Europe: Building a Banking Union

Politics / Eurozone Debt Crisis Oct 30, 2014 - 11:53 AM GMTBy: STRATFOR

The recent stress tests by the European Central Bank offered few surprises and did not cause any significant political or financial reactions in the Continent. However, these tests were only the beginning of a complex process to build a banking union in the European Union. Unlike the stress tests, the next steps in this project could create more divisions in Europe because national parliaments will be involved at a time when Euroskepticism is on the rise. More important, the stress tests will not have a particular impact on Europe's main problem: tight credit conditions for households and businesses. Without a substantial improvement in credit conditions, there cannot be a substantial economic recovery, particularly in the eurozone periphery.

The recent stress tests by the European Central Bank offered few surprises and did not cause any significant political or financial reactions in the Continent. However, these tests were only the beginning of a complex process to build a banking union in the European Union. Unlike the stress tests, the next steps in this project could create more divisions in Europe because national parliaments will be involved at a time when Euroskepticism is on the rise. More important, the stress tests will not have a particular impact on Europe's main problem: tight credit conditions for households and businesses. Without a substantial improvement in credit conditions, there cannot be a substantial economic recovery, particularly in the eurozone periphery.

Analysis

The European Central Bank had two basic short-term goals for this year's stress tests. On one hand, it had to come up with a test that was tough enough to be credible after tests held in 2010 and 2011 were widely seen as too soft and lacking in credibility. On the other hand, the tests could not produce results dire enough to generate panic. The European Union is going through a phase of relative calm in financial markets, and the European Central Bank was not interested in creating a new wave of uncertainty over the future of Europe's banks.

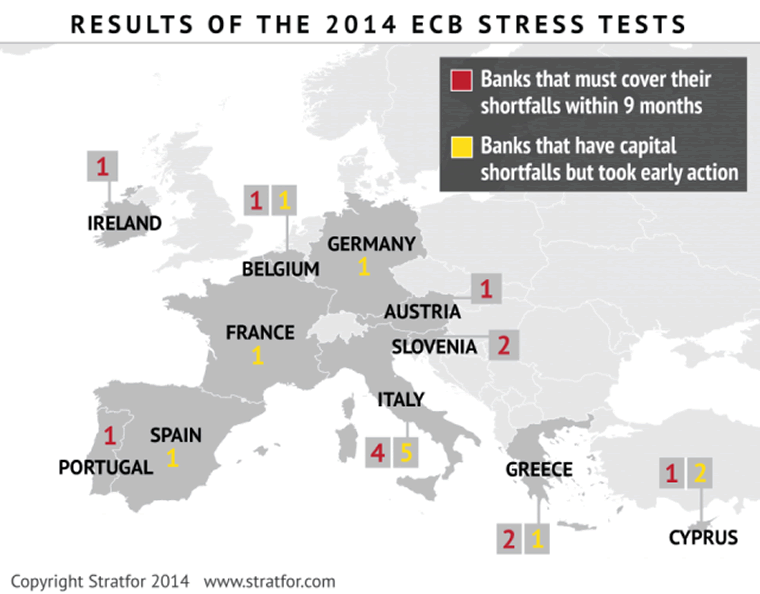

While the tests did attract some criticism, the central bank achieved both goals. Of the 130 banks involved in the tests, 25 had capital shortfalls, a finding slightly more severe than forecasts projected. Of those 25 banks, 13 must raise fresh capital and come up with 9.5 billion euros ($12.1 billion) in the next nine months. None of the failed tests came as a surprise, however. Italy's Monte dei Paschi, the worst performing bank in the tests, has been in trouble for a long time and had to receive assistance from the Italian government in 2012. Other failing banks are located in countries such as Slovenia and Greece, which have been severely affected by the financial crisis. And while the price of several banks' shares dropped during the Oct. 27 trading session, no collapses occurred.

The tests were not perfect -- they used data from December 2013 and were mostly done by each participating state. The methodology and scenarios were also criticized. For example, the most extreme "adverse scenario" included in the tests considered a drop in inflation to 1 percent this year, although the rate has already fallen to around 0.3 percent. The decision to include only 130 "systemic" banks while turning a blind eye on smaller -- and probably weaker -- institutions also drew criticism. But overall, markets considered the tests legitimate, especially in comparison with the weak tests that have taken place since the beginning of the European crisis.

The stress tests, however, are only the starting point in the much deeper and complex process of creating a banking union in Europe. The issue has traditionally been very controversial in the Continent. As Europe became more integrated, several policymakers proposed the creation of a banking union to complement the Continent's internal market and common currency. Nationalism and diverging political interests, however, made this quite difficult, and the idea was abandoned during the Maastricht Treaty negotiations in 1991 and again after it was reconsidered during deliberations for the Treaty of Nice in 2000.

But the eurozone crisis -- and the fear of financial instability spreading among the countries that share the euro -- has reignited the debate about a banking union. Simultaneous crises in countries such as Spain and Ireland, where national governments were forced to request international aid to rescue failing banks, made Europe consider the need to break the vicious circle between banks and sovereigns.

The Upcoming Political Debate

In 2012, the European Union announced that the banking union would be implemented in two stages. During the first stage, the European Central Bank would centralize the supervision of participating banks' financial stability. At a later stage, Brussels would introduce a "Single Resolution Mechanism" and a "Single Resolution Fund" to be responsible for the restructuring and potential closing of significant banks.

The first stage of the banking union was controversial because some member states refused to give the central bank full power to supervise every single bank in the European Union. A compromise was eventually found, and the bank was given supervisor powers over banks with holdings greater than 30 billion euros or 20 percent of their host nation's gross domestic product. This was not a minor compromise. National regulators remained in charge of supervising smaller banks such as Spain's cajas and Germany's Landesbanken, institutions generally having strong ties with local political powers -- and troubled balance sheets. The stress tests were a precondition for this stage of the banking union implementation process.

As the November implementation of the banking union's first stage draws nearer, the Europeans will have to make difficult political decisions regarding the second phase of the project. Twenty-six members of the European Union (Britain and Sweden decided not to participate) signed an intergovernmental agreement in May to create a special fund and a central decision-making board to rescue failing banks. According to the agreement, the fund will be built up over eight years until it reaches its target level of at least 1 percent of the amount of deposits of all credit institutions in all the participating member states, projected to be some 55 billion euros. The fund will initially consist of national compartments that will gradually merge into a single fund. The agreement also made official the "bail-in" procedure for future rescue plans.

Members of the European Parliament have said the fund should be larger because it may not be enough to deal with a new banking crisis. There is also the question of how the Single Resolution Fund will be financed. On Oct. 21, the European Commission proposed that the largest banks, representing some 85 percent of total assets, contribute around 90 percent of the funds. Opponents have criticized that instead of designating the contributions in proportion to the risks each bank presents, the proposal assigns contributions using a bank's total assets. The European Council, which represents member states, will have to ratify this proposal.

More important, the transfers of banks' contribution to the Single Resolution Fund are scheduled to start in January 2016. Before that happens, however, the parliaments of member states will have to ratify the intergovernmental treaty that was signed in May, a difficult proposition in the wake of rising Euroskeptical parties. In addition, a group of German professors have said they would challenge the banking union before the German Constitutional Court. According to this group, the banking union represents a huge risk for German taxpayers while leaving Berlin without any oversight authority. This is the same group that is currently challenging the European Central Bank's Outright Money Transactions bond-buying program.

The Real Problem: A Lack of Easily Accessible Credit

While the stress tests and asset quality review offer a clearer view of banks in Europe, most European households and businesses are facing more immediate problems. On Oct. 27, the central bank revealed that loans to the private sector fell by 1.2 percent year-on-year in September after a contraction of 1.5 percent in August. The data shows a slower rate of contraction in credit lending but does not signal a strong recovery of credit in the eurozone. The data also confirmed that credit conditions remain particularly tight in the eurozone periphery.

Since banking credit is crucial to households and companies, credit conditions are intimately linked to Europe's economic recovery. The European Central Bank has recently approved a battery of measures, including negative interest rates and cheap loans for banks. However, as banks are still trying to clean up their balance sheets, lending remains timid. Even in those cases where banks are willing to lend, they tend to impose strict conditions that are hard for customers to meet. There is also a demand problem. With weak economic activity and high unemployment in the European periphery, many households and companies are simply not asking for credit.

Finally, the central bank's latest policies have created significant disagreement within the institution. Some members of the governing council -- most notably Germany's Bundesbank -- are wary of measures that could finance governments and weaken the pace of economic reforms. The Germans are also concerned about the legality of measures such as quantitative easing and its potential impact on inflation.

The current frictions within the central bank are representative of the wider debate that is taking place in Europe between countries led by Germany that believe reforms should come before stimulus packages, and those led by France that think crises are not the best time to apply deep spending cuts. In the coming weeks and months, this debate will be key in deciding the future of the European Union.

This analysis was just a fraction of what our Members enjoy, Click Here to start your Free Membership Trial Today! "This report is republished with permission of STRATFOR"

© Copyright 2014 Stratfor. All rights reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis.

STRATFOR Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.