Chronicle Of A Debt Foretold - When Central Banks Buy Equities

Stock-Markets / Stock Markets 2016 Jan 23, 2016 - 03:17 PM GMTBy: John_Rubino

Critics of today’s fiat currency/fractional reserve banking world have (for what seems like forever) made the common sense point that when debt rises faster than cash flow, bad things are bound to happen. In every cycle since 1980 this has been dismissed by the vast majority who benefit from inflating bubbles — until the bubble bursts.

Critics of today’s fiat currency/fractional reserve banking world have (for what seems like forever) made the common sense point that when debt rises faster than cash flow, bad things are bound to happen. In every cycle since 1980 this has been dismissed by the vast majority who benefit from inflating bubbles — until the bubble bursts.

And here we go again. The following chart from Stock Traders Daily shows the relationship between margin debt (money borrowed by investors against existing stock positions in order to buy more stock) and cash on hand in brokerage accounts. The idea is that when investors hold lots of cash they’re pessimistic, and when they borrow a lot they’re optimisitc. Extremes of either tend to signal changes in market direction. At the end of 2015 investors were even more excited than at the peak of the housing bubble, indicating that there’s not much retail money left to be tossed at US stocks.

China, being a little more bubbly than the US, is a good indicator of where US margin debt might be headed:

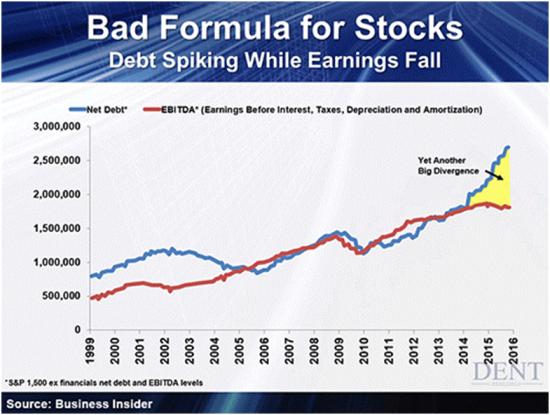

Another red flag is being waved by corporate debt, much of which is being taken on to fund share repurchase programs. These tend to benefit shareholders in the moment but at the cost of higher leverage and less flexibility in the future. Where in the past net debt has tended to track EBITDA (a broad measure of earnings). starting in 2014 the former has soared beyond the latter. Just as a spike in margin debt implies a lack of retail stock buying in the future, soaring corporate debt implies limited borrowing power and a scale-back of share repurchases going forward.

Based on both history and common sense, we should expect not just a slowdown, but a cratering of equity demand from both individuals and corporations in the year ahead. What happens then? Either the market crashes and prices go back to levels that attract wiser capital, or a new source of dumb money emerges.

And that would be government. Already, the Bank of Japan owns more than half of the Japanese stock market. And now China — displaying its customary cluelessness about what markets are and how they work — is countering the recent bear market with public (which is to say borrowed) funds:

China Vice President Vows to ‘Look After’ Stock Market Investors

(Bloomberg) – China is willing to keep intervening in the stock market to make sure a few speculators don’t benefit at the expense of regular investors, China’s vice president said in an interview.Calling the country’s market “not yet mature,” Vice President Li Yuanchao said the government would boost regulation in an effort to limit volatility.

“An excessively fluctuating market is a market of speculation where only the few will gain the most benefit when most people suffer,” Li told Bloomberg News after arriving at the World Economic Forum’s annual meeting in Davos, Switzerland. “The Chinese government is going to look after the interests of most of the people, most of the investors.”

Li, 65, is the most senior Chinese official yet to underline the government’s readiness to intervene should the market turmoil of last summer and the start of 2016 continue. So far this year, the Shanghai Composite and the Hang Seng China indexes have both lost more than 15 percent, even as the central bank injects cashinto the system to drive down borrowing costs and boost the economy.

Companies exchanging long term bonds for equities and individuals using equities as collateral to buy more tend to distort equity valuations, but only temporarily, as the players’ finite borrowing capacity is eventually maxed out and the buying has to stop.

Governments are a different story, since they can create trillions of dollars with a mouse click. Their ignorance is thus a lot more dangerous because it short-circuits price disclosure on a vast, potentially open-ended scale.

When a central bank buys equities, it doesn’t have teams of analysts running valuation studies and creating model portfolios. Presumably it just makes across-the-board purchases, which tends to float all boats. So the wheat doesn’t get separated from the chaff and capital has no idea where to flow. Malinvestment becomes rampant and the result is, well, what we have today: Chinese ghost cities, Japanese zombie companies and US tech unicorns worth billions before generating their first dollar of earnings. And that’s before the Fed and European Central Bank really get going.

By John Rubino

Copyright 2016 © John Rubino - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.