importantly, because plutonium is not created as a waste product in a thorium reactor, it cannot be separated from the waste and used to make nuclear weapons.

The portability of MSRs is another major advantage over the capital-intensive, permanent nuclear power plants we currently have.

To learn about the fascinating history of thorium and its potential for nuclear power generation, read Uranium’s ugly stepsister

Other than the fact that uranium is better than thorium in building nuclear weapons, how do the two nuclear fuels stack up against one another? According to the Royal Society of Chemistry, thorium’s benefits include:

- Thorium is three to four times more abundant than uranium. There is estimated to be enough thorium on the planet to last 10,000 years.

- Thorium is more easily extracted than uranium.

- Liquid fluoride thorium reactors (LFTR) - a type of molten salt reactor - have very little waste compared with reactors powered by uranium.

- It is more efficient. One tonne of thorium delivers the same amount of energy as 250 tonnes of uranium.

- LFTRs run at atmospheric pressure instead of 150 to 160 times atmospheric pressure currently needed for water cooled reactors.

- Thorium is less radioactive than uranium.

As far as disadvantages, thorium takes extremely high temperatures to produce nuclear fuel (550 degrees higher than uranium dioxide), meaning thorium dioxide is expensive to make. Second, irradiated thorium is dangerously radioactive in the short-term.

Detractors also say the thorium fuel cycle is less advanced than uranium-plutonium and could take decades to perfect; by that time, renewable energies could make the cost of thorium reactors cost-prohibitive. The International Nuclear Agency predicts that the thorium cycle won’t be commercially viable while uranium is still readily available.

Arguably though, the technology exists, so why not develop it?

Examples of companies and countries that are testing thorium’s viability as a nuclear fuel keep growing. In 2017 a Dutch nuclear institute started experimenting with MSRs. NRG, the name of the facility, on the North Sea coast of the Netherlands, launched the Salt Irradiation Experiment in collaboration with the EU. New Scientist reports the researchers will use thorium as the nuclear fuel for the reactor where both the reactor fuel and the coolant are a mixture of molten salt. The experiment will also examine how to deal with the nuclear waste.

In Norway, Thor Energy started producing power from thorium at its Halden test reactor in 2013, with help from Westinghouse. The third phase of a five-year thorium trial operation got underway in 2018.

India’s thorium program is well advanced. The country envisions meeting 30% of its electricity demands through thorium-based reactors by 2050. With large quantities of thorium and little uranium, India wants to use thorium for large-scale energy production. It plans to construct and commission a fleet of 500 sodium-cooled fast reactors - which burn spent uranium and plutonium - in order to breed plutonium to be used in its advanced heavy water reactors that employ thorium as the nuclear fuel.

Indonesia, which has a large amount of thorium contained within monazite, signed an agreement with US company ThorCon Power, to develop molten salt reactors. A 1,000-megawatt thorium-based reactor would be used for base-load power and produce 5 gigawatts a year. The country wants around 20% of its energy mix to come from thorium molten salt reactors by 2050.

In the United States, the Department of Energy is partnering with TerraPower, Vanderbilt and the Oak Ridge National Lab, among others, to build a molten chloride fast reactor - a type of MSR - Oilprice.com reported. Southern Company in 2016 was the second firm to receive a grant from the DOE.

China, seemingly always on the leading edge of new energy, has put aside US$3.3 billion to build two molten salt reactors in the Gobi Desert, to be up and running by 2020, the South China Morning Post said. The reactors could spawn new uses for the radioactive element, including applications in warships and drones.

Closer to home, the New Brunswick government has committed $10 million towards building a “nuclear research cluster” that includes a demonstration Stable Salt Reactor - Wasteburner (an SSR-W is suitable for grid-scale power, between 300 megawatts and 3GW) to be powered by spent uranium. SSRs can also use thorium as the nuclear fuel. A full-sized SSR-W is planned for 2030.

Think about British Columbia’s energy needs. Instead of meeting them with the Site C dam, which comes with its own environmental problems - flooding a 100-km stretch of the Peace River Valley - how about deploying thorium reactors?

The Site C dam is slated to provide 1,100 megawatts of capacity - enough to power half a million homes.

New Brunswick’s planned SSR and BC’s Site C are of equivalent size; $10.7B Site C has a design capacity of 1.1GW compared to 1GW for the $2B SSR.

The levelized cost of energy (the price a power station must receive over its lifetime to break even) of an SSR is one third the cost of coal, natural gas and conventional nuclear power - $45 a megawatt-hour.

That means New Brunswick’s plan for future emissions-free, green power is 80% cheaper, in terms of capital costs, than BC’s Site C hydroelectric dam, and 87.5% the cost of Site C plus LNG Canada tax breaks.

So not only does BC’s wrong-headed energy strategy cost taxpayers eight times as much as New Brunswick’s, it is also a lot worse for the environment. When will the people of BC wake up and see what a colossal mistake the province is making in embracing liquefied natural gas, with its fugitive methane emissions and the continuation of fracking BC’s northeast where hundreds of natural gas well will be drilled and fracked to supply BC’s growing LNG industry, wasting and poisoning our fresh water, causing earthquakes, releasing cancer-causing benzene into the water supply, and setting up a massive increase in tanker traffic, the effects of which will result in the disappearance of already endangered killer whales?

For more on the devastating impacts of LNG and natural gas, read The real price of LNG

Conclusion

This article has focused on the drawbacks of uranium and the futility of investing in uranium companies, at least for the foreseeable future. At Ahead of the Herd, we know energy markets inside and out, and we just don’t see an upside in uranium.

Yes, as the world transitions from fossil fuels to clean energy, nuclear will have to be in the mix of alternatives, along with hydro-electric and renewables ie. solar and wind. But that doesn’t mean we are tied to uranium. Thorium is a safer, more efficient and far more cost-efficient means of achieving the same amount of power as a hydro-electric dam - as in the Site C vs SSR example above - or a conventional water-cooled uranium-fed nuclear reactor.

China will remain a big source of uranium demand, but the market for U3O8 continues to languish as Western countries turn away from nuclear.

At Ahead of the Herd, we see thorium playing a critical role in the inevitable shift from fossil-fueled to clean (including nuclear) power generation. Electricity generated from thorium could also help to meet the extra power loads on electricity grids, expected to be demanded by the huge increase in electric vehicles, all needing to be regularly plugged in.

We see two markets for EVs during this transition. The first is fully-electrics for urban environments, maybe plug-in hybrids for drivers with longer commutes, and the second is full hybrids for longer journeys and commutes that don’t need to depend on battery-only power or charging infrastructure.

If the future is EVs, the near future is hybrids. Even a significant penetration of hybrid vehicles into urban markets would be a great start. As drivers get more comfortable with battery power, and technology advances, we predict a gradual shift from hybrids and plug-in hybrids to battery EVs.

With hybrids as the bridge, we also see a path forward to helping stop the advance of the global warming shadow. At the same time, switching from uranium to thorium is a way to bring badly needed trust back to the nuclear industry, at much lower capital expenditures and shorter time frames than it takes to build conventional, uranium-based nuclear facilities.

“In the 1980s there was a new nuclear reactor commissioned every 2½ weeks, on average. Today there are just 53 under construction world-wide, nearly all in Asia, according to the WNA, and many of the world’s 448 existing plants face decommissioning.” Wall Street Journal

Uranium’s story is not one of a shortage of supply. Rather the narrative is despite all the primary/ secondary supply cuts the spot price only went up 20% in 2018, has given back half of that in 2019 and the price is still going down. As discussed above there are too many negatives at play.

Perhaps it’s time to ditch uranium, along with a large chunk of our fossil fuel use, and go with thorium?

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2019 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.