Gold Price $250 Forecast - Dear Harry Dent: Wanna Bet?

Commodities / Gold and Silver 2015 Feb 18, 2015 - 04:04 PM GMTBy: Jeff_Clark

Some of you may be aware that investment guru Harry Dent has publicly stated that gold will fall to $250-$400. He specifically predicted:

Some of you may be aware that investment guru Harry Dent has publicly stated that gold will fall to $250-$400. He specifically predicted:

Around $700/ounce is a certainty in gold by 2015 to 2016, and $250 is a possibility well down the line by 2020–2023.

His forecast is largely based on his belief that deflation will prevail.

Governments are fighting deflation. If government stimulus fails, we will have deflation, not inflation.

And he claims that gold bugs are wrong about gold’s future price because they don’t understand how markets work.

Central bank stimulus has created a whole new set of financial asset bubbles that will have to burst. That is its consequences, not rising inflation that most gold bugs (who do understand the financial and debt crisis) warn about.

As a gold analyst who’s spent every day of the last seven-plus years watching this market, I can’t let this pass. I’m sure gold will not fall to $700, much less $250-$400—not in real terms (who knows if the US dollar will even exist in 2020?… Or maybe there will be new dollars with several zeros cut off).

Is this just because I’m a stubborn gold bug? No, because I agree that we’re seeing some deflation, too. But I definitely think some type of crisis is headed our way, and gold does well in crises—even deflationary ones.

Is it perhaps because I don’t like Mr. Dent? Not at all—at my suggestion, he was a speaker at one of our Summits.

Quite simply, I think Harry Dent is resoundingly wrong. And I’m so sure he’s wrong that this is a public invitation to him to enter a wager with me and put his money where his mouth is, which I’ll detail momentarily.

Why Harry Dent Is Wrong

There are a number of reasons why I think Mr. Dent will be wrong about the future gold price…

1. Deflation does not guarantee lower gold. It’s true that some significant deflationary forces have developed. Check out what’s occurred since early November.

- The 10-year Treasury fell to a paltry 1.7% yield.

- The oil price dropped to $50.

- January retail sales recorded the worst back-to-back decline since October 2009.

- Commodity indexes have fallen by over a third.

- The Baltic Dry Index, generally regarded as the best known global shipping index, is now at its lowest level ever.

- According to the Financial Times, there is now $3.6 trillion of government debt around the world with negative interest rates. Two-year government bonds are negative in Germany, Finland, Austria, Denmark, France, Holland, Belgium, Slovakia, Sweden, and Japan.

These are all serious deflationary trends. But what has gold done during that period? It is up 7.5%.

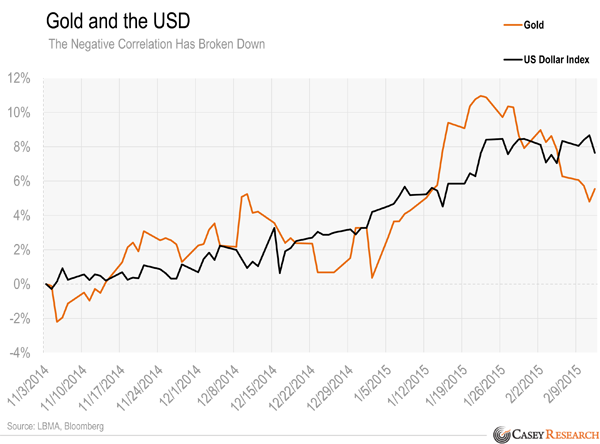

Even gold’s negative correlation with the dollar has bucked its trend.

This dollar/gold relationship has broken down other times, too. According to the Wall Street Journal:

- From January 11 to June 10, 2010, the DXY (US Dollar Index) rose almost 16%—but gold climbed nearly 12%.

- Since the turn of the century, gold and the DXY index have both finished higher year over year five times—in 2001, 2005, 2008, 2010, and 2011.

So why has gold risen during some of the most ominous deflationary trends we’ve seen in a long time?

Because what has been supportive for the dollar has also been good for gold.

In other words, gold is not just about inflation vs. deflation. Nor is it about the USD vs. the euro or even supply vs. demand. It’s about fear and chaos vs. confidence and stability.

Here are some recent examples of people buying gold for reasons other than inflation:

- Greek demand for gold coins from the UK Royal Mint has risen as a result of the country’s political and financial turmoil. They’re buying because, as Matthew Turner of Macquarie Bank put it, “The one thing everyone knows about gold is it is a good thing to hold if your currency is about to devalue.”

- After the Swiss central bank introduced a 0.75% negative interest rate on some deposits last month, investors bought more gold in lieu of holding Swiss franc cash deposits, according Vontobel Holding AG, a Swiss bank and wealth manager. “We keep noticing that gold is coming back into favor with investors,” said CEO Zeno Staub.

- Other European countries have seen a spike in gold demand due to the massive QE effort undertaken by the ECB and the anti-bailout party winning in Greece. German coin dealer Degussa reported a 35% year-on-year increase in gold coin sales in January. The Austrian Mint said sales of Vienna Philharmonic gold coins rose 6% last month.

So the investor who’s convinced deflation is coming shouldn’t overlook the fact that other factors can lead investors to buy gold. Keep in mind that most true deflations cause a crisis—or are caused by a crisis—and for thousands of years, crises have pushed people into gold.

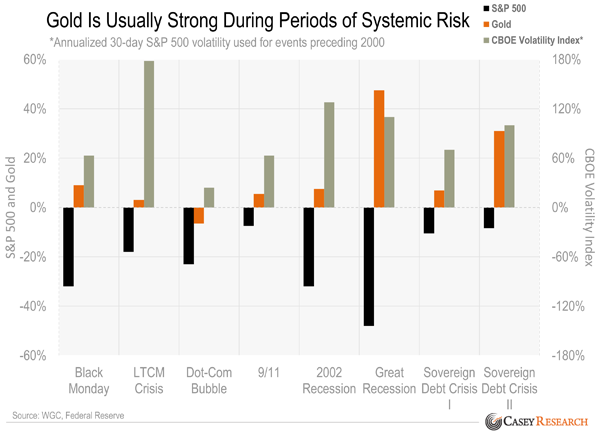

Consider how gold has performed during high periods of crisis and fear as measured by the VIX.

During these eight periods of high systemic risk, gold rose every time but one—and stock markets fell in all of them. This doesn’t mean the price couldn’t decline in the initial phases of a crisis, but it does show that gold is strong when fear is high.

2. True deflation will lead to higher inflation.

If we do get massive deflation, it will actually spur greater inflation.

Why? Here’s a hint…

An emergency meeting was held just last week regarding the solvency of the Disability Trust Fund. The problem is that benefits have exceeded tax receipts for several years now, and the shortfall has reached roughly 35%. The government itself has said the fund will officially go bankrupt next year.

It’s not the only one.

| Projected Government Bankruptcies | |

| Highway Trust Fund | 2016 |

| Disability Trust Fund | 2016 |

| Pension Benefit Corp | 2024 |

| Hospital Insurance | 2030 |

| Old Age Insurance | 2034 |

And did you know that Social Security took in $752 billion in 2013, but paid out $822 billion in benefits? It and Medicare are clearly on an unsustainable path, too.

Yes, this is all deflationary. But here’s the question: how will the Fed and politicians respond? They might reduce or delay benefits and raise taxes, but those are politically costly moves, and some officials have already publicly stated that they will print what they don’t collect in revenue.

Printing money is extremely inflationary, especially when you’ve already more than tripled the monetary base since 2008. Frankly, doing more of the same scares me, because someday all this monetary dilution will come home to roost. We face the very real possibility that the US currency will not just be damaged; it could be destroyed.

History is very clear on this point: currency crises lead to flights to gold.

But if Deflation Wins First…

But what happens to gold if we first go through a deflationary bust?

There aren’t a lot of modern-day examples of deflation. The Consumer Price Index (CPI), as faulty as it may be, has registered only four declines since 2000, and all were short-lived. The CPI fell:

- August to October, 2006;

- July to December, 2008;

- March and April, 2009; and

- December, 2014.

That’s it. You can find other fleeting periods further back, but nothing long enough to draw any strong conclusions.

The only example we have of true deflation is the Great Depression. You’ll recall that the United States was on a gold standard at the time.

But there’s still a lesson to be learned.

First, on April 5, 1933, President Roosevelt issued an executive order forcing delivery (confiscation) of gold owned by private citizens to the government in exchange for compensation at the fixed price of $20.67/oz. Less than nine months later, he raised the gold price to $35, effectively diluting the dollar in every wallet 41% overnight and swindling everyone who had turned in gold. So even in the midst of one of the biggest deflations the world has ever seen, the US government raised the gold price.

Second, the only way citizens could effectively own gold after Roosevelt’s confiscation was to buy gold stocks. How did they perform? Well, when the stock market crashed in 1929, gold stocks were part of the general wreckage. The market then rallied and recovered almost 50% of its losses by April 1930, with gold shares again tagging along. It’s what happened next that gives us another clue about gold and deflation…

When the bear market resumed in the summer of 1930, all securities sold off again—except gold stocks. Gold shares stayed basically flat until early 1931, when their appeal to the masses kicked into high gear.

Look at how shares of Homestake Mining, the largest gold miner in the US at the time, and Dome Mines, Canada’s senior producer, performed during the Great Depression.

| Company | Stock Price 1929 | Stock Price 1933 | Total Gain* |

| Homestake Mining | $65 | $373 | 474% |

| Dome Mines | $6 | $39.50 | 558% |

| *Returns exclude dividends | |||

During a period of soup lines, crashing stock markets, and falling standards of living, investors fled to the only gold with liquidity they could own at the time.

Gold’s status as a safe-haven asset during one of the greatest times of economic distress was demonstrated clearly by investors buying the stocks. So while we don’t know exactly what an untethered gold price would have done during the Depression, history says it will retain its purchasing power in a deflationary setting regardless of its nominal price. In other words, while the price of gold might not rise or could even fall, it would still provide monetary protection against an unstable economic environment, especially when you consider that most other assets would be in decline.

All this said, the overriding concern is that in a fiat system—like the one the entire globe uses today—any deflation will be met with an inflationary overreaction by central bankers. And the worse the deflation, the more extreme the overreaction will be. As we’ve pointed out before, inflation will win in the end because it always gets another turn.

Think about it: for central banks to be “successful” with their measures, the end result must be inflation. Someday soon they’ll get what they want. And when it shows up, the delayed effects of all the money created to that date will start to take hold, meaning there won’t be “just a little” inflation. Gold will soar in that environment, not fall.

Of course, it doesn’t have to be an either/or thing. We can have both inflation and deflation, AKA stagflation, like we had in the late 1970s/early 1980s. That’s still good for gold.

3. Gold is already at its cost of production.

Another reason I’m sure Mr. Dent will be wrong is that $700 is about $400 below the current global average cost of gold production. Even at $1,100 gold, roughly half of the primary gold producers lose money.

The reason is because the World Gold Council’s all-in sustaining cost metric excludes taxes and interest payments (among other items). Adding those in pushes many companies into the red when gold averages $1,100.

A $700 gold price would be 36% below the current cost of production. That (much less a $250 or $400 price) would kill the industry. But the sector won’t shut down, because the world needs and wants gold.

The Bottom Line

The basis of my argument is that there is no free lunch from the free-for-all actions central bankers have engaged in since 2008. Inevitably, the future purchasing power of our fiat money will be impacted. I thus think some kind of currency crisis hits in the future, perhaps sooner than skeptics like Harry Dent can imagine.

There are many examples of what happens to gold during a currency crisis. Last year provided another glaring example. Russia’s inflation rate was 11.4% in 2014, and the ruble fell a staggering 46.5%—but gold in rubles rose 73%. In other words, Russians gained more with gold than they lost in ruble purchasing power.

This didn’t occur just in conflict-ridden Russia. The price of gold rose against all currencies in 2014—except the US dollar. Gold was up in the euro, Japanese yen, Swiss franc, Canadian dollar, British pound, Australian dollar, New Zealand dollar, Chinese renminbi, Indian rupee, Swedish krona, Brazilian real, Israeli shekel, and South Korean won.

As Eric Sprott put it, “Last year, 84% of the world’s population would have made money owning gold because of various currency moves—even though gold in US dollars was down approximately 1%.”

We should expect the same reaction with gold in our currency when the odoriferous effluvia hits the fan.

Gold is not really a commodity or even an investment; it is an alternate currency and a store of value. And if ever there was a period in history for it to be sought as a store of value, the next few years will be among the most acute. Both gold and the US dollar have been pursued during the recent times of distress—but the dollar as a “safe haven” is at high risk. It may rise further yet, but it’s far from healthy; the US is the largest debtor nation in the history of mankind.

There are more reasons—I’m sure you can think of others yourself—but let’s get to the wager.

The Bet

Mr. Dent, I will bet you an ounce of gold that the gold price never falls to US$700, including intraday, for even one second, within the next two years, based on Comex pricing. You stated in January 2014 that “$700 is a certainty by 2015 to 2016,” so I’m giving your forecast even longer to work than you originally projected.

We’ll each store a one-ounce gold Eagle with an independent third party, who will pay the two ounces to the winner the day the bet is concluded, which is two years from today, February 16, 2017. If gold touches US$700 at any point in that time frame, you win. If, however, gold never reaches $700, this lunatic gold bug who doesn’t understand how financial and debt crises works wins the bet and takes your ounce of gold.

I hope you’ll take me up on the bet, because that’s about the time my son will finish his PhD program, and an ounce of gold will make a nice graduation present for him. It will also reinforce the ideas he’s formed on his own about money, as well as the fact that his dad is a stud.

I do have to give you fair warning, though: I’m so confident that I’ve already identified a third party, and I will give you its mailing address once you shake my digital hand.

Mr. Dent, do you really think gold will fall to $700? A gold Eagle says you’re wrong.

I await your reply…

I’m not just going to win this bet, but I’ll win big with my equity investments, because gold stocks will deliver the leverage to gold that they have many times in the past, especially since they’ll rise from depressed levels. I plan to make a killing on some special situations—and I have one right now: a new recommendation in the current issue of BIG GOLD. It’s one that tripled my money in the last bull cycle and will do it again in the next one. Easy money will be made if you buy now, and our brand-new recommendation is available with a risk-free trial to BIG GOLD.

Casey Research Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.