CPR for the Dieing US Dollar

Currencies / US Dollar Jun 10, 2008 - 02:26 AM GMTBy: Kurt_Kasun

Perhaps we should institute DNR rather than CPR. Two days ago Fed Chairman Ben Bernanke shocked the world by commenting on his concerns regarding the fall of the US Dollar. In past policy, the Fed refrained from discussing the US currency; US dollar commentary was supposed to have been within the exclusive purview of the US Treasury. But it is now clear that the Fed is making up the rules as it goes. The remarks have had the intended result of resuscitating the buck, a welcomed response, according to today's Wall Street Journal editorial, "The Buck Stops Where," "because the price of gold and oil have fallen in each of the last two days." In this election year, there is a coordinated effort among the Treasury, the Fed, and regulatory agencies to beat down the price of commodities. If only it were that easy.

Perhaps we should institute DNR rather than CPR. Two days ago Fed Chairman Ben Bernanke shocked the world by commenting on his concerns regarding the fall of the US Dollar. In past policy, the Fed refrained from discussing the US currency; US dollar commentary was supposed to have been within the exclusive purview of the US Treasury. But it is now clear that the Fed is making up the rules as it goes. The remarks have had the intended result of resuscitating the buck, a welcomed response, according to today's Wall Street Journal editorial, "The Buck Stops Where," "because the price of gold and oil have fallen in each of the last two days." In this election year, there is a coordinated effort among the Treasury, the Fed, and regulatory agencies to beat down the price of commodities. If only it were that easy.

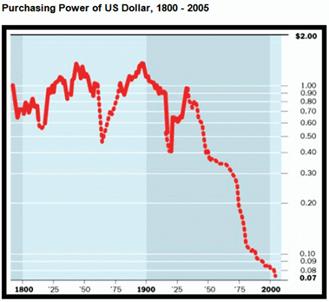

A nation's currency represents the heartbeat of that country's economy. A strong heart represents a strong patient just as a strong currency represents a strong economy. The typical lifespan for any currency over the last 3000 years has been 50-75 years. Amity Shales editorializes in today's Wall Street Journal in a piece titled "Contracts as Good as Gold:"

People these days fear inflation. We also fear changing rates of inflation...So it's worth remembering that, 75 years ago today, President Franklin D. Roosevelt destroyed an inflation hedge that was literally as good as gold: the so-called "gold clause." This helped prolong the Depression and has been causing damage ever since. Consider an investor in the gold standard era. An ounce of gold was worth $20.67 and you could, at least in theory, trade your greenbacks for gold at the bank. The gold standard checked a government's willingness to inflate, since it started losing gold when it did so. Those who traded bonds knew a confidence we can never know.

At 75 years of age, you could make the case that the patient, the US Dollar, is living on "borrowed time," which would be appropriate given the massive amount of "borrowing" that we seen with consumers, following in the footsteps of the federal government, who, as Shales notes, has from then on (referring to 75 years ago) enjoyed "wider license to inflate."

I continue to make the case, as I first outlined in my earlier commentary that the birth of our currency should be more directly tied to the formation of the Federal Reserve in 1913, and is coming up on its 100th birthday. Will this heart still be beating in 2013? I am not so sure, nor am I sure that we should want it. Rather than continual CPR efforts which would be required, perhaps we would be better served to place a DNR (Do Not Resuscitate) order on our currency.

Any efforts to maintain our currency will only result in higher inflation and a further damaged patient, the US economy. In the above mentioned commentary , I refer to three years which have sealed our economic fate. In addition to 1913 and 1933, 1971 marked the final de-linkage of our currency to gold. On August 15th of last year, Randall Forsyth wrote in a Barron's editorial marking the 36th anniversary of this de-linkage titled "That's How the Credit, and the Empire Crumble" that "The untethering of the dollar from gold 36 years ago today marked the beginning of the decline of the fall of the American empire." I don't know about ‘empire,' but it was another nail in the coffin of our flawed and failing currency.

I ask you to consider that each of these events that have changed our monetary system (Fed creation in 1913, FDRs removal of the gold standard in 1933, and Nixon's closing of the gold window in 1971) were born out of desperation rather than strength. I know that crisis and necessity are parents of invention, but there is just something very disconcerting about the distressed circumstances under which our monetary system has evolved. Shales reveals the inevitable result we have arrived today: "We have lost our bearings and our confidence in money general." The current currency regime, informally known as Bretton Woods II, is collapsing with the US dollar, as inflation soars in dollar-linked countries, forcing them to abandon their pegs to the dollar.

None other than Alan Greenspan, the maestro himself, was once one of the staunchest advocates of a strong gold-based currency. But that was just before he joined the ranks of government officials. Gene Epstein, who writes the weekly "Economic Beat" column for Barron's , insightfully reported in February piece titled, "Greenspan Was Right: The Case for Gold:'

[Greenpan] affirms that gold would check price inflation, referring to the "gold standard's inherent price stability." So why not support gold for this important reason? It turns out that, while the Greenspan of 1966 objected to chronic deficits financed by "an unlimited expansion of credit," the Greenspan of 2007 now accepts that very thing. "I have long since acquiesced in the fact that the gold standard does not readily accommodate the widely accepted ...view of the appropriate functions of government," he candidly admits -- namely, the "propensity of Congress to create benefits for constituents without specifying the means by which they are to be funded." But to accept the government's power "to create benefits...without specifying the means by which they are to be funded" is effectively to endorse the government's right to finance its operations, not just through taxing and borrowing, but through the unilateral creation of money and credit.

[Greenpan] affirms that gold would check price inflation, referring to the "gold standard's inherent price stability." So why not support gold for this important reason? It turns out that, while the Greenspan of 1966 objected to chronic deficits financed by "an unlimited expansion of credit," the Greenspan of 2007 now accepts that very thing. "I have long since acquiesced in the fact that the gold standard does not readily accommodate the widely accepted ...view of the appropriate functions of government," he candidly admits -- namely, the "propensity of Congress to create benefits for constituents without specifying the means by which they are to be funded." But to accept the government's power "to create benefits...without specifying the means by which they are to be funded" is effectively to endorse the government's right to finance its operations, not just through taxing and borrowing, but through the unilateral creation of money and credit.

On this point, gold advocate George Reisman observes: "When the government need not obtain its funds from the people, but instead can supply the people with funds, it can no longer easily be viewed as deriving its powers and rights from the people."

Two groups of people, who broadly represent the two largest segments of the American population among divisional lines, will continue to oppose and block the restoration of any type of gold standard. By limiting the amount of dollars which could be created, you limit their power to achieve their ideologically-based goals. No more "willy-nilly budget deficits," as Forsyth writes. Two traits which were critical in the formation and greatness of our country but have recently been removed from any national discourse are thrift and austerity. These two words are anathema to our culture of consumption and entitlement.

Progressive Intentions, Dreadful Consequences

As I have written before, our culture and entrenched interests will not willingly accept the strong medicine that a gold standard and disciplined monetary and fiscal policy would deliver. The pain and suffering that would immediately result is too tough for our society to bear. We have grown too accustomed to relying on "government" to "fix things" when they go awry. A recent CNN poll revealed that 82% of Americans believe that Congress is not doing enough to help the economy.

In 1913, when the Fed Reserve was established, a national income tax was put into place-at 1%! That was the proverbial camel's nose of big government entering into the tent of our free market culture and society. The first thing we need to understand is that there are no utopias. Second, we are basically following Europe 's chronology as we further lapse into government reliance and interventionism. Here is how it works: things get tough, the government intervenes with programs ‘to help', more money printing is required to fund said programs, the currency is debased and purchasing power declines, middle-class Americans fall further behind and things get even tougher and the vicious downward cycle accelerates.

In each iteration of this cycle, inflation further erodes the purchasing power of the middle class. This subtle decline in our middle class standard of living has become not so subtle. Furthermore, we are experiencing an income and wealth disparity not seen since just before the Great Depression in 1930. Those who were able to benefit from asset inflation, in both the housing and stock markets, saw their standard of living soar in both absolute terms and relative to those who did not have the means to ever possess those assets. But those gains proved to be ephemeral. In fact those who borrowed against capital gains that have since evaporated are more likely in worse shape. The only winners now are the few who are invested in assets which rise in our current inflationary environment.

The financial failures inherent in this currency-debasing, inflationary spiral are obvious. Other damaging effects to the American psyche, perhaps less so. Central government bureaucratic assistance tends to unmoor us from the collective bonds which tie us together, and we lose a sense of three important values that he defined us sense our founding:

1) Subsidiarity --that government should undertake only those initiatives which exceed the capacity of individuals or private groups acting independently. The principle is based upon the autonomy and dignity of the human individual, and holds that all other forms of society, from the family to the state and the international order, should be in the service of the human person.

2) Solidarity -we are one nation of individuals, not divided into segments; solidarity is a firm and persevering determination to commit oneself to the common good; that is to say, to the good of all and of each individual; people are to be viewed as ends rather than as instruments.

3) Freedom -to pursue happiness and private property; a person who is deprived of something he can call "his own", and of the possibility of earning a living through his own initiative, comes to depend on the social machine and on those who control it. This makes it much more difficult for him to recognize his dignity as a person, and hinders progress towards the building up of an authentic human community.

I would hope that we as a country could unite behind these principles.

I should say now that this commentary is meant to impugn the efforts or intentions of the proponents of Keynesian, interventionist economic measures, sometimes known as ‘progressives.' Rather, it is an attempt to illustrate the historical path that is currently leading us down " The Road to Serfdom ," as the late free-market economist Frederick Hayek warned in his book which bears this title. In pursuing freedom, solidarity, and subsidiarity we are each more likely to achieve our intended destinies on an individual basis, and are less likely to collectively fall prey to the harmful side-effects of over-reliance on the government.

As we become engulfed in to trying to service insurmountable debt obligations (unfunded liabilities approaching $100 trillion), we are in danger of government expenditures becoming larger than our private economy. I believe in some government intervention, but if the American people were truly aware of the debts which threaten our way of life, I think the majority would agree that we are becoming perilously closing to a tipping point. But a growing minority is actually beginning to boldly advocate socialist measures. First it will be in healthcare; next it will be the oil industry, followed by all of the other industries which emit carbon into the atmosphere. If you want to see how well nationalized oil companies do turn no further than to Mexico , where a constitutional law that prohibits privatized measures and assistance from foreigners to enhance oil recovery is threatening to make Mexico a net oil importer as early as 2014!

These are becoming desperate times, and in such times, people become susceptible to obscure messages of hope. You can expect to see further calls for government to ‘do something.' But this is where real leadership needs to emerge. In a recent interview in the Financial Times Henry Kissinger recently said, "if we give attention to our values, are candid about the nation's capabilities, and are prepared to deny the cherished American ideal that every problem has a solution that can be realized in a specific time-frame, some major problems can be managed." He was referring to our foreign policy goals when he said that, but he could have just as well been commenting on our current economic predicament. The best we can hope to do at this point is to manage the economic carnage that lurks as the first baby boomers begin to retire. Despite even the best of intentions (which is certainly not always the case) government activity, especially in the realm of economics, often yields negative unintended consequences which leave us worse off.

Take climate change, for example. It is clear that ethanol subsidies have been a boondoggle that has caused the price of corn to soar and threatened food supply for the indigent around the world. Yesterday, a Chinese province forced price cuts for a coal company for its July delivery ahead of the Olympic games. A Deutsche Bank analyst warned that "the pricing intervention measures could discourage coal supply to the region from other provinces, therefore further tightening the market and making a cap hard to implement." I am told it is hot in Beijing that time of year. I wonder what the hotel priority to receive air conditioning in Beijing is? You might want to check if you plan to attend the games. I hope that we learned our lesson in the 1970s when we tried to implement price caps on gasoline prices which resulted in shortages and rationing.

A large segment of our population, the vast majority who either have no investments or whose only exposure to the investment world is a pittance in their pension plan or 401(k), are hurting and beginning to feel a sense of desperation. They are rallying around messages of "hope" and "anything would be better than what we have endured over the last eight years." A message that they might not want to hear, but probably need to, is that things could get a lot worse. It is undeniable that the media has largely lined up behind Barrack Obama. The stories of the our economic struggles (though genuine and worsening) are hyperbolized and hyped in an effort to paint the gloomiest picture of the economy possible in an effort to tie Obama's opponent, John McCain to its causes, given he is a member of the incumbent party. I fear that we are headed to the reality of what the media is over-hyping today.

From my experience of sitting next to and learning from others who grew up in the Ukraine, Turkmenistan, Thailand, the Democratic Republic of Poland while pursuing my graduate degree in International Commerce and Policy at George Mason University a few years ago, I know that things can get a whole lot worse for us. The one recurring theme that struck in me the experiences which they shared was that we take for granted are our freedoms and resulting material benefits that we have been fortunate enough to enjoy. Not one of them ever mentioned social security or medical care as the reason they left their country to pursue permanent residency in the US . Enough knocking the progressives. I now turn my critique to the other side of the political spectrum, focusing on the "economic right."

Pathological Pollyannas

I am largely confining my discussions regarding the "political right" to the financial pundits who largely steer the discussion in the financial media. These are the people who were late to tell you to get out of tech (I was once part of this crowd), financials, and other US stocks during the crash of 2000 and who told us that a "bottom" was forming almost everyday for the next three years. After much financial pain and loss they were finally right. Well, sort of. A bottom had indeed occurred, but they wrongly (the overwhelming majority) continued to pump financial, tech, US consumer discretionary, and, for a couple of years anyway, homebuilding stocks. While most of the names in these groups moved higher, they barely outperformed inflation (real headline inflation, not the phony "core rate").

These guys (again, the overwhelming majority) have missed out almost entirely on the commodity boom which has occurred over the same period and trounced the performance of all other sectors.

They tend not to deny some of the economic hardship Main Street America is feeling, but, as they did in the 2000-2003 period, you hear this contingent claim that a bottom is just around the corner and you need to get in now or risk missing out. The stock market sniffs out the rebound six months before it happens so you better get in now is their popular refrain. This catchphrase has been repeated since the first cracks in the system were made visible on February 28, 2007 . Using the KBW Bank index as a proxy, let us see how that has worked out so far:

Courtesy: State Street Global Advisors

Ouch! That didn't turn out so well. Looks like we may be heading even lower. Now some of these financial institutions place their representatives out there to protect their investments and pump these names for less than admirable purposes. But the vast majority pathetically yearn for the good ole' days when America was indisputably, "Top Dog." They can't accept that a monumental change is occurring, wealth is irreversibly transferring to developing nations, and enormous unsustainable economic imbalances (after 37 years) are finally being unwound. Calls for "King Dollar" are silly. I refer here again to the beginning of this commentary: you have to look at the patient (the economy) before considering how to treat or heal the heart (the dollar). The patient is in no shape to take on a strong heart. Our consumption binge and accompanying debt makes a either a massive currency readjustment or total abandonment a prerequisite before a sound economy can be restored. These pathological pollayanas simply will not hear any of this.

What explains their fanatic obsession to cling to US stocks and favor them over emerging markets and commodities? How can you account for their unwillingness to admit that we are in the midst of a tectonic transformation of world leadership and investment opportunities? This might be the biggest case of denial in all of investment history. The best I can come up with is a partial explanation. In Tomorrow's Gold: Asia's Age of Discovery , Marc Faber, attempting to compare America 's situation to past countries which led the world, offers:

Cities and countries that became rich and powerful inevitably grew arrogant, overconfident and complacent and they tended to overspend...Having enjoyed incredible success, they adopted a "nothing can go wrong" attitude and committed gross efforts of optimism.

The pollayanas currently control the narrative in the investment community, though their grip is slipping as investment slowly continue their rotation out of Pro-Growth US names (tech, consumer, financials) and into commodities. Their unwavering commitment to this narrative would be commendable if it was not wrong. Their ideology is as flawed as their recent track record. Fervent supporters of free-markets, you will see them quote Frederick Hayek (mentioned earlier) and Joseph Schumpeter (economist who demonstrated the merits of "creative destruction"). But where I part company with these supply-side monetarists is their substitution of Milton Freidman for Ludwig von Mises over monetary policy.

As monetarists, they believe that the Fed can properly adjust interest rates and money supply to achieve higher sustainable rates of economic growth and controlled inflation. Austrian economists, who I follow, led by von Mises, point out that this is folly and that credit and excess money creation is doomed to bust in failure. I suppose the monetarists believe in free markets up to a point-except for where it pertains to setting interest rates and money supply. The free market should set the former and the supply of gold, should set the latter.

A favorite von Mises quote that I believe beckons for those on the political "left" and "right":

The boom produces impoverishment. But still more disastrous are its moral ravages. It makes people despondent and dispirited. The more optimistic they were under the illusory prosperity of the boom, the greater is their despair and their feeling of frustration.

If the pathological pollyanas had been around in Roman times I supposed that would have characterized the crumbling infrastructure, over-stretched military, collapsing currency, deteriorating culture, and depletion of resources as all part of "the greatest story never told." As the Visigoths and the Vandals crossed the Rhine , preceding the first and second "Sacks of Rome" they would have advised stock market participants (if exchanges had existed) to buy up shares with reckless abandon. Pointless to compare our situation to the "Fall of the Roman Empire ?" Perhaps not totally. Observe the graphs below:

From Marc Faber's In Tomorrow's Gold: Asia 's Age of Discovery , p. 300.

Courtesy: Barron's

In both instances the currency was almost totally debased in the period of 200 years...Though our coins are now currently worth more in for their metal content than they are for their face value. A penny would be worth almost three cents if you melted it for its copper and zinc material. The US was recently forced to create a law to prohibit this. Folks, the flags don't get much redder than this! David Walker, who just stepped down as US Comptroller to work for Pete Peterson (in a valiant effort to basically save us from ourselves) was quoted in Forsyth's Barron's article saying, "The Roman Republic fell for many reasons, but three reasons are worth remembering: declining moral values and political civility at home, an overconfident and overextended military in foreign lands, and fiscal irresponsibility by the central government... Sound familiar? In my view, it's time to learn from history and take steps the American Republic is the first to stand the test of time."

Fast Forward to Today: The Evidence

As an investor, it pays to steer clear of ideology and to embrace history, cycles and patterns to form any strategy. My investment views and strategy will change when the evidence changes. What is the current environment telling us? Today's trading was truly baffling on many fronts. Oil was up $5/barrel while gold was down $5/oz. The DJIA rallied over 200 points on a day when the price of oil registered its highest dollar gain in history. The stock market rallied in the face of disturbing monthly same store sales released today by our nation's retailers. It is only a slight overstatement to say that everyone is flocking to the discounters. Costco and Wal-Mart were really today's only beneficiaries.

The market celebrated when Wal-Mart's CFO informed us that their customers are now "living paycheck to paycheck" and an increasing portion of their sales are in gasoline and groceries. Credit cards are being maxed out and pension funds, 401(k)s, and life insurance policies are being raided and sold off as a last-ditch effort for consumers to be able to afford to buy necessities. I will refer to the tapped out consumer (yes after 25 years he has finally reached the end of the road) as strike one.

Strike two is the banking sector. Ah yes, the banking sector just loves all of this strong dollar talk and threat of higher interest rates. They are on life support and Bernanke is threatening to pull the plug! The monoline insurers experienced another 20% haircut as their debt ratings were downgraded. Fed vice-chairman Donald Kohn today voiced serious concern as he expects continued weak earnings and further write-downs in the banks. Growth in loan-loss reserves have not kept pace with problem assets, warranting more capital raises (and further dilution for shareholders). The next shoe to drop in the banking sector could be the small and mid-sized banks which are more leveraged to commercial and industrial lending (real estate and other). Phase one of this downturn was led by the consumer; phase two will be in the commercial sector as the economy further deteriorates. Will the Fed step in to bail out the little banks?

Consider that it takes much more effort to bail out dozens of little banks that it does to bail out one Bear Stearns. Higher rates would likely further infcrease corporate defaults. The head of credit analysis at Barclays informs us that "higher interest rates make borrowing more expensive. This combined with reduced availability of credit from capital-constrained banks could well increase defaults." As Marc Faber wrote in his most recent monthly update, "Unfortunately for the Fed, the crisis is now spreading to the real economy with great intensity." Note to Bernanke: Better cool your jets on the rate hikes.

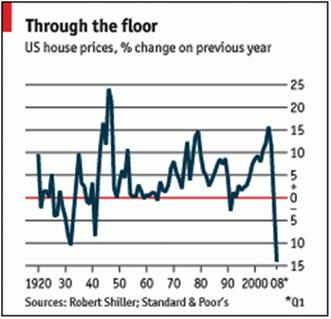

Strike three is also related to the consumer and is the biggest threat of all: the housing market. Existing home prices fell by a record 14.1% during the first quarter of 2008 and are now falling at a clip faster than during the Great Depression.

PricesCourtesy: The Economist

Perhaps more troubling was news today that people lost their homes at the highest rate on record during the first three months of this year with late payments also moving to a new high, signaling that worse is to come. Where is the evidence for the pathological pollayanas to be calling a bottom? Any economic recovery hinges on a housing turnaround. There will be no upturn or sustainable dollar strength until this occurs. Clive Crook sums up the combined effects of strikes one, two and three in a Financial Times commentary earlier this week titled "The Fed's year of living dangerously:"

The economy sags under the combined weight of house price falls, consumer confidence at a 25-year low, the credit crunch and a still widening financial sector squeeze. Nonetheless, soaring prices for oil and other commodities, not to mention the higher cost of imports thanks to a devalued dollar, are pushing up inflation and (especially) expectations of inflation. Consumers appear to have capitulated to the rise in gasoline prices - hence indications of a marked shift away from thirsty sports utility vehicles to smaller cars. The problem is that once you assume that oil at $100 a barrel will be more than a brief aberration and start to change behavior accordingly, you also begin to draw the implications for economy-wide inflation.

What's An Investor to Do?

During this election year you will likely see, despite today's record strength in oil prices and the rise of almost all commodities, sharp declines in most commodities as we did in election years 2004 and 2006. The parade of commodity bashers (George Soros, this week) continue to testify on how evil speculators need to be stopped and how price declines will follow. Despite the overwhelming academic and historical evidence to the contrary, Congress will hear none of this. Brfing on the next basher! With the Federal Trade Commission (FTC) and the Commodities Futures Trading Commission (CFTC) now being almost forced to find manipulators, traders have temporarily pulled back their long positions. Hopefully, this will not result in unsustainably-low non-free-market prices that will further lead to shortages and an even greater price spikes when free-market prices are restored to the system. The regulatory guns coupled with strong dollar jawboning should lead to declines in several commodities over the next few months.

Commodity prices most vulnerable (vulnerable until exactly the first Tuesday in November) include oil, gas, corn, wheat, sugar, and soybeans. Base metals should see a moderate correction-aluminum, zinc, copper, and nickel. These commodities represent larger positions of the broader commodity index funds and are most tied to the daily lives to the electorate which makes them the biggest targets. Less effected, based on that rationale would be the precious metals. I should note that today's decline in gold while almost every other commodity strongly rallied continues to confound me as it has over the last month as it failed to keep pace with the gains in gold.

Despite its nearly four-fold rise since 2002, gold continues to lag the gains in other commodities over the same period. It has become increasingly difficult to trade this group on a technical basis. I now believe that sometime within the next 12 months we are going to see the precious metals begin to rally almost "out of nowhere" and to assume leadership on what I believe will be a final spectacular grand finale rally for commodities.

But getting back to our current situation, there are three groups which have leaving most the others in the dust and they do not trade on exchanges (as the other commodities I mentioned do) and are not therefore not threatened by these Congressional high-jinks. They are in steel and the key ingredients required in making it-metallurgical coal and iron ore. My preference is to invest in the ingredient companies. I have recently added one company that produces both met coal and iron ore to the Global Megatrends Portfolio. The "second derivative commodity winners," mentioned in last week's commentary, are also beginning their next leg higher, benefitting from Sumitomo Metal's announcement to boost overseas mining projects and Rio Tinto's disclosure that they are seeking to develop Simandou, the world's top undeveloped iron ore resource, located in Africa. Two names owned in the Global Megatrends Portfolio are leading this group higher.

*My new retail newsletter service, the Global MegaTrends Portfolio , is now available to subscribers. Please click to learn more!

By Kurt Kasun

A contributing writer to GreenFaucet.com , Kurt Kasun writes a high-end investment timing service, GlobalMacro, which is focused on identifying opportunities that produce returns in excess of market with reasonable risk. He is strategically located in Washington , D.C. , a key to maintaining contacts and relationships which help Kurt understand global policy and economic factors as they emerge. His investment approach has always been macro in nature largely due to his undergraduate studies at the U.S. Military Academy at West Point (B. S. National Security, Public Affairs, 1989) and his graduate studies at George Mason University (M.A. International Commerce and Policy, 2006).

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any trading activities.

Kurt Kasun Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.