Euro-Zone Tooth Fairy Economics, Spain Needs to leave the Euro

Economics / Eurozone Debt Crisis Nov 20, 2014 - 03:29 PM GMTBy: Mike_Shedlock

Michael Pettis has a very interesting article on the Spanish news site ABC regarding a possible default of Spain and the eventual breakup of the eurozone.

Michael Pettis has a very interesting article on the Spanish news site ABC regarding a possible default of Spain and the eventual breakup of the eurozone.

Pettis Three Ways

- His article El exceso de deuda impide el crecimiento in Spanish.

- His article Debt Overhang Prevents Growth as translated by Google.

- His article Excess Debt Hampers Growth as translated by Microsoft Bing (Much, much slower than Google translation).

I used both translators in a verification process. What follows is my heavily modified translation of key portions of Pettis' article after reading both of the above translations.

In the Panic of 1837, two-thirds of the US, including several of the richest states, suspended payment of external debt. The United States survived. If the European Union is to survive, it will have to find a solution to the European debt.The more hope instead of action, the more likely there's a permanent breakdown of the euro and the European Union.

In a gesture more of faith than economic or historical data, Madrid assures us that with the right reforms, it will eventually be able to get out of debt.

Other countries in debt crises have made the same promise, but the promise is rarely fulfilled. Excessive debt itself impedes growth. Even without the straitjacket of the euro, Spain probably cannot afford its debt.

Even those who are against debt cancellation recognize that the only thing that shielded Germany from a Spanish default was the European Central Bank.

Despite their obnoxious policies, far-right parties across Europe flourish more than ever because the ECB protects the euro and European banks at enormous costs for the working and middle classes.

These extremists exploit the refusal of European leaders to acknowledge their errors. The longer the economic crisis, greater their chances of winning, and then comes an end to Europe.

The only thing that prevented a suspension of payments by Spain and other countries was the promise of the European Central Bank in 2012 to do "whatever it takes" to protect the euro. But debt continues to grow faster than GDP in Europe, and the European Central Bank load increases inexorably month after month.

There will come a time when rising debt and a weakening of the German economy will jeopardize the credibility of the guarantee of the European Central Bank (which will be useless), little by little at first, and then suddenly later. In a matter of months Spain will suspend payments.

For now, with debt settlement postponed, German banks strengthen capital to protect themselves from bankruptcy that many predict.

Berlin is playing the same game as Washington during the crisis in Latin America in the 1980s. Then US banks actively strengthened their capital, mainly at the covert expense of ordinary Americans, while insisting that Latin American countries needed further reforms and no debt forgiveness. However, multiple reforms led to extremely high rates of unemployment and enormous social upheaval throughout Latin America.

From 1987 to 1988, when US banks finally had enough capital, Washington officially recognized that full payment of the debt in 1990 was impossible and forgave the debt of Mexico. In the years following, US banks forgave almost the entire debt of other Latin American countries.

As has happened throughout history, it was only after debt forgiveness did Latin America finally begin to grow.

In Spain, it has to happen the same. German and European banks need to strengthen their capital, but it will be many years before they succeed. Only then, and only after Spain endures extremely high unemployment, senseless suffering, and tremendous social harm, will Berlin 'discover' Europe needs the debt relief.

Even if "saving the banks" deserved so much effort, the choice does not depend on Spain alone. The insolvency of small economies like Cyprus and Greece nearly collapsed the system. If Portugal, France, Italy or another country decides not to pay, this would generate enough panic to take Spain into the crisis as well. Each country in Europe has to be willing to pay the cost of protecting the banks.

History has made it clear that the cost of protecting the banks will be enormously high, and then it's likely a debt crisis occurs anyway. This means that ordinary people have to pay twice: first as covert transfers that strengthen bank capital and second with a high rate of unemployment and social erosion. Then, in most cases, the ordinary people do not get any of the advantages because either way, the crisis occurs.

To prevent this tragic history repeating, Spain needs open the debt debate honestly and democratically, asking whether protecting European banks is worth many more years of hardship! We must also be aware that history shows that however much we fight, the crisis will occur anyway.

There is no reason why Europe cannot recognize this unsustainable setup and make the necessary adjustments. Otherwise, the most likely winners will be extremist parties who want to put an end to the EU.

Political Arrogance

Of course there is a reason for this mess (just not a good one). The reason is political arrogance. Bureaucrats in every eurozone country committed to the project in spite of known flaws in the structure.

Problem Paragraphs

I struggled translating two paragraphs from the original article the Spanish . Here is the Google translation of the paragraphs in question. Emphasis mine. The first paragraph is especially convoluted.

Even those who are against debt cancellation recognize that all he has done that Spain has been no suspension of payments has been the guarantee of Germany, shielded after the European Central Bank. They note that as the German banking system could not survive the bankruptcy of even one country, Berlin has no choice but to endorse the Spanish debt forever.Suspension of payments in Spain

... There will come a time when rising debt and weakening the German economy will jeopardize the credibility of the guarantee of the European Central Bank (which will be useless) little by little at first and then suddenly later. In a matter of months will result in the suspension of payments in Spain.

Matter of Months

In the first problem paragraph above, I wonder if "he" is Draghi. If so, what follows is still not at all clear. I bounced both paragraphs off reader "Bran" who lives in Spain.

Bran replied "It is not clear in the original sentence if the ECB is shielding Germany with its related actions to the guarantee, or if it is shielding a guarantee offered by Germany, perhaps both. In other words, the ECB is using the perceived economic strength of Germany as a shield for its actions regarding Spain, simultaneously shielding Germany from Spanish default ."

In the second problem paragraph, it is unclear if Pettis means a suspension of payments will happen "in a matter of months" (from now), or a matter of months following realization that ECB guarantees are useless. I presume the latter. So does reader "Bran".

Translation Issues

Translation issues are more difficult this time because the article on ABC was itself a translation and I cannot find the original source in English. The article on ABC may have come from an interview or perhaps something Pettis sent to ABC.

I have an email in to Pettis seeking clarification and correction of anything I may have gotten wrong, as well as anything ABC may have gotten wrong.

Target2 Imbalances Revisited

When it comes to "suspension of foreign payments", I presume Pettis implies or incorporates Target2 Imbalances.

I discussed Target2 imbalances recently in Eurozone Target2 Imbalances Rise Again, Led by Italy.

Pater Tenebrarum at the Acting Man blog provides this easy to understand example.

"Spain imports German goods, but no Spanish goods or capital have been acquired by any private party in Germany in return. The only thing that has been 'acquired' is an IOU issued by the Spanish commercial bank to the Bank of Spain in return for funding the payment."

I have stated many times, Spain will never be able to pay back what it has borrowed from Germany. But that is not close to the full extent of the problem.

Cascading Defaults

Pettis believes Spain should discuss leaving the Euro. Let's investigate what happens if Spain does just that, starting with a look at the European Financial Stability Facility (EFSF).

The EFSF's mandate is to safeguard financial stability in Europe by providing financial assistance to euro area Member States within the framework of a macro-economic adjustment programme.The EFSF was created as a temporary rescue mechanism. In October 2010, the euro area Member States decided to create a permanent rescue mechanism, the European Stability Mechanism (ESM). The ESM Treaty was signed in February 2012 and the ESM started its operations on 8 October 2012.

When this programme is concluded in December 2014, the EFSF will continue to operate, as it is necessary to roll over outstanding EFSF bonds, which were issued to raise funds for the financial assistance programmes for Ireland, Portugal and Greece. This is necessary because the maturity of loans provided to these countries is longer than the maturity of bonds issued by the EFSF.

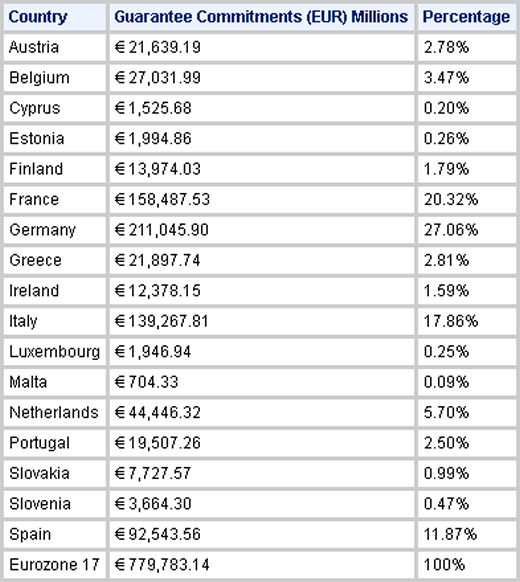

Table of Responsibilities

Wikipedia provides this assessment of the EFSF.

The table below shows the current maximum level of joint and several guarantees for capital given by the Eurozone countries. The amounts are based on the European Central Bank capital key weightings.

Guarantees Questioned

In the above table it's the percentages that I am most concerned about. The amounts may not be current.

Notice that Greece, Portugal, and Ireland are responsible for percentages of guarantees even though they are recipients of the program.

Should Greece or Portugal choose to leave the Euro, would Spain be able to pick up 12% of the tab?

Well, what if Spain does what Pettis asks and then suspends payment on what it owes Germany?

Could Italy and France pick up their share? Greece?

Cascade of Defaults

Should any country decide to exit the eurozone, expect a cascade of followers.

Notice that the ECB and EU fools brought this upon themselves. Greece could have defaulted long ago, with arguably a minimum amount of damage. Now Greece is saddled with hundreds of billions of euro "bailouts" that Greece cannot and will not repay.

One can only wonder how many trillions of dollars worth of derivatives would be immediately affected should a cascade occur. The ECB would of course would "guarantee" the amounts. But How?

The only conceivable answer is printing enough euros so that every Target2 imbalance can be met. That would violate ECB rules of course, but history shows central banks don't give a damn about rules in a crisis.

Should a panic scenario play out that way, the euro would collapse.

Alternative to Destructive Breakup

The alternative to a cascading and destructive breakup of the eurozone would be for Germany to exit the Eurozone first.

In that scenario, the euro would sink, the Deutschmark soar (at least initially), and trade would have some chance of balancing out. The collapse would have some semblance of order rather than total panic.

But, Germany would be paid back in euros, not Deutschmarks. Thus, no matter which way it plays out, Germany is 100% guaranteed to suffer major losses going forward. So are all of the other Northern eurozone creditor countries.

Thus, in spite of what anyone thinks, Germany cannot possibly avoid being hit, and hit hard.

The only open question is whether the process is somewhat controlled, or eventual panic sets in. Unfortunately, politics is such that I strongly suspect the latter.

Contingent Liabilities

I bounced the above off Pater Tenebrarum at the Acting Man Blog before posting. He chimed in with with an interesting set of comments.

Even the "strong" eurozone nations would be in truly dire straits if the contingent liabilities of the ESM were to come due.

Consider Austria, which has the lowest unemployment rate in the EU and is widely considered "rich". At the end of 2013, its government debt amounted to €262 billion, or 82% of GDP. Its 2013 annual deficit was €4.8 billion (it will soar in 2014 due to the Hypo Alpe Adria wind-up). Austria's ESM contingent liability is more than €21 billion!

This is not exactly small potatoes. It's about 7% of the country's GDP.

GDP incorporates "all spending on final goods, plus trade surplus, plus fixed capital investment." Final goods now include the drug trade and prostitution! But GDP cannot pay for debt or liabilities. Those must be paid from actual revenues/net income. So the ESM is a very unstable construct indeed.

Also, one must not forget, the losses have already occurred. Who has to pay for them has merely been postponed in the vain hope that the EU can "grow out of them" (similar to how banks are getting "fixed" via financial repression).

Worse yet, there is no sound economic policy that guarantees growth - not even in Germany. For example, Germany's government now has a disastrous energy policy in the vain attempt to do something about the non-problem of "climate change". It costs so much that it has appreciably lowered Germany's standard of living.

Household electricity bills have exploded into the wild blue yonder. Now the Germans have introduced minimum wages as well - which everybody already knows is going to raise unemployment.

Don't ask me why they have done this - it's utterly moronic. And it's the same problem everywhere - economic policies in Europe are based on a prosperity illusion/hallucination. Politicians all think there still is "surplus wealth" they can redistribute - but this is an illusion. Barely any new wealth is actually created.

Tooth Fairy Economics

Pater says "don't ask me why they have done this". Actually he knows. The answer is political arrogance in conjunction with unfading belief in the Tooth Fairy and Santa Claus.

The Tooth Fairy is Monetarism (free money under the pillow). Santa Claus is Keynesian economics (free gifts to everyone).

Not even Japan can convince economic fools of the stupidity of their programs.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2014 Mike Shedlock, All Rights Reserved.

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.