The IMF Leaks Greece, Institutions Forcing a Debt Default

Politics / Eurozone Debt Crisis May 18, 2015 - 03:10 PM GMTBy: Raul_I_Meijer

Whenever secret or confidential information or documents are leaked to the press, the first question should always be who leaked it and why. That’s often more important than the contents of what has been leaked. And since there’s been a lot of hullabaloo about a leaked document the past two days, here’s a closer look. Spoiler alert: the document(s) don’t reveal much of anything new, despite the hullabaloo.

Whenever secret or confidential information or documents are leaked to the press, the first question should always be who leaked it and why. That’s often more important than the contents of what has been leaked. And since there’s been a lot of hullabaloo about a leaked document the past two days, here’s a closer look. Spoiler alert: the document(s) don’t reveal much of anything new, despite the hullabaloo.

On Saturday, Paul Mason at Channel 4 in Britain posted an IMF document(s) that according to him says, among other things, that the IMF expects a June 5 Grexit – in one form or another – if there is no agreement before that date between Athens and its creditors, ‘the institutions’ (of which the IMF itself is one).

The leaking is simply what it is as long as we don’t know the how and why. But the question will remain why somebody takes the risk to leak something only a small and select group of people are privy to. Is it leaked because it’s politically important, does Paul Mason pay a lot of money for leaks? Or is it perhaps an intentional leak, in this case ordered by IMF higher-ups? And if so, for what reason? A veiled threat?

Fact is that when you look through the documents Mason published, you notice that he adds his own interpretation to them. Mason, to whom documents seem to be leaked on a regular basis – he wrote about 2 more leaked documents 3 months ago – for instance suggests quite strongly in his write up at Channel 4 that June 5th is the date for a possible default.

However, the documents don’t mention that date. They only talk about June, not June 5. Mason writes about IMF ‘staff’: “They point to the €1.5 billion due to the IMF in June as the first vulnerable payment.”

The €1.5 billion is not one payment, though. The first June payment, at least according to a Bloomberg overview , which is indeed scheduled for June 5, is ‘only’ €310 million. There are then subsequent payments to the IMF scheduled on June 12 (€348 million), June 16 (€581 million), and June 19 (another €348 million). These are rough numbers, there are slightly different ones doing the rounds; still, they’ll do.

But June 5 is by no means carved in stone as a default date (€310 million might be feasible for Athens), though Mason does make it seem like that. Every single day counts now in the negotiations. And a €310 million payment on June 5 would buy Greece at least another week. Which may prove crucial. For both sides of the negotiating table. Greece might even miss one or two payments; the consequences of such a move would be mainly a political decision, meaning there’s some room to move.

We noticed, by the way, another example of ‘Masonic’ interpretation in the video that accompanies the article. In it, Mason claims (at about 1:10) that “..the writer of this document thinks Greek pensions are too generous even now.” While it’s possible that he talked to the writer, or received additional information that he doesn’t mention, fact is that the document doesn’t corroborate his statement in the video. There’s no mention of this claim. Maybe it’s Paul Mason’s own opinion?! Take a listen:

The main sticking points with the ‘institutions’ now seem to be ‘labor reform’ (i.e. down with the unions -how IMF can you get?-) and pensions. Syriza has once again said this morning that it refuses to cave in on either. And there’s also the case of the 4000 or so re-hired cleaning ladies and school guards. The well-paid negotiators from Brussels and Washington want them out of their poorly paid jobs again. Not going to happen on Tsipras’ watch.

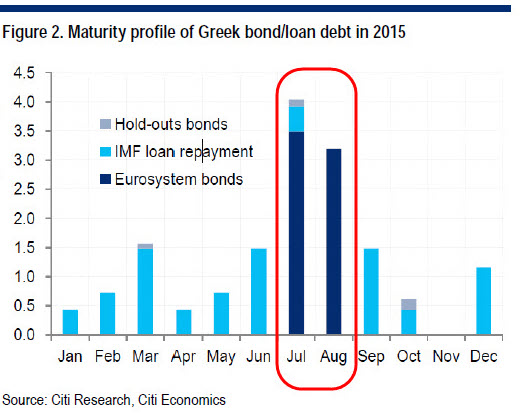

Yanis Varoufakis has already made clear what Syriza thinks should be done with the debt it owes to Europe: it should be swapped for paper with a repayment schedule that stretches way into the future. Looking at (re)payment schedules, it becomes clear this is not just a hollow idea. If Europe would allow for such a swap, Greece’s debt picture would change radically overnight. It would take away a large part of the burden this year:

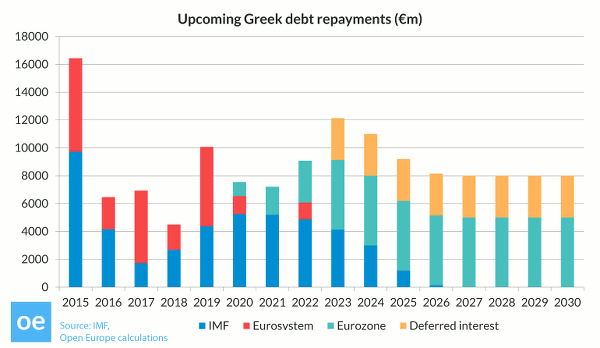

And when this year is over, everything looks a lot sunnier:

The biggest speedbump in Greece’s repayment schedule is summer 2015. Take that away and things look completely different. All the institutions need to do is to provide Greece with some leeway. It’s very possible to do so. If the EC, ECB and IMF decide not to allow for that leeway, there can -again- be only one conclusion, as I said before: Greece Is Now Just A Political Issue.

The ‘big kahuna’ issue for Syriza has been, ever since it won the elections in late January, that its voters want something seemingly impossible: an end to austerity combined with continued membership of the eurozone. ‘The institutions’ won’t let Greece have both. Which has a lot to do with the fact that polls show continued support for euro membership in Greece; it’s one big hammer that Tsipras can be banged over the head with, day after day.

‘The institutions’, and indeed the international media, expect Greece to cave in to their demands for more austerity at the ‘final moment’, because the alternative would not only be horrific – at least presumably -, it would go against the wishes of the Greek people. What not a lot of people seem to understand is that Syriza can’t give in, because it would mean the end of Syriza.

However, if the institutions force a Greece default, that would bring a potential disintegration of the eurozone much closer than it is today. And whoever says they’re confident it can be contained are delusional liars. The risks for all three, EC, ECB and IMF, would far outstrip the few billion euros on which they may receive repayment a few years later. And they should not want these risks. Not if they have functioning neurons left.

But the biggest threat to the negotiations may not come from the institutions after all. It may well come from inside Syriza. As the Greek Analyst site reported this morning:

Call For “Rupture Now” By The Political Secretariat & Central Committee Of Syriza

Prominent members of the Central Committee and the Political Secretariat of Syriza are preparing an event for tomorrow, Tuesday May 19. Quoting from the event description, as well as the title of the invitation-pamphlet, the message of the event seems quite clear: “the only way out [of the impasse] is the choice of rupture with the lenders.” :

The Moment of Truth For Syriza: “Rupture now with the lenders.”

The moment of truth has arrived. The lenders are pressuring the government to sign a Memorandum agreement of neoliberal strategy (privatizations, demolition of the insurance-pension system and of the labour rights, ENFIA, VAT tax, etc.)

It turns out that the agreement of the 20th of February facilitated, objectively, this attack and “creative ambiguity” favored the powerful. The assumption that a radical program of anti-austerity can be build with the tolerance of the neoliberal steering wheels of the Eurozone proved wrong. Now, we are moving to the critical hour of decisions for the government, the party of SYRIZA, and the social majority.

We need to choose between the signing of the looming austerity agreement and the rupture with the lenders. SYRIZA cannot be turned into a party of austerity; neither can the government implement the Memorandum. This is the reason why, both domestically and abroad, proposals for the internal “cleansing” of SYRIZA and governmental solutions for “national unity” are put on the table.

For all those reasons, the only way out is the choice of rupture with the lenders. With a suspension of repayments [of the debt], measures that restrict the “freedom” of capital flight, governmental control over the banks, taxation of capital and of the rich for the financing of pro-people measures, support of this policy with any and all possible means, and with the possible break from the EMU.

For all of the above, we invite you to discuss in the open event of Rproject on Tuesday 19/5 in 7:00pm at ESIEA. Today, the future of workers, unemployed, pensioners, young people is judged. And at the same time, the future of the Radical Left in Greece, but also internationally.

Anatole Kaletsky thinks Syriza will blink. I saw that a few days ago with all of its assumptions and I thought: whatever. I don’t even think Kaletsky knows what Syriza is. There are too many opinions and too many assumptions out there that see the negotiations as just that: negotiations (that will end badly for Tsipras and Varoufakis). But Syriza is not just another thirteen in a dozen political party. It comes with principles that it will not and cannot sell to the highest bidder. That, more than anything else, makes this a political issue.

By Raul Ilargi Meijer

Website: http://theautomaticearth.com (provides unique analysis of economics, finance, politics and social dynamics in the context of Complexity Theory)

© 2015 Copyright Raul I Meijer - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Raul Ilargi Meijer Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.