Gold to Beat Stocks 2016?

Commodities / Gold and Silver 2016 Feb 03, 2016 - 04:48 PM GMTBy: Axel_Merk

"Stocks beat gold in the long run!" is a 'rallying cry' to buy stocks we have heard lately that gets me riled up. It’s upsetting to me for two reasons: first, an out of context comparison, in my opinion, misguides investors. It might be the wrong assertion in the short to medium term.

"Stocks beat gold in the long run!" is a 'rallying cry' to buy stocks we have heard lately that gets me riled up. It’s upsetting to me for two reasons: first, an out of context comparison, in my opinion, misguides investors. It might be the wrong assertion in the short to medium term.

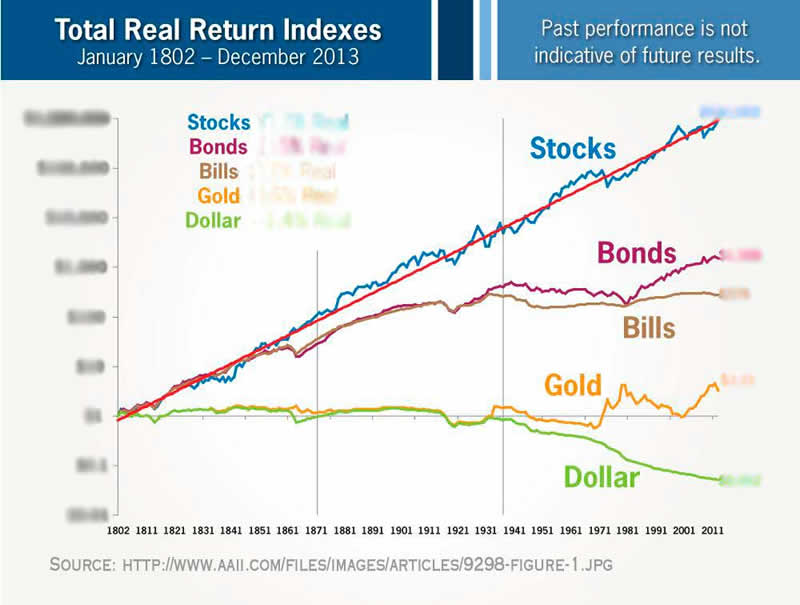

As background, Wharton School Professor Jeremy Siegel is author of the book Stocks for the Long Run, first published in 1994. I have heard Siegel, who is also the public face of a major ETF sponsor, frequently present the bullish case for stocks. Siegel had yet another bull-speech at a recent conference, in a follow-up discussion on gold that was on the outperformance of stocks versus gold. According to Siegel’s work, stocks returned a real rate of return of 6.7% from 1802 to 2013; in comparison, gold had a real rate of return of 0.6%. This provides the appearance that stocks beat gold hands down; assuming this is correct, why would this misguide investors? First, let’s clarify that these numbers are said to be real rates of return, not nominal rates (real rates of return are after inflation). Here is a publicly accessible chart of Siegel's theme; note that I intentionally obfuscated the specific numbers as I have concerns with the methodology used that go beyond the scope of this analysis (they are available at this 2014 interview with Siegel):1)

Gold as a diversifier?

Keep in mind that gold is a brick, albeit a shiny one. It's not meant to outperform stocks in the long run; the reason we use bonds and cash is not because we think they'll outperform stocks in the long run, but because they may be valuable diversifiers.

The chart shows the dollar started to underperform after the Fed was introduced in the early part of last century, then in earnest during the Great Depression. We also read into this chart that the credit driven super cycle that started at the end of the Great Depression was at the expense of the dollar.

The dollar was linked to gold for most of the period that chart shows. The link persisted until 1971; the outperformance of gold versus cash prior to 1971 is attributed to official debasements of the dollar. Let’s have a closer look at the performance of bonds from the end of the Great Depression until Paul Volcker became Chairman of the Fed (that was in August 1979). That negative performance has a good reason: we experienced an environment of financial repression as real interest rates were negative. It’s that sort of environment that we believe is favorable to gold as receiving no interest is better than negative real rates. However, gold couldn’t react at the time, because of the link between the dollar and gold. The 'gold window' closed because the U.S. could no longer sustain the link; not surprisingly, the period after 1971 was rather volatile and distortions (the boom/bust of 1980) were a side effect.

We believe that similar to the Great Depression, we are near the end of a debt super cycle. That means, after decades of credit expansion, it’s time to reduce the relative debt in the economy; the ways to achieve this are through growth, default or inflation; hedge fund manager Ray Dalio has been very outspoken on this of late. If our analysis is correct, then odds are high that the era of financial repression may well persist for some time, as the huge debt overhang is worked through. In that context, gold, these days no longer pegged to the dollar, may perform favorably compared to bonds and the dollar. As such, gold may be a good diversifier to a stock portfolio, in the right circumstances.

It’s in this context that I perceive Jeremy Siegel’s touting of stocks may be doing a disservice to investors. Very few advisers recommend a 100% stock allocation; the reason we diversify our portfolios is because most of us are looking to maximize risk-adjusted returns. Diversification is the one free lunch that Wall Street offers. This doesn’t mean gold, or any one specific asset is the ideal diversifier; but it strongly suggests that touting gold or any asset class as the single best investment may be problematic, unless accompanied by a litany of disclaimers/qualifiers.

Gold to outperform?

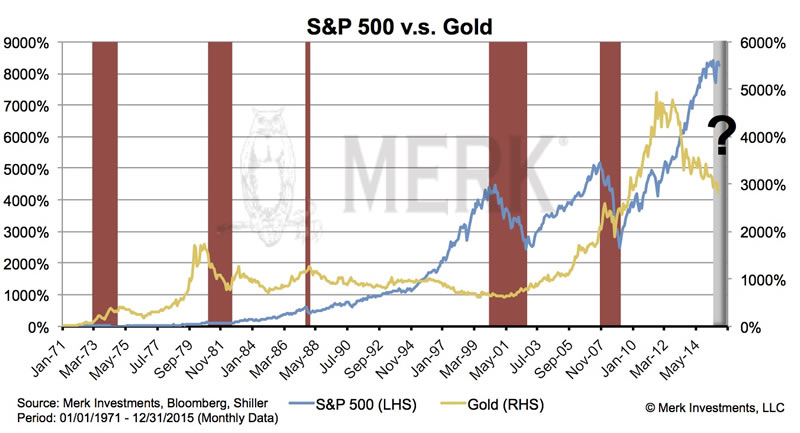

If stocks have done so well over 200 years compared to gold, is it possible for gold to outperform stocks over a shorter horizon, say 2 years, 10 years or 20 years? The challenge with historical comparisons is that one can always cherry pick to choose what suits one’s argument. One can choose the price of gold at the peak of 1980 to see how long it has languished; or one can pick the top of the Nasdaq bubble, just as gold bottomed out a few years later to see how gold might do versus stocks for many years. Ultimately, what matters to investors is what the price of gold is going to do going forward. We like to show the price of gold since 1971 (when it de-coupled from the U.S. dollar) in relation to past bear markets in equities. During this period from 1970 through 2015, gold had an annual return of 7.70% with a correlation to equities of zero:

One notable exception is the bear market that accompanied Volcker’s interest rate hikes in the early 1980s. As I have indicated in the past, anyone who expects a similar monetary policy, should not expect gold to perform well. However, we take the Fed at its word that even as inflation and employment moves back to what historically was considered normal, rates may continue to be lower than normal (as the last paragraph of the FOMC statement has stated this since the spring of 2014). To me, that’s a commitment to be ‘behind the curve’, i.e. that rates will be rising slower than inflation. In fact, Fed Vice Chair Stan Fischer in a speech on Monday, February 1, 2016, said that he wouldn’t mind for inflation to temporarily overshoot on the upside. All of this suggests that real interest rates may continue to be low, possibly even negative. While there is no assurance gold will do well in such an environment, to me, it is a key long-term driver for the price of gold.

If I look out 10 years and consider the projections of U.S. deficits, I have a hard time seeing how we can afford positive real interest rates. This may bode well for the price of gold. But will gold outperform stocks? I happen to be very negative on stocks in the current environment. Last August, before the sharp selloff in equities, I published a newsletter Coming Out - As a Bear!; the basic premise of the analysis is that the Fed had “compressed risk premia,” i.e. bid up asset prices and taken fear out of the market. For years, investors piled into risky assets, such as equities, not appreciative of their inherent risks. As part of that process, they are likely now over-exposed to equities, having ‘bought the dips’ rather than prudently diversifying. It seems the mentality is gradually shifting towards capital preservation, i.e. ‘selling the rallies,’ but this is a process that, in my assessment, will – at a minimum – take months.

As such, I see the current environment much more like 2000 where investors seemed to be in denial for a long time as equities cascaded lower. This time around, we may have a more aggressive Bank of Japan and European Central Bank; I might change my mind, but so far, I don’t see them being strong enough to stem against the tide. At some point the Fed may join the easing camp once again, but I believe they will be late as they are too focused on the labor market that’s generally considered a lagging indicator. Think of the Fed having removed the lid from a pressure cooker; so even if or when the Fed turns to easing once again, it might have a difficult time preventing this bear market from unfolding. Stay tuned as we update our view.

In the above outlined environment, gold may perform quite well. Can I make a prediction that gold will outperform stocks for 10 or even 20 years? No, because too many things can change. However, I state in the article above that I started shorting equities last August; I increased my short position last December. I also own a substantial position in gold, much higher than the small diversification amount advocated by some.

I’m not suggesting that everyone should go short equities; such a strategy is fraught with many risks. But I believe there may well be times when gold can outperform. My risk tolerance allows me to put my money where my mouth is; any investor, though, should carefully evaluate how much money they allocate to gold, as the price of gold can be rather volatile measured in U.S. dollars. That, by the way, applies to stocks too.

Please register for our upcoming Webinar entitled ‘Gold to Beat Stocks?’ on Thursday, February 25, to continue the discussion. Also make sure you subscribe to our free Merk Insights, if you haven’t already done so, and follow me at twitter.com/AxelMerk. If you believe this analysis might be of value to your friends, please share it with them.

Axel Merk

Merk Investments, Manager of the Merk Funds

The chart claims that an 1802 stock investment would have far outperformed gold over 200+ years. Yet, the Dow Jones Industrial Index wasn’t even created until 1896; at the time, it had 12 stocks, with General Electric as the only company that has survived; other firms have merged or gone out of business. The high returns proclaimed suggest a smart way of re-allocating one’s money at the appropriate time, preferably with no cost of ownership or moving to the latest index. In contrast, if one had gold 200+ years ago, the only cost to worry about is storage. The gold of yesteryear is still the same gold today. As such, any such 200+ year comparison requires closer scrutiny. There are also plenty of questions to be raised on how exactly bond investments have performed over 200+ years and whether a mere mortal could have indeed achieved the claimed returns. It’s in this context that I obfuscated the returns, so we can discuss the trends without getting bogged down in the specific numbers.

On a separate note, showing the real rate of return of gold is something that should raise some eyebrows. How come a brick can have a real rate of return? The brick is the constant, with everything else around it changing. As such, I can’t help but feel that maybe the CPI is under-stating inflation. But that’s a different discussion...

Axel Merk

Manager of the Merk Hard, Asian and Absolute Return Currency Funds, www.merkfunds.com

Rick Reece is a Financial Analyst at Merk Investments and a member of the portfolio management

Axel Merk, President & CIO of Merk Investments, LLC, is an expert on hard money, macro trends and international investing. He is considered an authority on currencies. Axel Merk wrote the book on Sustainable Wealth; order your copy today.

The Merk Absolute Return Currency Fund seeks to generate positive absolute returns by investing in currencies. The Fund is a pure-play on currencies, aiming to profit regardless of the direction of the U.S. dollar or traditional asset classes.

The Merk Asian Currency Fund seeks to profit from a rise in Asian currencies versus the U.S. dollar. The Fund typically invests in a basket of Asian currencies that may include, but are not limited to, the currencies of China, Hong Kong, Japan, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan and Thailand.

The Merk Hard Currency Fund seeks to profit from a rise in hard currencies versus the U.S. dollar. Hard currencies are currencies backed by sound monetary policy; sound monetary policy focuses on price stability.

The Funds may be appropriate for you if you are pursuing a long-term goal with a currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Funds and to download a prospectus, please visit www.merkfunds.com.

Investors should consider the investment objectives, risks and charges and expenses of the Merk Funds carefully before investing. This and other information is in the prospectus, a copy of which may be obtained by visiting the Funds' website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest.

The Funds primarily invest in foreign currencies and as such, changes in currency exchange rates will affect the value of what the Funds own and the price of the Funds' shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. The Funds are subject to interest rate risk which is the risk that debt securities in the Funds' portfolio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities which can be volatile and involve various types and degrees of risk. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. For a more complete discussion of these and other Fund risks please refer to the Funds' prospectuses.

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice. Foreside Fund Services, LLC, distributor.

Axel Merk Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.