Finding Record Investor Profits Hidden In The Fed Minutes

Interest-Rates / US Federal Reserve Bank Jun 01, 2019 - 02:29 PM GMTBy: Dan_Amerman

Sifting through the minutes of the Federal Open Market Committee (FOMC) to look for signals of changes in policy is a fixation for the financial media and the investment industry. Because both the stock and bond markets can reverse directions based upon the Fed's intentions for the direction of Fed Funds rates, there is an intense focus on finding signals for those intentions and whether the signals are changing.

Sifting through the minutes of the Federal Open Market Committee (FOMC) to look for signals of changes in policy is a fixation for the financial media and the investment industry. Because both the stock and bond markets can reverse directions based upon the Fed's intentions for the direction of Fed Funds rates, there is an intense focus on finding signals for those intentions and whether the signals are changing.

However, like generals preparing for the last war - there is a strong case to be made that most analysis of the FOMC minutes is focusing on the details, while missing the big picture for the next recession (which could be growing more imminent).

As explored herein, the Fed itself is as much focused on how to change the "SOMA" to enable the strongest form of "MEP" in the event of another recession, as it is on Fed Funds rates.

When we get past the jargon, what the Fed is debating in plain sight are the specifics for how to give as much money as possible to some investors in the event of another recession, in the shortest time possible.

Oh, the Fed doesn't use those exact words (of course), but they do have an unprecedented problem to overcome, they know it, they plan on taking unprecedented steps - and as a necessary but incidental byproduct, these steps will likely create unprecedented profits for some types of investments with the next recession.

This analysis is part of a series of related analyses, an overview of the rest of the series is linked here.

The Internal Debate, The Trap & Setting The Base For More QE

The minutes of the April 30-May 1, 2019 meeting of the Federal Open Market Committee(FOMC) are linked below:

https://www.federalreserve.gov/monetarypolicy/filesfomcminutes20190501.pdf

The meeting began with a resumption of the discussion and debate about “Balance Sheet Normalization”.

“Participants resumed their discussion of issues related to balance sheet normalization with a focus on the long run maturity composition of the System Open Market Account (SOMA) portfolio.”

As readers will recall, to contain the damage from the last recession, the Fed created trillions of dollars in new money to buy investments and intervene in the markets. The "System Open Market Account" (SOMA) is where those assets are kept. So, what the Fed is debating is what to do with the extraordinary amount of investments they currently own, as the result of prior rounds of quantitative easing.

A particular focus of the discussion/debate was what the Fed's goal should be with their massive holdings of U.S. Treasuries on their balance sheet - should their portfolio goals be "proportional" or "shorter maturity"?

"In the first scenario, the maturity composition of the U.S. Treasury securities in the target portfolio was similar to that of the universe of currently outstanding U.S. Treasury securities (a “proportional” portfolio). In the second, the target portfolio contained only shorter term securities with maturities of three years or less (a “shorter maturity” portfolio)."

To many people, the preceding may seem to be just jargon, and to have little to do with their investment choices.

As we will explore, the opposite is true - the markets are in a place that they have never been before. What the Fed is discussing could lead to investment price movements that are some of the largest in financial history - which could include some the largest profits seen to date, in multiple investment categories.

To understand the source of the profits, we have to start with the trap the Fed is stuck in, as I have been developing in this series. As a starting point, recessions don’t just end themselves, at least not in the modern era, but the Fed aggressively intervenes to shorten recessions and contain the damage.

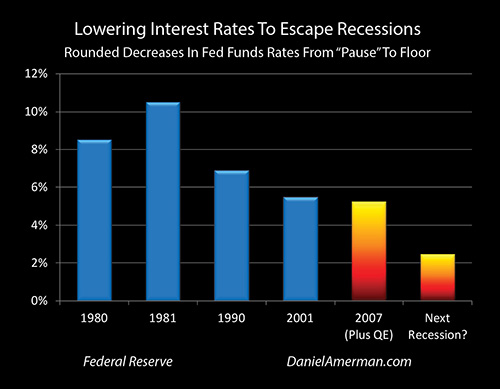

As can be seen in the five bars on the left and as explored in previous analyses (link here), the Fed relies on the shock factor of being able to slam down interest rates by large amounts to jolt the economy out of recessions. The average reduction in Fed Funds interest rates (from peak to trough) for the last five recessions is about 7.25%.

However, when we look to the bar on the right - current Fed Funds rates are less than 2.50%, which means that the Fed has a big problem - it only has about a third of the power needed, the shock factor traditionally used, to jolt the economy out of the next recession.

The Fed was trying to get interest rates back up again, to recover the power of its main recession fighting tool - but it ran into a problem, and has for now paused the cycle of increasing interest rates. The Fed stopped because further interest rate increases ran the risk of triggering the recession, and bringing it forward in time.

So the Fed is caught in a trap of its own making - interest rates are much too low to be fully effective for escaping the next recession, but raising interest rates would trigger the recession, which they don't have the tools to fight. Yet, the recession may be here soon anyway.

Whew!!! What a dilemma!!! What can this desperate group of cornered macroeconomists possibly do to escape this seemingly impossible trap they have created for themselves and the nation? (FOMC minutes may seem dense and boring on the surface, but can be much more exciting if one understands the jargon and the issues.)

Well, when the prior group of desperate and cornered macroeconomists found themselves caught in an impossible trap during the Great Recession and its aftermath - they tried to escape by running two unprecedented and dangerous experiments: slamming short term interest rates down to zero percent, and also creating trillions of dollars out of the nothingness (via quantitative easing) to buy investments and manipulate markets, forcing down first mortgage rates, and then (eventually) medium and long term Treasury interest rates.

This strategy exacted a huge toll on retirement investors and pension funds, particularly those relying on interest income to support their lifestyles or to pay beneficiaries - but as far as the Fed was concerned, both radical experiments were successes. So the current group of desperate and cornered macroeconomists plans to repeat both of those experiments if needed, but to take what they learned and raise the power a notch, in order to make up for the lower starting level of interest rates.

As a starting point - many people might think that we are back in normal times, and that zero percent interest rates are a somewhat bizarre relic of the past. That is not at all how the Federal Reserve sees things, however. The Fed plans to go straight back to zero percent interest rates in the event of another recession, and indeed, the staff expects bouts of zero percent interest rates to be "more frequent and protracted" in the future than in the past.

However, because the Fed relies on brute force, to shock the economy and the markets out of recession, and since interest rates won’t provide nearly the power, the Fed intends to use second form of shock therapy in the event of a future recession.

To compensate, the Fed intends to create trillions of additional dollars out of the nothingness - and spend it on the front end this time around, to change both interest rates, and investment prices.

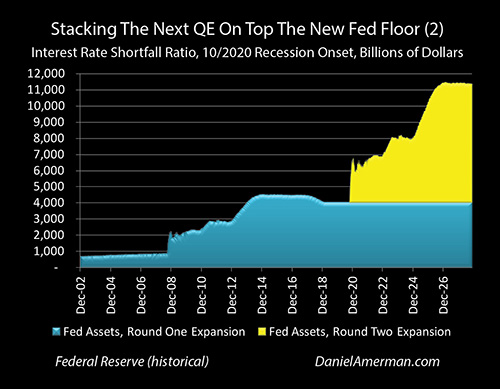

In the event of a future recession, the Fed has every intention of immediately entering into another massive round of quantitative easing, and jolt the economy out of recession if needed. This new round would stack on top of the old round, and one way this could happen is shown above and is explored in the analysis linked here.

The question that the Fed is focusing upon, is what it can do to change the current portfolio (the blue area above), so that when it is time to stack the new QE on top (the yellow area) - the maximum shock value is delivered to the economy and the markets?

How does the Fed get the most bang for its buck when it comes to the planned creation of trillions of dollars in new money in order to buy investments?

This then raises the question: where is the Fed also necessarily creating extraordinary new investment opportunities for investors, to an extent that has never existed in the past?

MEP & Historic Profit Opportunities

What is underlying the FOMC debate is how to maximize the effects of the planned “MEP” maturity extension program.

“The staff provided estimates of the capacity that the Committee would have under each scenario to provide economic stimulus through a maturity extension program (MEP).”

“In their discussion of a shorter maturity portfolio, many participants noted the advantage of increased capacity for the Federal Reserve to conduct an MEP”

To understand the vocabulary and the critical, market changing concepts, keep in mind that "QE", or quantitative easing is where the Fed gets the new money from, and it does not involve literally running printing presses, but using excess asset reserves from financial institutions. The money that is created via QEs can be used for different purposes, one of them is to fund an "MEP", or maturity extension program, which involves buying medium and long term Treasury obligations. QE2 the last time around was the first usage of an MEP by the Federal Reserve.

The traditional tool of the Fed is short term Fed Funds rates. When that tool was inadequate in the last round, the Fed used QE2 to conduct an MEP and buy trillions in medium and long term Treasury obligations. They did this to exert an unprecedented degree of control over long term rates, and force them down as well (through using the new money to buy bonds at ever higher prices, forcing the yields downwards).

The Fed did not start with QE2 or an MEP the last time around - that was years into the process, as discussed in the linked analysis on QE stacking. But the Fed does have every intention - if needed - the next time around to use a QE to fund an MEP as one of their primary recession fighting tools, and to do so right up front this time. They plan on buying massive amounts of medium and long term Treasuries, thereby extending the maturities of their portfolio while raising bond prices.

The point of the “shorter maturity” portfolio that is being considered, is to increase the force of the MEP. (That said, the MEP, and the corresponding blunt force being applied to long term bond prices, happens with either the "proportional" or "shorter maturity" alternatives.)

Moving Fed dollars from longer term to shorter term Treasuries now, means less Fed support now, which raises long term yields and lowers long bond prices, all else being equal and relative to where else they would otherwise.

The reason for this is that when the MEP hits, there is more room to very quickly lower interest rates - creating the maximum jolt for the markets and economy - which also necessarily, maximizes the increase in bond prices.

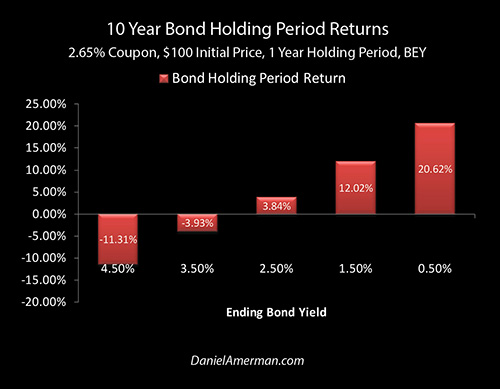

As explored in the analysis linked here, the Fed going to zero percent interest rates and adding in a round of QE could - using the traditional method that institutional investors use to profit from the Fed during a recession - produce a 21% one year holding period return.

Buying 10 year Treasury bonds is already a traditional way for astute investors to make money if they anticipate a coming recession. By indicating that for the first time they intend to use QE to fund an MEP as part of their initial response to recession - the Fed is quite clearly communicating that they intend to deploy massive amounts of newly created money to push bond prices up faster and higher than has ever happened before - which could make this traditional strategy the most profitable that it has ever been.

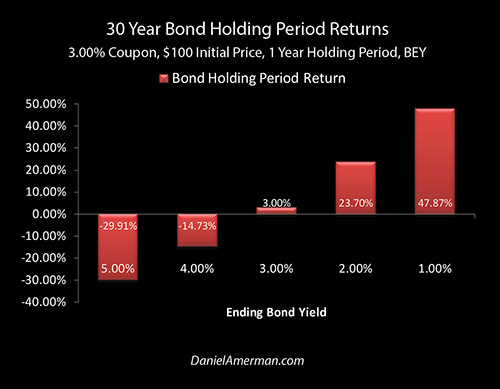

There is one thing that is better than the Fed having your back when it comes to making a quick 21%+ yield - and that is the Fed having your back when it comes to making a quick 48%+ yield.

As shown above and as explained in the analysis linked here, the financial mathematics change when we go out from 10 year bonds to 30 year bonds, and far larger potential profits are available from the longer term bonds, all else being equal. Our yield increases from 21% to 48%.

When the Fed staff is discussing maximizing the effectiveness of the MEP - they are talking about potentially using trillions of newly created dollars to buy up long term U.S. Treasury bonds, and thereby create larger price gains than would otherwise exist. For 30 year bondholders, these amplified and unprecedented returns could be in excess of twice the size of those realized by investors in 10 year bonds.

Making The Fed Work For You

So, let me offer a perspective on the April 30th to May 1st meeting of the Federal Open Market Committee, which is perhaps a little different from the usual one of a bunch of boring economists using dense and impossible to understand jargon.

Picture instead, a group of very bright people possessing extraordinary powers to create money and move markets, who are creatively brainstorming about who can come up with the best possible way of handing out as much money as possible, as fast as possible, to the people who own long term Treasuries, the next time there is a recession.

The previous ways this happened are just not good enough, so this diligent group of PhDs are going to work and work as they try to figure out even better ways where the powers of the Fed can be creatively applied, to find new ways where even more of the newly created money can be passed out to knowing investors, that much faster.

Kind of an interesting perspective, isn’t it?

They may not quite phrase it that way, but this group of cornered and desperate macroeconomists do need the maximum economic jolt to overcome the seemingly impossible trap that the Fed is currently in, and their weak starting point when it comes to very low interest rates.

So they need to compensate for the weakness in their traditional primary tool for fighting recessions (lowering Fed Funds rates) - by maximizing the effectiveness of their experimental secondary tool, that of an early and aggressive QE used to fund an MEP.

And the maximum economic jolt is created with the maximum concentrated move downward in long term interest rates, which necessarily creates the maximum concentrated move upwards in bond prices and holding period returns.

This movement - which necessarily means increased profit for those investors who are aligned - has never happened before, the Fed has never done this. When they used QE2 to fund an MEP and change medium and long term Treasury yields last time around, that was years after the initial recession. What the FOMC and staff are debating - is how best to make this first time event happen, with an intervention of extraordinary force on the front end.

One way of improving the force of the intervention - and the increase in bondholder profits - is to take the “shorter maturity” approach, which is why they are brainstorming it.

Another way of increasing the force of the intervention - and the size of the bondholder profits - is to take the “accelerated” transition approach, which I did not have the time to explore in this analysis, but is part of the FOMC minutes.

Each one of these is brand new, each one of these has the potential of creating extraordinary profits that are outside of the historic range, and each are being brainstormed in plain sight - for those who know how to understand the words and can follow the investment implications.

Another fascinating issue that there is not the room to explore in this particular analysis, can be found in the minutes and is quoted below.

“Based on the staff’s standard modeling framework, all else equal, a move to the illustrative shorter maturity portfolio would put significant upward pressure on term premiums and imply that the path of the federal funds rate would need to be correspondingly lower to achieve the same macroeconomic outcomes as in the baseline outlook.”

The Fed is actually considering lowering Fed Funds rates before a recession hits, specifically in order to get the room to increase the power of the MEP for when the recession does occur. This would be extraordinary and unprecedented - and could fundamentally change the short term paths for stock and real estate prices, as well as bond prices.

The Longer Term & The Wealth Function

The potential changes in bond prices are extraordinary - but they are also the least of the investment implications for investors over the long term. The biggest changes in prices and returns for most investors from these extraordinary and unprecedented Federal Reserve interventions are likely (over time) to be found with stocks, real estate and REITs.

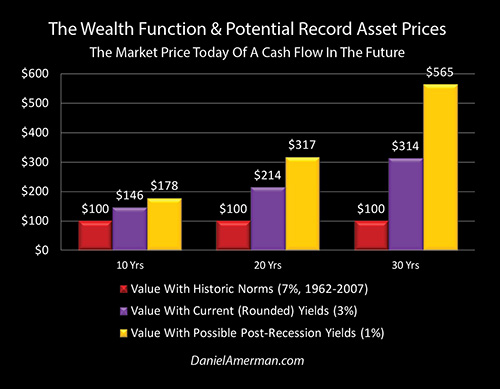

To help people understand how what the Fed is contemplating can also fundamentally change the stock and real estate markets, I developed the analysis “The Wealth Function, Fed Cycles & Record Asset Prices” (linked here), which goes down to the mathematical function at the bedrock level of all investment valuations, which I refer to as the “Wealth Function”.

There are two important takeaways from the discussion in the FOMC minutes, when it comes to the Wealth Function and potential long term stock, bond and real estate prices. These will apply if there is another recession and the Fed does indeed successfully contain the recession with its planned new tools of using not only an early and aggressive QE, but using the money from the QE to fund a MEP. In other words, if the Fed takes the new trillions and uses them to go long on the front end of the recession, in order to get the maximum bang for the buck.

As can be seen by comparing the red and purple bars above, the Fed has already created the mathematical foundation for the highest stock and real estate prices in history - and that is what we have now, record or near record stock and real estate prices.

What the Fed is strongly signaling is that its plans for the containment of a future round of recession and potential financial crisis, are to move the Wealth Function input variable to a place that will (eventually) support something in the range of the golden bars - the highest stock, bond and real estate prices in history, at levels that are potentially well above even what we are seeing today.

The other critically important information is that by focusing on MEP, the Fed will be disproportionately using its powers to boost the value of the longer term cash flows - and taller golden bars - on the right hand side of the graph, to an extent that would be historically unprecedented.

So, if things work in the way currently being brainstormed by the Fed, then the greatest (eventual) boost in value will be provided to the sectors of the stock, bond and real estate markets that have the highest sensitivity to changes in the Wealth Function input variable, and the greatest inherent mathematical ability to increase in value.

Cyclical Opportunities

The Federal Reserve used extraordinary and heavy-handed interventions to contain the Financial Crisis of 2008 and the Great Recession - and it has not been able to fully exit those policies, for fear of triggering another recession. We are indeed still inside of a cycle of crisis and the containment of crisis, and while that may sound a bit on the bleak side - one of that ways that it has been expressing itself is through record and near record asset prices.

Just as we have the possibility of still higher asset prices as part of this amplified cycle - we also have the possibility of amplified losses at some points in the cycles (as explored in the previous chapter).

Most crucially of all - this is in no way a random process.

Much of investment theory and traditional financial planning is based upon history (implicitly) endlessly repeating itself when it comes to the broad strokes of asset category performance over time, with the particulars being a “random walk” that can’t be anticipated.

Yet, what we have seen in the investment markets in the last couple of decades has not been random, but has been the result of quite deliberate and calculated interventions by extraordinarily powerful outside agency - the Federal Reserve.

As explored herein, the Fed has plans for even more extreme interventions with the next round of the business cycle, which could change stock, bond and real estate prices in ways that cannot be anticipated by merely studying history before such interventions.

And while we cannot have certainly - we can strongly shift the odds by understanding what motivates this outside agency, what it is considering next, and how its past and future interventions can transform investment results. Showing how such an understanding could be obtained through deciphering the publicly available minutes of the Federal Open Market Committee was the intent of this analysis / chapter, it is one example of that process.

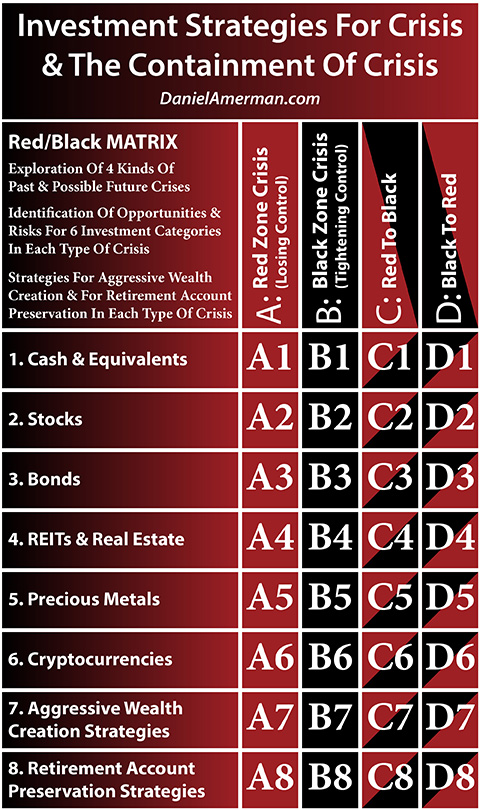

Because I believe the Fed's increasingly heavy-handed interventions have created cycles of crisis and the containment of crisis which are very important for individuals to understand, I created the framework below to help explain how these new changes in the cycles can change investment category results at various stage in the cycles.

An explanatory analysis for the matrix is linked here.

As explored in the link, the columns are the phases in the cycles, the rows are the investment categories, and the individual cells are how particular investments perform during particular times in the cycles.

The main initial focus of the FOMC meeting was the “C” column, the movement from crisis to the containment of crisis - even though they of course did not use that term.

Nonetheless, the Fed is intensely focused on how to contain a potential future recession and crisis, given that they do not have their usual tool at full strength.

What was explored in this analysis was how the unprecedented steps that the Fed is brainstorming as part of the future containment of crisis, could translate to unprecedented potential investment opportunities in the specific investment category of bonds, which is the 3rd row, so we were exploring the "C3" cell.

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

© 2019 Copyright Dan Amerman - All Rights Reserved

Disclaimer: This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.