The Better Short: Gold or Silver?

Commodities / Gold and Silver 2014 Oct 23, 2014 - 10:45 AM GMTBy: Bob_Kirtley

The fundamentals for the precious metals are weak. This has been highlighted in recent weeks by the lack of a major rally in gold and the losses in silver despite a spike in volatility to its highest since 2011. Improving economic data, the tapering of QE, and discussion of when the first rate hike will be have resulted in heavy losses over the past two years in the precious metals, and are to blame for the poor performance in the recent risk off market conditions stemming from the Ebola fears.

The fundamentals for the precious metals are weak. This has been highlighted in recent weeks by the lack of a major rally in gold and the losses in silver despite a spike in volatility to its highest since 2011. Improving economic data, the tapering of QE, and discussion of when the first rate hike will be have resulted in heavy losses over the past two years in the precious metals, and are to blame for the poor performance in the recent risk off market conditions stemming from the Ebola fears.

These overwhelmingly bearish fundamentals are the reason that we have taken short positions on the precious metals sector and why we intend to continue to do so. However, while both gold and silver offer attractive levels for new shorts, which metal holds the better risk reward dynamics in the current market situation? To answer this we must consider how each metal behaves and performs during both risk off and on conditions, as well as their current technical situations.

Given the recent turmoil in the markets, we will first look at how gold and silver have performed historically in other recent risk off situations and why this occurs. During August 2008 and the start of the GFC both took heavy losses alongside industrial metals. Proportionally, silver lost more than twice as much as gold in August as both were sold off.

A bounce in gold caused largely by safe haven buying pulled silver higher, but as silver is not a safe haven asset this relief was brief. Both metals fell significantly following this, yet the losses in silver were much more severe as it also suffered from a selloff of the industrial metals (represented by the ETF DBB and copper) and continued to move with them until mid-November as the risk off tone prevailed. By this point silver had lost 55.65% since the beginning of August while gold was down only 23.59%.

Moving forward to 2010 we will look the debt crisis in Greece that lead to another risk off situation in the markets. Following the Greek bailout there were only three trading days that saw gains in silver being greater than those of gold. Risk off sentiment followed these to show losses of 21.13% in base metals between the beginning of May early and June. This major selloff dragged silver down as an “industrial metal” by 7.19% at one point, whilst gold rallied more than 5%.

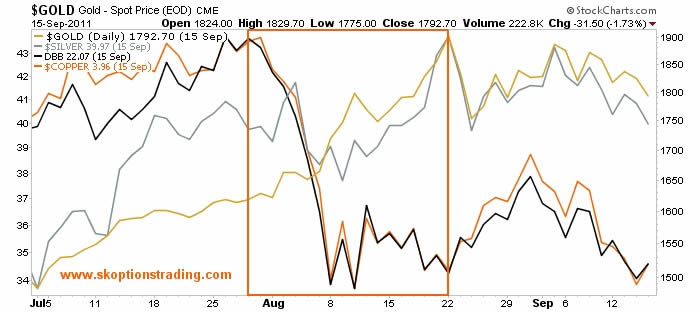

A similar situation occurred in the summer of 2011 when gold was making all-time highs. The Eurozone crisis caused fears of poorer economic performance to spike, and consequently the industrial metals lost 13.28% by August 10th, while safe haven buying in gold led to a rally of more than 10%. The lack of safe haven buying and the effect of the base metal selloff was that gains in silver were reduced to only 4.14% in August, which was almost a third of those in gold.

What we can take from this is that although gold and silver have a strong relationship, both perform differently during risk off periods. In the GFC gold’s losses were lessened as safe haven buying slowed the decline and caused the metal to bounce. In the Greek and later Eurozone crises gold again performed well as a result of safe haven demand, making all-time highs in 2010 and breaking them in 2011.

However, silver did not have the benefit of being a safe haven asset to drive it higher during risk off periods, and still does not. In fact, silver suffered from the risk off tone in the markets as industrial metals were heavily sold. This means that in future risk off situations silver is likely to underperform gold as it behaves as a hybrid of base and precious metals, rather than a pure safe haven asset, making it the better short.

What happens to precious metals in a risk on situation?

If the Ebola panic dissipates quickly, the effect on confidence levels and the economy as a whole will be minimal. Thus economic data would continue to improve and allow the Fed to hike in 2015. Given that gold is a function of monetary policy and that silver has a strong relationship with the yellow metal, this situation is highly bearish for both.

Since 2013 economic conditions have been improving and as a result markets have enjoyed a relatively consistent and continued risk on tone. Considering how gold and silver performed relative to each other over that time is an indicator of how they are likely to perform in future risk on situations.

As the above graph shows, during the significant risk off periods since 2013 silver has not performed as a safe haven asset that was bought, but as an industrial metal that was sold; each time silver lost ground while gold traded at least 2% better.

Throughout periods of risk on market conditions since 2013 there were only three periods when silver rallied significantly more than gold. The first of these was August 2013 when the markets began to price out a taper from the Fed in September. This led to a rally in both gold and copper with silver gaining the most at a peak 24.02%.

Silver next outperformed gold when it rallied 13.73% as emerging markets woes waned and the Ukraine situation began to escalate. These respectively resulted in increased growth expectations that caused a rally of 3.38% in copper, and safe haven buying in gold that pushed the metal 5.19% higher.

The most recent incident was in the second half of June this year after the ECB cut rates to historic lows and concerns as to growth in China subsided. This led to a significant rally in both the industrial and precious metals with copper gaining 5.52% and gold 5.24%, these combined to push silver higher by just less than double as it rallied 9.88%.

This tells us that through risk on market conditions silver is only likely to outperform gold in situations where both the industrial and precious metals rally, which are few, far between, and short lived. Therefore it is clear that in risk on market situations silver is still a better short than gold, as its vulnerability to losses in the industrial metals make it likely to underperformance gold.

Silver is potentially a better short in both risk off and on situations, but is it a better short right now?

A risk off tone is currently present in the markets while Ebola fears remain prevalent. We have established that in these situations silver behaves more similar to industrial metals than to the safe haven assets, such as gold. Since the market became “risk off” the base metals have been sold, thus it is likely that silver will decline as one of them. Additionally, if sentiment improves, silver is likely to underperform gold as safe haven buying will be reversed, putting negative pressure on gold that will drag silver lower. Therefore, silver is more likely to fall, and by a greater degree from this perspective.

However, one must also consider the technical factors for both metals and how these will effect movement going forward. The MACD’s for both underwent a sub-zero positive crossover in early October, which has provided positive pressure that has clearly been more prevalent in gold than silver. This means that crossover is likely to continue to have a lesser effect in silver, which makes it weaker by this indicator.

In terms of support levels, gold has gained the level of $1220 and the recent downtrend, broken earlier this month, to slow a decline if market conditions move back towards risk on. However, silver has very little in the way of support near the current price. The closest major level from here is $17.50 and that will act as resistance to slow a rally, as will the now near impenetrable level of $19. Silver has also failed challenge the recent downtrend to make any significant gains.

In addition, the RSI in gold has moved and stayed above 50 while silver’s flutters around the 40 mark. This indicates that gold is stronger, which makes a decline more likely to occur in silver.

Therefore, the current technical situation and trend in the industrial metals indicate that silver is likely to underperform gold whether Ebola fears are dispelled or not, that is, if the market sentiment remains risk off or becomes risk on again.

Should the Ebola situation escalate and the markets continue to react negatively, gold is likely to behave as a safe have asset while silver will continue to behave as an industrial metal. In this case a short on silver is more likely to be profitable as the industrials are likely to decline a drag silver down, and if silver is pulled higher by gold these gains are likely to be lessened, meaning that a short trade would show smaller losses.

If panic leaves the market, then it is likely that economic conditions will continue to improve and that the Fed will hike next year. This would be highly bearish for gold, and thus cause silver decline as well. As we have shown, in a risk on market situation as this would be, silver underperforms gold.

Thus a silver short is likely to result in higher gains than a gold short. In the event that safe haven buying in gold flows through to silver the selling in the industrial metals would lessen the gains made, meaning silver short is has a smaller potential drawdown. Accordingly, the risk reward dynamics are more favourable for a short on silver than they are on gold, which makes shorting silver the better trade.

As the situation changes we will continue to use analysis such as this to take positions on the market as we have done in the past to generate our 932.79% return since inception. To find out the specifics of these trades or for further market analysis, all you need to do is become a member of our service by signing up below.

Subscribe for 6 months - $499

Go gently.

Bob Kirtley

Email:bob@gold-prices.biz

URL: www.silver-prices.net

URL: www.skoptionstrading.com

To stay updated on our market commentary, which gold stocks we are buying and why, please subscribe to The Gold Prices Newsletter, completely FREE of charge. Simply click here and enter your email address. Winners of the GoldDrivers Stock Picking Competition 200

DISCLAIMER : Gold Prices makes no guarantee or warranty on the accuracy or completeness of the data provided on this site. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This website represents our views and nothing more than that. Always consult your registered advisor to assist you with your investments. We accept no liability for any loss arising from the use of the data contained on this website. We may or may not hold a position in these securities at any given time and reserve the right to buy and sell as we think fit.

Bob Kirtley Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.