Germany Fights on Two Fronts to Preserve the Eurozone

Politics / Germany Sep 30, 2014 - 02:04 PM GMTBy: STRATFOR

The European Court of Justice announced Sept. 22 that hearings in the case against the European Central Bank's (ECB) bond-buying scheme known as Outright Monetary Transactions (OMT) will begin Oct. 14. Though the process is likely to be lengthy, with a judgment not due until mid-2015, the ruling will have serious implications for Germany's relationship with the rest of the eurozone. The timing could hardly be worse, coming as an anti-euro party has recently been making strides in the German political scene, steadily undermining the government's room for maneuver.

The European Court of Justice announced Sept. 22 that hearings in the case against the European Central Bank's (ECB) bond-buying scheme known as Outright Monetary Transactions (OMT) will begin Oct. 14. Though the process is likely to be lengthy, with a judgment not due until mid-2015, the ruling will have serious implications for Germany's relationship with the rest of the eurozone. The timing could hardly be worse, coming as an anti-euro party has recently been making strides in the German political scene, steadily undermining the government's room for maneuver.

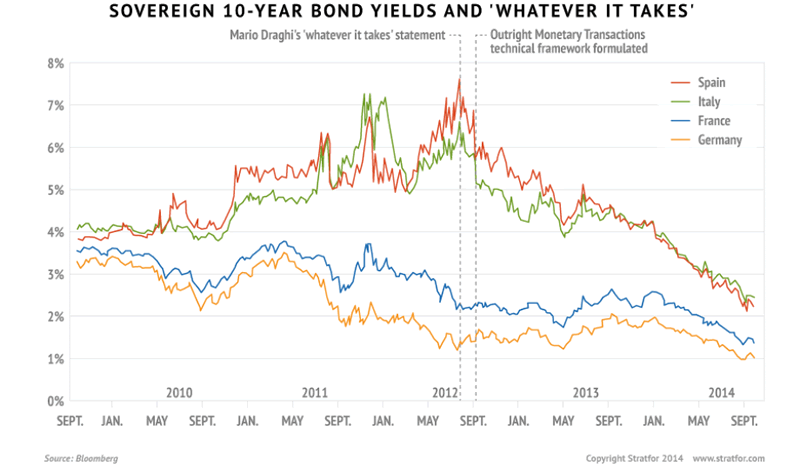

The roots of the case go back to late 2011, when Italian and Spanish sovereign bond yields were following their Greek counterparts to sky-high levels as the markets showed that they had lost confidence in the eurozone's most troubled economies' ability to turn themselves around. By summer 2012 the situation in Europe was desperate. Bailouts had been undertaken in Greece, Ireland and Portugal, while Italy was getting dangerously close to needing one. But Italy's economy, and particularly its gargantuan levels of government debt, meant that it would be too big to receive similar treatment. In any event, the previous bailouts were not calming financial markets.

As Spain and Italy's bond yields lurched around the 7 percent mark, considered the point where default becomes inevitable, the new president of the European Central Bank, Mario Draghi, said that the ECB was willing to do whatever it took to save the euro. In concert with the heads of the European governments, the ECB developed a mechanism that enables it to buy unlimited numbers of sovereign bonds to stabilize a member country, a weapon large enough to cow bond traders.

ECB President Mario Draghi never actually had to step in because the promise of intervention in bond markets convinced investors that eurozone countries would not be allowed to default. But Draghi's solution was not to everyone's taste. Notable opponents included Jens Weidmann, president of the German Bundesbank. Along with many Germans, Weidmann felt the ECB was overstepping its jurisdictional boundaries, since EU treaties bar the bank from financing member states. Worse, were OMT ever actually used, it essentially would be spending German money to bail out what many Germans considered profligate Southern Europeans.

In early 2013, a group of economics and constitutional law professors from German universities collected some 35,000 signatures and brought OMT before the German Constitutional Court. During a hearing in June 2013, Weidmann testified for the prosecution. In February 2014, the court delivered an unexpected verdict, ruling 6-2 that the central bank had in fact overstepped its boundaries, though it also referred the matter to the European Court of Justice. Recognizing the profound importance of this issue, the court acknowledged that a more restrictive interpretation of OMT by the European Court of Justice could make it legal.

The German judgment suggested that three alterations to OMT would satisfy the Constitutional Court that the mechanism was lawful. Two of the three changes, however, are problematic at best. One alteration would limit the ECB to senior debt, a change that would protect it against the default of the sovereign in question but also risk undermining the confidence of other investors who would not be similarly protected. The second alteration would make bond buying no longer "unlimited," constraining the bank's ability to intimidate bond traders by leaving it with a rifle instead of a bazooka.

A New German Political Party

The group of academics who organized the petition kept busy while the court deliberated. The Alternative for Germany, a party founded in February 2013 by one of their number, economics professor Bernd Lucke, and frequently known by its German acronym, AfD, has made significant gains in elections across Germany. Founded as an anti-euro party, the party came very close to winning a seat in the Bundestag, the lower house of the German parliament, in the September 2013 general elections, a remarkable feat for a party founded just six months before. It made even larger gains in 2014, winning 7.1 percent of the vote in European Parliament elections in May and between 9.7 and 12.2 percent in three regional elections in August and September.

Germany is currently ruled by a grand coalition, with German Chancellor Angela Merkel's center-right Christian Democratic Union party (and its sister party, the Bavaria-based Christian Social Union) sharing power with the center-left Social Democratic Party. This has resulted in the Christian Democratic Union being dragged further to the center than it wanted to be, creating a space to its right that the Alternative for Germany nimbly entered.

Originally a single-issue party, the Alternative for Germany has begun espousing conservative values and anti-immigration policies, a tactic that worked particularly well in elections held in eastern Germany in the summer. Its rise puts Merkel, a European integrationist, in a quandary that will become particularly acute if the Alternative for Germany proves capable of representing Germans uncomfortable with the idea of the country financially supporting the rest of Europe.

Since the beginning of the European crisis, Merkel has proved masterful at crafting a message that combines criticism of countries in the European periphery with the defense of bailout programs for those same countries. But while Merkel has become accustomed to criticism from left-wing parties over the harsh austerity measures the European Union demanded in exchange for bailouts, she had not counted on anti-euro forces mounting serious opposition in Germany. Merkel is not alone in this, of course: center-right parties across Europe, from David Cameron's coalition in the United Kingdom to Mark Rutte's People's Party for Freedom and Democracy in the Netherlands, have seen Euroskeptical populism emerge to their right, eating into their traditional voter platforms.

This anti-ECB sentiment in Germany has swelled during 2014, as Draghi's attempts to increase the eurozone's low inflation have departed further and further from economic orthodoxy. German conservatives have greeted each new policy with displeasure. The German media has called negative interest rates "penalty rates," claiming they redistribute billions of euros from German savers to Southern European spenders. On Sept. 25, German Finance Minister Wolfgang Schauble spoke in the Bundestag of his displeasure with Draghi's program to buy asset-backed securities. Judging from the German hostility to even "quantitative easing-lite" measures, the ECB's attempts to rope Germany into further stimulus measures could prove troublesome indeed.

Institutional and Political Challenges for Berlin

All of the measures the ECB has announced so far, however, are mere appetizers. Financial markets have been demanding quantitative easing, a broad-based program of buying sovereign bonds in order to inject a large quantity of money into the market. Up to this stage, three major impediments have existed to such a policy: the German government's ideological aversion to spending taxpayers' money on peripheral economies; the political conception that quantitative easing would ease the pressure on peripheral economies to reform; and the court case that has been hanging over OMT (the only existing mechanism available to the ECB for undertaking sovereign bond purchases). Notably, the OMT in its original guise and quantitative easing are not precisely the same thing. In the original conception of OMT, the ECB would offset any purchases in full by taking an equivalent amount of money out of circulation, (i.e., not increasing the money supply itself). Nonetheless, any declaration that OMT is illegal would severely inhibit Draghi's room for maneuver should he wish to undertake full quantitative easing.

This confluence of events leaves Merkel nervously awaiting the decision of the European Court of Justice. In truth, she is in a no-win situation. If the Luxembourg court holds OMT illegal, Draghi's promise would be weakened, removing the force that has kept many sovereign bond yields at artificially low levels and permitting the desperate days of 2011-2012 to surge back. If the European Court of Justice takes up the German court's three suggestions and undercuts OMT to the extent that the market deems it to be of little consequence, the same outcome could occur. And if the European Court of Justice rules that OMT is legal, a sizable inhibitor to quantitative easing will have been removed, and the possibility of a fully fledged bond-buying campaign will loom ever closer, much to the chagrin of the German voter and to the political gain of the Alternative for Germany.

When analyzing the significance of this case, it is important to bear in mind that Germany is an export-driven power that must find markets for its exports to preserve cohesion and social stability at home. The eurozone helps Germany significantly — 40 percent of German exports go to the eurozone and 60 percent to the full European Union — because it traps its main European customers within the same currency union, depriving them of the possibility of devaluing their currencies to become more competitive.

Since the beginning of the crisis, Germany has managed to keep the eurozone alive without substantially compromising its national wealth, but the moment will arrive when Germany must decide whether it is willing to sacrifice a larger part of its wealth to save its neighbors. Berlin has thus far been able to keep its own capital relatively free of the hungry mouths of the periphery, but the problem keeps returning. This puts Germany in a dilemma because two of its key imperatives are in contradiction. Will it save the eurozone to protect its exports, writing a big check as part of the deal? Or will it oppose the ECB moves, which if blocked could mean a return to dangerously high bond yields and the return of rumors of Greece, Italy and others leaving the currency union?

The case will prove key to Europe's future for even deeper reasons. The European crisis is generating deep frictions in the Franco-German alliance, the main pillar of the union. The contrast between Germany, which has low unemployment and modest economic growth, and France, which has high unemployment and no growth, is becoming increasingly difficult to hide. In the coming months, this division will continue to widen, and Paris will become even more vocal in its demands for more action by the ECB, more EU spending and more measures in Germany to boost domestic investment and public consumption.

This creates yet another dilemma for Berlin, since many of the demands coming from west of the Rhine are deeply unpopular with German voters. But the German government understands that high unemployment and low economic growth in Europe are leading to a rise in anti-euro and anti-establishment parties. The rise of the National Front in France is the clearest example of this trend. There is a growing consensus among German political elites that unless Berlin makes some concessions to Paris, it could have to deal with a more radicalized French government down the road. The irony is that even if Berlin were inclined to bend to French wishes, it would find itself constrained by institutional forces beyond its control, such as the Constitutional Court.

Germany has managed to avoid most of these questions so far, but these issues will not got away and in fact will define Europe in 2015; the Alternative for Germany, for example, is here to stay. Meanwhile, the Constitutional Court will keep challenging EU attempts at federalization even if this specific crisis is averted, and the Bundesbank and conservative academic circles will keep criticizing every measure that would reduce German sovereignty to help France or Italy. Though it is impossible to predict the European Court of Justice's final ruling, either way, the dilemma will continue to plague an increasingly fragile European Union.

By Adriano Bosoni and Mark Fleming-Williams

Editor's Note: Writing in George Friedman's stead this week are Stratfor Europe Analyst Adriano Bosoni and Economy Analyst Mark Fleming-Williams.

"Germany Fights on Two Fronts to Preserve the Eurozone is republished with permission of Stratfor."

This analysis was just a fraction of what our Members enjoy, Click Here to start your Free Membership Trial Today! "This report is republished with permission of STRATFOR"

© Copyright 2014 Stratfor. All rights reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis.

STRATFOR Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.