Gold's Fundamental Supply Picture

Commodities / Gold and Silver 2014 Nov 07, 2014 - 05:31 PM GMTBy: Richard_Mills

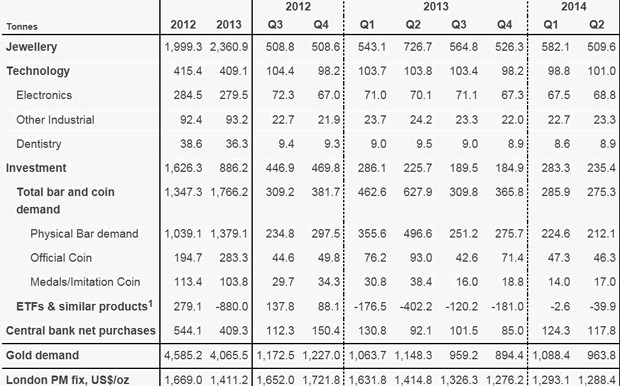

Demand

Demand

Global gold demand was 964t in Q2 2014, significantly reduced from the record high in Q2 2013.

ETF outflows slowed sharply.

Central Banks continued to buy gold for the 14th consecutive quarter in Q2 2014. CB's purchased 118t in Q2 2014 up 28% over Q2 2013. The announcement of a fourth CBGA in the second quarter also reiterated that sales will not be forthcoming from some of the largest holders.

Jewellery demand weakened year-on-year, but the broad, 5-year uptrend remains intact. Jewellery accounted for 53% of gold's global demand and is by far and away the anchor of gold's market.

Supply

China is the largest producer in the world, accounting for around 14 per cent of total production. East Asia as a whole produces 21 per cent of the total newly-mined gold. Latin America produces around 18 per cent of the total, with North America supplying around 15 per cent.

Around 19 per cent of production comes from Africa and 5 per cent from Central Asia and Eastern Europe.

Recycling accounts for around one third of the total supply of gold.

Thanks to the World Gold Council you now know where gold comes from, whose buying it and what they use if for.

Deeper into the #'s

Gold comes from three sources:

- Central Banks - sales stopped and are staying stopped.

- Recycling - mostly flat in 2014.

- Mining

Global gold demand across all sectors in 2013 was 4,065.60t.

The top 2013 six gold producing countries - China 420t, Australia 227t, U.S. 226t, Russia 220t, Puru 150t, South Africa 145t and Canada 120t - together produced 1,653.00t.

Other top gold producing countries include Mexico 100t, Ghana 85t, Brazil 75t, Indonesia 60t and Chili 55t.

According to GFMS estimates total gold mine supply reached 2,982 tonnes in 2013, up 4.1% from 2012.

High grading & refocusing

Two mostly unrecognized influences are at work in the global gold market, unsustainable production levels and a shifting of demand focus.

Many miners are processing greater quantities of ore to maintain revenue and contain costs at today's lower gold prices.

It's also very possible some companies are focused on solely mining the higher grade portions of their mines. The result is higher production and lower costs over a short term, but it is not sustainable and means a much higher gold price is needed to economically mine the lower grades left.

The focus of the gold industry is shifting east.

The key driver of gold's price over most of the last decade was institutional investors buying gold bullion through exchange-traded funds (ETF). That changed in 2013 with investors dumping 800t or 31m ozs.

On the other side of the trade was an enormous physical, almost insatiable, gold demand coming from Asia. According to GFMS China imported unprecedented amounts of gold from the rest of the world and became the world's largest consumer of jewellery last year, with demand rising 30% to 724 tonnes.

The quest for gold

Here's a few facts from SNL Metals & Mining's 2014 edition of 'Strategies for Gold Reserves Replacement.'

Over the past two dozen years mining companies have discovered 1.66 billion ounces of gold in 217 major gold discoveries. That's a lot of gold!

But it wasn't enough - there were 1.84 billion ounces produced over the same period. That's a shortfall of 180 million ounces of gold for reserve replacement over the 24 year period or a shortfall of 7.5m ozs a year.

The amount of gold discovered and the number of major discoveries has been trending downward - from 1.1 billion ounces in 124 deposits discovered during the 1990s to 605 million ounces in 93 deposits discovered since 2000.

"The amount of potential production from these major discoveries is particularly concerning when looking at the discoveries made in the past 15 years. Assuming a 75% rate for converting resources to economic reserves and a 90% recovery rate during ore processing, the 674 million ounces of gold discovered since 1999 could eventually replace just 50% of the gold produced during the same period.

However, considering that only a third of the discovered gold has been upgraded to reserves or has already been produced, and that many of these deposits face significant political, environmental or economic hurdles, the amount of gold becoming available for production in the near term is certainly much less.

Between 1985 and 1995, 27 mines with confirmed discovery dates began production an average of eight years from the time of discovery. The time from discovery to production increased to 11 years for 57 new mines between 1996 and 2005, and to 18 years for 111 new mines between 2006 and 2013.

The length of time from discovery to production is expected to continue trending higher: 63 projects now in the pipeline and scheduled to begin production between 2014 and 2019 are expected to take a weighted-average 19.5 years from the date of discovery to first production." Kevin Murphy, mining.com

Conclusion

The production of mined gold remains well below market demand. As long as demand exceeds mined supply how can gold's bull run be over? Your author doesn't believe it can be.

The best way to profit is to buy when everyone else has sold and assets are at rock bottom prices. That would be now.

Your best bet for high returns will be to invest in junior resource companies.

After all, they find the deposits, so they own the world's future mines, yeah that's right, junior resource companies own the gold the gold miners need to replace their reserves.

Why don't we all ignore the endless bombardment of economic white noise spewing from mainstream media outlets and instead concentrate on gold's fundamental supply problems?

I've got a couple promising junior gold companies on my radar screen. Do you have a few on yours?

If not, maybe you should.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2014 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Richard (Rick) Mills Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.