Russia Nervously Eyes the U.S.-Iran Nuclear Deal

Politics / Nuclear Weapons Apr 07, 2015 - 12:23 PM GMTBy: STRATFOR

Reva Bhalla writes: When a group of weary diplomats announced a framework for an Iranian nuclear accord last week in Lausanne, there was one diplomat in the mix whose feigned enthusiasm was hard to miss. Russian Foreign Minister Sergei Lavrov left the talks at their most critical point March 30, much to the annoyance of U.S. Secretary of State John Kerry, who apparently had to call him personally to persuade him to return. Even as Lavrov spoke positively to journalists about the negotiations throughout the week, he still seemed to have better things to do than pull all-nighters for a deal that effectively gives the United States one less problem to worry about in the Middle East and a greater capacity to focus on the Russian periphery.

Reva Bhalla writes: When a group of weary diplomats announced a framework for an Iranian nuclear accord last week in Lausanne, there was one diplomat in the mix whose feigned enthusiasm was hard to miss. Russian Foreign Minister Sergei Lavrov left the talks at their most critical point March 30, much to the annoyance of U.S. Secretary of State John Kerry, who apparently had to call him personally to persuade him to return. Even as Lavrov spoke positively to journalists about the negotiations throughout the week, he still seemed to have better things to do than pull all-nighters for a deal that effectively gives the United States one less problem to worry about in the Middle East and a greater capacity to focus on the Russian periphery.

Russia has no interest in seeing a nuclear-armed Iran in the neighborhood, but the mere threat of an unshackled Iranian nuclear program and a hostile relationship between Washington and Tehran provided just the level of distraction Moscow needed to keep the United States from committing serious attention to Russia's former Soviet sphere.

Russia tried its best to keep the Americans and Iranians apart. Offers to sell Iran advanced air defense systems were designed to poke holes in U.S. threats to bomb Iranian nuclear facilities. Teams of Russian nuclear experts whetted Iran's appetite for civilian nuclear power with offers to build additional power reactors. Russian banks did their part to help Iran circumvent financial sanctions. The Russian plan all along was not to help Iran get the bomb, but to use its leverage with a thorny player in the Middle East to get the United States into a negotiation on issues vital to Russia's national security interests. So, if Washington wanted to resolve its Iran problem, it would have to pull back on issues like ballistic missile defense in Central Europe, which Moscow saw early on as the first of several U.S. steps to encircle Russia.

Things obviously did not work according to the Russian plan. As we anticipated, the United States and Iran ultimately came together in a bilateral negotiation to resolve their main differences. Now the United States and Iran are on a path toward normalization at a time when Russian President Vladimir Putin is trying simultaneously to defend against a U.S.-led military alliance building along Russia's European frontier and to manage an economic crisis and power struggle at home. And the situation does not look any better for Russia on the energy front.

Russia Stands to Lose Energy Revenue

The likelihood of the United States and Iran reaching a deal this summer means that additional barrels of Iranian oil eventually will make their way to the market, further depressing the price of oil, as well as the Russian ruble. To be clear, Iranian oil is not going to flood the market instantaneously with the signing of a deal. Iran is believed to have as much as 35 million barrels of crude in storage that it could offload quickly once export sanctions are terminated by the Europeans and eased by the United States via presidential waiver. But Iran will face complications in trying to bring its mature fields back online. Enhanced recovery techniques to revive mothballed fields take money and infrastructure, which is difficult to apply when oil prices are hovering around $50 per barrel. Under current conditions, Iran can bring some 400,000-500,000 barrels per day back online over the course of a year, but this will be a gradual process as Iran vies for foreign investment in its dilapidated energy sector.

U.S. investors will likely remain shackled by the core Iran Sanctions Act until at least the end of 2016, when the legislation is set to expire. However, European and Asian investors will be among the first to begin repairing Iran's oil fields, as long as Iran does its part in improving contractual terms and the economics make sense for firms already cutting back their capital expenditures.

Europe's New Options

The rehabilitation of Iran's energy sector, however gradual a process that may be, will complicate Russia's uphill battle in trying to maintain its energy leverage over Europe. Russia is a critical supplier of energy to Europe, currently providing about 29 percent and 37 percent of Europe's natural gas and oil needs, respectively. An additional 50 billion cubic meters of natural gas available for export from the United States within the next five years will not be able to compete with Russia on price due to the low operational and transport costs of Russian natural gas. Even so, the United States will still be creating more supply in the natural gas market overall to give Europe the option of paying more for its energy security should the political considerations outweigh the economic cost. The Baltic states are already working toward this option, with Lithuania taking the lead in creating a mini-liquefied natural gas hub for the region to try to reduce, if not eliminate, Baltic dependence on Russia. This year, Poland is debuting its own LNG facility, and the Sabine Pass terminal in Louisiana is scheduled to bring the first LNG exports from the Lower 48 to market, with shipments already contracted for Asia.

In Southern Europe, the picture for Russia is more complicated but still distressing. Aside from the significant issue of cost for energy companies already cutting their capital expenditures, Turkey's veto on the transit of LNG tankers through the Bosporus effectively neutralizes any LNG import facility project on the Black Sea. But Europe is proceeding apace with the much more economically palatable option of building pipeline interconnectors across southeastern Europe. This does little to dilute Russia's control over energy supply, but it does strip Moscow of its ability to politicize pricing in Europe. Pipeline politics in Europe have allowed Russia to reward — and punish — its Eastern European neighbors through pricing contracts. However, Brussels is more thoroughly examining contracts signed by EU member states for this very reason and in line with one of the main tenets of the EU's Third Energy Package, which seeks to break monopolies by splitting energy production and transmission and to implement fair pricing. Meanwhile, the construction of interconnectors allows member states to influence pricing downstream from Russia.

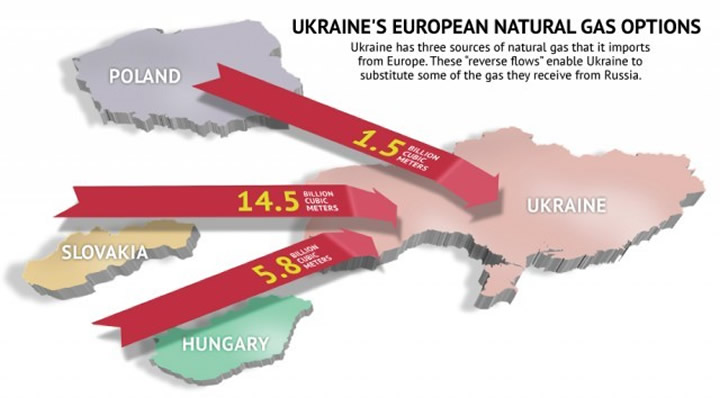

This gambit has been on display over the past year in Ukraine. Kiev depended heavily on its neighbors in Slovakia, Poland and Hungary for reverse flows of Russian natural gas at discounted rates to stand up to Russia's energy swaggering. Though Russian natural gas will still be flowing primarily through these pipelines, the expansion of interconnectors will open up options for non-Russian natural gas from the North Sea and from LNG terminals in Northern Europe to make their way southward to embattled frontline states such as Ukraine.

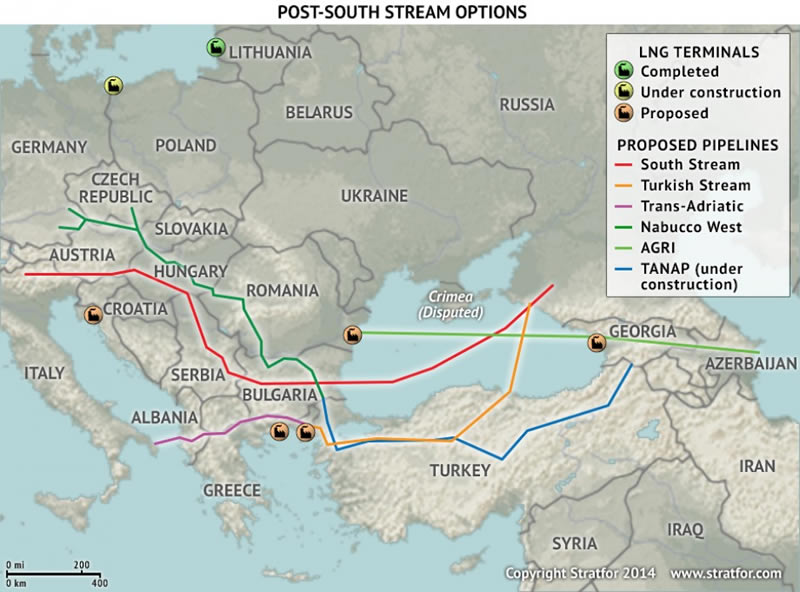

Russia thought it would be able to keep a hook in Southern Europe through the construction of South Stream, a mammoth pipeline project with a $30 billion price tag and 63-bcm capacity that sought to cut Ukraine out of the equation by moving natural gas across the Black Sea and through the Balkans and Central Europe. The combination of plunging energy prices and growing EU resistance to another pipeline that would allow Russia to draw political favors sent this project to the graveyard, but Russia had a backup plan. The Turkish Stream pipeline would make landfall in Turkey after crossing the Black Sea, before using the Trans Adriatic Pipeline and the Trans Anatolian Pipeline to feed Southern Europe through the web of interconnectors and pipelines already in development. On the surface, Moscow's plan appears quite brilliant: Use the very infrastructure that Europe was already counting on to diversify away from Russia and then, when the political skirmishing over Ukraine eventually settles down, reinsert itself into Europe's energy mix via a willing partner like Turkey.

Post-South Stream Options

But the plan remains full of holes. Someone needs to pay for the main pipeline expansion between Russia and Turkey, and both countries will struggle to find private investors in this geopolitical and pricing climate. Moreover, there is no indication that the Europeans will be willing to take additional Russian natural gas from a yet-to-be-built Turkish Stream when a perfectly good pipeline running from Russia to Eastern Europe already exists. Russia does not have the option of refusing natural gas shipments when it is already desperate for those energy revenues. In the end, this is a Russian bluff that the Europeans will not be afraid to call. When Putin agreed to a three-month natural gas deal with Ukraine last week (with a huge discount to boot, at $247.20 per thousand cubic meters), he likely did so realizing that Russia playing hardball with Ukraine on energy would only spur further investment and construction into pipelines and connectors in southeastern Europe that would accelerate the decline of Russia's energy influence in Europe. The best he can hope for is to slow that timeline down.

Not only will Russia's pricing leverage wane in Europe over the long term, but its influence on Europe's energy supply also will decrease over the longer run. Azerbaijan was the first southern corridor supplier to Europe circumventing Russia and is now expanding that role by bringing natural gas from its Shah Deniz II offshore fields online for export. Turkmenistan is still vulnerable to Russian meddling but has been increasingly willing to host Turkish and European investors looking to build a pipeline across the Caspian to feed Europe. Whether these talks translate into action will depend on the Turkmen government's political will to stand up to Moscow, not to mention legal battles over the Caspian Sea. But while the lengthy courting of Ashgabat by the West continues, a rehabilitated Iran is now the latest addition to the list to join the southern corridor.

Russia's Influence Wanes in the Middle East

Just a day after the Iranian nuclear framework deal was announced, Russia's state-owned RIA Novosti published a story quoting Igor Korotchenko, the head of the Moscow-based Center for Analysis of World Arms Trade, as saying it would be a "perfectly logical development" for Russia to follow through on a sale of S-300 surface-to-air missiles to Iran if the embargo is lifted. Korotchenko noted that specifications to the deal would have to be made as "the United States is watching very closely" to whom Russia sells these weapons. Russian Deputy Foreign Minister Sergei Ryabkov also made a point to say the U.N. arms embargo against Iran should be lifted as part of the nuclear deal. These well-timed statements likely caught Washington's eye but probably did little to impress. The S-300 threat mattered a lot more when the United States needed to maintain a credible military deterrent against Iran. If the United States and Iran reach an understanding that neutralizes that threat through political means, Russian talk of S-300s is mostly hot air.

This was a small, yet revealing illustration of Russia's declining position in the Middle East. For many years, the Middle East was a rose garden for the Russians, filled with both sweet-smelling opportunities to lure Washington into negotiations and ample thorns to prick their American adversary when the need arose. Russia's support for the Syrian government is still relevant, and Moscow will continue to court countries in the region with arms deals out of both political and economic necessity. Even so, bringing down the Syrian government is not on Washington's to-do list, and countries like Egypt will still end up prioritizing their relationship with the United States in the end.

Russia's influence in the Middle East is fading rapidly at the same time Europe is starting to wriggle out of Russia's energy grip. And as Russia's options are narrowing, U.S. options are multiplying in both the Middle East and Europe. This is an uncomfortable situation for Putin, to be sure. But a narrow set of options for Russia in its near abroad does not make those options any less concerning for the United States as the standoff between Washington and Moscow continues.

"Russia Nervously Eyes the U.S.-Iran Deal is republished with permission of Stratfor."

This analysis was just a fraction of what our Members enjoy, Click Here to start your Free Membership Trial Today! "This report is republished with permission of STRATFOR"

© Copyright 2015 Stratfor. All rights reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis.

STRATFOR Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.