Corporate Debt - Road To Oblivion In A Stocks Bear Market

Stock-Markets / Stocks Bear Market Aug 18, 2015 - 10:32 AM GMTBy: James_Quinn

Any article that starts with a quote from Jim Grant is guaranteed to be a fact based, common sense, reasoned analysis of our warped, debt saturated, over-valued, Federal Reserve rigged financial markets. John Hussman starts his weekly letter with this quote from Jim Grant:

Any article that starts with a quote from Jim Grant is guaranteed to be a fact based, common sense, reasoned analysis of our warped, debt saturated, over-valued, Federal Reserve rigged financial markets. John Hussman starts his weekly letter with this quote from Jim Grant:

"The way to wealth in a bull market is debt. The way to oblivion in a bear market is also debt, and nobody rings a bell." - James Grant

We've been in a Fed QE and ZIRP induced six year bull market that has been sputtering since QE 3 ended in October 2014. Leveraging yourself to the hilt and piling into the stock market has been the road to riches for six years, just as leveraging to the hilt in real estate was the road to riches from 2002 through 2007, and leveraging to the hilt in internet stocks was the road to riches from 1998 through 2000. Of course, the dot.com and housing road to riches detoured into ditches that wiped out trillions of phantom wealth, just as the current road is leading to a grand canyon size ditch.

Total credit market debt has reached all-time highs. The de-leveraging of consumers, liquidation of insolvent Wall Street banks, and bankruptcies of zombie retailers, real estate developers, and mall owners was postponed by Federal Reserve intervention, changing accounting rules to hide bad debt, political shenanigans, and taxpayers paying for the extreme risk taking by bankers and corporate CEOs. Total credit market debt sits at $59 trillion, up from $52 trillion in 2009 at the depths of the recession. This increase has been entirely driven by a $5.3 trillion increase in government debt and a $1.6 trillion increase in corporate debt. The propaganda about corporations flush with cash is bold faced lie. Corporations have increased their debt load by 25% since 2009.

As Dr. Hussman points out, the Fed has encouraged this behavior by the biggest corporations on the planet with their suppression of market interest rates and their gift of $3 trillion to the Wall Street banks. Corporate CEOs are supposed to be the smartest guys in the room, but they haven't been able to grow their businesses through innovation, creativity, new products, or new investments in plant and equipment. Their entire playbook consists of outsourcing jobs to foreign countries, keeping wages below the level of inflation, and borrowing cheaply from Wall Street banks to buyback their stock and boost earnings per share, so their stock price will go higher, enriching themselves.

The opposite of a debt-equity swap, of course, is a debt-financed stock repurchase, which leverages up the claims of existing shareholders. One of the more troubling aspects of the Federal Reserve's suppression of interest rates is the speculation it has encouraged, by giving companies access to enormously cheap funding on a 5-7 year horizon. Though nominal economic growth has been tepid, revenue growth has turned negative, and profits as a share of GDP have been falling for more than a year, companies have scampered to boost their per-share earnings by taking out debt to repurchase and reduce the number of shares outstanding. This leveraging has been done at market valuations that are near the highest levels in history on historically reliable measures.

These Ivy League educated CEO titans are nothing but greedy lemmings, following the guidance of corrupt Wall Street bankers by buying back their stock at all-time high valuations. They did it from 2005 through 2008 and paid the price shortly thereafter. It appears some one taught them the "buy low, sell high" concept backwards. They bought no stock at the 2009 lows.

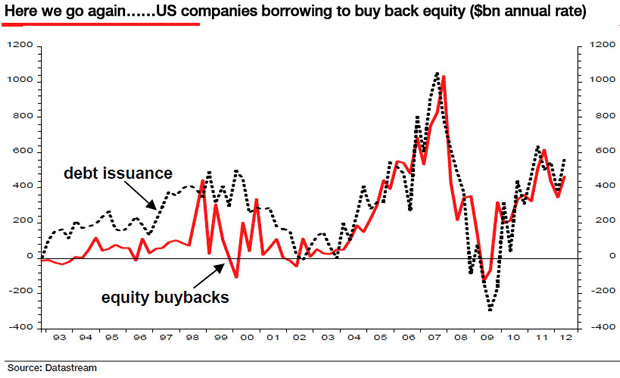

See, the timing of buybacks at an aggregate level has nothing to do with value. As Albert Edwards at SocGen has often observed, not only do buybacks increase at rich market valuations and dry up in depressed markets, they are also typically financed by issuing debt. What drives buyback activity is not value, but the availability of cheap, speculative capital at points in the business cycle where profit margins are temporarily elevated and make the increased debt burden seem easy to handle. The chart below showed the developing situation a few years ago...

They are presently buying back their own stock at a pace never before seen in market history. Every valuation metric known to mankind is flashing red and showing the market to be as overvalued as any time in history, but corporate CEO's are borrowing like madmen and buying their own stock. Where is the prudence, risk management, and responsibility for the long-term financial viability of these corporations from the executives running these companies? Does only next quarter's EPS matter?

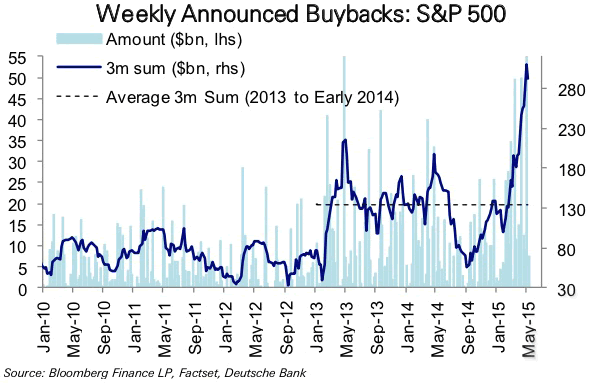

... and the chart below shows the frantic pace that repurchases have reached - at what are now the most extreme levels of valuation in U.S. history outside of a few months surrounding the 2000 market peak.

Hussman, inconveniently for the Wall Street huckster crowd and CNBC cheerleaders, points out that corporate profits peaked two quarters ago and are headed downward. Revenue growth is non-existent and corporate debt yields are rising. The high yield financed shale oil boom is imploding, zombie retailers are struggling, and marginal players are seeing interest rates rise. Borrowing to buy back stock as a recession takes hold becomes untenable, even for delusional greedy CEOs. Stockholders are going to wish these CEO's hadn't levered their balance sheets just before Depression 2.0 hit.

One emerging problem here is that credit spreads in corporate debt have begun to widen considerably, increasing the cost of debt, while profit margins continue (predictably) to come under pressure. Corporations tend to press their luck when it comes to buybacks, largely because profit margins tend to be deceptively high at major market peaks, but it's difficult to maintain a high pace of repurchases when fading revenue growth and narrowing profit margins are joined by wider credit spreads.

The larger problem with repurchases is that debt-financed buybacks effectively put investors on margin. As corporations have borrowed in order to aggressively buy back their stock near the highest market valuations in history, existing stockholders have quietly become heavily leveraged, without even realizing it.

You can thank Janet, Ben and their merry band of central bankers for this epic level of malinvestment. Their ongoing ZIRP has left pensions plans, life insurance companies, and other large institutional investors with no yields. The Fed is a perpetual bubble machine and the latest bubble is in debt financed corporate equity purchases. It will end the same way all Fed bubbles end, with a financial crisis, trillions in losses, bankruptcies, and soaring unemployment. The unwind of these excesses will be epic.

So not only is the equity market at the second most overvalued point in U.S. history, it is also more leveraged against probable long-term corporate cash flows than at any previous point in history. As we observed during the housing bubble, yield-seeking by investors opens the door to every form of malinvestment. The best way to create a debt-financed wave of speculative and unproductive activity is to starve investors of safe return. In 2000 that wave of speculation focused on technology. The next Fed-induced wave of speculation focused on mortgage securities, which financed a housing bubble. In our view, the primary avenue of speculation in the current cycle has been debt-financed corporate equity purchases.

Over the completion of this cycle, we fully expect that many companies and private-equity firms will be forced to reverse this activity through involuntary debt-equity swaps, with a corresponding dilution in the ownership stakes of existing shareholders. Indeed, the group that led the largest leveraged buyout in the oil and gas sector in 2011 announced last week that its ownership stake would be handed over to lenders. Back in 2011, profit margins were elevated in the energy sector, making the new debt burdens seem easy to handle. But part of the signature of an emerging global economic slowdown has been pressure on energy and industrial commodity prices (see the February 2, 2015 comment, Market Action Suggests an Abrupt Slowing in Global Economic Activity). The grandiose leveraged buy-outs of 2011, now facing Chapter 11, are the canaries in the global economic coal mine. In the words of Bad Company, "It ain't the first time baby... baby it won't be the last."

The market was down 275 points last Wednesday and finished flat on the day. The market was down 135 points today and reversed by 200 points in a matter of minutes. In these low volume markets, large corporations are propping up their stocks and the market by wading in and buying back their stock. The savvy investors have been selling hand over foot, while the lemming CEO crowd keeps wasting their cash on their over-priced stocks. They call this adding value.

As usual, Dr. Hussman provides a succinct, factual, and dire warning to anyone invested in this market. The current overvalued market conditions have only been present 8% of the time over the last century. Market crashes have only occurred when the current conditions existed in the past. The ghosts of 1929, 2000 and 2007 are warning you to beware. Ignore the warnings at your own peril.

The current set of conditions has been observed in only about 8% of market history, and that 8% of history captures the only set of conditions that we associate with expected and severe market losses. It's the 8% of history that matches current conditions where most market crashes have occurred.

Join me at www.TheBurningPlatform.com to discuss truth and the future of our country.

By James Quinn

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer, and are not sponsored or endorsed by his employer.

© 2015 Copyright James Quinn - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

James Quinn Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.