Gold Coins "Not Available" in Europe? - Untrue

Commodities / Gold and Silver 2015 Jun 17, 2015 - 12:38 PM GMTBy: GoldCore

- Armstrong and blogosphere on shortage of gold coins in Europe

- Armstrong and blogosphere on shortage of gold coins in Europe

- No shortage of gold whatsoever at retail level in Europe

- Gold demand in most of Europe quite mixed despite significant risks

- Germany, Switzerland, Greece seeing strong demand but no shortages

- Alarmist warning that governments to make gold “illegal”

- Poor data and research or disinformation?

A rumour has been making its way around the blogosphere suggesting that gold coins are not available for purchase from retail outlets across Europe. As one of Europe’s larger gold brokerage and storage providers, GoldCore can can confirm that this information is misleading and incorrect.

Martin Armstrong, who is well resourced and whose historical perspectives we sometimes find interesting, wrote about this supposed development recently and it has been taken up by other blogs.

Armstrong wrote:

“There is a very curious new development with respect to gold. In many European countries, people can no longer buy retail gold coins for bullion. Shops will buy but no one is selling. Banks that previously offered gold to the public have shut down in Spain. If someone leaves Spain wearing a lot of jewelry, authorities will pull them aside to weigh whatever jewelry they may have.”

The piece is entitled “Is gold becoming illegal?” and strikes us as being rather alarmist. We have seen no shortage of gold on a retail level whatsoever. Armstrong suggests that governments are “shutting down retail sales” and may confiscate gold and make it “illegal to even own.”

“Little by little, this hunt for money by desperate government is turning toward gold. Shutting down retail sales is quite alarming, for what typically follows is some decree of forcing the public to turn over bullion by a certain date, or thereafter it can be confiscated and illegal to even own.”

This is not true and there is no example of any European government “shutting down retail sales.”

Why these European governments would confiscate the tiny amounts of gold that their citizens have and not simply buy gold on the open market as is being done by the central banks of Russia, China and many other nations is ignored.

Also, the logistics of a government in this day and age confiscating gold and the enforcement of that confiscation is not considered.

It also ignores the fact that the gold bullion market is now a mature, sophisticated market that has become internationalized in recent years – arguably making the bullion market today more liquid than at any time in history.

If a prospective European buyer in one European country, such as Spain, cannot access gold from a local or national dealer there is absolutely nothing stopping them going online and buying from any of the scores of reputable bullion dealers in other EU countries or indeed from refineries and mints internationally.

Nor, is there anything to stop them from wiring funds to a bullion dealer or storage provider and storing gold in vaults in Zurich, Singapore or Hong Kong.

Demand for gold has actually been quite mixed across Europe in recent months. Refineries and mints we work with will attest to that fact.

This despite the unprecedented monetary experiment that is the ECB’s version of QE, the threats to the European project posed by a “Grexit” or “Brexit” and simmering tensions in the Middle East and between the EU and Russia.

At the same time Germany, Switzerland and Greece have seen robust demand for gold coins. Degussa, one of the larger refiners and wholesalers of gold in Europe reported a 30% surge in German demand in the first five months of this year.

“We expect demand to remain very buoyant as the uncertainty is still very high about Greece’s exit and concerns about other countries,” Bloomberg report the company’s CEO, Wolfgang Wrzesniok-Rossbach, as saying at the International Precious Metals Institute (IPMI) event on Monday in San Antonio, Texas.

He gave no indication of any shortages or inability to supply clients in Europe.

Indeed, even in Greece which looks set to default in the coming days and where we have seen some demand for gold sovereigns, including from Greek bullion dealers, there are no shortages of gold.

The suggestion that gold coin dealers across Europe are being hampered from selling to the public by national governments is incorrect. And when one poses the question “Is gold becoming illegal?” it begs the question – who benefits from the dissemination of this kind of negative information about gold?

Such information would likely discourage retail investors who are considering whether they should have an allocation of gold. Why would the typical retail investor buy something that the government may confiscate?

Of course, some governments may decide to confiscate gold but, unlike the experience in the U.S. in 1933 when the medium of exchange and currency was gold, as already indicated the amount of gold owned by the public today is minuscule.

This makes confiscation of gold bullion at an individual level highly unlikely. The risk is that governments may look to confiscate large pools of gold – with unallocated and ETF holdings held in banks being a prime target. There is also the risk that companies that control large pools of client gold could be nationalised by their national government.

We believe that there is possibility of debtor governments nationalising large gold deposits in large brokers, financial institutions and banks in their jurisdictions in the event of a systemic or monetary crisis.

This is why we advise clients to directly own physical gold and silver coins and bars en bailment (allocated, segregated, outright legal ownership and with the ability to take delivery) with secure, reputable vaulting companies in safe jurisdictions such as Singapore and Switzerland.

Armstrong also suggests that Chinese demand and indeed global demand for gold has fallen sharply and that this may result in the gold price falling further:

“Meanwhile, April saw the biggest decline in gold shipment to China that traditionally goes through Switzerland. In April, they fell 67%. As the economy has been turning down in Asia, the demand for gold has fallen by about 36%.

With governments in Europe cutting off the ability to buy gold, which is already declining in demand, mixed with the rising dollar, everything warns that the final low for gold may be on the horizon. …”

This is simplistic analysis as it focusses on Chinese mainland imports of gold from just Switzerland and ignores the huge supplied of gold flowing into China from all over the world into a variety of mainland Chinese cities and indeed Hong Kong.

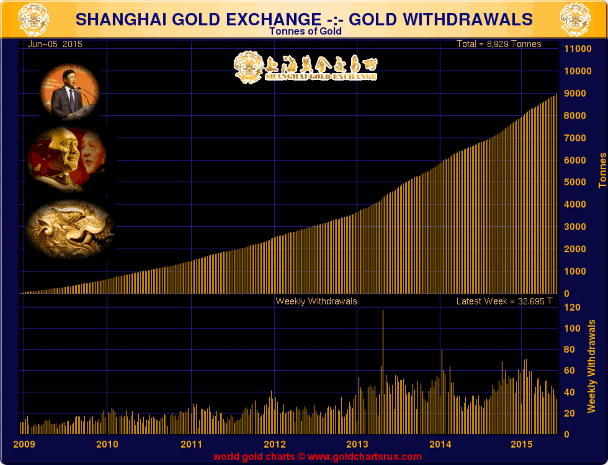

Shanghai is obviously increasingly important in this regard and the best benchmark of total global Chinese demand remains withdrawals from the Shanghai Gold Exchange (SGE) and these remain robust (32.695 tonnes for the week ending June 5th) as indeed do premiums on gold bars in China.

Premiums on the Shanghai Gold Exchange were about $1-$2 an ounce overnight.

We have heard speculation regarding falling Chinese and Indian demand in recent years.

In fact, this has been the ebb and flow of the market and demand has fallen from record highs and then risen again. Indeed, when you fade out the daily, weekly and indeed monthly noise and focus on the quarterly and indeed the annual demand trends, it is clear that gold bullion demand in China, India has remained very robust and supportive of the gold market.

It is dangerous to use such simplistic analysis in order to make price predictions. Further lows and a “final low” in the gold market are possible but not due to European governments shutting down retail gold demand or alleged falling demand in China and Asia.

To conclude, there is no shortage of gold in Europe. If there were, it would be very much be in our interest and it would indeed be important to highlight that fact.

Given the very small size of the entire physical gold market and the even smaller size of the entire physical silver market, we believe shortages will likely develop when the next global financial crisis erupts.

This is a question of when rather than if as it is only a matter of time before this happens. Be assured – when shortages of gold coins and bars in Europe and internationally materialise you will hear about it.

For most, it will be then be too late to secure their coins and bars.

Must Read Guide: 7 Key Gold Must Haves

MARKET UPDATE

Today’s AM LBMA Gold Price was USD 1,181.70, EUR 1,045.65 and GBP 748.92 per ounce.

Yesterday’s AM LBMA Gold Price was USD 1,186.20, EUR 1,050.06 and GBP 759.36 per ounce.

Gold slid $4.50 or 0.38 percent yesterday to $1,181.70 an ounce. Silver fell $0.09 or 0.56 percent to $16.02 an ounce.

Gold in Singapore for immediate delivery fell 0.2 percent to $1,179.01 an ounce an ounce near the end of the day, while gold in Switzerland was flat again.

Gold continued losses overnight and stayed near $1,180 an ounce this morning despite the real and deepening risk of a Greek default. Jitters in the bond market and the risk of contagion are likely supporting gold and should see gains once the current period of lockdown below $1,200 comes to an end.

It appears Prime Minister Alexis Tsipras has no intention of making a last minute effort to meet the austerity demanded by the IMF and European lenders. Tsipras accused Greece’s creditors yesterday of trying to “humiliate” Greeks with more cuts. Europe appears to be preparing for Greece to leave the euro.

Some investors await the U.S. Federal Reserve policy statement at 1830 GMT. Janet Yellen’s wording will be listened to for any hints as to the timing of the Fed’s interest rate hike. As ever, best to phase out the Fed’s words and focus on their actions and the reality that ultra low interest rates are set to continue for a few more months and likely for a few more years.

In late morning European trading gold is down 0.26 percent at $1,179.00 an ounce. Silver is off 0.25 percent at $15.96 an ounce and platinum is down 0.48 percent at $1,075.36 an ounce.

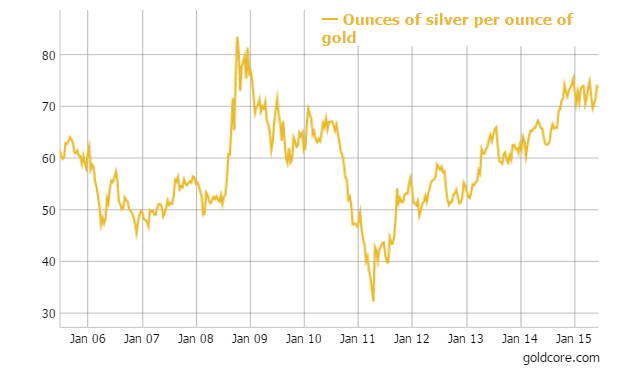

Silver continues to be accumulated. Smart money is taking the view that the supply and demand fundamentals are sound and the silver price is very undervalued versus increasingly frothy stock and bond markets and indeed even the depressed gold market (see Gold Silver ratio chart).

This update can be found on the GoldCore blog here.

Stephen Flood

Chief Executive Officer

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.