Greece Debt Crisis Outrageous Malevolence

Interest-Rates / Eurozone Debt Crisis Feb 11, 2017 - 03:44 PM GMTBy: Raul_I_Meijer

Earlier this week I was talking in Athens to a guy from Holland, who incidentally with a group of friends runs a great project on Lesbos taking care of some 1000 refugees in one of the camps there. But that’s another topic for another day. I was wondering in our conversation how it is possible that, as we both painfully acknowledged, people in Holland and Germany don’t know what has really happened in the Greek debt crisis. Or, rather, don’t know how it started.

Earlier this week I was talking in Athens to a guy from Holland, who incidentally with a group of friends runs a great project on Lesbos taking care of some 1000 refugees in one of the camps there. But that’s another topic for another day. I was wondering in our conversation how it is possible that, as we both painfully acknowledged, people in Holland and Germany don’t know what has really happened in the Greek debt crisis. Or, rather, don’t know how it started.

That certainly is a big ugly stain on their media. And it threatens to lead to things even uglier than what we’ve seen so far. People there in Northern Europe really think the Greeks are taking them for a ride, that the hard-working and saving Dutch and Germans pay through the teeth for Greek extravaganza. It’s all one big lie, but one that suits the local politicians just fine.

By accident(?!), I saw two different references to what really happened, both yesterday in the UK press. So let’s reiterate this one more time, and hope that perhaps this time someone in Berlin or Amsterdam picks it up and does something with it. There must be a few actual journalists left?! Or just ‘ordinary’ people curious enough, and with some intact active neurons, to go check if their politicians are not perhaps lying to them as much as their peers are all over the planet.

What I’m talking about in this instance is the first Greek bailout in 2010. While there are still discussions about the question whether the Greek deficit was artificially inflated by the country’s own statisticians, in order to force the bailout down the throats of the then government led by George Papandreou, there are far fewer doubts that the EU set up Greece for a major league fall just because it could, and because Dutch, French, German politicians could use that fall for their own benefit.

The reason to do all this would have been -should we say ostensibly or allegedly?-, to get Greece in a situation where the Germans and the French could abuse the emergency they themselves thus created, to transfer the Greece-related bad debts of their banks to the EU public at large, and subsequently to the Greek public, instead of forcing the banks to write these debts down. That is still the core of the Greek problem to this day. It’s also the core problem with the IMF’s involvement: the fund’s statutes prescribe it should have insisted on writedowns long ago, from the very first moment it got involved.

The bailout, as Yanis Varoufakis repeats below, was not -and never- meant to help Greece. Instead, it was meant to do the exact opposite, to enable Europe’s richer countries -and their banks- to escape the only just punishment for reckless lending practices, by unloading their debt onto the Greek people.

Varoufakis Accuses Creditors Of Going After Greece’s ‘Little People’

Former Greek finance minister Yanis Varoufakis [..] said that the country has been put on a fiscal path which makes everyday life “unsustainable” in Greece. “The German finance minister agrees that no Greek government, however reformist it might be, can sustain the current debt obligations of Greece,” he said. Earlier in the day, Wolfgang Schäuble told German broadcaster ARD that Greece must reform or quit the euro. “A country in desperate need of reform has been made unreformable by unsustainable macroeconomic policies,” Mr Varoufakis said.

He said that “instead of attacking the worst cases of corruption, for six years now the creditors have been after the little people, the small pharmacists, the very poor pensioners instead of going for the oligarchies”. Greece in 2010 was given a huge loan that Mr Varoufakis said was not designed to save the bankrupt country but to “cynically transfer huge banking losses from the books of the Franco German banks onto the shoulders of the weakest taxpayers in Europe”.

The Financial Times, in a rare moment of lucidity, and with an unintentionally hilarious headline, puts its fingers on that same issue, as well as a few additional sore spots, and with admirable vengeance and clarity:

Conflict Over Athens’ Surplus Needles The IMF

First of all, to put Greece and ‘sustainable growth’ together in one sentence is as preposterous as it is to do the same with Greece and ‘surplus’. But more importantly, the FT is right in just about every word here. Europe de facto decides what the IMF does. So despite all the recent conflicts between the Troika members (though they reportedly just announced they agreed on what to dictate to Greece over the weekend), it’s really all EU (i.e. Germany, France) all the time. Greece never stood a chance, and neither did justice.

The point about upcoming elections in Holland, France and Germany gets more important by the day. Since former EU parliament chief Martin Schulz left that post to head the ‘socialist’ SPD in Germany’s elections, he’s seen his poll numbers soar so much that Merkel and Schaeuble are getting seriously nervous about their chances of re-election. Like in all countries these days, certainly also in Europe, their knee-jerk reaction is to pull further to the right. Which is the opposite of setting the record straight with regards to.

As for Dijsselbloem, Schaeuble’s counterpart as finance minister for Holland, his Labor Party (PVDA) -yes, that twit claims to be a leftie- is down so much in the polls that you have to wonder where he gets the guts -let alone the authority- to even open his mouth. PVDA has 38 seats in the Dutch parliament right now and are predicted to lose 27 of them and have just 11 left after the March 15 vote, taking them from 2nd largest party to 7th largest. And out of power.

And he still heads the eurogroup, including in the negotiations with Greece and the IMF?! It’s a strange world. Dijsselbloem proudly proclaimed this week that without the IMF being involved in the next bailout, Holland wouldn’t ‘give’ Greece another penny anymore. Think Dijsselbloem and Schaeuble don’t know what happened in 2010? Of course they do. They know better than anyone.

It’s simply better for their careers -or so they think- to further impoverish the entire Greek nation and the poorest of its citizens than it is to come clean, to tell their people the whole story has been based on dirty tricks from the start. And since their media refuse to tell the truth, too, the story will last until at least after their respective elections. Thing is, Dijsselbloem will be out of a political job by March 16, so what’s he doing, setting himself up for a juicy job at one of the banks whose debts were transferred to Greek pensioners in 2010? No conscience?

Perhaps Greece’s best hope is, of all people, Donald Trump. Yeah, a long shot if ever you saw one. But Trump can overrule the IMF board simply because the US is the biggest party involved in the fund. He can tell that divided board to get its act together and stop harassing a valuable NATO member. At least he has the business sense to understand that a country with 23% unemployment -and that’s just the official number- and 50-60% youth unemployment cannot recover no matter what happens, and that sustainable growth, any kind of growth, is an impossibility once you take people’s spending power away.

Meanwhile, elite and incumbent Europe seems to think that publicly agitating against Trump is the way to go (they may come to regret that stance, and a stance it all it is). Trump’s apparent choice for EU ambassador, economist Ted Malloch, was accused by European Parliament hotshots Weber and Verhofstadt -in a letter, no less- of “outrageous malevolence” towards “the values that define this European Union”, for saying the Union needs ‘a little taming’. For some reason, they don’t seem to like that kind of thing. “Outrageous malevolence”, we’re talking Nobel literature material here.

Malloch also said EU president Juncker was a “very adequate mayor, I think, of some city in Luxembourg.” And that he “should go back and do that again.” And Malloch said on Greek TV this week that Greece should have left the eurozone four years ago. “Why is Greece again on the brink? It seems like a deja vu. Will it ever end? I think this time I would have to say that the odds are higher that Greece itself will break out of the euro.”

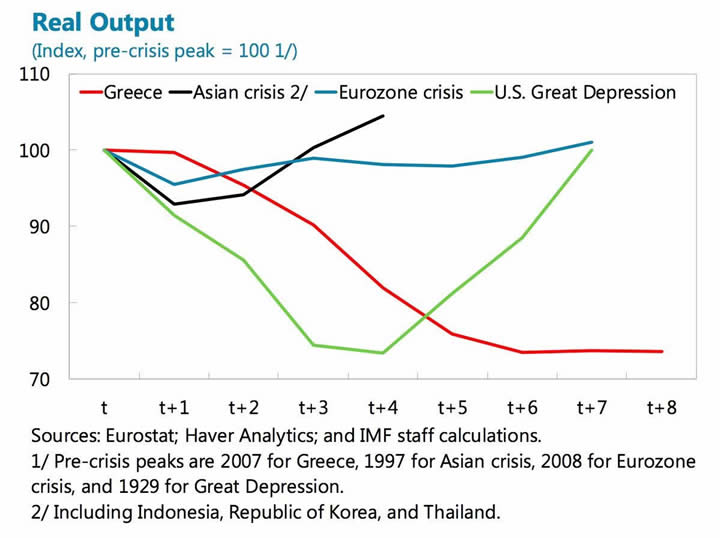

Why would he say that? How about because of the numbers in this by now infamous graph, straight out of the IMF itself, which shows EU countries have conspired to plunge one of their fellow “Union” member states into a situation far worse than the US was in during the Great Depression? Would that do it?

And we haven’t even touched on the role that Goldman Sachs plays in the entire kerfuffle, with its fake loans and derivatives, yet another sordid tale in this Cruella De Vil web of power plays spun by incompetent petty men. And Americans think they got it bad… Guess that Goldman role makes it less likely for Trump to interfere in Greece’s favor. Which would seem a bad idea, for everyone involved, not least of all because of rising tensions with Turkey over islands and islets and rocks (I kid you not) in the Aegean Sea.

It would be much better and safer for Trump, and for all of Europe, to make sure Greece is a strong nation, not a depressed and demoralized penal colony for homeless and refugees. That is asking for even more trouble. But nary a soul seems to be tuned in to that, it’s all narrow windows, short term concerns and upcoming elections. No vision.

Or perhaps Merkel will do something unexpected. Word has it that Greek finance minister Tsakalotos is meeting with Angela this weekend, a move that would seem to bypass Schaeuble, who once again said yesterday that Greece can only get a debt writedown if it leaves the eurozone. And that’s something Merkel is not exactly keen on. If only because it means unpredictability, volatility, not a great thing if your popularity as leader is already on shaky ground.

But to summarize, the Greek people didn’t do this. Of course plenty of Greek citizens borrowed more money than they should have in the first decade of the millenium, stories about credit cards in people’s mailboxes with a ‘free’ €5000 credit on them are well known in Athens. But they were by no means the ones who profited most. And the country has a long history of corruption and tax evasion. Which is what the French and German banks ‘cleverly’ played into as their politicians acted like they had no idea. Still, none of that comes even close to a reason or an excuse for completely eviscerating a fellow member of both the EU and NATO.

And it makes little sense. Do these people really want to risk peace in the eastern Mediterranean, or inside Greece itself (which will inevitably explode if this continues), just in order to keep Commerzbank or BNP Paribas out of the trouble they rightfully deserve to be in?

No, it’s not Tim Malloch’s ‘statements that reveal’ “outrageous malevolence” towards “the values that define this European Union”. It’s the actions of the European Union itself that do.

By Raul Ilargi Meijer

Website: http://theautomaticearth.com (provides unique analysis of economics, finance, politics and social dynamics in the context of Complexity Theory)© 2017 Copyright Raul I Meijer - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Raul Ilargi Meijer Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.