Scary Bank of Japan Goes All In Again - Abenomics 2.0

Economics / Japan Economy Nov 11, 2014 - 08:13 PM GMTBy: John_Mauldin

Grant Williams writes: Last week, appropriately enough on Halloween, the Bank of Japan did something truly scary.

Grant Williams writes: Last week, appropriately enough on Halloween, the Bank of Japan did something truly scary.

As shocks go, this one — though it had been fairly well-telegraphed to the markets that something wicked this way might be coming — was in a league of its own.

I’m sure that by now you’re well aware of what Kuroda-san (the Governor of the Bank of Japan) announced to the world; but in case you’re not, here’s a little recap:

(Japan Times): The bank will “enter a new phase of monetary easing in terms of quantity and quality,” Kuroda said.... “This is coming from a different level in both quality and quantity,” Kuroda told reporters after the two-day Policy Board meeting. “We have put forward everything there is to do at this point,” he said....

The former chief of the Asian Development Bank said the BOJ will aim to expand the amount of outstanding JGBs by hiking purchases to an annual pace of ¥50 trillion.

Increasing the amount outstanding of the bank’s JGBs at an annual pace of ¥50 trillion will bring the current balance of ¥89 trillion to about ... ¥190 trillion by the end of 2014.

It also will target longer-term debt, including JGBs with maturities as long as 40 years, as well as ETFs and real estate investment trusts, it said....

Kuroda said he’d allow this monetary experiment to run until the inflation target is met.

He also said the main target of the BOJ’s operations would switch from the uncollateralized overnight call rate to the monetary base, which will be fattened via money market operations to the tune of about ¥60 trillion to ¥70 trillion a year.

Kuroda also pledged that the BoJ:

Will invest ¥1 trillion in exchange-traded funds and ¥30 billion in real-estate investment trusts annually.

Vows to continue quantitative and qualitative monetary easing until 2 percent inflation is achieved in a stable manner.

Will conduct monetary market operations so Japan’s monetary base expands at an annual pace of about ¥60 trillion to ¥70 trillion per year. The monetary base is cash in circulation and the balance of current-account deposits held by financial institutions at the BOJ.

Shocking? Unprecedented? Foolhardy?

All of the above... except...

That was the announcement Kuroda made in April of 2013 as the first of Abenomics’ Three Arrows was fired.

Last week, barely 19 months after the world digested the news that Japan was going all-in, Kuroda pointed over the shoulders of all the other players at the table, said “Look! Behind you! An Austrian economist!” And in the ensuing panic, he slipped a bunch of freshly minted chips from a secret pocket in his jacket onto the table and, once calm had returned, went all-in again.

This time, apparently, he was serious.

The Bank of Japan, said Kuroda, would first be increasing its purchases of JGBs to ¥80 trillion a year from the previous range of ¥60-70 trillion.

What does this mean in real(ish) money? Well that’s about $720 billion. Sounds OK, right? After all, TARP was $787 billion, and that hasn’t done any damage whatsoever, has it?

However, there’s this age-old problem with comparing apples to oranges; and so, once we get our citrus fruits straight and convert the BOJ’s stimulus to a number proportionate to the larger economy of the USA, we find ourselves staring at the equivalent of the BoJ’s splashing out almost $3 trillion. Each year.

JP Morgan swiftly pointed out that this means the BoJ will be buying more than double the amount of new JGBs issued by the government.

Yes. You read that right. Double the total new government issuance. The Fed are lightweights compared to this mob.

We’ll get back to why they’re doing this a little later.

But this is just the beginning.

The BoJ will also triple its purchases of ETFs and J-REITs (yes, direct intervention by a Central Bank into the stock market is now not something to be afraid of, but rather embraced) which will make the BoJ the largest buyer of Japanese equities.

Do you smell anything wrong with this, Dear Reader?

Well, by way of a change, a few mainstream commentators are also beginning to question the logic of Kuroda-san’s latest incursion into monetary madness:

(Gavyn Davies, FT): [The BoJ’s] gigantic increase in QE activities... [is] ...of first order global importance… ensuring that the total central bank injection of liquidity into the global economy in 2015 will be much larger than it has been in the last year....

The Japanese injection... relative to the size of the economy, is far larger than anything attempted by the other central banks.

[Japan is now conducting] a laboratory experiment... [and] Governor Kuroda’s monetary experiment has in effect morphed into a strategy of devaluation plus financial repression.

But Davies isn’t alone in highlighting the sheer madness of Kuroda’s latest move:

(Richard Katz, The Oriental Economist): In the face of growing loss of faith in the Bank of Japan’s ability to either achieve its 2% inflation target in the foreseeable future or to help boost real growth, Kuroda has doubled down his strategy of lots of confident talk and even more money-creation.... (I)t is well known that Prime Minister Shinzo Abe, who keeps a stock monitor in his offices, sees rising stock prices as critical to voter confidence in Abenomics and hence his own approval ratings.... Moves to lower the yen and raise stock prices are key to the BoJ’s own strategy and tactics; Kuroda is an Abe ally, not a puppet.

However, leave it to David Stockman — one of the shoutiest sane people you’ll ever come across — to dispense with journalistic niceties.

In a piece entitled The BOJ Jumps the Monetary Shark — Now the Machines, Madmen and Morons Are Raging, Stockman takes Kuroda and the BoJ to task as only he can:

This is just plain sick. Hardly a day after the greatest central bank fraudster of all time, Maestro Greenspan, confessed that QE has not helped the main street economy and jobs, the lunatics at the BOJ flat-out jumped the monetary shark. Even then, the madman Kuroda pulled off his incendiary maneuver by a bare 5-4 vote. Apparently the dissenters — Messrs. Morimoto, Ishida, Sato and Kiuchi — are only semi-mad.

Never mind that the BOJ ... balance sheet which had previously exploded to nearly 50% of Japan’s national income or more than double the already mind-boggling US ratio of 25%.

In fact, this was just the beginning of a Ponzi scheme so vast that in a matter of seconds it ignited the Japanese stock averages by 5%. And here’s the reason: Japan Inc. is fixing to inject a massive bid into the stock market based on a monumental emission of central bank credit created out of thin air. So doing, it has generated the greatest frontrunning frenzy ever recorded.

The scheme is so insane that the surge of markets around the world in response to the BOJ’s announcement is proof positive that the mother of all central bank bubbles now envelopes the entire globe.

The “surge of markets” to which Stockman refers illustrates the madness that has consumed both equity and bond markets in the wake of the 2008 ceding of custody of formerly free markets to the world’s central banks.

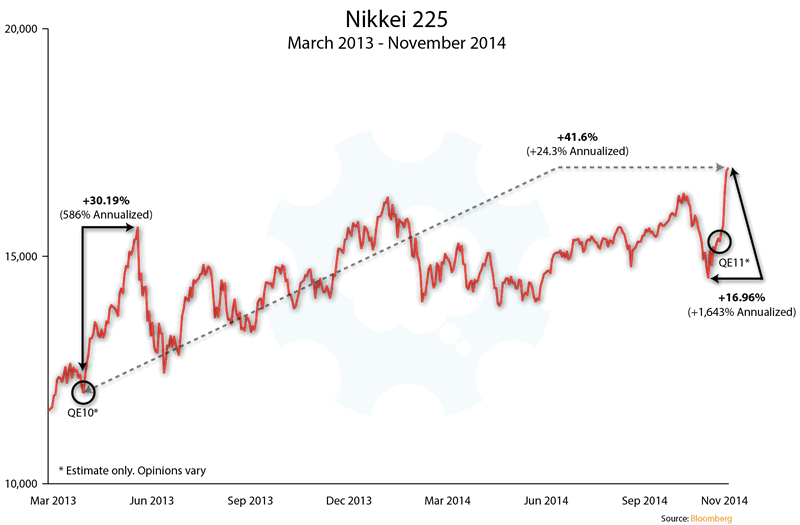

These are the two charts that people care about when discussing the Bank of Japan’s moves.

Firstly, the Nikkei 225:

As you can see, stocks have exploded in Japan since the beginning of Abenomics, rising 41.6% in just 19 months — but it wasn’t a straight line. Initially, after a 30% surge, the doubts set in and the Nikkei retraced most of its gains before beginning a long grind higher as investors reluctantly bought into the idea that Abenomics might just work raise the Nikkei 225.

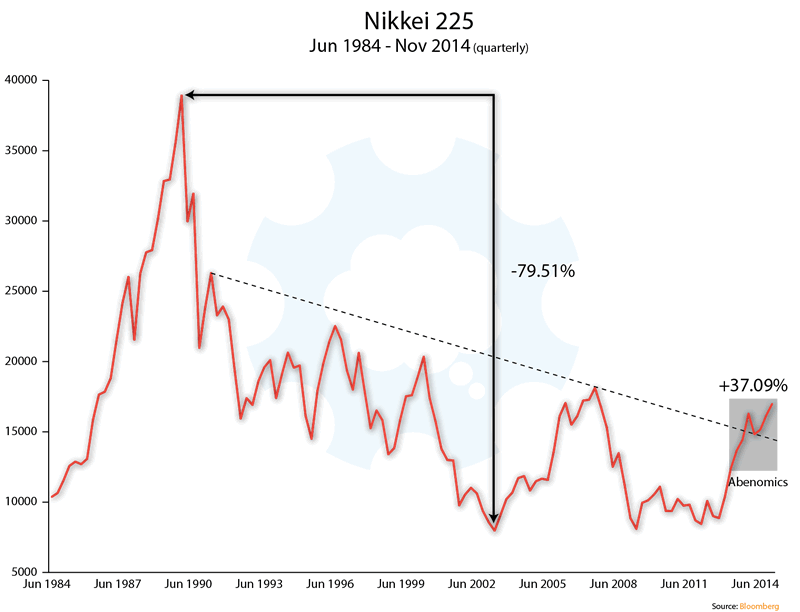

Taking a step back, we get to see just how poorly stocks have behaved since the bursting of the twin Japanese bubbles in real estate and equities back in the late 1980s, as well as the clear breakout, retest, and break higher from the 25-year downward trendline:

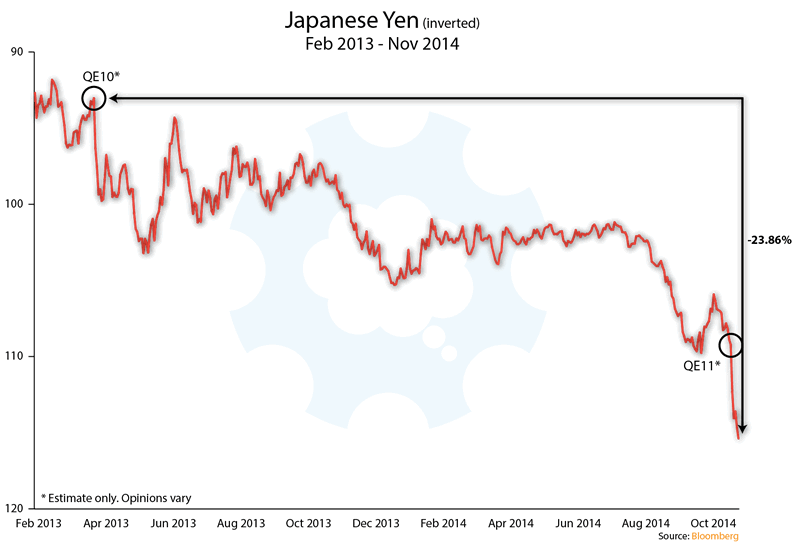

The second chart that folks care about in the wake of the BoJ’s moves is this one, the yen:

Again, as you can clearly see, QE10 and now QE11 jumpstarted the yen. (Are you paying attention, Janet? Do you think for a second that when the BoJ announced QE1, it was as the first installment of a cunning 11-part plan to be implemented over a couple of decades?)

However, jumpstarted tends to imply a positive effect, as does a chart that travels from bottom-left to top-right. In the chart above, I have inverted the yen to better reflect the damage being done to it by the BoJ rather than the kinda-cool-looking chart where it explodes “higher.”

Of course, thanks to the wisdom of guys like Kyle Bass (whose Rational Investor Paradox warned of a plummeting yen and a skyrocketing Nikkei) and Dylan Grice (whose 63,000,000 call for the Nikkei by 2025 is occasioning fewer chuckles by the day), everybody is riding both these horses — hard. However, the fact that everybody got “long the Nikkei” and everybody got “short the yen” when Abenomics’ first arrow was fired is the wrong reason to be cheering Kuroda’s interference in the natural forces that used to drive markets.

Now, “long the Nikkei and short the yen” is undoubtedly a great trade and has much further to go — something my friend Jared Dillian pointed out in his excellent Daily Dirtnap recently. Pointedly, the piece was entitled “Unlimited Upside”:

(The Daily Dirtnap): I am starting to wonder if nobody understands why this trade works and why it will continue to work, and why, in November 2012, I called it “THE GREATEST TRADE EVER.” The reason it is the greatest trade ever is because you literally have unlimited upside. JPY can infinitely weaken. The stock market can go infinitely high....

So USDJPY is going to get to 120 in a hurry, then what? You’ve seen the chart. If it gets through that trendline, the sky is the limit. Where could the Nikkei go? Beats the heck out of me. But that is the great and interesting thing about this trade, is that if Japan really does find itself in trouble, they can’t default — well, I suppose they could, and that actually would be the smart thing to do, but no, they will print their way out.

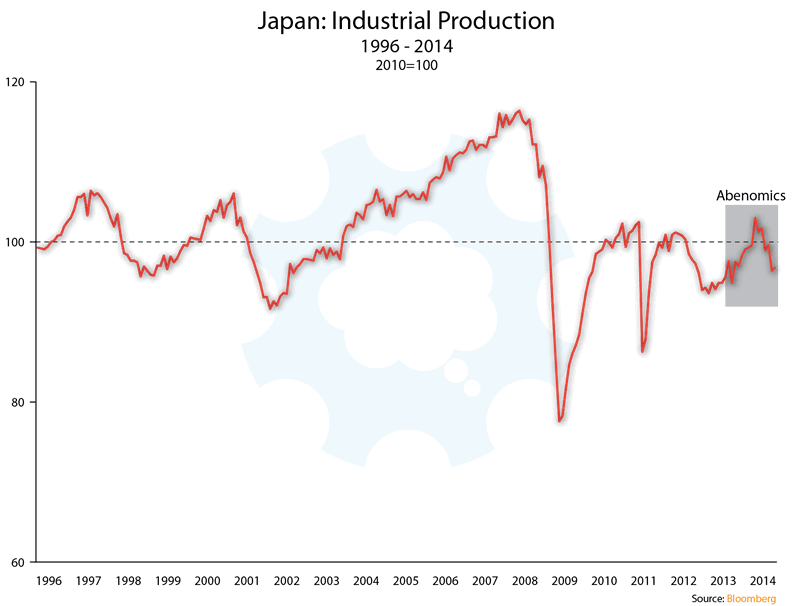

No arguments from me there, Jared, BUT... the charts that people need to be looking at to try to understand the dire state Japan is in (as well as the ultimate futility of the Keynesian free lunch) are charts of things that can’t be directly influenced by the BoJ but which are instead supposed to be indirect beneficiaries of Abenomics and to generate the organic growth needed to revive Japan’s moribund economy.

Charts like... oh, I dunno, Japanese industrial production:

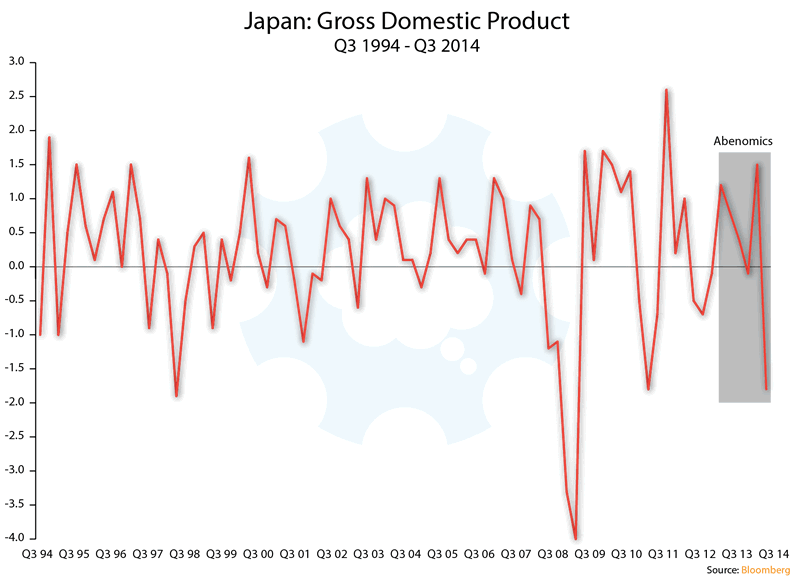

Orrrr... perhaps that relatively unimportant macroeconomic datapoint, GDP:

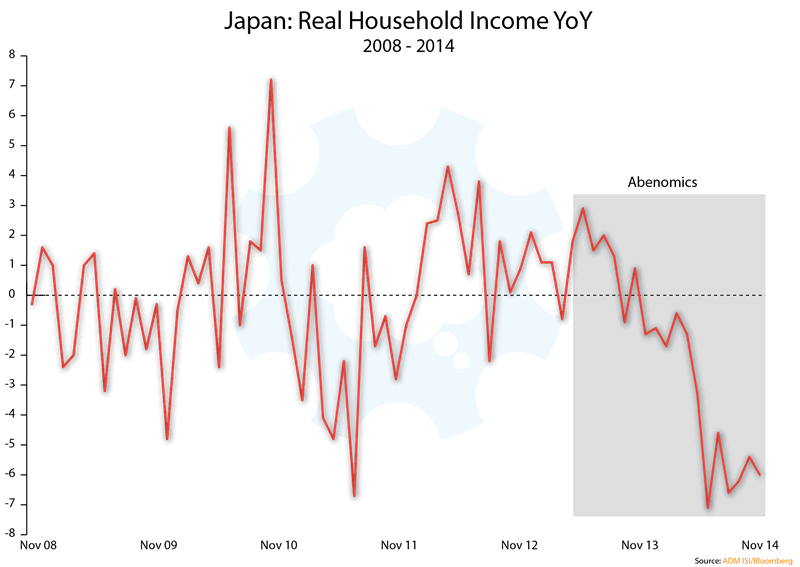

Then there are the places my friend Paul Mylchreest of ADM ISI looked at this week in an excellent piece that landed in my inbox — places like real Japanese household incomes:

(Paul Mylchreest): You only know with hindsight, but there’s a good chance that Japan’s economy has just moved into the terminal ward of mismanagement and decline.

Kuroda went nuclear just as Mr and Mrs Watonabe… never mind the rest of the world… had begun to realise that “Abenomics” wasn’t working.

Real household incomes in Japan are running 6.0% lower year-on-year, which is close to the worst they’ve been in a decade… and most of the bad data points have followed the implementation of Abenomics.

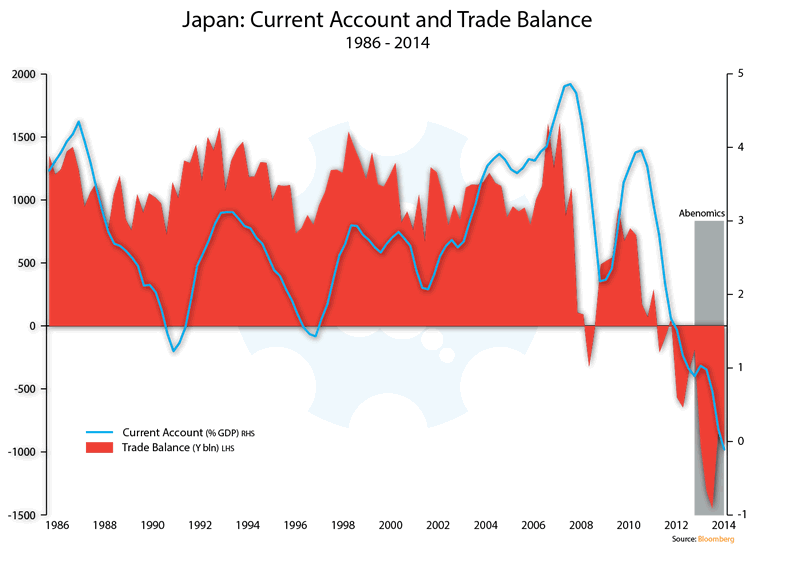

And then of course there are the twin charts from my presentation at the Strategic Investment Conference back in May: Japan’s trade balance and current account (updated here to show the improvement in the data):

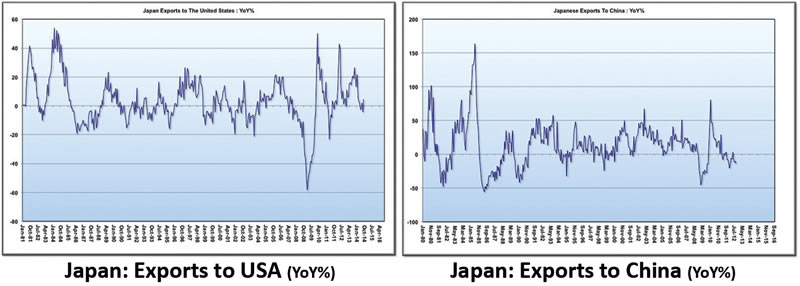

In his most recent Global Macro Investor, my friend and colleague Raoul Pal pointed out a couple more problems with the Japanese economy that no amount of prestidigitation can hope to cure, beginning with the reaction to Abe’s recent sales tax hike and moving swiftly along to exports (ordinarily the natural beneficiary of a plummeting currency for an exporter like Japan):

(Global Macro Investor): Japan’s economy has reacted as it always has with regards to the tax hike — it got flushed down the toilet…. It puts to rest any stupid notions that you can falsely raise inflation and see it stick. It also shows that QE does not help the economy in any way.

We can also see that massive Japanese QE has not helped its industrial production base…. And exports are just not picking up with a cheaper currency…. And even after a massive currency move versus the RMB, it is still not able to export its way out of trouble… demand is just not there, regardless of price….

Ahem!

So the simple truth is this:

Japan’s only solution to its crippling debt burden and seemingly unbreakable deflationary spiral is to weaken its currency.

Period.

Yes, there is plenty of talk of reform, though given Japan’s corporate culture that is far harder to achieve and much farther in the distance than most outside observers could possibly imagine; but were the narrative presented to the world simply as “we are going to destroy our currency,” even the market monkeys who continue to see no evil would be forced to take drastic action.

By maintaining the pretense that weakening the yen is actually part of a broader strategy which will ultimately be successful, the Bank of Japan is engaged in simply that: pretense.

Now don’t get me wrong: I’m not saying the necessary reforms CAN’T be achieved in Japan — just that theywon’t. Not in time to save the country from disaster at the hands of Abe, Kuroda, and the rest of the Crazy Gang, anyway.

Those stagnant exports are a huge, flashing-red warning sign in the face of what can only be described as a resounding success in beginning the complete destruction of weakening the yen.

Click here to continue reading this article from Things That Make You Go Hmmm… – a free newsletter by Grant Williams, a highly respected financial expert and current portfolio and strategy advisor at Vulpes Investment Management in Singapore.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.