OPEC Lost the Shale-Oil-War: Deflation Looms

Commodities / Crude Oil Feb 20, 2016 - 05:10 PM GMTBy: Andrew_Butter

In the unspoken plan to shut down what the oil-aristocrats called, “high cost producers”, let’s call that the Shale-Oil-War, the war-word was never mentioned.

In the unspoken plan to shut down what the oil-aristocrats called, “high cost producers”, let’s call that the Shale-Oil-War, the war-word was never mentioned.

But it was war and there were casualties, Big-Time. There will be more bankruptcies in the Exploration and Production (E&P) sector and painful write-downs by the banks who supported it; many once oil-rich countries have been pushed into recession and the ripples are traveling down the value chain...there are long lines of cold-stacked brand-new drilling barges built on credit, closed steel plants and the mines that fed them, all the way through to the FAO Food-price Index that tracks oil prices. No wonder China is in some sort of recession, they were the final assembly point for a good part of the stuff you need to get oil out of the ground.

OPEC just blinked. That means they lost and shale-oil won; this is how that played out:

Albeit unspoken, the plan was simple; (1) drive the price down so the shale-oil drillers would not be able to afford to start new wells, (2) so they would not be able to keep up payments the loans they took to buy acreage, (3) and the service companies that bought rigs and equipment would not be able to make their payments either, (4) so the banks would go bust, particularly the ones who had written the production hedge derivatives and most particularly those who took advantage of the lack of regulation and were negligent lining up counterparties, (5) absent any drilling the legacy shale-oil wells would deplete to about nothing in two years, (6) so quite soon things would get back to “normal” with the oil price bouncing to a level just under what’s economical for shale-oil drillers to start drilling again, i.e. about $70; just like T. Bourne said it would by Christmas...last Christmas, and the one before; and (7) everyone would live happily ever after.

Great plan, analysts figure that about $1-Trillion went into developing shale oil in U.S.A; out of that about $600 billion came back, so that leaves a collective hole in balance sheets of $400 billion, plus or minus. Whoever is in line to take a share of the hit won’t be trying that one on again in a hurry – R.I.P.

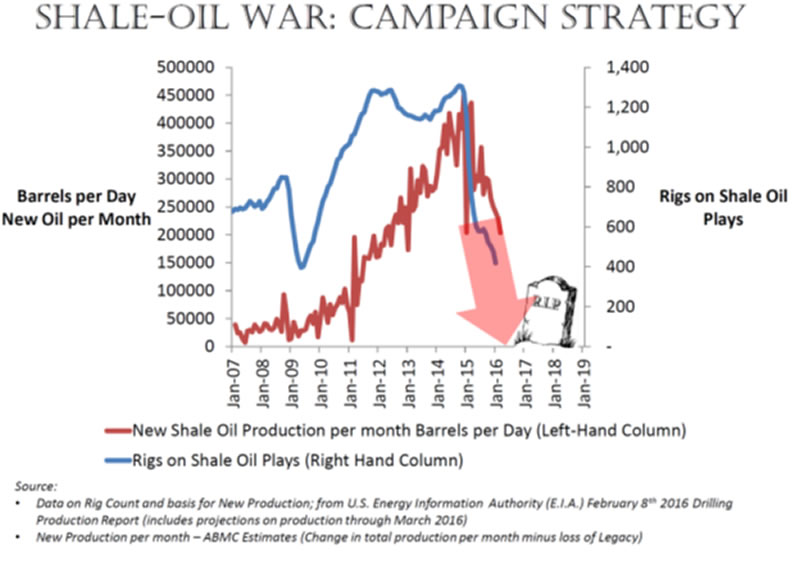

Clearly the strategy is working perfectly. Look at the chart, trend-line (the big arrow) says just one more year to go until shale-oil is a dead-duck; and all that talk of exporting the technology to places that don’t mind mini-earthquakes and polluted groundwater (allegedly), such as Argentina and Australia, will be forgotten hot air.

But here’s the thing, in war, it’s always a mistake to forget, even for a fleeting moment, the words of Helmuth von Moltke...“No battle-plan survives the first contact with the enemy”. Translating that into Cajun, that says; “it ain’t over until the fat-lady sings”; or perhaps in this case, until she blinks.

Have another look at the chart; in March 2016...in case you were wondering, E.I.A. can report pretty accurately what will happen a month in advance from the data they collect...the U.S. shale-oil drillers will bring on line an extra 200,000 barrels per day of production capacity, by comparison Iran is threatening to bring on 500,000 in a year, that works out at about 40,000 in a month, which in the grand scheme of things, is small potatoes, and anyway, talk is cheap...you should see the condition of their jackets, top-sides and conductors (I did), more likely much of that will end up in the sea and drift across to pollute the beaches in Saudi Arabia.

The shale-oil drillers are doing that when the price is under $30. That’s not “high-cost-production”

Are they mad?

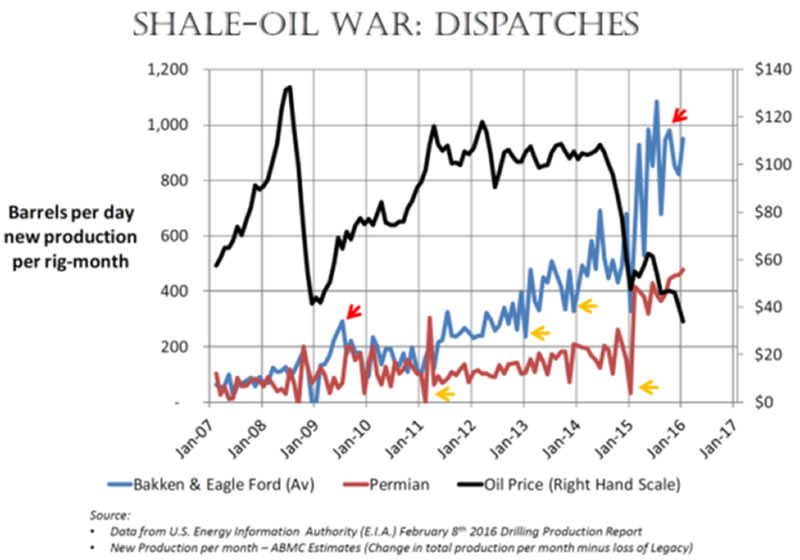

Not exactly, here is the history of on average how much oil the industry managed to bring on line out of utilizing a drilling rig for a month; for the three main shale-oil areas which account for 93% of production.

Interesting how traditionally the production rate is down in January (orange arrows), could be the cold, or perhaps everyone goes on holiday? That didn’t happen this year, I suppose anyone who still had a job sent Santa’s presents by FEDEX, but that’s bye-the-bye.

Productivity per rig in Bakken and Eagle Ford more than doubled from 2011 to 2014, and then when the price-slump started it almost doubled again, pretty much the same story in Permian. Seems that a similar increase in productivity happened in 2009, the last time oil prices tanked (red arrows).

Clearly the focus now of the vastly reduced activity is on the more promising holes, but that doesn’t explain everything. Back in the days when everyone said it only makes sense to dig for shale oil when the price was over $75, drilling concessions cost $10,000 per acre; that was about 30% of the cost; and drilling rigs were renting at $22,000 a day.

You can likely pick up prime acreage these days for $2,000 and if you already paid for it and there are no buyers, the marginal cost of drilling reference the cost of the acreage is zero. You can rent a rig for $13,000 a day; do the math, at say 4x the productivity per rig compared to 2011 it ought to make sense to drill today in some places where it would only have made sense to drill if the oil price was $75; because that tipping-point just went down, in some areas, from $75 to $15 a barrel. That’s less than the marginal cost of pumping oil out of Saudi Arabia. As in “go-blink”.

Granted, almost all of the activity is horizontal rather than vertical, and a good part could also be the new re-fracking technology that Halliburton has been peddling, all the same, it looks like someone is making good money at under $30, if not, they wouldn’t be drilling.

Of course, if/when prices go up and two out of three drilling rigs are not stacked, the rents will go up; so will the cost of acreage. And of course, most of the drillers who piled in when oil was $110 have lost their shirts and these days their bankers only talk to them via their attorneys. But just because the pioneers got scalped, doesn’t mean the next wave will; expect the same sort of consolidation that happens after all disruptive technologies go through their growing pains.

It will be interesting to see how much new oil get’s developed in April, and May. According to my wild-guess from eye-balling the chart and doing neural models on the numbers on SAS-JMP, I’d be surprised if that’s less than 150,000 barrels per day per month.

Depletion is currently running at 300,000 per day per month, so at that rate it will take seven months for total shale oil production to drop by one million barrels per day. So if OPEC and Russia continue to pump the extra three million barrels per day they brought on over the past two years, and Iran adds 500,000 barrels per day (joke); oil prices will stay super-low.

But regardless of how low and how long, the simple reality is that shale-oil will not die and it will not go away, no matter what OPEC does. Sooner or later the oil-aristocrats will wake up to the idea that defending market share against a “low cost producer”, by discounting, just makes no sense. Of course, how long it will take for that penny to drop is anyone’s guess. Meanwhile, if the protagonists want to sell oil at half the price or less than what the world can afford to pay, so they can settle their differences, all there is left to say is “Happy Christmas”.

What Next?

Back-tracking a bit; the Saudi’s knew in 2011 that oil at $110 was a bubble; their argument was that the world could not afford that price, which is/was a good argument. They were saying the world could only afford $75 and also at that price there was sufficient incentive for E&P to go and develop new oil to make up for depletion.

Except that the world was awash with easy-money so it could borrow to pay the premium. In the last big bubble caused by the Iran/Iraq war, the world also borrowed rather than go through the pain to adapt its lifestyle (bicycles), which caused rampant inflation; what was different this time; was then they borrowed from the oil-states; this time the source of money was the Central Banks.

There was no perceptible inflation this time, likely because the world was getting pushed into deflation by the fall-out from the credit-crunch, so any inflation caused by the oil bubble was offset by the deflationary effect of QE.

But bubbles always bust. In the 1980’s what bust the bubble was the development of new technology to drill for offshore oil; what bust the bubble this time was the development of new technology to go after shale-oil. Last time the bust lasted twenty years before prices went up to the price the world could afford, relevant to now is how long this bust will last?

The Saudi’s knew; they knew then that (some) shale oil drillers were making a fortune at $110, and they ought to have known that the more shale oil was drilled, the better the technology would get. But they did nothing; they just counted the cash rolling in and went on a gleeful spending spree.

So did the Russians, and the Nigerians, and the others; and that was just what the Central Banks wanted to “re-stimulate” the world economy. Mission Accomplished, except the inflation was concentrated on things rich people buy...fast cars, London property, shopping in Dubai, plastic surgery, and education so their kids can get the top jobs; for the rest of the world, wages didn’t budge.

There are three ways to value oil; the easy way is to look up the price today; but that tells you nothing about where the price is going; and the futures markets are just betting in a casino.

Another way you can work out what the customers can afford, that’s quite tough; but according to my analysis the Saudi’s had that one about right, $75. Of course no one will pay $75 when they can buy oil today at $30, even if they can afford to pay $75.

The third way is the replacement cost; how much it costs for the latest technology to bring in new oil? It doesn’t matter that the marginal cost of pumping from established oil fields might be $20, the price that matters is the price at which the customers say, “No Sir, I’m not paying your price, because I can go and find oil myself at that price”.

In 2011 that price was about $75. Looks like today it’s under $30; albeit, that price is only for 200,000 barrels per day of new oil per month, but looking at the numbers, if oil was $50, that could be 400,000 barrels per day per month, or in other words 100,000 barrels per day per month more than depletion.

Oh, and then there is Argentina, and Australia and lots of other places where the new technology, the latest stuff, developed over ten years of trial and error, is ready to be unlocked if oil goes to $50.

Ironically, that new technology was financed ultimately, via the bubble, by the Central Banks in their battle against deflation; looks like perhaps there was an un-intended consequence there, as in the inflation of oil prices, caused ultra-low oil prices, which will lead to...wait for it, deflation; and/or recession in nominal terms.

Now there’s a New World Order to look forward to...cheap oil, as much as you want! So much for wind-farms, Peak Oil, and rolling back global warming; my Cajun mate Jeff from Mississippi is buying himself a brand new real-man-redneck Ford pickup (complete with gun-rack), and trading-in his Toyota.

In hindsight; the oil-aristocrat incumbents might sensibly have started their little war in 2011, when the technology was less developed, like one analyst told them to at the time; looks like now the rabbit is out of the bag, and its set to make babies; lots of them.

By Andrew Butter

Twenty years doing market analysis and valuations for investors in the Middle East, USA, and Europe. Ex-Toxic-Asset assembly-line worker; lives in Dubai.

© 2015 Copyright Andrew Butter- All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Andrew Butter Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.