Commodities Keel Over as US Heads for Prolonged Recession

Economics / Recession 2008 - 2010 Aug 03, 2008 - 02:54 PM GMT

As oil prices seesawed through the past week, fresh uncertainty about the outlook for the beleaguered financial sector triggered another wave of volatility in financial markets.

As oil prices seesawed through the past week, fresh uncertainty about the outlook for the beleaguered financial sector triggered another wave of volatility in financial markets.

With the exception of Friday, crude prices closed each day with a gain or loss of more than 1%, with US stocks doing likewise as sentiment waxed and waned on the back of a barrage of economic and corporate earnings reports. Economic data were mixed, whereas earnings were mostly better than feared. After all the action, the S&P 500 Index closed the week virtually unchanged, posting a small gain of 0.2%.

David Fuller ( Fullermoney ) re-emphasizes that the oil price is currently by far the most important factor in terms of global GDP growth. Consequently it is also a huge influence on the direction of various stock market indices, and big moves up or down have a psychological leash effect on currencies and other commodities.

Source: Financial Times , July 29, 2008.

Also center to the roller-coaster ride was Merrill Lynch (MER), plunging 11.6% on Monday, prior to announcing drastic steps to right its capital position on Tuesday. Its stock fell by 9.5% to a 10-year low on the news, but then rebounded to finish the day 7.9% higher.

Traders speculated that the latest capital raise was a sign that the worst was over for financials, but Meredith Whitney, analyst of Oppenheimer & Co and “godmother” of financials, had no illusions and said in an interview that 25 institutions would have to bolster their balance sheets within the next two months.

Offering some reprieve to the financial sector, the Fed, together with the European Central Bank and the Swiss National bank, announced that “emergency” lending facilities to bolster the money markets would stay in force until January 30. The facilities were implemented to improve liquidity arising from the credit market turmoil.

Formalizing the housing bill, President Bush signed into law legislation to support homeowners facing foreclosure and to offer a lifeline to Fannie Mae (FNM) and Freddie Mac (FNM).

Separately, the SEC is extending its temporary restriction on naked short selling on 19 financial institutions until August 12.

Next, a tag cloud of the text of all the articles I have read during the past week. This is a way of visualizing word frequencies at a glance. It is quite obvious that the key areas last week were “banks”, “prices”, “inflation” and “growth”, with “housing” and “financial” also prominent. As the saying goes: A picture paints a thousand words …

Volatility of the S&P Financials Index is as high as it has been since 1987. Gavekal states: “Spikes in volatility have often signaled a turning point.” I maintain that what is good for the banks is good for the overall stock market and vice versa, and one should pay particular attention to this group.

Stock Trader's Almanac alerts us that August typically ranks among the worst months of the year and anchors the middle of the worst four months of the year, namely July to October. “The month is generally weak in the first half, then stronger in the middle,” says editor Jeffrey Hirsch.

This is an exceptionally difficult market to read. In my opinion, we are still in a primary bear market, but this does not preclude powerful rallies. From a short-term perspective, a decline below the July 28 lows will cause a serious headwind for any recovery rally, whereas a drop below the mid-July lows will significantly increase the risk of another general sell-off. On a multi-year horizon, we are probably in for an extended convalescence period of relatively low returns. In short, not a dartboard market, but also not necessarily bad from a canny stock-picking perspective.

Before highlighting some thought-provoking news items and quotes from market commentators, let's briefly review the financial markets' movements on the basis of economic statistics and a performance round-up.

Economy

“The global economy continues to skirt recession,” according to the Survey of Business Confidence of the World conducted by Moody's Economy.com . “While the US, European and Japanese are contracting moderately, the Asian economy continues to experience growth that is near its potential and South American growth is just below potential.”

Economic reports released in the US during the past week included the following key data:

• Real GDP increased by 1.9% in the second quarter at an annualized rate, below the consensus expectation of 2.4% growth. Over the past year, real GDP has increased by 1.8%. Growth was 0.9% in the first quarter, revised downward from 1% last month. Relative to the first quarter, trade and consumer spending were positives for growth; there was also a smaller decline in homebuilding. A large drop in inventories offset these positives to some extent.

• The economy lost fewer jobs than expected in July, but it is certainly not out of the woods yet. Payrolls fell by 51,000, while losses for the previous two months were revised downward. However, the unemployment rate increased by 20 basis points to 5.7% – the highest level in more than four years.

• The Institute for Supply Management's Manufacturing Index inched slightly lower to 50 for July compared with June's 50.2. The modest dip is about on par with expectations and the ISM Index is consistent with a sluggish economy that has avoided a severe downturn.

• The Conference Board Index of Consumer Confidence rebounded slightly in July, rising to 51.9 from June's 51.0 (revised from 50.4).

Summarizing the economic situation, Drew Matus, economist of Merrill Lynch, said in a research report : “Recent data releases and reports suggest that the consumer will continue to be pressured on all fronts: income (or cash flow), wealth and credit. Consumers can spend using any of these buckets. However, with the labor market continuing to weaken, housing continuing to deteriorate and credit harder to come by, the outlook for spending remains bleak despite recent declines in gasoline prices.”

“The US may now be in a ‘very long' recession that will drive the unemployment rate higher, with little that the Federal Reserve can do to help,” remarked Harvard University's Martin Feldstein. “I don't see recovery on the horizon,” Feldstein, who headed the National Bureau of Economic Research until June and serves on the group's recession-dating panel, said in an interview with Bloomberg .

Hat tip: Barry Ritholtz's The Big Picture , July 31, 2008.

As far as the Fed's upcoming interest rate decision on Tuesday is concerned, Asha Bangalore ( Northern Trust ) said: “It is nearly certain the Fed will leave the Federal funds rate unchanged at the August 5 meeting. The market expects a higher Federal funds rate at the end of the year. We do not. The details of the GDP report point to significant weakness in the economy. Against this backdrop and financial market fragility, the Fed would only exacerbate the economic situation by raising the Federal funds rate in haste. Fighting inflation will have to remain on the back burner until financial and economic conditions improve. By that time, inflation is likely to be moderating as it is a lagging economic process.”

Asha's colleague Paul Kasriel ( Northern Trust ) added: “If it walks like a recession and talks like a recession, it must be a recession. Is the Fed going to raise its funds rate target over the remainder of 2008? Not bloody likely!”

In the Eurozone, inflation accelerated to the fastest pace in more than 16 years, with the 15-nation number rising to 4.1% in July. Furthermore, economic sentiment declined to its lowest level in five years and the manufacturing PMI dropped to 47.4 in July from 49.2 in June. (A value below 50 means contracting activity.) Germany, the largest economy of the region, seems destined to record negative GDP growth in the second quarter.

Also, the data from Britain remain grim, with the Nationwide Housing Price Index falling for the ninth consecutive month in July (down 8.1% since a year ago), consumer confidence plunging to its lowest level since the survey began in 1974, and the manufacturing PMI dropping from 45.9 in June to 44.3 last month – the lowest reading since December 1998.

Moving to Asia, industrial production in Japan contracted 2% month to month in June, making it three down-months out of the past four. Inflation accelerated to 1.9% in June, the fastest pace in more than a decade.

China's manufacturing PMI dropped below 50 for the first time since 2005, suggesting a contraction in manufacturing that is hurt by both slower exports and higher input costs.

In summary, a more pronounced slowdown in global economic activity is rapidly manifesting itself.

WEEK'S ECONOMIC REPORTS

Date |

Time (ET) |

Statistic |

For |

Actual |

Briefing Forecast |

Market Expects |

Prior |

| Jul 29 | 10:00 AM | Consumer Confidence | Jul | 51.9 | 50.0 | 50.0 | 51.0 |

| Jul 30 | 8:15 AM | ADP Employment | Jul | 9K | - | -60K | -77K |

| Jul 30 | 10:35 AM | Crude Inventories | 07/26 | -81K | NA | NA | -1558K |

| Jul 31 | 8:30 AM | Chain Deflator-Adv. | Q2 | 1.1% | 2.7% | 2.4% | 2.6% |

| Jul 31 | 8:30 AM | Employment Cost Index | Q2 | 0.7% | 0.7% | 0.7% | 0.7% |

| Jul 31 | 8:30 AM | GDP -Adv. | Q2 | 1.9% | 2.8% | 2.3% | 0.9% |

| Jul 31 | 8:30 AM | Initial Claims | 07/26 | 448K | 380K | 395K | 404K |

| Jul 31 | 8:30 AM | Chain Deflator-Adv. | Q2 | 1.1% | 2.7% | 2.4% | 2.6% |

| Jul 31 | 8:30 AM | Employment Cost Index | Q2 | 0.7% | 0.7% | 0.7% | 0.7% |

| Jul 31 | 8:30 AM | Initial Claims | 07/26 | 448K | 380K | 395K | 404K |

| Jul 31 | 9:45 AM | Chicago PMI | Jul | 50.8 | 50.1 | 49.0 | 49.6 |

| Aug 1 | 12:00 AM | Auto Sales | Jul | - | 5.0M | NA | 4.9M |

| Aug 1 | 12:00 AM | Truck Sales | Jul | - | 5.0M | NA | 5.0M |

| Aug 1 | 8:30 AM | Average Workweek | Jul | 33.6 | 33.8 | 33.7 | 33.7 |

| Aug 1 | 8:30 AM | Hourly Earnings | Jul | 0.3% | 0.3% | 0.3% | 0.3% |

| Aug 1 | 8:30 AM | Nonfarm Payrolls | Jul | -51K | -40K | -75K | -51K |

| Aug 1 | 8:30 AM | Unemployment Rate | Jul | 5.7% | 5.5% | 5.6% | 5.5% |

| Aug 1 | 8:30 AM | Hourly Earnings | Jul | 0.3% | 0.3% | 0.3% | 0.3% |

| Aug 1 | 8:30 AM | Average Workweek | Jul | 33.6 | 33.8 | 33.7 | 33.7 |

| Aug 1 | 10:00 AM | Construction Spending | Jun | -0.4% | -0.1% | -0.3% | 0.0% |

| Aug 1 | 10:00 AM | ISM Index | Jul | 50.0 | 50.5 | 49.2 | 50.2 |

Source: Yahoo Finance August 1, 2008.

In addition to the Federal Open Market Committee interest rate announcement (Tuesday, August 5) and Bank of England and European Central Bank rate decisions (Thursday, August 7), next week's economic highlights, courtesy of Northern Trust , include the following:

1. Personal Income and Spending (August 4): The earnings and payroll numbers for June indicate moderate growth in income (+0.2%). Auto sales fell to an annual rate of 13.6 million from 14.3 million in May. Non-auto retail sales were lackluster, excluding price-related hikes in gas and food sales. All of the available information points to a steady reading of consumer spending in July. Consensus : Personal Income -0.2%, Consumer Spending 0.5%.

2. Other reports : Factory orders (August 4), Pending Home Sales (August 7), Productivity and Costs (August 8).

Click here or on the thumbnail below for a summary of Merrill Lynch 's economic and interest rate forecasts.

Click here or on the thumbnail below for a summary of Merrill Lynch 's economic and interest rate forecasts.

Markets

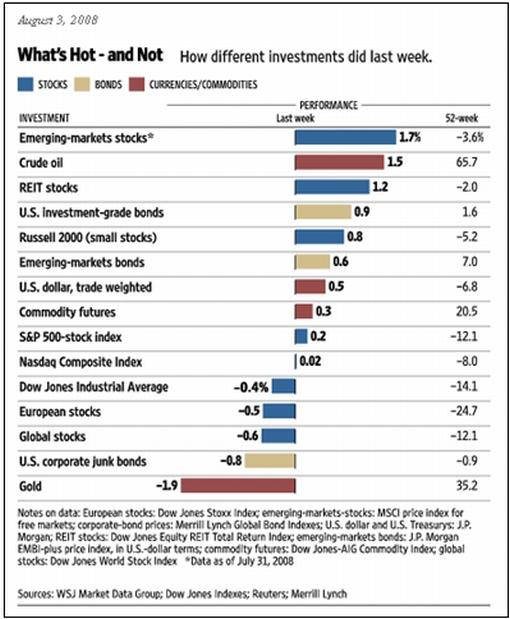

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , August 3, 2008.

Equities

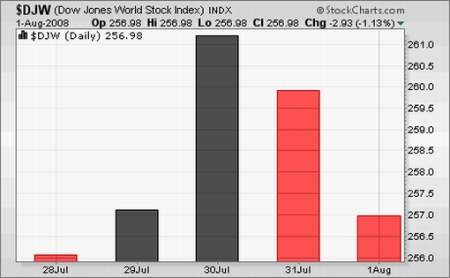

Global stock markets, in general, ended the volatile past week in the red, with the Dow Jones World Index registering a loss of 0.6%.

The Japanese Nikkei 225 Average was the worst performer among developed markets, declining by 1.8%.

The emerging markets category included a mixed bunch, varying from Turkey (+14.4%), the Philippines (+2.9%) and India (+2.7%) that performed strongly, to the less fortunate markets such as Pakistan (-7.8%), Taiwan (-3.2%) and China (-2.2%).

The MSCI World Index has been outperforming the MSCI Emerging Markets Index over the past month (-2.5% versus -4.2%), the past three months ( 9.4% versus -12.6%) and the year to date (-14.0% versus -16.4%). (Click here for a comprehensive global stock market performance round-up.)

The US stock markets were mixed, with mid-cap and small-cap stocks outperforming their larger counterparts. The major index movements were: Dow Jones Industrial Index -0.4% (YTD -14.6%), S&P 500 Index +0.2% (YTD -14.2%), Nasdaq Composite Index 0% (YTD 12.9%) and Russell 2000 Index +0.8% (YTD -6.5%).

Click here or on the thumbnail below for a market map, courtesy of Finviz.com , providing a quick overview of the performance of the various segments of the S&P 500 Index over the week.

Click here or on the thumbnail below for a market map, courtesy of Finviz.com , providing a quick overview of the performance of the various segments of the S&P 500 Index over the week.

The paper products group was the best performer for the week, rising by 18%. Both members of the group, International Paper (IP) and MeadWestvaco (MWV), rose after posting better-than-expected earnings reports. The personal products group was the second-best-performing group, up by 14%, led by Avon Products (AVP), which reported earnings in excess of the analyst consensus estimate.

The real estate management and development group was the worst performer, down by 26%, led down by its single member, CB Richard Ellis Group (CBG), which reported earnings substantially below expectations. The specialized finance group (-7%) was also among the underperformers. Stock exchange operator NYSE Euronext (NYX) reported earnings that were slightly below the consensus estimate.

As far as corporate news was concerned, Exxon Mobil (XOM) – the world's largest company by market capitalization – posted a 14% increase in net income to $11.68 billion, marking the largest quarterly profit in US history.

General Motors (GM) declined by 14%, swinging to a massive $15.5 billion second-quarter net loss as consumer preferences shifted away from large trucks and SUVs in the face of record gasoline prices.

Fixed-interest instruments

Government bonds gained ground as the global economic outlook worsened and the prospects faded of interest rate increases any time soon.

The two-year US Treasury Note dropped by 21 basis points during the week to close at 2.51%. Similarly, the UK two-year Gilt yield declined by 19 basis points to 4.86%, the German two-year Schatz yield by 17 basis points to 4.27% and the Japanese two-year bond yield by 3 basis points to 0.75%.

US mortgage rates also declined, with the 15-year fixed rate dropping by 7 basis points to 5.97% and the 5-year ARM 9 basis points higher at 5.95%.

Credit markets eased somewhat as shown by the slightly narrower spreads of both the CDX (North American, investment grade) Index and the Markit iTraxx Europe Crossover Index.

Currencies

Currency traders' benign view of the US economic situation caused the US Dollar Index to rise by 0.9%.

Individually, the greenback gained ground against the euro (-0.9%), the British pound (-0.8%) and the Swiss franc (-1.3%), but lost marginally against the Japanese yen (+0.2%).

The Australian dollar declined sharply on indications that the Reserve Bank of Australia would seriously consider cutting interest rates at its policy meeting next week. With the Chinese manufacturing PMI falling below 50, concerns were also raised that Chinese demand for Australian commodities might have peaked.

Commodities

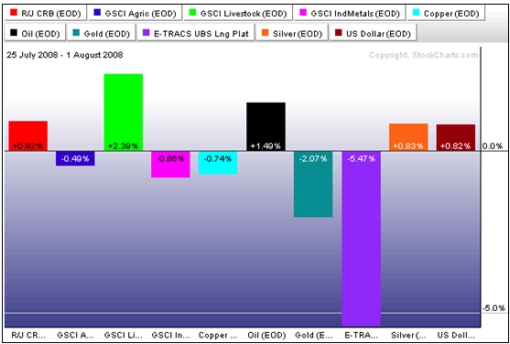

Crude oil prices seesawed during the past week, with West Texas Intermediate hitting a high of $128.60 and a low of $120.80, settling the week with a 1.5% gain as a result of an unexpected drop in gasoline inventories. Oil lost 11.5% during July – the biggest monthly decline in absolute terms in 25 years and in percentage terms since 2004 – on concern that global consumption is falling amid slowing economic growth.

Platinum (-5.5%) and palladium (-4.2%) came under heavy selling pressure as poor results from the vehicle manufacturers stoked fears of much weaker demand. Gold bullion (-2.1%) experienced further weakness, but silver (+0.8%) bucked the trend.

The chart below shows the past week's performance of the various commodities.

Source: StockCharts.com .

Now for a few news items and some words and charts from the investment wise that will hopefully assist in preserving our capital in these demanding times. And remember the old Boy Scout motto: “Be prepared” for all eventualities.

Source: Slate

Barron's: Nouriel Roubini – $2 trillion of credit-related losses

Source: Robin Goldwyn Blumenthal, Barron's , August 4, 2008.

Charlie Rose: A conversation with Pimco's Mohamed El-Erian

Source: Charlie Rose , July 24, 2008.

CNBC: Housing, economy still far from recovery – Greenspan

“Former Federal Reserve Chairman Alan Greenspan said the US is ‘nowhere near the bottom' of the housing slump and is ‘right on the brink' of a recession.

“In an exclusive interview on CNBC, Greenspan said the US economy is holding up ‘rather well' considering the ‘extraordinary pressures from the financial sector'. But he added that a recession appears inevitable.”

Click here for the full article.

Editor's comment: Greenspan has been the world's worst economic forecaster.

Source: CNBC , July 31, 2008.

Mr Mortgage: Meredith Whitney, godmother of financials, gives her outlook

“Whitney says (loosely transcribed):

• Fed knows there is no quick fix. Every time they open window they lose fire power for next crisis. There is not much capital out there that wants to rescue brokers.

• I keep saying we are less than 50% done with this crisis and are still there.

• All capital raised by banks so far ($450 billion) was only to plug holes and not to grow business.

• All banks' ‘assets' marked at unrealistic levels

• Creditors have cut mortgages and credit lines to the areas with the worst house prices depreciation. That will hurt consumers even more.

• Corporate loan market will get hit soon as well.

• Maria was prodding to find out how quickly the stock prices were going back to the highs. Pump Pump Pump! Whitney says: There is no way the bank stocks will return to the highs in next 3 years. No comment on 5 years out.

• The brokers are not growing capital and diluting the shareholder. They can't grow earnings that way.

• Merrill raised tremendous amounts of capital just to plug holes. They still have to shed assets and are not out of woods yet.

• Most every bank has to write down assets like Merrill and raise capital.

• Banks who got in bed with housing assets such as C, UBS, MER, BAC, WB will be in the market ‘soon' to do another capital raise.

• Everyone was involved in mortgages. All of these banks are in trouble now.

• 25 institutions will have to raise capital in next two months.

• Banks will cut dividends. I don't understand why banks raise capital and then still pay a dividend. It is not prudent for board members to keep paying when they are so capital restrained.

• Fannie Freddie in same situation as every other institution. All banks are betting on house price assumptions that are far too optimistic. No banks are close to Case-Shiller.

• Due to banks' bad math, losses will apply to everyone across the board.

• In 2006-07 $2.5 trillion was securitized. Nobody can replace this mortgage money and housing prices will continue to suffer as a result.

• When Maria asked if Lehman will survive, she said ‘huh huh huh huh huh huh I don't know'.

• I am very opinionated on the short selling rule. If you want to have faith in the capital market there has to be two sides to every trade and people have to be able to hedge. Restricting free trade will have the opposite effect and endanger the markets.

• Jamie Dimon and Goldman are ‘pros' and very cautious and aware of risks.”

Source: Mr Mortgage , July 30, 2008.

Bloomberg: Harvard's Feldstein – US may be in “very long” recession

“The US may now be in a ‘very long' recession that will drive the unemployment rate higher, with little that the Federal Reserve can do to help, said Harvard University Professor Martin Feldstein.

“‘I don't see recovery' on the horizon, Feldstein, who headed the National Bureau of Economic Research until June and serves on the group's recession-dating panel, said in an interview with Bloomberg Radio.

“Feldstein said the Fed has already lowered interest rates as much as it can to help growth, and that exports offer the only bright spot, while they aren't strong enough to fuel a recovery. A former adviser to President Ronald Reagan, he also warned that policies proposed by Senator Barack Obama, the presumptive Democratic presidential candidate, would prolong the downturn.

“The next president ‘should not be raising taxes', Feldstein said. He said he was ‘really surprised' that Obama ‘hasn't backed off his proposals for a major tax increase'.

“Feldstein said today's gross domestic product figures reinforced his view that the economy entered a recession in December or January. GDP shrank at the end of 2007 and grew less than forecast in this year's second quarter, the Commerce Department reported today.

“Fed officials have lowered their benchmark rate to 2% from 5.25% since September, bringing the reductions to a halt in June amid rising concern that inflation will accelerate. Feldstein indicated the central bank should refrain from lowering borrowing costs further.”

Source: Kathleen Hays and Timothy R. Homan, Bloomberg , July 31, 2008.

Asha Bangalore (Northern Trust): GDP growth – temporary boost from stimulus package

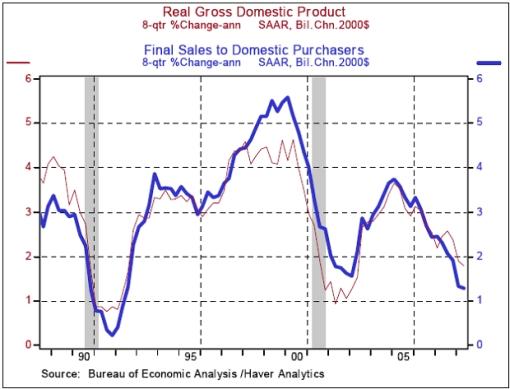

“Real gross domestic product of the US economy grew at an annual rate of 1.9% in the second quarter, following a revised 0.9% increase in the first quarter. This report also contained revisions of GDP estimates going back to the first quarter of 2005.

“Real GDP grew at a slightly slower pace during the period of revision (2005-2007). The most noteworthy aspect was the contraction in real GDP growth in the fourth quarter of 2007 (-0.2%) from an increase of 0.6% as per the previously published estimate.

“In the second quarter, consumer spending grew at an annual rate of 1.5%, which is an improvement from the 0.9% increase in the first quarter. The fiscal stimulus package gave a boost to consumer spending in the second quarter. This being a one-off event implies that going forward consumer spending is most likely to show significant weakness in the absence of extra dollars from tax rebates.

“Exports of goods and services grew at an annual rate of 9.2% in the second quarter, while imports fell 6.6%. The resultant sharp narrowing of the trade gap (-$395.2 billion versus -$462.0 billion) was another big plus for the headline. Imports have declined for three straight quarters, which has helped to narrow the trade gap. The outstanding growth in exports may not be a repeat story because incoming data from trading partners of the US has been weak, suggesting that less positive contributions from exports are likely in the quarters ahead.

“Essentially, economic growth has slowed over the past two years. We have gone down the laundry list of the different components of GDP and concluded that it is unlikely that any one sector can possibly give a lift to economic growth in the near term.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary , July 31, 2008.

Paul Kasriel (Northern Trust): If it walks like a recession and talks like a recession, it must be a recession

“ Civilian Unemployment Rate : 5.7% in July versus 5.5% in June; cycle low is 4.4% in March 2007.

Payroll Employment : -51,000 in July versus -51,000 in June, net gain of 26,000 jobs after revisions of payroll estimates for May and June.

Hourly earnings : +6 cents to $18.06, 3.4% yoy change versus 3.4% yoy change in June; cycle high is 4.28% yoy change in Dec. 2006.

“Total nonfarm payrolls fell by 51,000 in July – the seventh consecutive monthly decline. Private nonfarm payrolls fell by 76,000 in July. Although revisions to May and June total payrolls netted out to a plus 26,000 jobs, these revisions netted out to a minus 11,000 jobs in the private sector. There were job losses across a wide spectrum of industries as evidenced by the July diffusion index falling a full point to 41.2 – the lowest reading since August 2003.

“In the past 12 months, private nonfarm payrolls have declined by a net 535,000. In the past 12 months, the so-called birth/death adjustment has added a net 853,000 jobs. If the birth/death adjustment is excluded, private nonfarm payrolls declined by 1,388,000 in the 12 months ended July 2008. If the birth/death adjustment is inaccurately biasing upward private nonfarm employment, then all of the other government economic statistics that are derived from nonfarm payrolls also are inaccurately biased upward. Without the birth/death adjustment, perhaps the US economy might not look quite as ‘resilient' as it allegedly is thought to be by T he Wall Street Journal and its op-ed contributors.

“After the November elections, the National Bureau of Economic Research will tell us what we and the Fed already know – the US economy currently is in a recession. Industrial commodity prices appear to have peaked, which will begin to moderate the trend in headline US inflation in a couple of months. Businesses have little pricing power at the consumer level. There is no evidence of a wage-price spiral. The inflation-expectations' anchor does not appear to be dragging. The dollar appears to have stabilized, in large part because of economic growth in the rest of the world appears to be slowing significantly. Losses continue to mount on the books of financial institutions, which will inhibit credit creation. Is the Fed going to raise its funds rate target over the remainder of 2008? Not bloody likely!”

Source: Paul Kasriel, Northern Trust – Daily Global Commentary , August 1, 2008.

Los Angeles Times: White House cuts GDP growth forecast

“The White House cut its forecast for US economic growth this year and indicated President George W. Bush's successor will face the dual headwinds of rising unemployment and faster inflation.

“‘US gross domestic product will grow 1.6% this year and expand 2.2% in 2009, the White House's Council of Economic Advisers said in a mid-year review today. The forecasts were slashed from an outlook in February for 2.7% growth this year and 3% for 2009.

“The effects of the economic slump have worsened the job market, and the White House forecast the jobless rate will average 5.3% this year and 5.6% in 2009. The unemployment rate averaged 5.1% in the first six months of 2008 and was at 5.5% in June, unchanged from the 3 1/2-year high reached in May.

“‘The US economy has continued to expand, but growth has slowed as a result of the sharp housing decline, disruptions in financial markets, and high energy prices,' the report said. ‘Because of the recent slower economic growth, the labor market is likely to remain sluggish for a period of time before returning to better performance.'

“The consumer price index will rise 3.8% this year, compared with a February forecast for 2.7%, the White House said. Next year, the cost of living will increase 2.3%, faster than the 2.1% gain predicted five months ago.

“The White House's latest forecast for GDP growth was similar to private economists for this year and more optimistic for 2009. The economy will expand 1.6% in 2008 and grow 1.7% in 2009, according to the median estimate of economists surveyed by Blue Chip Economic Indicators this month.”

Source: Los Angeles Times , July 28, 2008.

Bill King (The King Report): US budget deficit soaring

“The US Treasury on Monday said its borrowing would increase to $171 billion this quarter. Let us note three important points: 1) Budget deficits increase 50% to 100% in recessions; 2) official budget deficit estimates historically greatly underestimate the deficits due to ridiculous assumptions; and 3) surging nationalization and socialization is substantially increasing US guarantees and debt.”

Source: Bill King, The King Report , July 29, 2008.

Financial Times: US credit crunch set to last for months

“The credit squeeze in the US economy is likely to persist for many months and might even get worse, Gary Stern, president of the Federal Reserve Bank of Minneapolis, has told the Financial Times.

“He said that with interest rates at 2% the Fed was well-placed to cope with any negative surprises on growth. By contrast, he said, it was not as well positioned to deal with any negative surprises on inflation.

“Even without any such surprises, the Minneapolis Fed chief also said real interest rates were at levels that, if sustained for too long, would not be compatible with medium-term price stability.”

Source: Krishna Guha, Financial Times , July 27, 2008.

Bill Gross (Pimco): Writing off 1 trillion dollars

“An asset deflation in turn becomes a debt deflation … Pimco estimates a total of 5 trillion dollars of mortgage loans are in risky asset categories and that nearly 1 trillion dollars of cumulative losses will finally mark the gravestone of this housing bubble. The problem with writing off 1 trillion dollars from the finance industry's cumulative balance sheet is that if not matched by capital raising, it necessitates a sale of assets, a reduction in lending or both that in turn begins to affect economic growth, creating what Mohamed El-Erian fears as a ‘negative feedback loop'.”

Source: Bill Gross, Pimco , August 2008.

Bloomberg: Bush signs measure for homeowners, Fannie, Freddie

“President George W. Bush signed into law legislation that helps 400,000 homeowners facing foreclosure and extends a lifeline to Fannie Mae and Freddie Mac.

“Bush signed the measure at the White House shortly after 7 a.m., spokesman Tony Fratto said. Treasury Secretary Henry Paulson, Housing and Urban Development Secretary Steve Preston and Federal Housing Administration Director Brian Montgomery were among those present.

“‘We look forward to putting in place new authorities to improve confidence and stability in markets, and to provide better oversight for Fannie Mae and Freddie Mac,' Fratto said.

“The law is aimed at stemming foreclosures and halting a free-fall in housing prices by providing federal insurance for refinanced 30-year mortgages for homeowners struggling to make their monthly payments.

“The measure also is designed to restore confidence in Fannie Mae and Freddie Mac by tightening regulations and authorizing the Treasury secretary to inject capital into the two biggest U.S. providers of mortgage money.”

Source: Roger Runningen, Bloomberg , July 30, 2008.

Bloomberg: Poole says Fannie, Freddie should be private firms

“William Poole, former president of the Federal Reserve Bank of St. Louis, talks with Bloomberg about Standard & Poor's proposed downgrade of Fannie Mae and Freddie Mac bonds, June's durable goods and new homes data, and the outlook for legislation to aid the hobbled mortgage market.”

Click here for the full article.

Source: Bloomberg , July 25, 2008.

Financial Times: US delays accounting changes

“Banks have been given a one-year reprieve by US accounting standard-setters from having to take up to $5,000 billion of debt assets on to their balance sheets, easing fears that they would be forced to raise large amounts of new capital quickly.

“The Financial Accounting Standards Board voted to delay until January 2010 the introduction of rules that will force banks to consolidate more off-balance-sheet vehicles directly in their accounts.

“Robert Herz, FASB chairman, said that the move was made reluctantly after a staff recommendation for a delay because there might not be enough time for all companies to adjust to the up-heaval.

“‘It does pain me to allow something that has been abused by certain folks, to let that go on for another year,' he said.”

Source: Paul J Davies and Joanna Chung, Financial Times , July 30, 2008.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.