Obstacles to Trump’s Economic Growth Plans

Economics / US Economy Nov 21, 2016 - 06:12 PM GMTBy: Raul_I_Meijer

For the second time in a few weeks (see ‘End of Growth’ Sparks Wide Discontent), former British diplomat Alastair Crooke quotes me extensively, and I return the favor. Crooke here attempts to list -some of- the difficulties Donald Trump will face in executing the -economic- measures he promised to take in his campaign. Crooke argues that, as I’ve indicated repeatedly, for instance in America is The Poisoned Chalice, the financial crisis that never ended may be one of his biggest problems.

For the second time in a few weeks (see ‘End of Growth’ Sparks Wide Discontent), former British diplomat Alastair Crooke quotes me extensively, and I return the favor. Crooke here attempts to list -some of- the difficulties Donald Trump will face in executing the -economic- measures he promised to take in his campaign. Crooke argues that, as I’ve indicated repeatedly, for instance in America is The Poisoned Chalice, the financial crisis that never ended may be one of his biggest problems.

Here, again, is Alastair Crooke:

We are plainly at a pivotal moment. President-Elect Trump wants to make dramatic changes in his nation’s course. His battle cry of wanting to make “America Great Again” evokes – and almost certainly is intended to evoke – the epic American economic expansions of the Nineteenth and Twentieth centuries.

Trump wants to reverse the off-shoring of American jobs; he wants to revive America’s manufacturing base; he wants to recast the terms of international trade; he wants growth; and he wants jobs in the U.S. – and he wants to turn America’s foreign policy around 180 degrees.

It is an agenda that is, as it were, quite laudable. Many Americans want just this, and the transition in which we are presently in – dictated by the global elusiveness and search for growth (whatever is meant now by this term “growth”), clearly requires a different economic approach from that followed in recent decades.

As Raúl Ilargi Meijer has perceptively posited, greater self-reliance “is the future of the world, ‘post-growth’, and post-globalization. Every country, and every society, needs to focus on self-reliance, not as some idealistic luxury choice, but as a necessity. And that is not as bad or terrible as people would have you believe, and it’s not the end of the world … It is not an idealistic transition towards self-sufficiency, it’s simply and inevitably what’s left, once unfettered growth hits the skids. …

“Our entire world views and ‘philosophies’ are based on ever more and ever bigger and then some, and our entire economies are built upon it. That has already made us ignore the decline of our real markets for many years now. We focus on data about stock markets and the like, and ignore the demise of our respective heartlands, and flyover countries …

“Donald Trump looks very much like the ideal fit for this transition … What matters [here] is that he promises to bring back jobs to America, and that’s what the country needs … Not so they can then export their products, but to consume them at home, and sell them in the domestic market …There’s nothing wrong or negative with an American buying products made in America instead of in China.

“There’s nothing economically – let alone morally – wrong with people producing what they and their families and close neighbours themselves want, and need, without hauling it halfway around the world for a meagre profit. At least not for the man in the street. It’s not a threat to our ‘open societies’, as many claim. That openness does not depend on having things shipped to your stores over 1000s of miles, that you could have made yourselves, at a potentially huge benefit to your local economy. An ‘open society’ is a state of mind, be it collective or personal. It’s not something that’s for sale.”

A Great Wish

That’s Trump’s ostensible great wish, (it seems). It is not an unworthy one, but things have changed: America is no longer what it was in the Nineteenth or Twentieth centuries, neither in terms of untapped natural resources, nor societally. And nor is the rest of the world the same either.

Mr. Trump rather unfortunately may find that his chief task will not be the management of this Great Re-orientation, but more prosaically, fending off the headwinds which he will face as he hauls on the tiller of the economy.

In short, there is a real prospect that his ambitious economic “remake” may well be prematurely punctured by financial crisis.

These headwinds will not be of his making, and for the main part, they lie beyond human agency per se. They are structural, and they are multiple. They represent the accumulation of an earlier monetary doctrine which will fetter the President-elect into a small corner from which any chosen exit will carry adverse implications.

Ditto for anyone else trying to steer any ship of state in this contemporary global economy. Paradoxically – in an era moving toward greater self-sufficiency – what success Trump may have, however, will likely depend not on self-reliance so much as he would like.

For his foreign policy about turn, he will depend on finding common interest with Russian President Vladimir Putin (that should not be too hard) – and for the economic “about turn” – on Trump’s ability not to confront China, but to come to some modus vivendi with President Xi (less easy).

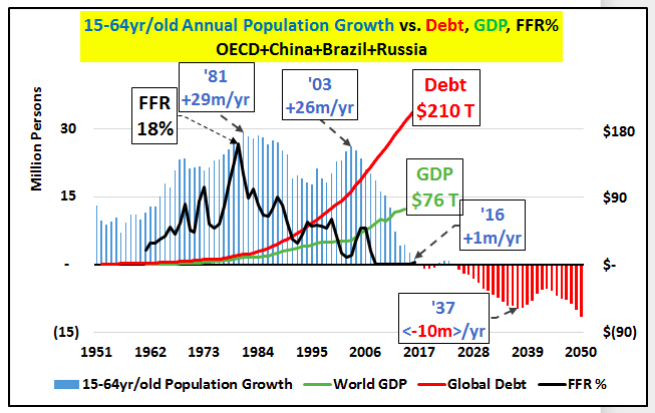

“Things are not what they were.” Complexity “theory” tells us that trying to repeat what worked earlier – in very different conditions – will likely not work if repeated later. In the Clinton era, for example, 85 percent of the U.S. population growth derived from the working-age population. The headwind that Trump will face is that, over the next eight years, 80 percent of the population growth will comprise 65+ year olds. And 65+ year olds are not a good engine of economic growth. This is not an uniquely American problem; it is a global trend too.

“The peak growth” (according to Econimica blog), “in the annual combined working age population (15-64 year/olds) among all the 35 wealthy OECD nations, China, Brazil, and Russia has collapsed since its 1981 peak. The annual growth in the working age population among these nations has fallen from +29 million a year to just +1 million in 2016 … but from here on, the working age population will be declining every year … These nations make up almost three quarters of all global demand for oil and exports in general. But their combined working age populations will shrink every year, from here on (surely for decades and perhaps far longer). Global demand for nearly everything is set to suffer.”

(FFR stands for Federal Funds Rate: i.e. the US key interest rate) Source: http://econimica.blogspot.it/2016/11/trump-lies-no-different-than-obama-or.html

And then there is China: It too is passing through a difficult “transition” from the old economy to an “innovative” one. It too, has an aging population and a debt problem (with a debt-to-gross domestic ratio reaching 247 percent). Trump argues that China deliberately holds down the value of its currency to gain unfair trade advantage, and he further suggests that he intends to confront the Chinese government on this key issue.

Again, Trump does have a point (many nations are managing their exchange rates precisely in order to try to “steal” a little bit extra growth from the diminished global pot). But as noted at Zerohedge, citing the analysis of One River Asset Management executive Eric Peters:

“What’s good for the US in this case [the rising dollar and interest rates in anticipation of ‘Trumponomics’], is not good for emerging markets (EMs). Emerging markets benefit from a weaker dollar, and you’re not going to get that. Emerging markets benefit from global capital flows moving in their direction and that’s not happening either. Back in February, emerging markets were in sharp decline, driven by (1) a strong dollar, (2) rising US interest rates, and (3) slowing Chinese growth. Then China spurred a massive credit stimulus, the Fed became wildly dovish, and the dollar declined sharply.

“Interest rates collapsed throughout the year. As the growing pool of dollar, euro and yen liquidity searched for a decent return, it headed to emerging markets. Trump has reignited the dollar rally, and his fiscal stimulus will force interest rates higher. This reversed everything. [the dollars are heading home]

“And to be sure, the Beijing boys don’t want to see material weakness ahead of next autumn’s Party Congress. But we’re currently near peak impulse from China’s Q1 stimulus.”

In short, Peters is saying that, with the appreciating dollar and rising interest rate environment, growth from emerging markets as a whole will falter, since emerging markets have effectively leveraged their economies to Chinese growth. It used to be the case that they were closely tied to U.S. growth, but it is now China which dominates the EMs’ trade flows [i.e. without China growth, the EMs languish]. The question is, can America reboot its growth whilst China and the EMs languish? It is another structural shift, whereas heretofore, it was vice versa: without U.S. growth, the EMs and China languished. Now it is the converse.

Hollowed-Out Economies

There are other structural changes of course which will make it harder for the industrially hollowed-out economies of the West to recuperate jobs off-shored earlier. Firstly, there has been a systemic shift of innovation and technology eastwards (often to a more skilled and better-educated workforce). This represents not only an economic event, but a redistribution of power too. In any case, technology in this new era is being more job destructive than creative.

In one sense, Trump’s economic plan to “get America working again” through massive debt-financed, infrastructure projects, harks back to the Reagan era, which was also a period in which the dollar was strong. But yet again, “things today are not what they were then.” Inflation then was at 13 percent, Interest rates were around 20 percent, and crucially, the U.S. debt to GDP ratio was a mere 35 percent (compared to today’s estimate of 71.8 percent or 104.5 percent with external debt included).

Then, as Jim Rickards has suggested, the strong dollar was deflationary (deliberately so), and interest rates had nowhere to go, but down. It was the beginning of the three decades’ bond boom, which finally seems to have come to an end, coincident with Trump’s election. Today, inflation has nowhere to go but up – as have interest rates – and the bond market, nowhere to go, but (perilously) down.

Growth and Jobs?

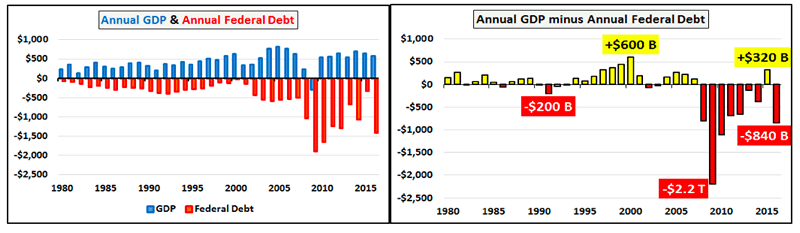

Can Trump then achieve growth and jobs through infrastructure expenditure? Well, “growth” is an ambiguous, shape-shifting term. The first chart shows both sides of the equation … the annual GDP growth and the annual federal debt incurred, spent, and (thus counted as part of the growth) to achieve the purported growth.

Source: http://econimica.blogspot.it/2016/11/trump-lies-no-different-than-obama-or.html

The second chart shows the annual GDP minus the annual growth in federal debt to achieve that “GDP growth.” In other words, unlike in the earlier Reagan times, more recently, the debt is producing no growth – but … well … just more debt, mostly.

In fact, what the second chart is reflecting is the dilution – through money “printing” – of purchasing power: away from one entity (the American consumer), through the intermediation of the financial sector, to other entities (mostly financial entities, and to corporations buying back their own shares). This is debt deflation: the American consumer ends having less and less purchasing power (in the sense of residual discretionary income).

The point here is that “growth” is becoming rarer everywhere. Russia and China, like everyone else, are in search for new sources for growth.

As Rickards has said, debt is the “devil” that can undo Trump’s whole schema: a “$1 trillion infrastructure refurbishment plan, along with his proposal to rebuild the military, will — at least in the short-term — significantly increase annual deficits. In fact, deficits are already soaring; the fiscal 2016 budget hole jumped to $587 billion, up from $438 in the prior year, for a huge 34% increase…in addition to this, Trump’s protectionist trade policies would implement either a 35% tariff on certain imports or would require these goods to be produced inside the United States, at much higher prices. For example, the increase in labor costs from goods made in China would be 190% when compared to the federally mandated minimum wage earner in the United States. Hence, inflation is on the way.”

In sum, self-sufficiency implies higher domestic costs and price rises for consumers.

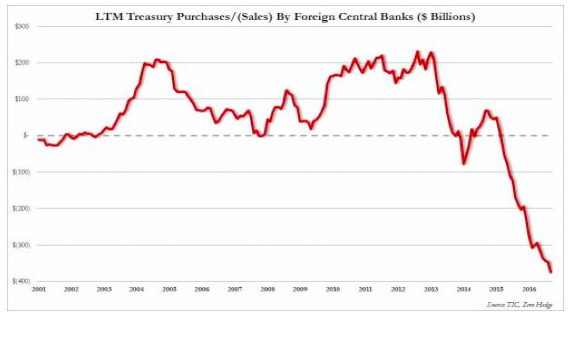

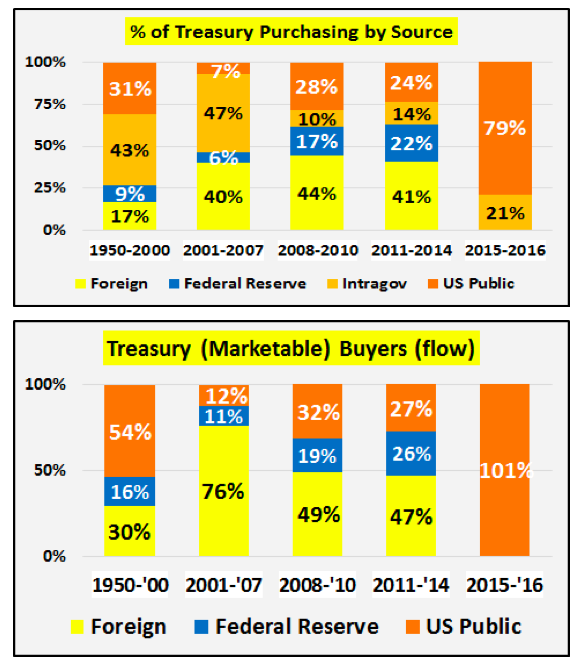

Debt will rise. And there is seemingly already a buyers’ strike against U.S. government debt underway: well over a third of a $1 trillion worth of Treasuries were disposed of, and sold in the year to Aug. 31 by foreign Central Banks. And who is buying it? (Below, the chart shows what this purchasing looks like, as a percentage of total debt issued by the Treasury). Well, foreign central banks have disappeared. (The Chinese have not bought a U.S. Treasury bond since 2011.)

(Above: who purchased the marketable debt as a percentage, by period)

Source.

It is the American public who are buying. Will they be willing to take on Trump’s $1 trillion infrastructure spree? Or, will it be “printed” in yet another dilution of the American consumer’s purchasing power? The question of whether the infrastructure splurge does give growth hangs very much in the balance to such answers. (Equity shares in construction firms will do okay, of course).

The bottom line: (Michael Pento, Pento Report): “If interest rates continue to rise it won’t just be bond prices that will collapse. It will be every asset that has been priced off that so called ‘risk free rate of return’ offered by sovereign debt. The painful lesson will then be learned that having a virtual zero interest rate policy for the past 90 months wasn’t at all risk free. All of the asset prices negative interest rates have so massively distorted including; corporate debt, municipal bonds, REITs, CLOs, equities, commodities, luxury cars, art, all fixed income assets and their proxies, and everything in between, will fall concurrently along with the global economy.

“For the record, a normalization of bond yields would be very healthy for the economy in the long-run, as it is necessary to reconcile the massive economic imbalances now in existence. However, President Trump will want no part of the depression that would run concurrently with collapsing real estate, equity and bond prices.”

A Pending Financial Crisis

Trump, to be fair, has said consistently throughout the election campaign that whoever won the Presidential campaign to take office in January would face a financial crisis. Perhaps he will not face the “violent unwind” of the QE and bond bubble as some experts have predicted, but many more – according to Bank of America’s survey of 177 fund managers over the last six days, and controlling just under half a trillion of assets – expect a “stagflationary bond crash.”

This has major political implications. Trump is setting out to do no less than transform the economy and foreign policy of the U.S. He is doing this against a backdrop of many of the followers of the liberal élite, so angered at the election outcome, that they reject completely his electoral legitimacy (and, with the élites themselves staying mum at this rejection of the U.S. democratic process). Movements are being organized to wreck his Presidency (see here for example). If Trump does indeed experience a severe financial “unwind” at a time of such domestic anger and agitation, matters could turn quite ugly.

Alastair Crooke is a former British diplomat who was a senior figure in British intelligence and in European Union diplomacy. He is the founder and director of the Conflicts Forum, which advocates for engagement between political Islam and the West.

By Raul Ilargi Meijer

Website: http://theautomaticearth.com (provides unique analysis of economics, finance, politics and social dynamics in the context of Complexity Theory)© 2016 Copyright Raul I Meijer - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Raul Ilargi Meijer Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.