Crashing Global Economy Boosts Dollar as Interest Rate Differentials Narrow

Economics / Recession 2008 - 2010 Aug 17, 2008 - 09:01 AM GMT

Almost exactly a year after the advent of the credit debacle, the term “credit crunch” squeezed into Britain's Chambers dictionary, defined as “a sudden and drastic reduction in the availability of credit”.

Almost exactly a year after the advent of the credit debacle, the term “credit crunch” squeezed into Britain's Chambers dictionary, defined as “a sudden and drastic reduction in the availability of credit”.

Fittingly, the past week witnessed market participants focusing anew on deteriorating global growth prospects, arguing that slower growth and belt-tightening times could reduce inflation pressures.

A wave of weak data hit the global economic headlines during the week. Real GDP growth in the Eurozone contracted by 0.2% in the second quarter, the first decline since record-keeping for the Euro area commenced in 1995. Germany and France, the two largest economies of the group, recorded declines in GDP of 0.5% and 0.3% respectively. The UK economy is on the verge of a recession, facing its gloomiest outlook since the early 1990s. Japan, the world's second largest economy, also contracted by 0.6% in the second quarter.

The notion that the US was further along the slowdown process than foreign economies, and an expectation that interest rate differentials could narrow in favor of the US dollar, resulted in continued strength in the greenback, further weakness in commodities, lower bond yields and mixed stock markets.

BCA Research said: “… lower energy prices, if sustained, should begin to help cool inflation fears. … inflation lags economic growth by several quarters and the economy continues to slow. … inflation fears should gradually recede.”

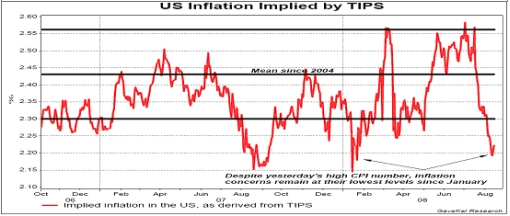

Further evidence that worries about inflation were decreasing was seen by implied inflation in the US, as derived from Treasury Inflation-protected Securities (TIPS), falling to their lowest level since January.

Regarding the inflation/deflation debate, Richard Russell ( Dow Theory Letters ) weighed in with the following comment: “With credit being restricted, a second and very serious danger surfaces. That danger is asset deflation. The very thought of asset deflation sends chills of fear up Fed chief Ben Bernanke's spine. Credit contraction, asset deflation – shades of the Great Depression.”

Next, a tag cloud of the text of all the articles I have read during the past week. This is a way of visualizing word frequencies at a glance. As expected, “economy”, “prices”, “inflation”, “bank”, “credit” and “dollar” were the words most often used in financial reports.

The mystery of where the markets are heading continues, reminding me of physicist Niels Bohr's quotation: “Tomorrow is going to be wonderful, because tonight I do not understand anything.” (Hat tip: Paul Kedrosky's Infectious Greed .)

“Very frankly, I can't come to a firm conclusion as to whether we're dealing with a bull or a bear market. Sometimes you just have to wait and allow the market to tell its story. Remember, we may be in a hurry, but the market never is,” said 84-year old Richard Russell .

As mentioned previously, investors should brace themselves for a lengthy convalescence period, where a shift in central bank policy to targeting GDP growth rather than inflation is part of the patient's eventual recuperation. However, in the short term I still give the nascent stock market rallies the benefit of the doubt provided the mid-July lows are sustained. Always be on the alert for new leadership groups and ensure that the earnings and valuation fundamentals stack up before committing money to the market.

Before highlighting some thought-provoking news items and quotes from market commentators, let's briefly review the financial markets' movements on the basis of economic statistics and a performance round-up.

Economy

“Global businesses are very nervous. They are more upbeat than they were in the spring, but confidence is low and is fragile,” according to the Survey of Business Confidence of the World conducted by Moody's Economy.com . The survey results suggested that the global economy was just barely skirting recession. The US, European and Japanese economy were contracting, but the Asian economy continued to post growth that was near its potential.

Economic reports released in the US during the past week were mixed and included the following:

• The July Senior Loan Officer Opinion Survey from the Fed indicated further tightening in lending standards over the previous three months. About 60% of large banks indicated tighter standards for commercial and industrial loans from the previous survey. Three-quarters of banks reported tightening standards on prime mortgage loans since the spring and the share of banks tightening standards on credit-card loans has more than doubled since the last survey.

• Total retail sales inched down 0.1% in July, following a revised 0.3% gain in June (originally 0.1%) as a decline in sales at auto dealers offset strong growth elsewhere. Sales excluding autos rose by 0.4% after gaining 0.9% in June.

• The top-line Consumer Price Index increased by 0.8% for the month and 5.6% for the year in July compared with 1.1% for the month and 4.9% for the year in June. The core CPI rate of inflation remained level at 0.3% for July, the same as in June, though the core rate of inflation for the year was 2.5% in July compared with 2.4% in June. Energy increased by 4% for the month in July compared with 6.6% in June, whereas food prices increased by 0.9% for the month compared with 0.8% in June.

• Industrial production rose by a better than expected 0.2% in July. Manufacturing and mining output improved during the month, while utilities production declined sharply. Overall, the report was similar to the industrial production reports seen so far this year: a soft reading, though not of the magnitude normally seen in recessions.

Almost one-third of US homeowners who bought in the last five years now owe more on their mortgages than their properties are worth, according to Zillow.com , an Internet provider of home valuations. Also, delinquency rates on single-family mortgages have reached their highest level on record (the Fed started tracking the statistics in 1991), pushing up the delinquency rate on all loans held by US banks.

Hat tip: Barry Ritholtz's The Big Picture

Summarizing the US economic situation, Asha Bangalore ( Northern Trust ) said: “Tax rebate dollars supported economic growth in the US in the second quarter. By the next FOMC meeting on September 16, the FOMC will have another month's data for inflation, employment, and retail sales. Employment and retail sales should continue to show weakness and headline inflation will likely be considerably lower. Therefore, the Fed is firmly on hold.”

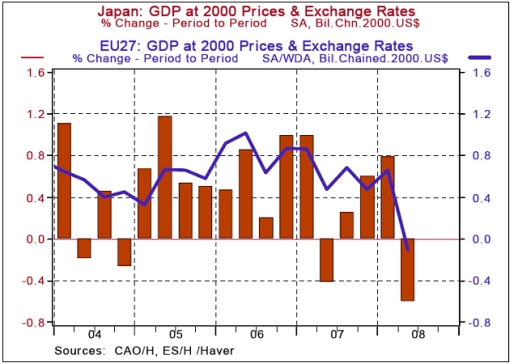

As mentioned above, the incoming reports in the Eurozone and Japan strongly point to weakening economic conditions, as shown by contracting real GDP growth in the Eurozone and Japan in the following chart:

Source: Asha Bangalore, Northern Trust – Daily Global Commentary , August 14, 2008.

WEEK'S ECONOMIC REPORTS

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Aug 12 | 8:30 AM | Trade Balance | Jun | -$56.8B | -$59.0B | -$61.9B | -$59.2B |

| Aug 12 | 2:00 PM | Treasury Budget | Jul | -$102.8B | NA | -$86.8B | -36.4B |

| Aug 13 | 8:30 AM | Export Prices ex-ag. | Jul | 0.8% | NA | NA | 0.9% |

| Aug 13 | 8:30 AM | Import Prices ex-oil | Jul | 0.9% | NA | NA | 0.9% |

| Aug 13 | 8:30 AM | Retail Sales | Jul | -0.1% | 0.0% | -0.1% | 0.1% |

| Aug 13 | 8:30 AM | Retail Sales ex-auto | Jul | 0.4% | 0.5% | 0.5% | 0.8% |

| Aug 13 | 10:00 AM | Business Inventories | Jun | 0.7% | 0.5% | 0.6% | 0.3% |

| Aug 13 | 10:35 AM | Crude Inventories | 08/09 | -316K | NA | NA | 1614K |

| Aug 14 | 8:30 AM | Core CPI | Jul | 0.3% | 0.2% | 0.2% | 0.3% |

| Aug 14 | 8:30 AM | CPI | Jul | 0.8% | 0.3% | 0.4% | 1.1% |

| Aug 14 | 8:30 AM | Initial Claims | 08/09 | 450K | 435K | 436K | 460K |

| Aug 15 | 8:30 AM | NY Empire State Index | Aug | 2.8 | NA | -5.0 | -4.9 |

| Aug 15 | 9:00 AM | Net Foreign Purchases | Jun | $53.4B | NA | $57.5B | $83.2B |

| Aug 15 | 9:15 AM | Capacity Utilization | Jul | 79.8% | 79.9% | 79.8% | 78.8% |

| Aug 15 | 9:15 AM | Industrial Production | Jul | 0.2% | 0.0% | 0.0% | 0.4% |

| Aug 15 | 10:00 AM | Mich Sentiment-Prel. | Aug | 61.7 | 63.0 | 62.0 | 61.2 |

Source: Yahoo Finance , August 15, 2008.

Next week's economic highlights in the US, courtesy of Northern Trust , include the following:

1. Producer Price Index (August 19): The Producer Price Index for Finished Goods is expected to have risen by 0.5% in July. The core PPI is most likely to have risen by 0.1% after a 0.2% increase in June. Consensus : +0.5%, core PPI +0.2%.

2. Housing Starts (August 19): Permit extensions for new single-family homes fell by 3.0% in June, but rose for that of multi-family homes. The weakness in the housing market, particularly the large inventory of unsold homes, points to a reduction of housing starts in July (940,000 versus 1.066 million in June). Consensus : 950,000.

3. Leading Indicators (August 21): Interest rate spread and consumer expectations are the only two components likely to make a positive contribution in July. Stock prices, money supply, initial jobless claims, and building permits are expected to make negative contributions. Forecasts of money supply and orders of consumer durables and non-defense capital goods are used in the initial estimate. The manufacturing workweek and vendor deliveries held steady in July. The net impact is a 0.2% drop in the leading index during July. Consensus : -0.2% versus -0.1% in June.

4. Other reports : NAHB Survey (August 19), Philadelphia Fed Survey (August 21).

Click here for a summary of Merrill Lynch 's US economic and interest rate forecasts.

A summary of the release dates of economic reports in the UK, Eurozone, Japan and China is provided here . It is important to keep an eye on growth trends in these economies for clues on, among others, which way the US dollar is going to move and how strongly.

Markets

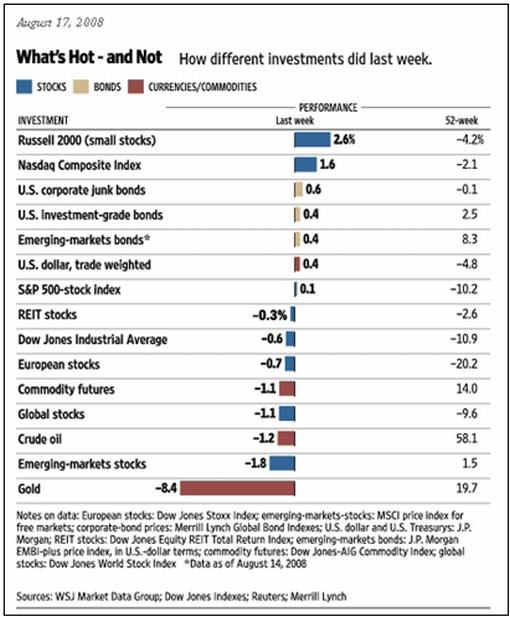

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , August 17, 2008.

Equities

Stock markets, in general, were lower during the past week, with the softer inflation outlook unable to offset the gloomy growth prospects in a number of cases. The MSCI World Index declined by 1.1% for the week, with the MSCI Emerging Markets Index losing 2.4%.

Mounting concerns about the German and Japanese economies heading for recession resulted in the XETRA Dax Index (-1.8%) and the Nikkei 225 Average (-1.1%) being the worst performers among developed markets.

The emerging markets category saw large declines by China (-6.0%), Brazil ( 4.1%), Hong Kong (-3.3%) and India (-2.9%), whereas solid gains were registered by Turkey (+3.0%), Pakistan (+3.5%) and Russia (+3.6%). Notwithstanding the past week's gains, the Russian Trading System Index is still down a hefty 28.2% from its record high of mid-May.

The US stock markets were mixed as shown by the major index movements: Dow Jones -0.6% (YTD -12.1%), S&P 500 Index +0.1% (YTD -11.6%), Nasdaq Composite Index +1.6% (YTD 7.5%) and Russell 2000 Index +2.6% (YTD -1.7%).

The outperformance of small caps is significant as they have a history of often turning up before large caps at market bottoms. A breakout through the June high should be positive for the entire market.

Source: StockCharts.com

The Russell 2000 Index and the Nasdaq Composite Index are trading above both their 50- and 200-day moving averages, whereas the Dow Jones Industrial Index and S&P 500 Index are flirting with their 50-day averages and still have some work to do in order to breach the important 200-day line – often used as an indicator of the primary trend.

Click here or on the thumbnail below for a market map, courtesy of Finviz.com , providing a quick overview of the performance of the various segments of the S&P 500 Index over the week.

Retailers were a notable pocket of strength despite persistent debate about the consumer's demise in the face of high food and gas prices, falling home values, rising unemployment and tighter credit conditions. For the week, the S&P Retail Index jumped by 4.8%, bringing its gain since the July 15 low to 23.6%.

Several retailers, including Wal-Mart (WMT), Kohl's (KSS), J.C. Penney (JCP) and Nordstrom (JWN), posted better-than-expected second quarter earnings results, although most expressed caution about the outlook for the third quarter and/or full year.

On the other end of the scale, the financial sector (-2.8%) was the week's worst sector performer, falling on omnipresent concerns about credit market conditions and low levels of business activity. This caused several broking firms to slash earnings estimates for leading investment bank Goldman Sachs (GS). Also, a warning from JP Morgan Chase (JPM) that it had seen a substantial deterioration in trading conditions since the end of the second quarter, acted as another trigger for the selling interest.

Fixed-interest instruments

Global government bond yields declined further during the past week, particularly in those parts of the world with the most dismal economic scenarios.

Leading the way, the UK ten-year Gilt yield declined by 10 basis points to 4.58% and the German ten-year Bund yield by 11 basis points to 4.15%. The Japanese ten-year bond yield closed unchanged at 1.47% after hitting a four-month low of 1.515% on Thursday.

The ten-year US Treasury Note also dropped – by 8 basis points to 3.86% – as investors turned to the perceived safety of government bonds amid continued selling of mortgage securities.

Source: StockCharts.com

US mortgage rates declined somewhat, with the 15-year fixed rate and the 5-year ARM both 3 basis points lower at 6.05% and 6.03% respectively.

Money-market rates rose on the back of strong demand for one- and three-month money lent by the Fed and the ECB.

Currencies

The US dollar's surge continued for a fifth consecutive week as the currency benefited from the view that foreign central banks will be quicker to cut rates than the Fed will be to tighten rates.

Bloomberg reported that Goldman Sachs reversed course on its dollar forecast, saying the greenback has “bottomed” as global growth weakens, oil prices decline and the US trade balance improves. “The fundamental picture for the dollar has improved substantially in recent weeks,” Goldman's Thomas Stolper wrote in a research note.

Source: StockCharts.com

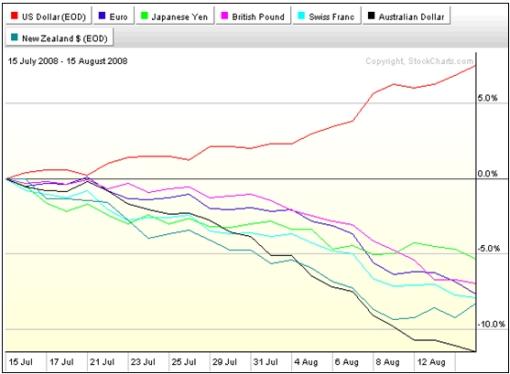

The past week saw the greenback rising against the euro (+1.6% – a six-month high), the British pound (+2.9% – a two-year peak), the Swiss franc (+1.3% – a six-month high), the Japanese yen (+0.8% – a five-month high) and the Australian dollar (+2.5% – a seven-month high).

Sterling has come under strong selling pressure as pessimism about the UK economic picture intensified, resulting in an 11-day losing streak – the longest stretch of consecutive down-days in 35 years.

The following chart illustrates the US dollar's accent against various currencies over the past month:

Source: StockCharts.com

Commodities

The dollar's strength and growing concerns of slowing demand knocked dollar-denominated commodity prices as seen in the Reuters/Jeffries CRB Index declining by a further 1.3%. The Index has plunged by 19.3% since its record peak of July 2.

Source: StockCharts.com

West Texas Intermediate crude traded at $113.9 a barrel on Friday, extending its five-week decline from a record $147.27 to 29.3%.

The rallying US dollar and reduced concerns about inflation resulted in gold bullion falling below the $800 level on Friday for the first time since December 2007. The yellow metal plunged by 8.4% over the week, with silver (-15.7%), platinum (-11.0%) and palladium (-14.4%) also at the forefront of the selling orders.

Agricultural commodities were the only category registering gains last week as a result of reassurance from the US Department of Agriculture on this year's harvest. CBOT September corn rose by 6.3%, wheat by 8.1% and soyabeans by 2.4%.

Putting a more positive spin on commodities' fall from grace, Frank Holmes ( US Global Investors ) said: “This commodities sell-off, which began in July and has continued into August, also corresponds to the long-term seasonal cycle in which prices for many commodities tend to bottom out in late summer before rebounding in the fall.”

Now for a few news items and some words and charts from the investment wise that will hopefully assist with navigating our portfolios through the treacherous investment waters. In the meantime, remember that the emphasis in these times should be on return of capital rather than return on capital.

Source: Slate

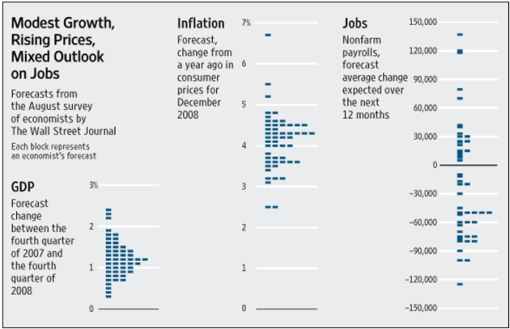

The Wall Street Journal: Forecasting survey indicates further slowdown

Economists are deeply divided on whether or not we are in a recession, according to the latest WSJ forecasting survey. WSJ's Phil Izzo and Kelsey Hubbard discuss the survey, where many economists agreed we will see a further slowdown.

Click here for the full report.

Source: Phil Izzo, The Wall Street Journal , August 14, 2008.

Financial Times: Fund managers forecast global recession

“A global recession is widely expected by fund managers as the credit crunch marks its first anniversary by mutating from a financial crisis into a world economic downturn, according to Merrill Lynch.

“Almost one-quarter of the fund managers questioned by Merrill in August for its monthly survey said the global economy was already in recession and almost half expect the world economy to contract over the next 12 months.

“However, inflation fears are fading after the recent fall in oil prices.

“In an extraordinary reversal, a net 18% of the survey's respondents said they expected global core inflation to fall over the next 12 months. Two months ago, a net 33% thought inflation would rise.

“‘Fears about stagflation are starting to give way to fears that the (global) economy is in for a period of below-trend growth and below-trend inflation,' said David Bowers, of Absolute Strategy Research and independent consultant to Merrill's fund managers surveys.

“Mr Bowers said it was ‘crystal clear' that fund managers did not believe analysts' profit forecasts with a net 83% describing earnings estimates for the coming year as ‘too high'.

“But as the economic downturn spreads to Europe and Japan, enthusiasm for US assets has been rediscovered by fund managers with 53% expecting the dollar to appreciate and 38% planning to overweight US equities over the next twelve months. Both readings are record highs.

“The fall in oil prices has prompted a partial unwinding of the highly popular ‘long' energy ‘short' financials trade.

“Among European fund managers, the net overweight position in the oil and gas sector has fallen sharply, from 62% in June to 11% in August. Meanwhile, the net underweight in banks has shrunk from 62% in June to 40%.”

Source: Chris Flood, Financial Times , August 13, 2008.

Times Online: Why the Russia-Georgia conflict matters to the West

“It would be a serious mistake for the international community to regard the dramatic escalation of violence in Georgia as just another flare-up in the Caucasus.

“The names of the flashpoints may be unfamiliar, the territory remote and the dispute parochial, but the battle under way will have important repercussions beyond the region.

“The outcome of the struggle will determine the course of Russia's relations with its neighbours, will shape Dmitri Medvedev's presidency, could alter the relationship between the Kremlin and the West and crucially could decide the fate of Caspian basin energy supplies.

“It was known that a serious confrontation had been building up. British Intelligence predicted this year that a war in the Caucasus was probable. The focus was Georgia, the West's main ally in the region and the only export route for Caspian oil and gas outside Kremlin control.

“Part of the responsibility must lie with President Saakashvili. The US-educated Geogian leader has rightly been praised for turning around his country's dire economy, transforming the Soviet-style army into a modern Western force and standing up to the Kremlin.

“On paper the small Georgian military is no match for the might of Russia. But Mr Saakashvili has calculated that his friends in the West, notably America and Britain, will protect him.

“… Russia has made clear in word and deed that it will do anything to prevent Nato's expansion on its western and southern flanks.

“America and Britain are closely involved in providing military assistance to the Georgians in the form of arms and training. The support is aimed at encouraging the rise of Georgia as an independent, sovereign state.

“But the help is also partly a means of protecting the oil pipeline across Georgia that carries crude from the Caspian to the Black Sea, the only export route that bypasses Russia's stranglehold on energy exports from the region.”

Source: Richard Beeston, Times Online , August 8, 2008.

John Authers (Financial Times): US dollar and commodities

John Authers says that the shift in forex markets ended a period when it was safe to bet against the dollar.

Click here for the full article.

Stephen Roach (Morgan Stanley): Pitfalls in a post-bubble world

“In short, Washington has responded to this financial crisis with a politically-driven, reactive approach. Policy initiatives have been framed more by the circumstances of the moment than by a strategic assessment of what it truly takes to put the US economy back on a more sustainable path.

“By perpetuating excess consumption, low saving, unrealistic goals of home ownership, and moral hazards in financial markets, this patchwork approach has the biggest flaw of all - it does little to change bad behavior. Far from heeding the tough lessons of an economy in crisis, Washington is doing little to break the daisy chain of excesses that got America into this mess in the first place.

“If this crisis is anything, it is a wake-up call. For all too long, the United States broke many of the most important rules of conduct for a leading economy. It failed to save. It levered asset bubbles in both equities and homes to sustain unparalleled excesses in current consumption. It went deeply into debt to sustain that course of action and borrowed heavily from the rest of the world to close the funding gap. The authorities were complicit in this binge – especially a central bank that condoned unbridled risk taking and excessive monetary accommodation.

“The longer the United States sustained the unsustainable, the more it believed in the perpetuity of its charmed existence. The real message of this crisis is that this game is now over. But steeped in denial and feeling the heat of voters in a politically charged presidential election year, Washington politicians insist that the game can go on.

“More than anything, America now needs ‘tough love' – a new course that owns up to years of excess and the remedies those excesses now require. It is the broad outlines of what that new approach might entail – more saving, as well as more investment in both people and infrastructure. An energy policy might be nice as well – as would be more prudent stewardship of the financial system. This program won't win any popularity contests. But in the end, it is America's only hope for a sustainable post-bubble prosperity.”

Click here for the full report.

Source: Stephen Roach, Morgan Stanley , August 1, 2008.

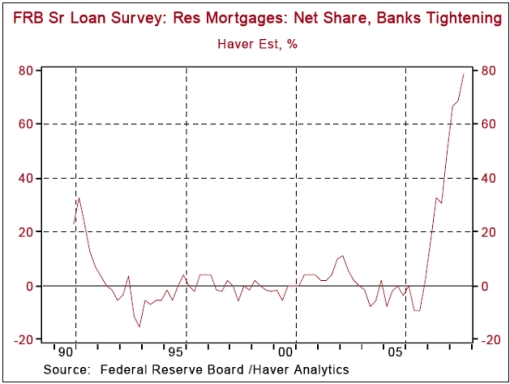

Asha Bangalore (Northern Trust): Credit conditions remain unfavorable

“The Fed has lowered the federal funds rate 325 basis points since September and set up various programs to support fragile financial markets. According to the Senior Loan Officer Opinion Survey, despite these endeavors the credit crunch remains in place for the most part.

“The details of the survey show that the housing market, which was the trigger for the current financial market crisis, is unlikely to stage a rebound in the near term. Almost 80% of respondents (78.7%) indicated that they have tightened mortgage underwriting standards, up from nearly 68.7% in the April 2008 survey.

“On the business side, the fraction of banks indicating they had tightened lending standards for small firms hit a new high (see chart 6) at 65.3%, while the percentage of banks reporting tighter conditions for large firms rose to 57.6% from 55.4% in the April survey.

“The survey also included questions about the outlook for credit standards in the second-half of 2008 and the first-half of 2009. The main message from answers to these questions is that a large percentage of banks would be tightening standards in the latter half of 2008 and the fraction of banks indicating they would tighten standards in the first two quarters of 2009 showed a small decline.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary , August 11, 2008.

John Authers (Financial Times): Credit squeeze to get more painful

“The logic of the credit squeeze is inexorable. The latest data from banks, and prices in the secondary credit market, point to a much slower economy.

“The Federal Reserve's survey of US banks' senior lending officers came out with little fanfare this week. In the past it has proved to be an excellent leading indicator. When banks tighten the supply of credit, historically this has led to lower employment, lower investment and lower consumer demand, with a lag of between six months and a year.

“Lending officers said they were continuing to tighten standards, whether on credit cards, prime mortgages, consumer or business loans, even though a strong majority of banks had done this in the second quarter. That implies a squeeze on consumption, and lower investment, as the year goes on.

“A similar exercise by the European Central Bank, polling lenders in the eurozone, seemed a little less gloomy, but only on the surface. There were slight decreases in the proportion of banks planning to tighten standards for corporate and household loans, but the supply of consumer credit was still tightening. Furthermore, lending officers said demand for company loans was decreasing and economic risks were putting pressure on them to tighten.

“The implications are not lost on the credit market. The recovery for credit in the wake of the Bear Stearns crisis petered out in May. Since then, in Europe and the US, the cost of insuring against default for investment-grade companies has risen but stayed well below recent highs, while the default risk for high-yield or lower-quality credits has shot up, almost regaining its highs. Spreads payable on speculative-grade credits are at their highest in four months.

“With banks planning to lend less and charge more for loans, this makes sense; it will be harder for companies to avoid default.”

Source: John Authers, Financial Times , August 14, 2008.

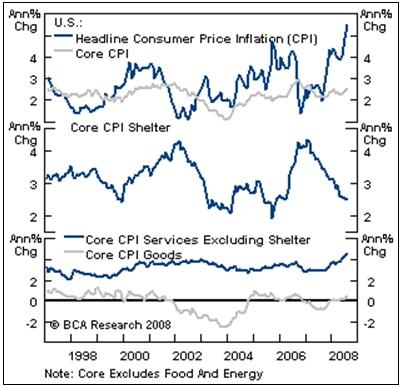

BCA Research: US inflation – soon to erode

“The July headline and core inflation numbers were higher than expected. However, lower energy prices, if sustained, should begin to help cool inflation fears. In addition, core inflation will turn lower because the economy remains weak and companies are failing to pass through higher input costs.

“We have highlighted several times before that core CPI is likely at a cyclical peak: inflation lags economic growth by several quarters and the economy continues to slow. We still assign a very low probability to rising inflation on a cyclical basis, because wage costs failed to rise during the economic boom and are already rolling over substantially. In addition, the gap between headline and core inflation is likely to close dramatically, via a sharp decline in the headline rate as both energy and food inflation cool.

“Bottom line: Hawkish Fed rhetoric is unlikely to translate into a change in policy rates for a long time because inflation fears should gradually recede. Further economic weakness remains the more immediate threat.”

Source: BCA Research , August 15, 2008.

GaveKal: US inflation implied by TIPS

Source: GaveKal – Checking the Boxes , August 15, 2008.

Asha Bangalore (Northern Trust): Despite soaring current inflation, the Fed remains on hold

“The CPI's rapid ascent in the past three months undoubtedly remains near the top of the list of concerns of the FOMC. The recent decline in oil prices has reduced the anxiety about inflation somewhat. Although food prices are worrisome, the drop in these prices in recent weeks is reassuring. The grim reality is that the Fed and other central banks can only watch and wait for weakening economic conditions to translate into a moderation of inflation, which is entirely conceivable given the nature of incoming data.

“GDP in the Euro-area declined 0.2% in the second quarter, the first since record keeping for the Euro area commenced in 1995. Germany and France, the two largest economies of the group, recorded declines in real GDP of 0.5% and 0.3%, respectively, in the second quarter. Real GDP growth in Japan also fell 0.6% in the second quarter.

“Tax rebate dollars supported economic growth in the US in the second quarter. By the next FOMC meeting on September 16, the FOMC will have another month's data for inflation, employment, and retail sales. Employment and retail sales should continue to show weakness and headline inflation will likely be considerably lower. Therefore, the Fed is firmly on hold.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary , August 14, 2008.

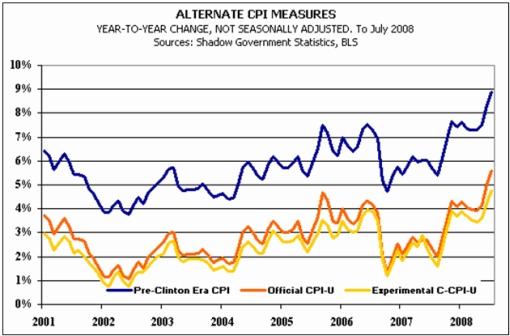

John Williams (Shadow Government Statistics): Annual CPI growth at 8.6%

“Adjusted to pre-Clinton (1990) methodology, annual CPI growth rose to roughly 8.6% in July from 8.3% in June, while the SGS-Alternate Consumer Inflation Measure, which reverses gimmicked changes to official CPI reporting methodologies back to 1980, rose to a 28-year high of roughly 13.4% in July, up from 12.6% in June … Real July Retail Sales declined 0.9% m/m and are down 2.47% y/y.”

Source: John Williams' Shadow Government Statistics , August 14, 2008.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

NS Rana

07 Oct 08, 00:14 |

US Economy is crashing but US $ is going up !

US Economy is crashing but US $ is going up how and why ? |