Continuing Credit Crisis About to Get a Lot Worse

Economics / Credit Crisis 2008 Sep 06, 2008 - 02:11 AM GMTBy: John_Mauldin

Thoughts on the Continuing Crisis

Thoughts on the Continuing Crisis- Fool Me Once, Shame on You

- Delinquencies and Foreclosures Spike UP

- Unemployment Rises to 6.1%

- Action Is Needed Now

We are entering the next stage of the credit crisis, and one which is potentially more troubling than what we have seen over the past year, absent some policy reactions by the central banks and governments world wide. The crisis was started by an intense run-up in leverage by financial institutions and investors world wide, investing in increasingly risky assets such as subprime mortgages and then the realization that leverage could hurt. The deleveraging process started to intensify last year about this time. The easy part of that process has been just about done. Now is the time for the really hard work. It will not be pretty. In this week's letter, we look at the process and think about its implications for the markets and the economy, and visit some data on the housing market and unemployment.

And just for the record, the problems I am describing in this letter are very real. But we will get through them, as we have always done. This is not the end of the world. There are a lot of very good things happening here and there. As we will see, for most smaller banks, it is business as usual. In general, in most places and for most people, life is going on just fine. There are opportunities being created. The markets will find new solutions. But there is some more short-term pain for many market participants, and we need to be aware of the problems and see if we can avoid them for ourselves.

But first, let me ask you for some help. I get to travel a lot with my daughter and business partner Tiffani (actually she runs the business) and meet new people. Over the years, she has become as fascinated as I have with their individual stories. Everyone has a story to tell or a lesson to teach. As I announced a few months ago, we have decided to write a book (or series of books) about those stories, looking at the differences in perspective between old and young, retired and working, those who are wealthy and those who aspire to wealth. What are the differences in attitudes, in work habits, in how you manage money, in how you look at the future, and a score of other items? How do all of these things correlate?

We have created a totally anonymous online survey seeking answers to these questions and more. We have had more than 12,000 of my readers fill out the survey (thank you!!!) and we are learning a lot. We are eager to see what we find as we pore over the resulting data and engage in a lot of in-depth analysis. Are the rich really different? Is there a difference in people from Europe, Asia, Latin America, Africa, and the US? I think we will find some very interesting information.

Please note: this is not just a survey for millionaires. We want everyone, of all income levels and ages, to take the survey, so we can get a true representative sample. We would especially like more ladies and international individuals to take the survey.

You can get to the survey page by clicking here. It will take about 10-15 minutes to complete, and I think that going through the questions will make you think about your own situation. Some have told us the survey is quite thought-provoking. If you have attempted to take the survey and had problems, we think we have worked out the bugs.

Thanks in advance. And now on to the letter.

Thoughts on the Continuing Crisis

Let's start by explaining the process of de-leveraging in what I know are VERY simplistic terms. On average today, FDIC insured banks have about 7.89% of capital for their outstanding assets (loans are generally about 60% of assets), so they are roughly levered up by about 12.5 times. Some investment banks are leveraged up to 30 times. Fannie and Freddie are leveraged 50 times their capital. But to make matters simple, let's assume leverage of 10 times.

(For the record, to be considered "well capitalized" you have to have at least 5% of capital in Tier One assets, and 10% of what is considered risk based assets, with anecdotal evidence that the regulators want to see 12%.)

That means for every $1 million in capital you have, you can lend out $10 million. The profit you make is the difference in the cost of your capital and money your borrow to lend and the interest rate you charge. If your are paying 4% for your money and charging 8%, you would make 4% times $10 million, or gross profits of $400,000. That is a return of 40% on invested capital, which is why so many small banks are being started all over the country every year. Nice business if you can get it.

Of course, you have to be able to take some losses. If you had a $500,000 loan go bad, you would have eaten up all your profits and dipped into your capital. Now you would only have $900,000 in capital. That means you could only make $9 million in loans. Either you will have to raise more capital from investors or reduce your loan portfolio, in addition to writing off the bad loan.

Now, what constitutes capital at real world banks is a very complex thing. How much it costs to find money to lend can vary wildly. Many of us "lend" money to our banks at zero cost to the bank in our checking accounts. They pay more for savings accounts, borrowing from other banks, etc. They charge different rates for different types of loans. It is a very complicated business, and we will not go into any details. The basics of my simple illustration will get us to where we need to go.

When I want to find out something about US banks, I turn to my friends at PL Capital. They run a fund which invests in smaller banks, and have been consulting with banks for many, many years. They really know the business. I caught up with Rich Lashley and asked him to give me his thoughts. I am going to pass them on to you, as they are not as bad as one would think.

In the US, and in much of the developed world, there are two tiers of banking. There are about 8500 banks. The top 50 banks have more than 80% of the assets. The rest of the banks are generally much smaller. Outside of five states hit particularly hard by the housing crisis (see more below), for most of the under top 50 banks, it is business as usual.

There is money for most smaller businesses and projects at the smaller banks except for residential development. The true credit crunch is at the top for larger projects. Want to do a $3 million deal? If you have a reasonable project, it can get financed. Want to do a $300 million deal? Lot's of luck, for reasons we note below.

Most of the smaller banks have plenty of capital and are looking to put it too work. Rich guesses there are about 4-500 banks (5% of the total, with concentrations in states with bad housing markets) which are in some level of financial stress, meaning they need to raise capital or reduce lending. His guess is that we will see about 100-150 banks fail over this cycle. He would be surprised if we saw more than 3 top 50 banks fail. Most of the larger banks, if they get into trouble, would be absorbed by better capitalized banks in search of market share.

In fact, Rich is quite bullish on selected bank shares. 86% of the banks/thrifts in the U.S. made money in Q1 2008 and almost 50% earned more in Q1 2008 than they made in Q1 2007 (i.e. they made more money after the credit crunch than before.) But nearly all banks stocks have declined in sympathy with the problems brought on by the credit crunch. Over times, growing earnings will make for a rebound.

So, middle America and middle American business, except for construction, are not by and large experiencing a credit crunch. The smaller banks are not cutting home equity lines and Rich says they are not experiencing abnormal losses. That is because they are local bankers who know their customers. It is the banks which offer home equity loans and have brokers do the lending without really having any incentive to make sure the loan will be good which are the ones in trouble. Securitized home equity loans and second mortgages are showing significant losses.

Fool Me Once, Shame on You

It is a different story at many of the larger banks. Let's look at two tables from my friend Gary Shilling's latest letter. (www.agaryshilling.com) It is well worth the $275 a year (the investment professional version is $1,000).

To set up the tables, there have been writedowns and losses of about $501 billion in both investment and commercial banks. They have raised $353 billion in capital. As I have written repeatedly, it is likely that we will see another $500 billion in losses. The IMF estimates total losses of $1 trillion. Private estimates from credible sources can run as high as $2 trillion.

As you would expect, the largest losses are typically in the larger banks, with some exceptions. Goldman has only written off $3.8 billion. Citigroup has written off $55 billion. The table, if I am adding correctly, sums up the losses from 64 banks, and adds in "other" banks losses from European, US, Asian and Canadian banks. Outside of the top 64, there have only been writedowns of $16 billion. Again, that speaks to the phenomenon Rich alluded to earlier. It seems that the bigger banks took the riskier bets, getting stuck with the "Old Maid" of subprime and other mortgages and loans. Banks that could not afford to get into the game did not have the losses. In this case, being small was an advantage.

So, how did the investors who gave the various banks capital do on their investment. Shilling shows us 9 deals done by sovereign wealth funds. The best return was down a mere 26.6%. The worst was Singapore in UBS for down 56% in less than nine months.

The old line is "Fool me once, shame on you! Fool me twice, shame on me!" How difficult do you think it is for any major bank to go back to sovereign wealth funds and ask for more? If they got it, you can bet the terms will not be favorable to current shareholders.

Last week I talked about how much it costs for many banks to raise money today. For weaker banks, the cost of new capital is prohibitive.

But going back to my simplistic illustration, regulatory requirements mean that if you are deemed not to have adequate capital, you have to raise money or reduce your loan portfolio. Raising money in today's environment is going to be difficult for many banks. Lehman has been shopping for capital for months. Merrill has had to sell some key assets. It is a strange philosophy of selling the best and keeping the rest, but that is what regulations require you to do. Merrill, for instance, recently sold $30.6 billion of poorly performing mortgage related assets for (which they valued at $11.1 billion) to a private equity firm called Lone Star for $6.7 billion, which is a 78% discount to the original face value. But Merrill had to finance 75% of the deal, which means they may only get 5 cents on the dollar.

And while I am picking on Merrill, let me quote this paragraph from Shilling's latest letter to illustrate the problems the large banks have.

"To add insult to injury, Merrill Lynch recently announced plans to sell $8.5 billion in new common stock, which will dilute shareholders by 38%. Previously, in response to writedowns, which totaled $46 billion since June 2007, Merrill has raised $15 billion in common and preferred stock. And this new common stock sale will be even more costly to Merrill since earlier sales of $5 billion in stock at $48 per share to Temasek, a Singapore state owned investment company, required compensation for the difference if Merrill sold stock at a lower price within 12 months. The stock is now $27 per share, which will cost Merrill over $2 billion."

If there are in fact more large losses coming in the next year, what will the banks do? Raising capital is going to be tough and come at serious costs to current shareholders. We will see some of that, and that is a reason I would be very cautious about the stocks of large financial companies. The bulls would say that the problems are already in the price. Of course, that is that they said six months ago as well. Caution is to be taken.

The second thing they can do to repair their balance sheet is reduce their loan books or sell off assets or loans. And that is happening. And it is going to happen more and more. It is going to be increasingly difficult to get large new loan deals done and that is going to put a damper on the economy. 60% of banks report they are tightening their lending standards. In the recent Beige Book, the Fed reported that all districts have seen tightening standards, something that is unusual.

Leverage loan for mergers and buyouts have dropped 75% since last year. They were only $50 billion in the first quarter, and it is almost certain to have dropped to even lower levels this last quarter.

And the leverage that was so helpful as it rose? It is now going to have the opposite effect. If you lose a billion and can't raise the capital, you are going to have to reduce your loan book or sell off assets by (using my analogy) $10 billion. If we have potential write-downs of several hundred billion more, that pain is going to be felt in both the corporate and individual worlds, as credit availability is going to decrease and rates are going to go up.

And the pain may not be abating. While some suggest that we have seen the bottom in housing and the economy, the data out the last three days suggest that is not the case.

Delinquencies and Foreclosures Spike UP

Phillippa Dunne (The Liscio Report) sent me this note a few moments ago:

"The MBA delinquency numbers just came out. In Q2, foreclosures were started on 1.19% of outstanding mortgages, up from 0.99% in Q1, and nearly three times the pre-2000 record. The total stock in foreclosure was 2.75% of all mortgages, more than twice the pre-2000 record. Seriously delinquent (90 days or more, plus those in foreclosure): 4.50%, also more than twice the pre-2000 record. Most of the previous records were set in the 1980s, when both unemployment and interest rates were considerably higher than they are now."

If 4.5% are 90 days or more behind, it is likely that foreclosures will rise precipitously. If you think there is a crisis today, just wait six months. Mortgages past due by 30 days are more are now at a nose bleed 6.35%

Think about this. Freddie and Fannie guarantee 50 times their capital in mortgages. What would a 2% default rate do to them? 8,000,000 homeowners now have negative equity in their homes as of the end of the first quarter. That number is rising as home values drop.

Some cheered the fact that home sales rose last month, and that is a good thing. But the number of homes for sale rose even more. There are now 11.4 months of inventory in the existing home market. New homes show an inventory of over 8 months versus an industry norm of 4.3 months.

As I have been saying for almost two years, the housing market will not normalize until some time in 2010. It is going to take a long time for the markets to work off the excess inventory.

Anecdotally, I have a realtor friend in Dallas who is working with a number of investors buying distressed homes (using some leverage) and condos and then leasing them for returns of 8-10% or more. I am sure that is happening in a lot of places. Such activity is needed to get excess inventory off the "for sale" lists.

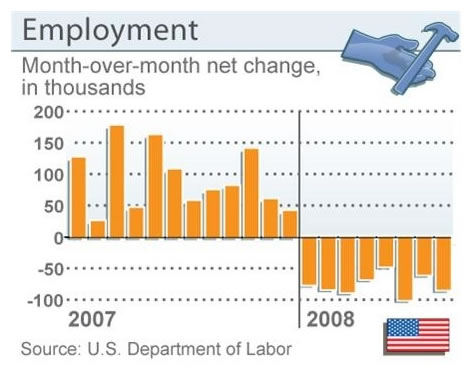

Unemployment Rises to 6.1%

There is a reason that consumers are falling behind on their home loans (and on credit cards, auto loans and student loans - you get the picture). Over the last 8 months, unemployment has risen by 685,000. And that assumes there are hundreds of thousands of jobs created in the birth/death model. When the numbers are revised next year, I would be willing to wager that job losses are closer to 1,000,000. That would be consistent with an unemployment number of 6.1%, up from 5.7% last month. That is the highest level in five years.

Greg Weldon provides us with the following thought (www.weldononline.com)

"From the top-down macro-perspective, there is NO denying that the US Labor Market is in a RECESSION, as might be best evidenced via a perusal of the chart on display below, in which we plot the monthly change in the headline Non-Farm Payrolls, along with its 12-Month Exponential Moving Average. Indeed, EVERY time the moving average falls below zero ... it has indicated that the broader economy has dipped into a RECESSION, in 1973-74, 1980-81, 1990-91, 2000-01 ... and ... 2008 !!!!"

Action Is Needed Now

It is unfortunate that the crisis in housing and the credit markets seems to be coming to a head in the middle of a hotly contested election cycle and a lame duck president. Matters are such that waiting until a new president is in power and has his new appointees in place is a very bad option. Things could spiral down very quickly without action by the Treasury and the Fed and other regulators.

Lax regulation of both the mortgage industry and the rating agencies allowed the current crisis to develop. While new regulations will be helpful in the future, we have to deal with the problems as they are today. As I noted above, the credit crunch has the potential to get much worse in the coming quarters. It is clear to a number of observers that Freddie and Fannie are dead men walking. They are going to need capital from the Treasury. Those with mortgages that have the ability to pay at some level should be helped, and the rest need to be sold off at market clearing prices. But that means mortgage debt must be available. Because of the problems in the markets, mortgage rates are higher than they should be, making the housing problems worse.

Since we are going to have to take action sooner rather than later, we should do it sooner. One of the main rules in investing is that "The first losses are the best losses." The longer we wait, the more distress there will be in the housing markets and the lower values will go. Putting off action until next year will mean more losses for taxpayers and more pain in the markets when action is finally taken.

It physically hurts me to write those words. It is so against my free market economic beliefs. But a slow implosion of Freddie and Fannie, and a non-existent jumbo loan market, will mean a very serious recession if not checked soon. Art Cashin sent me this note today: "Paul Volcker at Calgary Conf. says financial crisis "most complicated" he's ever seen. Losses will clearly exceed $500B and U.S. growth will be slowest since the Great Depression."

Those are not light words from a man who is one of the better insights into the economy. I will leave it to wiser men than I to figure out how to stabilize the housing market and Fannie and Freddie. But it must be done.

Further, some thought should be given to allow for slower writedowns of assets, giving troubled banks with otherwise profitable businesses the time to heal. This should be done in conjunction with better regulations and a requirement for reduced leverage over time from investment banks that have access to the Fed window would be helpful.

And while I am indulging myself in wishful thinking, would someone please force Credit Default Swaps onto a regulated derivative exchange like futures and options? This has the potential to magnify the credit crisis into a real nightmare. Maybe we can dodge that, but why risk it? I see no reason to do so, and about $60 trillion (the value of the CDS markets) reasons to do so.

Annapolis, La Jolla and Wedding Videos

It is a good thing I looked at the invitation a few days ago. I thought I was going to Baltimore. As it turns out, I will be traveling to Annapolis (not too far away) tomorrow morning with Tiffani to go to my really good friend Bill Bonner's 60th birthday bash. We met 26 years ago. How time has gone by. When I first went to his office in a very bad part of Baltimore so long ago, I was seriously nervous about walking two blocks from my car. Bill decided that low rents were worth it. And as rich as he is, he is still frugal. He scraped and painted 100 shutters himself (with his kids) at his chateau in Ouzilly in the country side in France.

We have some things in common. Both our mother's are alive and served in the Women's Army Corps in WW2. He has six kids and I have seven. We both have several New York Times Best sellers. We have ridiculous travel schedules. And life has blessed us immensely. We also have a lot of mutual friends, so this is going to be a very fun weekend! Bill throws great parties.

Bill writes the Daily Reckoning. He is one of the best pure writers I know. I sometimes feel like a house painter looking at a Rembrandt when I read his essays. You can read some of his essays and subscribe to the free Daily Reckoning (be warned: Bill is quite bearish) by clicking on this link: http://www.dailyreckoning.com/rpt/mauldin.html.

Tiffani just sent me a link to this short version of what will be a major video production of her wedding in a few months. If you have a bride coming up in your family, you might view this to see what a non-traditional wedding can look like. And she is a very beautiful bride. Pay attention to the fireworks in the background as they kiss. You can see it at http://vimeo.com/1615007. And yes, the strawberries on the treasure chest wedding cake are to hide where I put my thumb through it, thinking it was a real chest.

Take some time this week to see families and call that old friend up and say hello.

Your really ready to party analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.