Yet Another Greek Secret: The Case of Greece's Phantom Assets

Politics / Eurozone Debt Crisis May 06, 2015 - 10:22 AM GMTBy: Steve_H_Hanke

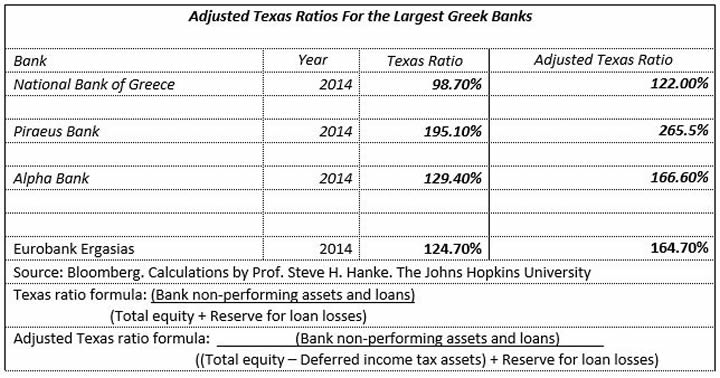

When banks are in distress, it is important to assess how easily the bank’s capital cushion can absorb potential losses from troubled assets. To do this, I performed an analysis using Texas Ratios for Greece’s four largest banks, which control 88% of total assets in the banking system.

We use a little known, but very useful formula to determine the health of the Big Four. It is called the Texas Ratio. It was used during the U.S. Savings and Loan Crisis, which was centered in Texas. The Texas Ratio is the book value of all non-performing assets divided by equity capital plus loan loss reserves. Only tangible equity capital is included in the denominator. Intangible capital — like goodwill — is excluded.

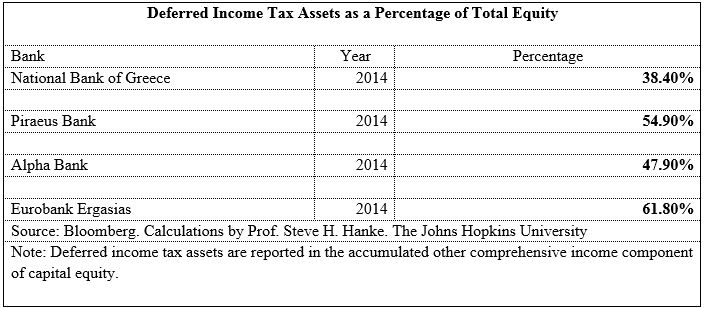

Despite the already worry-some numbers, the actual situation is far worse than even I had initially deduced. A deeper analysis of the numbers reveals that Greece’s largest banks include deferred tax assets as part of total equity in their financial statements. Deferred tax assets are created when banks are allowed to declare their losses at a later time, thereby reducing tax liabilities. This is problematic because these deferred tax assets are really just “phantom assets” in the sense that these credits cannot be used (read: worthless) if the Greek banks continue to operate at a pretax loss.

Similar to its neighbors — Portugal, Spain and Italy —Greece provides significant state support to its banks by offering credit for loss deductions for taxable future profits. For the four largest banks, this type of support made up 38-61% of total equity (see accompanying chart).

Adjusting the Texas Ratio to account for the phantom assets yields much higher ratios. These indicate significantly higher risk of bank failures, barring a capital injection (see the accompanying chart).

By Steve H. Hanke

www.cato.org/people/hanke.html

Twitter: @Steve_Hanke

Steve H. Hanke is a Professor of Applied Economics and Co-Director of the Institute for Applied Economics, Global Health, and the Study of Business Enterprise at The Johns Hopkins University in Baltimore. Prof. Hanke is also a Senior Fellow at the Cato Institute in Washington, D.C.; a Distinguished Professor at the Universitas Pelita Harapan in Jakarta, Indonesia; a Senior Advisor at the Renmin University of China’s International Monetary Research Institute in Beijing; a Special Counselor to the Center for Financial Stability in New York; a member of the National Bank of Kuwait’s International Advisory Board (chaired by Sir John Major); a member of the Financial Advisory Council of the United Arab Emirates; and a contributing editor at Globe Asia Magazine.

Copyright © 2015 Steve H. Hanke - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Steve H. Hanke Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.