Tax Reform: Implications for Gold

Commodities / Gold and Silver 2017 Oct 04, 2017 - 03:50 PM GMTBy: Axel_Merk

Last week, I got several calls asking me how U.S. tax reform will impact the price of gold. If you can answer this question, you might be able to answer how tax reform will impact other assets. Let me explain.

Last week, I got several calls asking me how U.S. tax reform will impact the price of gold. If you can answer this question, you might be able to answer how tax reform will impact other assets. Let me explain.

If you were to analyze the impact of any tax changes on any asset, you have two sets of dynamics to consider: those of the tax reform and those of the asset. What makes the comparison to gold unique is that gold is, if I may call it such, the purest of all assets because it doesn’t change. It is the world around it that changes.

Monetary policy affects nominal prices, whereas fiscal policy affects real prices. That is, printing money might affect the price level, but fiscal policy affects where money gets allocated, and what investments take place. I would like to caution that not everyone agrees, especially with regard to monetary policy, but even if you do not fully agree, bear with me, as a simplified model might help in understanding price dynamics.

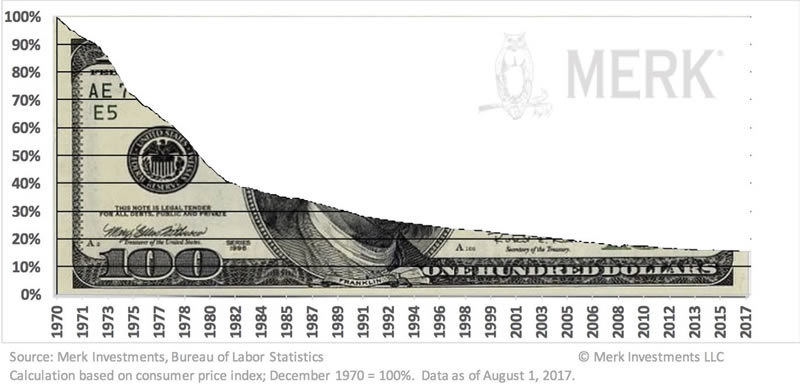

When held in a vault (rather than leased out), gold doesn’t generate cash flow. Investors have the choice of investing in a so-called productive asset that generates cash flow; or to park it in something unproductive, such as a hundred-dollar bill in your pocket; or gold. While there’s a convenience factor to the hundred-dollar bill to use for purchases, most would agree depositing the cash in an interest-bearing deposit may be worth the risk. There’s the risk of the default of the counter-party. For bank deposits, FDIC insurance tends to mitigate the risk; and for Treasury Bills or Treasury bonds, there is the full faith of the U.S. government that the principal will be paid back. Yet Treasuries aren’t entirely risk free: the longer you commit your money for, the more interest rate risk you bear (the market value of Treasuries tends to fluctuate the further out the maturity even if the principal is not at risk); and while the US government guarantees to pay back the principal value of its debt, it doesn’t guarantee it will have the same purchasing power at maturity. The chart below shows the purchasing power of the U.S. dollar since December 1970, that is, the purchasing power of your hundred-dollar bill when sitting in your pocket:

This illustrates why the price of gold has appreciated: at the end of 1970, an ounce of gold cost less than $40; currently, it costs over $1,200 an ounce. The gold never changed, but the purchasing power of the dollar has eroded. Indeed, since 1970, the price of gold has appreciated substantially more than the purchasing power of the dollar has declined, suggesting the price of gold is influenced by more than merely the consumer price index.

In my assessment, a key driver of the price of gold is the real rate of return available on other investments. The benchmark for these “other” investments for U.S. dollar based investors is the so-called risk-free investment: Treasuries. Most people don’t walk around with hundred-dollar bills in their pocket, they make a conscious decision how to allocate their money. If they get compensated more for holding Treasuries, the price of gold may suffer (again: because gold is the constant here).

As such, if one believes tax reform increases the real rate of return on investments, the price of gold - all else equal - may suffer. When President Trump was elected, after the brief overnight spout of volatility, the price of gold fell as Treasury yields rose. I argued at the time that the market was pricing in higher real rates of return. In the subsequent months, the so-called Trump trade fizzled out as, and that’s my interpretation, the market priced in lower odds of meaningful tax reform.

In recent weeks, the price of gold has experienced some softness, as Treasuries have fallen once again. Note that the correlation between bonds and gold is currently elevated, but that this relationship is by no means stable. That’s why I earlier used the qualifier “all else equal”. In that context, is the most recent weakness in the price of gold due to more hawkish talk at the Federal Reserve, i.e. due to monetary factors, or due to the tax reform framework announced by the Administration, i.e. fiscal factors?

Let’s look at each, then broaden the discussion. If you believe that the tax proposals will a) meaningfully alter the long-term growth prospects of the U.S. economy; and b) will be implemented, then odds are downward pressure is exerted on the price of gold. Note there is a different between tax cuts and tax reform. Imposing a lower tax rate may be a short-term stimulus, but it may not fundamentally alter investor behavior. Take the estate tax, for example: let’s assume for a moment the estate tax will be eliminated (the odds of that passing are rather low), but that the elimination will expire after 10 years. Many tax provisions expire after 10 years as that’s how they get passed under Senate budget reconciliation rules requiring only a simple majority. If you are a wealthy foreign individual considering relocating to the U.S., and your life expectancy is greater than ten years, the change in tax code would unlikely change your behavior. Had this person relocated to the U.S., even as a retiree, he or she likely would have spent substantial money over the rest of his or her lifetime, contributing to higher U.S. growth.

The estate tax example is easy to visualize, even if the total impact of the estate tax is rather small. The same applies to other provisions in the tax code as well, though. For example, if U.S. companies have a long-term assurance that they won’t be taxed on income abroad, they can make resource allocation decisions based on where they believe money is best deployed rather than based on quirks in the tax code encouraging them to shield it from the IRS.

There’s also an argument to be made that long-term investors in the U.S. want to see the U.S. budget be on a fiscally sustainable course. Because if the U.S. is on a fiscally irresponsible course, odds are, the government will at some point take the money from those who have it (and/or cut benefits; or be unable to keep up the infrastructure, etc.).

That said, one should not get too carried away with the politics. It’s not that each proposal by your favorite party is good; and the end of the world is about to come when ‘the other’ party wins. To pass through Congress, most tax proposals are substantially watered down. Indeed, the Administration’s proposal has lots of wiggle room, suggesting already that the final product, if any, may not hold up to the rhetoric: the blueprint proposed leaves open the possibility that the U.S. will not fully embrace a territorial tax system (i.e. no longer tax earnings abroad); it also leaves open the introduction of a higher tax rate for top earners, amongst others. Given the failure to pass healthcare reform, one shall be excused to be a cynic about the odds of tax reform passing as well.

Needless to say, my own assessment is that we might get a few tweaks in the tax code, but odds are low that it will be a structural transformation causing real growth to substantially change. I have not been able to identify attributes in the market that suggest otherwise. By all means, if you draw different conclusions, this is intended as a framework to think about the issue rather than a crystal ball.

So how come the price of gold has weakened since the announcement of the Administration’s plan for tax reform? Nothing ever happens in a vacuum: we also had the Federal Reserve meet and provide a more hawkish outlook; several economic indicators were positive, causing Treasuries to fall. There were also some global events that I won’t digress to for the simplicity of the argument here.

With regard to the Federal Reserve, I would like to make two comments: the tail-wagging-the-dog argument, as well as one on risk premia:

With regard to tail-wagging: it’s been my impression that the Fed would like to raise rates, but only as long as financial conditions don’t deteriorate. That’s a bit of an oxymoron as the whole purpose of rate hikes is to tighten financial conditions. In my view, the Fed is concerned about a sell-off in asset prices. According to what a former regional Fed President once told me, under normal circumstances, the Fed would not worry about asset prices; unless, that is, they created a bubble. Differently said, when the markets behave, expect hawkish Fed talk. But let the markets have a hiccup, and those good intentions are thrown out of the window. And since the markets have behaved, the Fed’s most recent talk has been hawkish. That puts a short-term dampener on the price of gold (but may be a buying opportunity if one believes this hawkishness won’t translate into higher real rates).

The other attribute is risk premia. The Fed has announced it will reduce the size of its balance sheet. I have seen Fed studies that suggest this will lead to lower bond prices (higher yields). I disagree. I believe it will lead to higher risk premia. Quantitative Easing (QE) cause the spreads between junk bonds and Treasuries to narrow; more broadly speaking, so-called risk assets rose in price; with regard to stocks, the lower volatility, in my opinion, is a direct result of QE. In contrast, in my view, Quantitative Tightening (QT) will expand risk premia. That is, risk assets are at risk of falling as volatility increases; such volatility is often associated with a “flight to safety”, i.e. purchases of Treasuries. But, and here we go back to the tail-wagging argument, the Fed doesn’t want asset prices to plunge. And, hence, the Fed is telling us QT is akin to watching paint dry. Sticking with abbreviations, the paint-drying argument is, in the opinion of yours truly, a bunch of BS.

Circling back to the price of gold: my framework is that the reason risk assets tend to fall as volatility rises is because the cash flow of said assets gets discounted more (the cost of capital is a function of the risk/volatility). As gold does not have cash flow, it shines in contrast when volatility rises.

And with that, I make assertions not just about the price of gold, but asset prices in general:

- The benchmark of risk is Treasuries, the risk-free rate of return. That’s why it is so important to know what the Fed is up to (and so bad to have a tail-wagging-the-dog Fed).

- To the extent tax reform affects expectations of real returns, it affects Treasuries.

- The lower real rates of returns are, the more favorable for the price of gold and vice versa.

- Risk assets trade at a discount to the risk-free asset (“discount” w.r.t. fixed income means the yields are generally higher). That discount varies based on financial conditions.

- The lower risk premia are (high complacency/favorable financial conditions), the more favorable for risk assets.

- Higher risk risk premia (fear) tends to be favorable for the price of gold.

- QE compressed risk premia; QT will cause risk premia to expand.

In other words: don’t expect much from the tax reform, consider holding gold as a diversifier in your portfolio and buckle up, the unwinding of the Fed’s balance sheet may cause some sparks.

If you believe this analysis might be of value to your friends, please share it with them; follow me on LinkedIn and Twitter.

Axel Merk

Manager of the Merk Hard, Asian and Absolute Return Currency Funds, www.merkfunds.com

Rick Reece is a Financial Analyst at Merk Investments and a member of the portfolio management

Axel Merk, President & CIO of Merk Investments, LLC, is an expert on hard money, macro trends and international investing. He is considered an authority on currencies. Axel Merk wrote the book on Sustainable Wealth; order your copy today.

The Merk Absolute Return Currency Fund seeks to generate positive absolute returns by investing in currencies. The Fund is a pure-play on currencies, aiming to profit regardless of the direction of the U.S. dollar or traditional asset classes.

The Merk Asian Currency Fund seeks to profit from a rise in Asian currencies versus the U.S. dollar. The Fund typically invests in a basket of Asian currencies that may include, but are not limited to, the currencies of China, Hong Kong, Japan, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan and Thailand.

The Merk Hard Currency Fund seeks to profit from a rise in hard currencies versus the U.S. dollar. Hard currencies are currencies backed by sound monetary policy; sound monetary policy focuses on price stability.

The Funds may be appropriate for you if you are pursuing a long-term goal with a currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Funds and to download a prospectus, please visit www.merkfunds.com.

Investors should consider the investment objectives, risks and charges and expenses of the Merk Funds carefully before investing. This and other information is in the prospectus, a copy of which may be obtained by visiting the Funds' website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest.

The Funds primarily invest in foreign currencies and as such, changes in currency exchange rates will affect the value of what the Funds own and the price of the Funds' shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. The Funds are subject to interest rate risk which is the risk that debt securities in the Funds' portfolio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities which can be volatile and involve various types and degrees of risk. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. For a more complete discussion of these and other Fund risks please refer to the Funds' prospectuses.

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice. Foreside Fund Services, LLC, distributor.

Axel Merk Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.