The Chinese Copper Elephant

Commodities / Copper Dec 25, 2014 - 01:50 PM GMTBy: Richard_Mills

Wood MacKenzie sees stronger prices for copper.

"Over the last 10 years, copper's annual average growth rate in demand has been 13% for China. The annual growth rate over the next five years is going to be 5%. Over the last 10 years, average annual copper consumption has been 600,000 tonnes, and going forward it's going to be 500,000 tonnes..." - Northern Miner

Rio Tinto

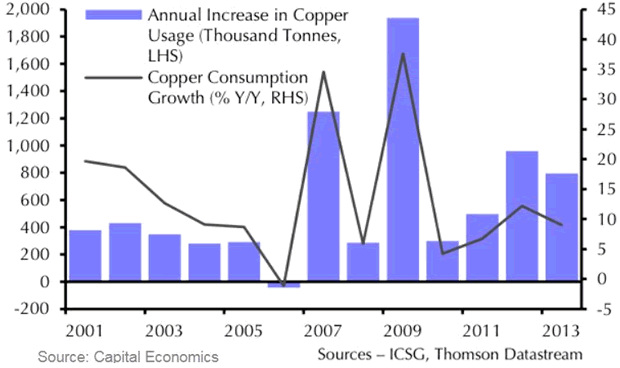

An October update to the Thomson Reuters GFMS 2014 Copper Survey predicts global demand will have grown by 859,000 tonnes in 2014.

Again from the Northern Miner interview with Julian Kettle head of metals and mining research at Wood Mackenzie in London:

"Copper is always the most interesting metal, and the issue with copper is that we get disruptions to supply on an ongoing basis. Mine disruptions will typically vary from 3-8% of global copper supply, but this year we think it's going to be above trend at 5-5.5%. So this year, we'll see about 1 million tonnes of copper supply taken out of the market.

TNM: Why are disruptions so typical of copper?

JK: There are a whole range of factors. You've got pit-wall failures, strike action, technical issues, slow ramp-ups, weather-related issues and grade. If you were to look at what's happened so far this year, the major contributor to disruption has been lower ore grades, slow project ramp-ups and a disruption to supply out of Indonesia because of the concentrate export ban. You had Grasberg reduce production levels to 60% of capacity and you also had a short-term stoppage of production at Batu Hijau."

The International Copper Study Group forecast the copper market, after five straight years of deficits, should swing into a 2015 production surplus of roughly 390,000 tonnes - less than a month of current daily demand. It's obvious that even short lived disruptions would will have a huge impact on copper's price.

BNP Paribas said that 18 new mines and expansions could result in 1.8 million mt of new mine supply over the next two years. If we can count on Thomson Reuters GFMS 2014 Copper Survey prediction of global demand growing by 859,000 tonnes in 2014 being carried forward another two years it's very evident there is little to no copper surplus if we factor in even the low 3% estimate let alone use the 5.5% (1 million tonne) estimate given by Julian Kettle.

The elephant in the copper supply room is China, after all the country does consume 45% of the worlds copper.

"Time to turn positive on base metals, by Caroline Baine, senior commodities economist at Capital Economics, features a graph that shows China's copper consumption growth in relation to physical copper usage.

It highlights the fact that like GDP, copper consumption in the country is now coming from a much higher base and points out that a 9% increase in copper consumption in 2004 resulted in a 280,000 tonne increase in usage, while the 9% jump in 2013 represented nearly 800,000 tonnes of additional copper.

Even better, copper consumption growth is outpacing overall economic growth and according to the independent research house the latest data suggest that China's apparent copper consumption will have grown by a robust 10% this year and demand indicators point to strengthening going into 2015."

- Frik Els, China vs copper - much better than you think, Mining.com

Conclusion

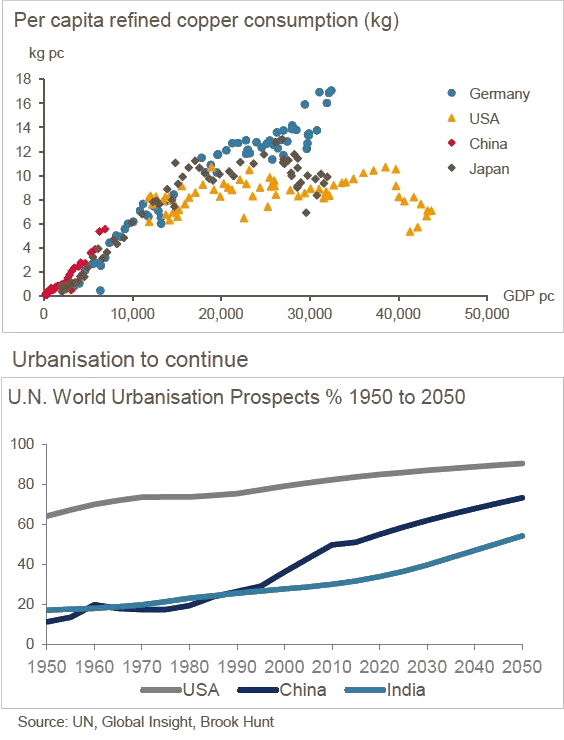

This author believes that the US and Europe are, or are in the process of becoming, mostly irrelevant when it comes to the demand side of the copper supply equation. Increased demand for the red metal in developing nations will more than make up for decreased demand in the western world. And when western economies recover, as they eventually must, then the supply squeeze will become even tighter.

The citizens of the worlds developing nations aspire to have what we have, the ease of travel, home phones, electricity, central plumbing, heating and air conditioning, cars, toys, consumer electronics and home appliances.

When you consider the recent lack of exploration spending, increasing demand from developing countries, country risk (the Democratic Republic of the Congo, the DRC, comes to mind) declining resources/grades at the world's largest copper mines and that a sufficient number of new deposits that have been found are not being brought on stream in a timely enough fashion - and those that are, carry, for the most part, much lower grades than those presently being mined then you might be forgiven for coming to the same conclusion that I have - If even just one small black swan event happens in the finely balanced, extremely tight copper supply sector people are finally going to realize just how precarious our supply situation is regarding the red metal.

China alone has one fifth of the world's population, India another 1.2 billion people, most of them want the same quality of living and level of consumerism and materialism we enjoy in the west. Most of our forecast population growth is expected to come from developing countries and Africa is expected to provide the lion's share of that growth.

Could copper come into a major demand squeeze? Is the red metal on your radar screen?

If not, maybe you should.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2014 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Richard (Rick) Mills Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.